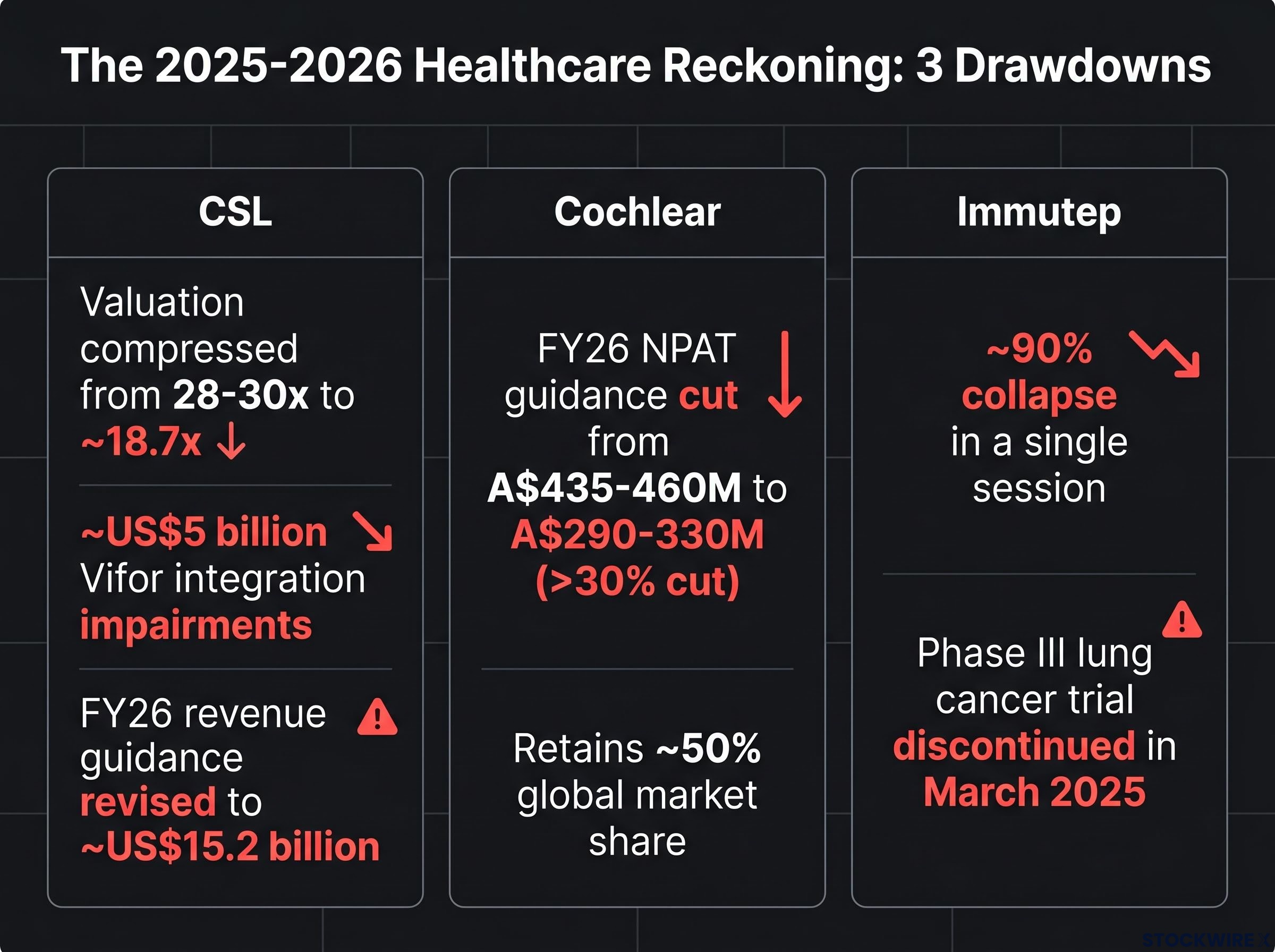

When Cochlear posted one of the worst guidance cuts in its listed history, the share price fell further in a single session than it had on any day on record. The company remained profitable, globally dominant, and structurally intact. It did not matter. The 2025-2026 period has forced a reckoning for retail investors who treated ASX healthcare stocks as a defensive sleeve. CSL reached a decade-low after slashing multi-year growth projections. Cochlear’s FY26 earnings guidance was cut by more than 30%. Immutep collapsed approximately 90% in a single day after its lead Phase III trial was discontinued. These events did not happen to failing businesses or speculative penny stocks. They happened to some of the most widely held, professionally researched names on the ASX. What follows unpacks what actually drove each of these drawdowns, why the market reacted as severely as it did, and what the pattern across all three cases teaches investors about assessing downside risk in healthcare before it arrives.

CSL’s decade-long de-rating shows what happens when a premium valuation meets compounding disappointment

CSL shares had made no meaningful price progress over approximately four years before the acute selloff began. That stagnation was not inertia; it was a slow erosion of confidence that the market eventually priced all at once.

The sequence of disappointments compounded across multiple reporting periods:

- The Vifor integration produced approximately US$5 billion in impairments and failed to deliver the margin uplift the acquisition thesis required

- China albumin pricing deteriorated, pressuring a geography that had supported growth for years

- The Seqirus vaccines unit delivered weaker-than-expected revenue in H1 FY25, contributing to a miss on consensus EBIT and NPAT

- A cardiovascular drug candidate failed its clinical trial, extending execution concerns beyond the plasma franchise

- A CEO transition and broader restructuring were announced alongside the impairment disclosure

In October 2025, CSL cut its multi-year growth projections covering FY26 through FY28. FY26 revenue guidance was subsequently revised to approximately US$15.2 billion, according to analyst estimates. The share price reached a 10-year low.

Why the size of the drawdown is a valuation story, not just a business story

Each of those individual setbacks was, on its own, arguably forgivable for a business of CSL’s scale and franchise quality. Together, they were not, because CSL’s starting valuation left no room for any of them.

A stock trading at 28-30x earnings that re-rates to approximately 18.7x, according to analyst estimates, while earnings expectations are simultaneously cut creates a double-hit: the numerator falls and the denominator compresses at the same time. The arithmetic of that compression at scale is what explains a drawdown far larger than any single guidance miss would suggest.

The mechanism is valuation, not business quality. CSL remains a large, profitable global plasma and vaccines franchise. The damage came from paying a price that required flawless mid-teens growth, and then watching that growth fail to materialise across four consecutive years.

The compression CSL experienced from roughly 28-30x to approximately 18.7x is a textbook illustration of why a margin of safety matters in practice: investors who required a meaningful discount to intrinsic value before entering would have needed the stock to trade at a substantially lower multiple before committing capital, which the market never offered during the growth years.

When big ASX news breaks, our subscribers know first

What CSL, Cochlear, and Immutep actually are, and why the label “healthcare” obscures more than it reveals

The word “healthcare” groups together businesses with fundamentally incompatible risk profiles. CSL and Cochlear fail via earnings downgrades and multiple compression, a slow grind that plays out across quarters. Immutep fails via a single trial announcement in a single day. These are not variations of the same risk. They are different categories of risk wearing the same sector label.

| Company Type | Examples | Main Risks | Typical Failure Mode |

|---|---|---|---|

| Established commercial healthcare | CSL, Cochlear | Valuation, guidance, macro, competition | Multiple compression plus earnings downgrades over quarters |

| Device/services with disruption risk | ResMed | New therapies (e.g. GLP-1), pricing pressure | Slower growth and prolonged de-rating, not binary |

| Clinical-stage biotech | Immutep | Binary clinical outcomes, funding, regulatory | Single announcement can erase the majority of equity value |

Immutep fell approximately 90% in a single session following Phase III lung cancer trial discontinuation in March 2025. Cochlear holds an estimated 50% global market share in cochlear implants with only approximately 3% penetration of an addressable market exceeding 6 million people in developed markets. An April 2025 assessment examined tariff exposure across CSL, ResMed, Cochlear, and Ansell. These companies share a sector classification but not a risk profile, and investors who treat them interchangeably will systematically misprice their downside.

Understanding guidance risk: why premium healthcare companies get punished so harshly for missing expectations

Premium healthcare compounders are priced for reliability. Their valuations embed an assumption that earnings will compound at a steady, above-market rate for many years into the future. When that assumption is questioned, both the earnings estimate and the multiple applied to those earnings fall at the same time.

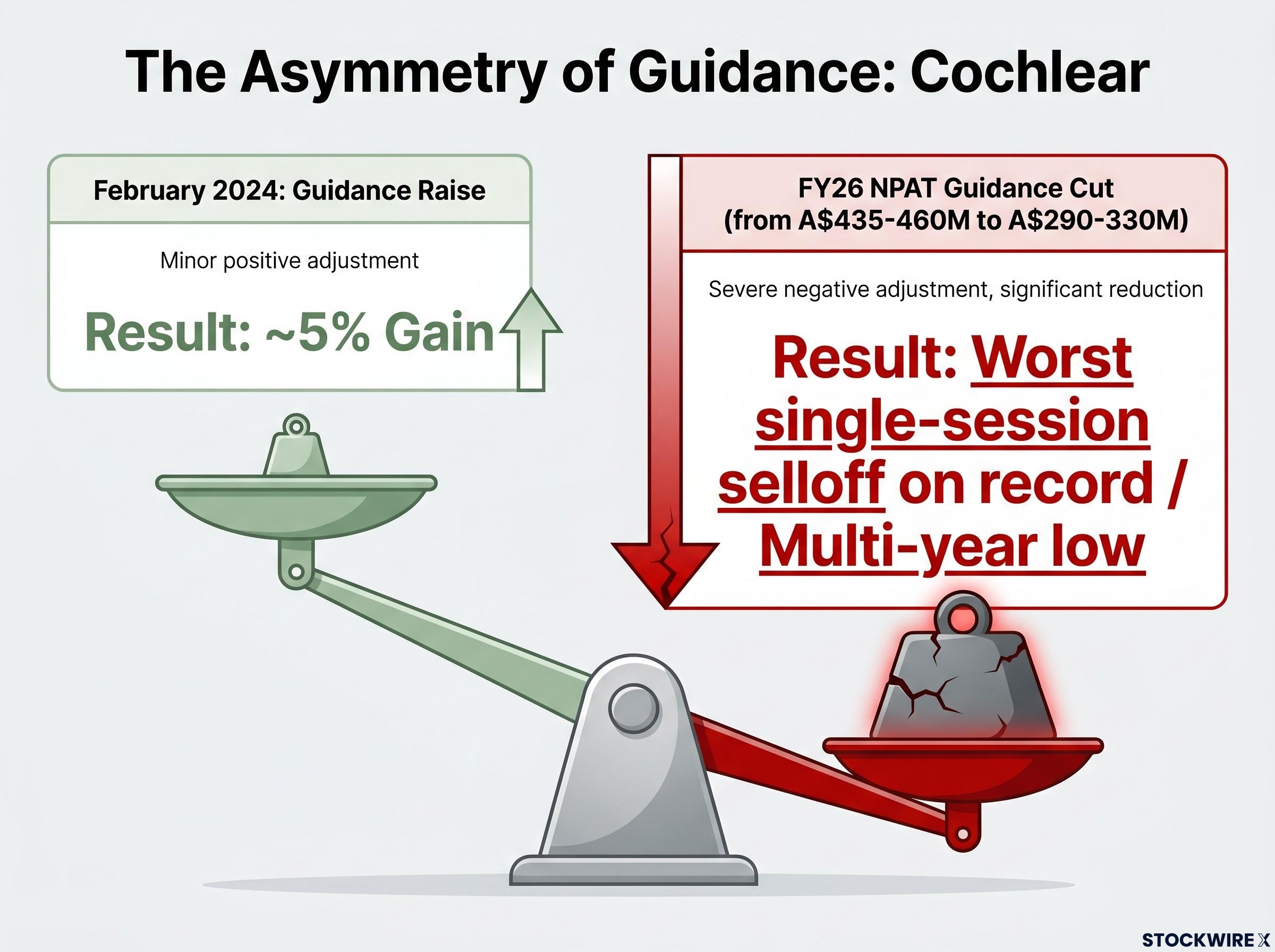

The asymmetry is measurable. In February 2024, Cochlear raised FY24 guidance. Shares responded with an approximately 5% gain. When Cochlear subsequently cut FY26 underlying NPAT guidance from A$435-460 million to A$290-330 million, one of the worst earnings cuts in the company’s listed history, the stock suffered its worst single-session selloff on record and fell to a multi-year low.

ASX continuous disclosure obligations under Listing Rule 3.1 require listed companies to disclose information that a reasonable person would expect to have a material effect on price, which means a guidance cut of the magnitude Cochlear delivered cannot be deferred or softened through selective timing.

A guidance upgrade produced low single-digit upside. A single severe downgrade produced a share price low not seen in over a decade. That asymmetry is not irrational. It is the rational consequence of pricing an asset whose value is almost entirely in the long-duration tail of future earnings.

The drivers of Cochlear’s downgrade were a mix of operational and macro causes:

- Hospital capacity constraints reducing patient referrals

- Middle East disruptions delaying surgeries and shifting demand patterns

- US cost-of-living pressures leading some patients to treat cochlear implants as discretionary

Understanding this mechanism before holding a premium compounder into a results season changes the question from “will guidance be fine?” to “what is my actual downside if it is not?” The second question is far more useful.

Why clinical-stage biotech sits in a risk category of its own: the Immutep case study

Immutep’s share price fell approximately 90% following the discontinuation of its Phase III lung cancer trial in March 2025. That figure deserves to sit on its own for a moment, because it describes not an outlier but the mathematically expected outcome when a single late-stage asset represents the majority of a company’s equity value.

A clinical-stage biotech is not a commercial business with recurring earnings. It is a bundle of probability-weighted options on drug outcomes. The equity value is concentrated in whichever asset is closest to regulatory approval, and when that asset fails, the value it represented disappears.

BIO clinical development success rates covering 2011-2020 show that Phase III oncology trials face among the lowest transition-to-approval probabilities of any therapeutic area, quantifying the structural risk that makes a single late-stage asset failure so consequential for a clinical-stage biotech’s equity value.

After the Phase III discontinuation, what remained of Immutep was:

- Cash on hand

- Early-stage pipeline assets with far lower probability-adjusted value

What was lost:

- The dominant value driver for the entire equity

- The investor narrative that justified the position and the share price

The contrast with CSL and Cochlear is structural. Commercial compounders experience painful but survivable drawdowns driven by guidance and valuation. Clinical-stage biotech can experience investment-case extinction in a single announcement.

What is left after a Phase III failure, and what the rebuilding path looks like

What typically survives a Phase III failure is a cash reserve, a management team seeking a new lead asset, and earlier-stage pipeline candidates with lower probability-adjusted value. The rebuilding path is long and uncertain. Investors entering after such a collapse should treat the position as a speculative bet on the early-stage pipeline, not a recovery of the original thesis. Position sizing in clinical-stage names must account explicitly for the possibility that a 70-90% loss is a realistic outcome for any individual holding.

For investors who understand the binary risk category and want to assess specific names with defined inflection points, our deep-dive into ASX biotech binary catalysts for 2026 examines Dimerix and Paradigm Biopharma, covering funded runways, regulatory precedent from the April 2026 sparsentan approval, and the position-sizing discipline required when a single trial result can move a stock by 70-90% in either direction.

Macro forces that hit ASX healthcare from outside the annual report

Even investors who correctly assess company-level fundamentals can be wrong-footed by forces that have nothing to do with the company itself.

Rising bond yields compress valuations for long-duration growth assets. Healthcare compounders are priced on future cash flows many years out, making their present value acutely sensitive to the discount rate applied. The Australian healthcare sector touched 8-year lows at points during the 2025-2026 period, according to market analysis, illustrating how sector-wide selloffs amplify company-specific bad news.

The macro risk categories extend beyond rates:

- Interest rate sensitivity: Rising yields compress multiples across the sector, regardless of individual company performance

- US tariff exposure: An April 2025 assessment identified tariff-related risk for CSL, ResMed, Cochlear, and Ansell, adding a policy-uncertainty layer

- Geopolitical disruption: Middle East conflict directly affected Cochlear’s surgical volumes and demand patterns

- Narrative risk: ResMed’s 2026 selloff was driven in part by the perception that GLP-1 obesity drugs could reduce sleep apnoea prevalence, even where company data showed CPAP adherence remained strong

Holding concentrated positions in global healthcare exporters is partly a macro bet, on interest rate direction, US trade policy, and geopolitical stability, not just a stock-picking decision.

US structural policy shifts represent a meaningfully different category of risk from the cyclical headwinds discussed here: FDA approval instability and the RFK Jr.-led reorientation away from infectious disease prevention carry no natural reversal point, meaning CSL’s Seqirus vaccine franchise faces a form of risk that neither rate normalisation nor AUD depreciation will resolve.

Five questions every investor should ask before sizing a healthcare position

The three case studies above produce a consistent set of pre-investment questions. These are framed as questions rather than rules, because the goal is genuine reflection on actual portfolio risk rather than mechanical checklist-ticking.

- What growth path does the current price imply, and is it realistic? CSL’s historical multiple of 28-30x required flawless mid-teens earnings growth. When that growth failed to materialise, the compression to approximately 18.7x (per analyst estimates) produced a drawdown far larger than the underlying earnings miss.

- Is the downside a slow grind or a binary event? Cochlear’s selloff played out across quarters of deteriorating guidance. Immutep’s 90% decline occurred in a single session. Position sizing should reflect which type of risk is being taken.

- How concentrated is the thesis in a single asset, trial, or geography? CSL’s China albumin exposure and the Vifor acquisition drove compounding guidance downgrades. Immutep’s entire equity value rested on one Phase III programme. Concentration magnifies both upside and downside.

- What is the historical pattern of market reaction to news, both positive and negative? Cochlear’s FY24 guidance raise produced approximately 5% upside. Its guidance cut produced the worst single-session selloff in the company’s history. Asymmetry of this magnitude should inform position sizing before results season, not after.

- What macro exposures come with the position? Rates, tariffs, geopolitical disruption, and narrative risk from adjacent therapeutic categories all affected ASX healthcare names during the 2025-2026 period. A concentrated healthcare position is also, whether the investor intends it or not, a macro bet.

Healthcare’s “defensive” reputation has a price, and recent years show what it costs when investors overpay for it

The common thread across CSL, Cochlear, and Immutep is not that these were bad businesses. CSL remains a global plasma franchise of genuine scale. Cochlear holds an estimated 50% global market share with only approximately 3% penetration of a large addressable market. Even Immutep’s science was credible enough to reach Phase III.

The damage was caused by a combination of premium valuations that required flawless execution, false assumptions about the consistency of earnings delivery, and failure to account for macro and clinical risks that sit outside the annual report. The “defensive” label was not wrong in the sense that healthcare demand is structurally supported by ageing demographics and underpenetrated markets. It was dangerously incomplete, and the cost of treating it as complete has been measurable and painful across several of the ASX’s most respected names.

CSL’s compression from 28-30x to approximately 18.7x illustrates that the same business can be a poor or a potentially interesting investment depending purely on entry price. Immutep serves as a reminder that one end of the healthcare spectrum offers no defensive qualities whatsoever.

The issue is not healthcare as a sector. It is healthcare as a label that investors have historically used to justify overpaying and under-sizing the actual risk being taken.

The lesson is not to avoid healthcare. It is to enter at prices and position sizes that reflect the actual risk profile of each company type rather than the genre label. These are distinct analytical tasks, and the 2025-2026 period has made the cost of conflating them difficult to ignore.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections referenced in this article are subject to market conditions and various risk factors.