Five AI infrastructure stocks doubled in value in the first five months of 2026, and none of them were the hyperscalers that dominated the investment conversation for most of the year. While Microsoft, Alphabet, Amazon, and Meta absorbed the bulk of institutional attention, the equity returns told a different story. Niche infrastructure providers in power generation and optical networking posted 90-130% revenue growth and outpaced even the Nasdaq-100 year-to-date. Several AI-focused exchange-traded funds (ETFs) captured the trend, raising a direct question for retail investors: is their AI exposure positioned where the returns are actually being generated? This analysis dissects the infrastructure-over-hyperscaler thesis using verified 2026 data, profiles two companies at the centre of the trade, explains the structural mechanics behind the outperformance, and provides a framework for evaluating whether AI infrastructure stocks belong in a portfolio.

The market signal hiding in plain sight: AI infrastructure is beating the index

The Nasdaq-100 is ahead of the S&P 500 year-to-date in 2026. That is a high baseline. What makes it worth pausing on is that several AI-focused ETFs are outpacing even the Nasdaq-100, according to analysis by Jennifer Saibil at The Motley Fool, published 17 May 2026.

Three ETFs in particular are leading the theme:

- Roundhill Generative AI and Technology ETF

- iShares U.S. Power and Infrastructure ETF

- Pacer Data and Infrastructure Real Estate ETF

Five highlighted AI infrastructure stocks each at least doubled in value within the first five months of 2026.

That is not a modest beat. It is a performance gap wide enough to suggest something structural is happening beneath the headline index numbers. The returns are not coming from the companies building AI. They are coming from the companies those builders cannot operate without.

The question is why, and whether the pattern has a framework investors can apply going forward rather than simply chasing it in hindsight.

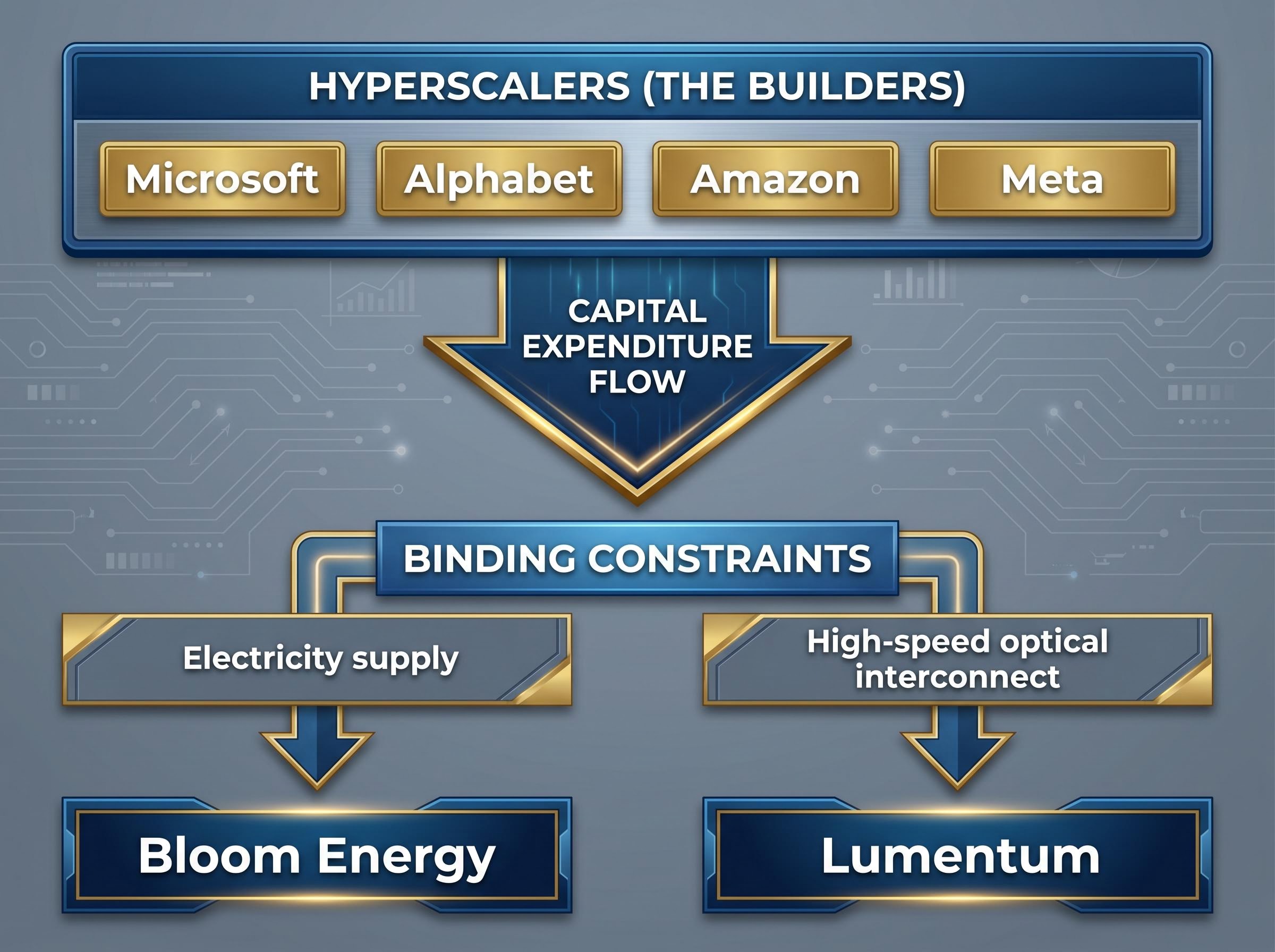

The scale of spending underpinning the supplier thesis is substantial: hyperscaler capex commitments for 2026 from Google, Amazon, Microsoft, and Meta combined are projected at approximately $725 billion, a 77% increase over the prior year, with power and land costs cited by multiple CFOs as primary drivers of budget escalation.

When big ASX news breaks, our subscribers know first

Why the suppliers are winning while the builders are being watched

The logic begins with where hyperscaler capital expenditure actually goes. When Microsoft or Amazon commits billions to data centre expansion, those dollars do not remain on the hyperscaler balance sheet. They flow to the specialist suppliers providing the physical inputs: power systems, optical networking equipment, cooling infrastructure, and high-speed interconnects. The suppliers are not secondary beneficiaries. They are direct revenue recipients of the largest technology capital expenditure cycle in a decade.

Two binding constraints are channelling a disproportionate share of that expenditure:

The scale of hyperscaler capital expenditure provides the demand floor that makes supplier revenue forecasts credible: Amazon, Microsoft, Alphabet, and Meta collectively spent $130 billion in Q1 2026 alone, with full-year 2026 combined guidance reaching approximately $725 billion and a trajectory toward $1 trillion annually by 2027.

- Electricity supply: AI data centres consume significantly more power per rack than traditional cloud workloads, and utility grid capacity is not expanding at the same pace as demand.

- High-speed optical interconnect: AI training and inference workloads require massive, low-latency data movement between servers, making optical networking components a structural requirement rather than a discretionary purchase.

Both constraints create pricing power and demand durability for the suppliers that can address them. Bloom Energy and Lumentum, profiled in the sections that follow, are representative of each.

A pattern that has played out before in technology cycles

The dynamic is not new. During the semiconductor expansion of the 2010s, equipment manufacturers such as ASML captured outsized returns relative to many of the chipmakers they served. During the cloud buildout, networking and storage suppliers delivered early-cycle equity appreciation that outpaced some of the hyperscalers building the infrastructure.

The picks-and-shovels pattern is a useful calibration tool: it explains why supplier outperformance is structurally plausible. It is not, however, a guarantee of continued returns. Every prior cycle eventually saw supplier valuations compress as buildout pace normalised. The pattern should inform position sizing and risk awareness, not replace it.

Bloom Energy and the power problem AI cannot solve without it

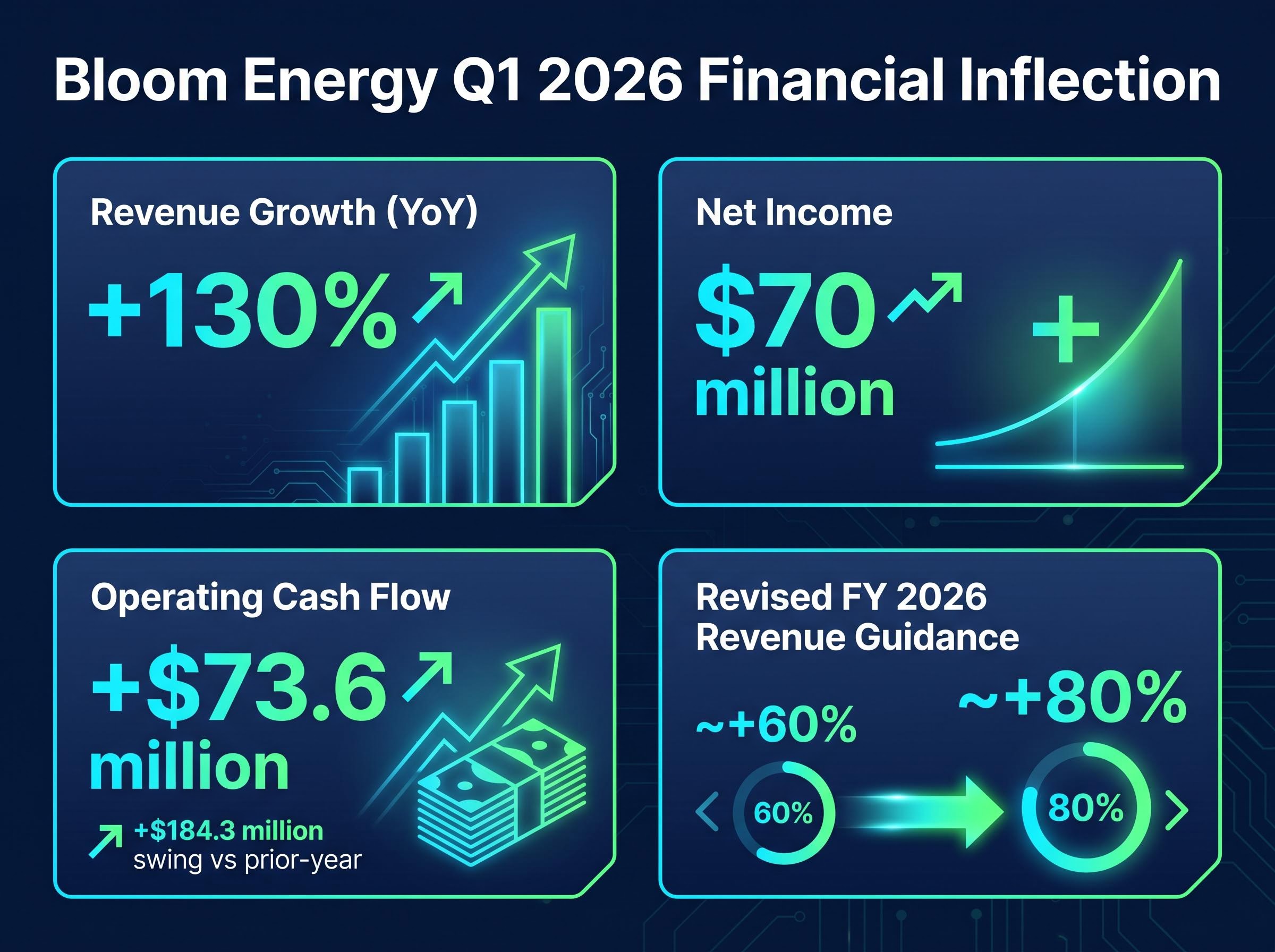

Bloom Energy has been operating for approximately 25 years, and for most of that history, it was an industrial energy company serving retail and aerospace clients. It was not on the AI watchlist. Then its Q1 2026 results arrived.

Revenue grew +130% year-over-year. Net income reached $70 million, a profitability milestone after roughly a quarter-century of losses. The company revised its full-year 2026 revenue guidance upward from approximately +60% to approximately +80%.

| Metric | Q1 2026 result |

|---|---|

| Revenue growth (YoY) | +130% |

| Net income | $70 million |

| Operating cash flow | +$73.6 million |

| Operating cash flow swing (vs prior-year Q1) | +$184.3 million |

| Revised FY 2026 revenue guidance | ~+80% (up from ~+60%) |

The +$184.3 million swing in operating cash flow from the prior-year quarter captures the speed of the financial inflection: from cash-burning industrial supplier to cash-generating AI infrastructure provider in a single year.

The specific differentiator is Bloom’s off-grid fuel cell energy servers. These standalone power systems can be rapidly deployed and scaled at data centre sites without dependence on constrained utility grid infrastructure. In an environment where grid capacity is the binding constraint on data centre expansion, Bloom offers something the traditional utility model does not: speed of deployment.

The company’s market capitalisation sits at approximately $86 billion, with a 52-week trading range of $18.12 to $322.83, a range that illustrates both the scale of the appreciation and the implied volatility investors are accepting.

Lumentum and the optical layer that AI data centres cannot function without

Where Bloom Energy addresses the physical supply problem of power, Lumentum addresses a performance problem: moving data between servers at the speed and cost that AI workloads demand. Optical components transmit large data volumes across server interconnects at reduced cost and high bandwidth, making them a structural requirement for data centres running AI training and inference workloads.

Lumentum reported fiscal Q3 2026 results (quarter ended 28 March 2026) showing revenue growth of +90% year-over-year. The company returned to GAAP operating profitability in the quarter, reversing an operating loss in fiscal Q3 2025. Market capitalisation stands at approximately $71 billion, with a 52-week trading range of $71.04 to $1,085.68.

Lumentum is not the only beneficiary of the structural shift toward high-bandwidth interconnect: among optical networking peers, Nokia’s optical and IP networks segment had its revenue growth guidance revised upward to 18-20% for 2026, with Morgan Stanley projecting 21% growth and naming the stock a top equity pick in May 2026, illustrating how broadly the optical layer thesis is distributing returns across the supply chain.

The profitability recovery is significant on its own. What sharpens the forward picture are two specific technology catalysts named by CEO Michael Hurlston.

Two technologies that could extend Lumentum’s growth runway

Hurlston identified two product categories expected to further enhance the company’s earnings capacity:

- Co-packaged optics: Integrating optical components directly with compute or switching silicon. This reduces the distance data must travel as electrical signals before converting to light, lowering latency and power consumption at the chip level. For investors, this represents a shift from standalone optical modules to a deeper integration point in the data centre architecture.

- Optical circuit switches: Enabling more flexible, high-bandwidth interconnect architectures inside data centres. Rather than fixed connections between specific server racks, optical circuit switches allow dynamic reconfiguration of data pathways, which supports the variable workload patterns of AI training runs.

Both technologies are already referenced in management guidance, positioning them as incremental adoption cycles rather than speculative bets. The distinction matters for evaluating the durability of Lumentum’s revenue growth beyond the current quarter.

The LightCounting optics for AI clusters forecast projects this market segment to double from approximately $5 billion in 2024 to more than $10 billion in 2026, with co-packaged optics and low-power optics scheduled for scaled deployment at major hyperscalers starting in 2026-2027, providing an independent demand baseline against which Lumentum’s forward guidance can be evaluated.

How to evaluate AI infrastructure exposure before committing capital

The Bloom and Lumentum profiles illustrate a pattern, but two companies do not constitute a portfolio strategy. Investors evaluating individual AI infrastructure stocks can apply three criteria drawn from the structural mechanics behind the outperformance:

- Revenue growth paired with a profitability inflection: High revenue growth alone does not distinguish a durable infrastructure position from a one-quarter demand spike. The profitability turn, as seen in both Bloom and Lumentum, signals that the business model is scaling efficiently with the demand.

- Competitive differentiation tied to a structural bottleneck: The company’s product should address a constraint (power supply, optical interconnect, cooling capacity) that data centre operators cannot easily resolve through alternative means. If the constraint loosens, so does the pricing power.

- Upward revisions to forward guidance: Management raising full-year guidance, as Bloom did from approximately +60% to approximately +80%, is a signal that demand visibility extends beyond the reported quarter.

For investors preferring diversified thematic exposure over individual stock selection, three ETFs provide access to the broader AI infrastructure theme:

- Roundhill Generative AI and Technology ETF

- iShares U.S. Power and Infrastructure ETF

- Pacer Data and Infrastructure Real Estate ETF

Data transparency note: Specific year-to-date return figures for these ETFs and precise index comparisons were not independently verified at the time of writing. Investors should check current performance data directly before making allocation decisions.

This is not a gap that weakens the thesis; it is a standard due diligence step that the verified company-level data does not replace.

Investors exploring how their existing index holdings may already be implicitly exposed to the AI infrastructure capex cycle will find our full explainer on AI infrastructure concentration risk in US portfolios, which examines how S&P 500 earnings growth forecasts have become disproportionately reliant on a small number of AI-exposed firms and outlines the diversification adjustments major institutional allocators including CalPERS are making in response.

The infrastructure cycle is early, but so is the risk of arriving late

The verified data points are clear. Bloom Energy grew revenue +130% year-over-year, reached profitability after roughly 25 years, and revised guidance upward. Lumentum grew revenue +90%, returned to operating profitability, and named two specific forward catalysts. Five AI infrastructure stocks at least doubled within the first five months of 2026.

The case for the infrastructure-over-hyperscaler thesis has evidence behind it.

What the evidence does not answer is how much of the forward opportunity is already priced in. Bloom’s 52-week range of $18.12 to $322.83 represents more than a 17x spread. Lumentum’s range of $71.04 to $1,085.68 spans more than 15x. Appreciation of that magnitude compresses the margin for error on entry. The same structural demand that drives the thesis also attracts capital at scale, and capital at scale compresses future returns.

The infrastructure outperformance relative to semiconductors is not a 2026-specific phenomenon: over the three years through May 2026, Bloom Energy returned 1,774.7%, more than quadrupling the Morningstar US Semiconductors Index return of 423.9%, while Quanta Services and MasTec posted three-year returns above 335.8%, a pattern that suggests the picks-and-shovels dynamic has been compounding across the entire AI buildout cycle.

Bloom Energy’s 52-week trading range: $18.12 to $322.83. The distance between the low and the high tells the story of the opportunity and the volatility in a single line.

The framework outlined above, revenue growth with profitability, bottleneck positioning, and guidance revisions, applies whether evaluating the next AI infrastructure name or reassessing positions in those already held. The infrastructure cycle appears early. The price of being late to recognise it is that valuations have already moved.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.