Why AI Makes Markets Safer Daily but Riskier in a Crisis

2 hrs ago

Two Wall Street calls landed within days of each other in early May 2026, and they pointed in opposite directions. William Blair and Cantor Fitzgerald downgraded HubSpot on 8 May despite a clean revenue beat, while Wolfe Research initiated Rubrik with an Outperform rating on 1 May despite a premium valuation that already prices in aggressive growth. The divergence is not noise. It is a signal about how sophisticated investors are differentiating within the software sector at a moment when artificial intelligence is simultaneously building new competitive moats and destabilising old ones. What follows is a walk through both calls, an explanation of what each analyst saw, and a reusable framework for evaluating whether a software company’s AI exposure is a structural tailwind or a near-term growth headwind.

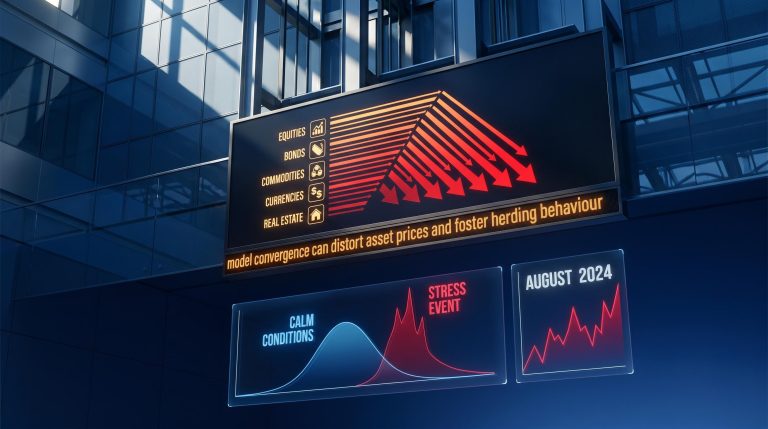

The Q1 numbers were genuinely strong. HubSpot reported revenue of $881M, up 23% year on year, clearing the $862.8M consensus estimate by a comfortable margin. Constant-currency revenue growth of 18% exceeded prior guidance of 16%. Operating margin came in at 17.8%, roughly 100 basis points above estimates.

None of that saved the stock from two downgrades in a single session.

The issue was not what HubSpot delivered. It was what management signalled about the rest of the year. Cantor Fitzgerald’s team identified three specific concerns:

Cantor cut its price target to $580 from $650. William Blair moved to Market Perform without issuing a price target.

William Blair explicitly framed the downgrade not as a view of HubSpot as “an AI loser” but as a visibility call, with limited near-term catalysts to move shares out of a trading range.

That distinction matters. This was not a bearish thesis on HubSpot’s product. It was a statement about the gap between product capability and revenue visibility.

The analyst verdict reflects a company caught mid-transition, with real product momentum on one side and unresolved monetisation friction on the other.

HubSpot’s Spring Spotlight event on 29 April 2026 launched AI agents for sales automation. Early pilots demonstrated a 25% pipeline velocity boost. The 15 April Google Cloud partnership for AI embeddings expanded the platform’s technical reach. AI credit consumption grew 67% sequentially, a figure William Blair flagged as evidence that adoption is real.

JMP Securities maintained its Market Outperform rating with a $700 price target, citing 20% productivity gains in beta tests.

Zero revenue from AI agents was booked at Q1 earnings. The gap between adoption and monetisation is where the friction sits, and three specific factors explain it:

Morgan Stanley projects only 5-7% annual recurring revenue (ARR) uplift from AI agents in H2 2026, citing legacy CRM integration hurdles as the primary constraint.

The stock is not broken. The market simply cannot yet determine which side of the transition HubSpot will land on, and that uncertainty is what keeps the shares range-bound rather than re-rating higher.

Wolfe Research analyst Patrick O’Neil initiated coverage of Rubrik on 1 May 2026 with an Outperform rating and a $70 price target, built on a thesis that separates Rubrik from legacy backup vendors at a structural level. The distinction O’Neil identified: Zero Trust architecture and AI-native resilience versus legacy platforms that bolt on AI features after the fact.

NIST Special Publication 800-207 defines Zero Trust architecture as a paradigm that shifts security controls from static network perimeters to protecting individual resources, a foundational distinction that separates purpose-built platforms like Rubrik from legacy backup vendors that layer security features onto perimeter-dependent infrastructure.

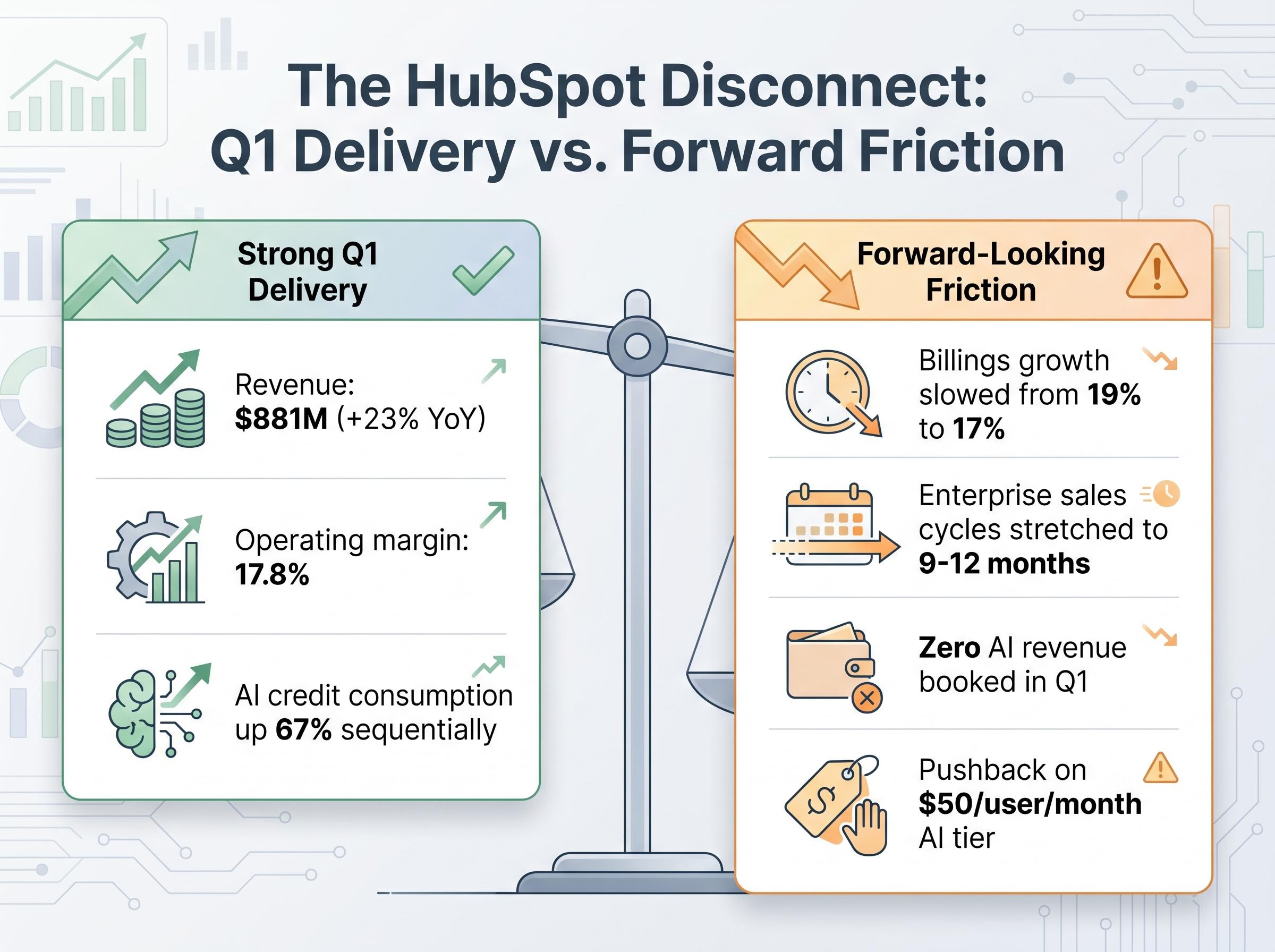

O’Neil projected 32% FY2027 subscription ARR growth, meaningfully ahead of Rubrik’s own guidance of approximately 25%. He valued the company at 7.5x CY2027 EV/Sales and 36x free cash flow, multiples that assume the growth premium is earned rather than aspirational.

The market responded. RBRK gained approximately 12% from its 7 May close through 10 May, with trading volume running roughly 2x the average.

The Identity Security segment adds a second growth vector. The business contributed approximately $30M in net new ARR in the prior year, with the potential to double. This is not a footnote; it is an expanding addressable market that legacy backup vendors do not compete in.

Wolfe Research characterised Rubrik as an “AI data security winner,” positioning it alongside CrowdStrike, Snowflake, and Datadog in the AI infrastructure tier.

The bull case is not unanimous. Jefferies initiated with a Hold rating and a $55 price target, citing competitive risk from CrowdStrike’s Velocity platform. That counterpoint is worth noting: Rubrik’s premium valuation leaves limited room for execution misses.

| Firm | Rating | Price Target | Key Thesis |

|---|---|---|---|

| Wolfe Research | Outperform | $70 | AI-native resilience; 32% FY2027 ARR growth; CrowdStrike gap in unstructured data |

| Piper Sandler | Overweight | $68 | Zero Trust edges Cohesity on AI workload recovery (sub-1 min vs. 5 min benchmarks) |

| Guggenheim | Buy | $72 | 40% gross margins from AI-orchestrated backups; multi-cloud security moat |

| Jefferies | Hold | $55 | Competitive risk from CrowdStrike’s Velocity platform; acknowledged 25% YoY ARR acceleration |

The HubSpot and Rubrik cases illustrate a distinction that Wall Street is pricing in real time, and understanding it provides a reusable lens for evaluating AI-related software stocks more broadly.

An AI-native company is one whose core architecture was built around AI from the outset. Rubrik’s Zero Trust data security platform is an example: AI orchestrates backup, recovery, and threat detection as foundational functions, not add-ons. Buyers deploy it specifically for those AI-driven capabilities.

An AI-adjacent company is one that adds AI features to an existing product. HubSpot’s CRM platform now includes AI agents for sales automation, but the core product predates those features. Buyers adopted HubSpot for its CRM functionality; the AI layer is an upsell, and an elective one at that.

The distinction between surface-level and infrastructure-level enterprise AI adoption explains much of the HubSpot dynamic: research from Gartner, McKinsey, and Forrester converges on a projection that infrastructure-level adopters will achieve roughly 3x the ROI of surface-level counterparts by 2027, a gap that mirrors the valuation spread Wall Street is already pricing between AI-native and AI-adjacent software vendors.

The difference matters because security spending is non-discretionary (companies must protect their data), while CRM AI is deferrable (companies can delay adopting a sales automation agent without immediate operational risk).

Overall software budgets remain relatively flat at approximately 8.5% of total IT spend. Within that flat envelope, security and AI-specific sub-allocations are growing at roughly 20%. Capital is not expanding for software broadly; it is reallocating toward security and AI infrastructure at the expense of application-layer tools.

Wellington Management observed on 10 May that sales cycles elongate 20-30% when AI features are added to legacy software. AI-native platforms bypass that friction through greenfield deployment. Average enterprise software sales cycles now run approximately 10 months; AI-native vendors see pilot-to-close cycles roughly 35% faster.

Baillie Gifford, in its Q1 2026 letter released 2 May, cited Rubrik’s approximately 95% gross margins as justifying roughly 8x EV/ARR versus 5x for adjacent platforms.

| Category | AI-Native (e.g., Rubrik) | AI-Adjacent (e.g., HubSpot) |

|---|---|---|

| Valuation multiple range | ~16-22x FY2027 EV/Sales | ~10-14x FY2027 EV/Sales |

| ARR growth threshold for premium | 30%+ with 70%+ net retention | Greater than 25% demonstrated ARR growth |

| Sales cycle dynamics | ~35% faster pilot-to-close (greenfield) | 20-30% elongation (legacy integration) |

| Budget allocation trend | Security/AI sub-allocations growing ~20% | Flat overall software budgets (~8.5% of IT spend) |

The analyst calls establish a starting position. What follows determines whether those positions hold.

For HubSpot, three signals will validate or challenge the current consensus:

Gross retention remains in the high-80% range according to William Blair, providing a floor. Full-year guidance of $3.7B-$3.708B implies management expects acceleration in H2, though the guidance flow-through mechanics suggest that confidence is measured.

For Rubrik, two waypoints matter most:

A broader dynamic sits beneath both stocks. An estimated 60% of software deals currently bundle AI as a “free rider” rather than a monetised add-on, according to Evercore ISI framing. Legacy CRM vendors face an estimated 15% churn risk as enterprise buyers evaluate AI-native alternatives. AI monetisation across the software sector is broadly delayed to H2 2026 and H1 2027.

The churn risk for legacy CRM vendors is structural rather than cyclical: autonomous AI agents are systematically dismantling per-seat SaaS models by automating the human-driven workflows that historically justified per-user pricing, and enterprise buyers evaluating AI-native alternatives are increasingly framing a seat-count reduction as a feature rather than a trade-off.

The two calls, issued within the same week and touching the same AI theme, arrive at opposite conclusions because they evaluate companies occupying different positions in the software stack. Where a company sits in that stack determines whether AI accelerates or complicates its path to monetisation.

Goldman Sachs has noted that AI-adjacent multiples face derating risk on monetisation delays, while AI-native platforms hold approximately 20% valuation premiums due to defensibility. Rubrik trades at roughly 18x FY2027 EV/Sales versus a sector average of approximately 14x. That premium is real, and it must be earned through execution at every quarterly report.

The genuine uncertainty in both cases deserves acknowledgement. HubSpot could re-accelerate faster than bears expect if Spring Spotlight’s AI agents gain enterprise traction in H2. Rubrik’s premium leaves limited margin for error; a single quarter of below-guidance ARR growth could compress the multiple sharply.

The discipline the pairing illustrates is straightforward. The question “does this company use AI?” is no longer sufficient. The question that separates productive analysis from surface-level screening is: “Is AI a structural moat for this specific business, or is it an integration project?”

Investors wanting to map the HubSpot and Rubrik cases onto the broader technology sector rotation will find our deep-dive into AI stock divergence in 2026, which examines how a 70-percentage-point performance gap opened between semiconductor equipment and software applications indices year-to-date, and identifies which categories of AI exposure are attracting capital versus shedding it.

KBW framed the divergence as “security as AI table stakes” versus an “elective CRM upsell,” a distinction that applies well beyond these two names and into every AI stock analysis an investor conducts from here.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including analyst price targets and growth projections, are subject to change based on market developments and company performance.

An AI-native company builds its core architecture around AI from the outset, meaning AI orchestrates foundational functions rather than acting as an add-on. An AI-adjacent company adds AI features to an existing product, making AI adoption an elective upsell rather than a core requirement for buyers.

William Blair and Cantor Fitzgerald downgraded HubSpot because management only flowed through about two-thirds of the Q1 beat into full-year guidance, constant-currency billings growth decelerated, and enterprise sales cycles have elongated, all of which reduce near-term revenue visibility despite the strong headline numbers.

Wolfe Research initiated Rubrik with an Outperform rating and a $70 price target, projecting 32% FY2027 subscription ARR growth based on the company's Zero Trust, AI-native architecture and an expanding Identity Security segment that legacy backup vendors do not compete in.

Overall software budgets remain relatively flat at around 8.5% of total IT spend, but security and AI-specific sub-allocations are growing at roughly 20%, meaning capital is reallocating from application-layer tools toward security and AI infrastructure rather than expanding broadly.

Investors should watch for AI agent revenue appearing in Q2 or Q3 results (zero was booked at Q1), a re-acceleration in constant-currency billings growth from the current 17% level, and whether the $50 per user per month AI pricing tier gains enterprise traction or requires restructuring.