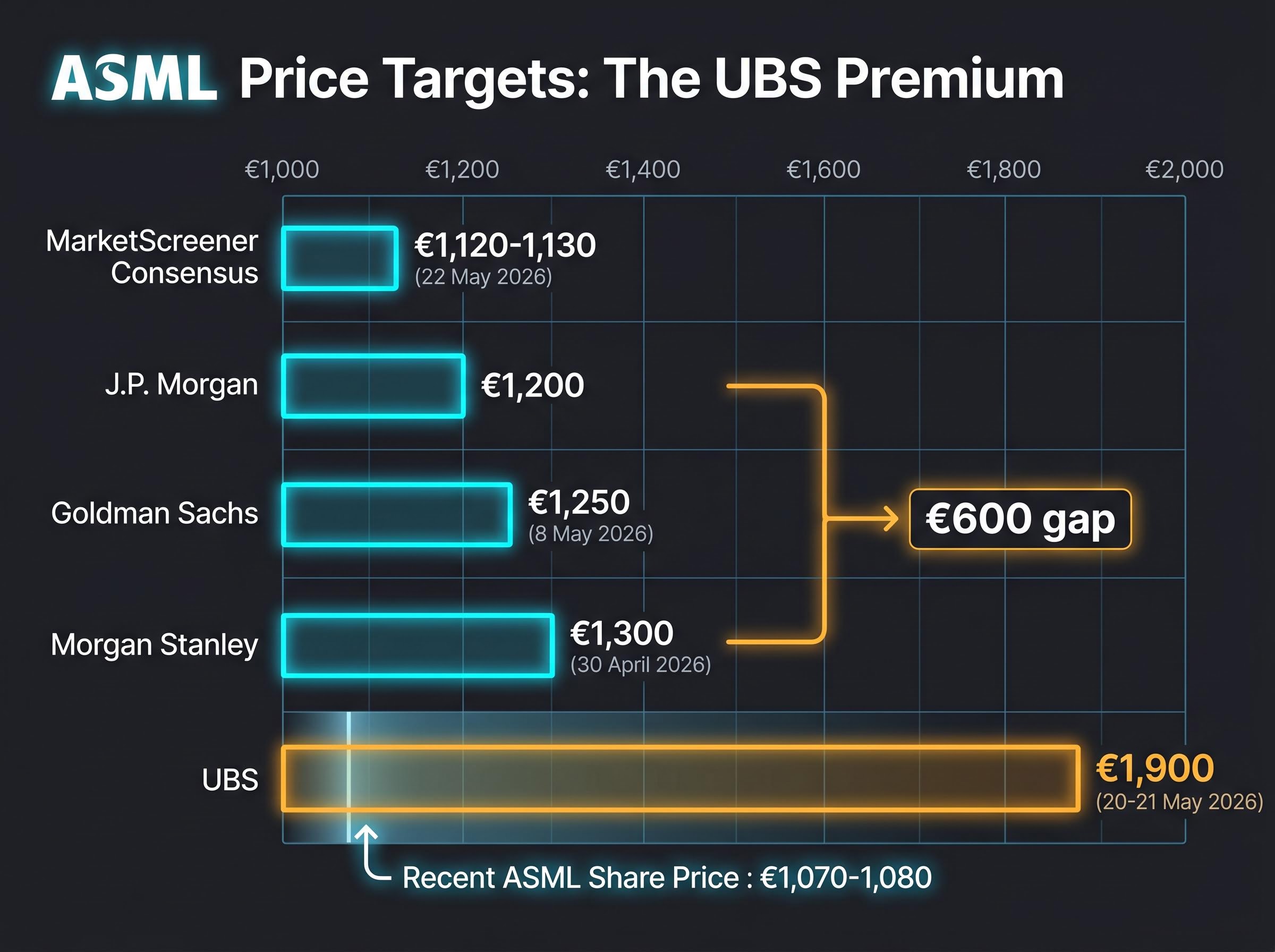

UBS has raised its ASML price target to €1,900, a figure more than 75% above the stock’s recent trading range, calling it “the most compelling equity opportunity” in a market the bank already considers rich. The call arrived on approximately 20-21 May 2026, with ASML shares trading near €1,070-1,080 in Amsterdam, up more than 50% over the prior 12 months and sitting near all-time highs. Most major brokers already rate the stock a Buy, but UBS’s target stands alone, more than €600 above Morgan Stanley’s next-highest major target of €1,300. That gap demands explanation.

What follows breaks down the three investment theses behind UBS’s call, examines the revenue forecast revisions that underpin the €1,900 figure, places the target against the broader analyst consensus, and identifies the specific conditions under which the bull case can or cannot be realised.

Why UBS’s €1,900 ASML target sits far above a consensus that is already bullish

A stock near all-time highs in a semiconductor sector where the iShares Semiconductor ETF (SOXX) has climbed 65% year-to-date does not, at first glance, look underappreciated. UBS acknowledges the backdrop is elevated. The distinction the bank draws is structural: the consensus already rates ASML a Buy, but the consensus, in UBS’s view, still underestimates how much lithography demand the next two years will produce.

UBS characterised ASML as “the most compelling equity opportunity” in the current market, a label that separates it from a routine reiteration of a Buy rating.

The ASML valuation discount to U.S. semiconductor equipment peers has compressed from a 10-year historical average premium of roughly 84% to approximately 6-15% as of mid-May 2026, a collapse that UBS treats as the central evidence of mispricing rather than a justified repricing of geopolitical risk.

The €1,900 target rests on three independent theses, each representing a source of upside that UBS believes the street has not fully priced:

- Excess lithography capacity: real EUV output in 2027 could materially exceed published guidance

- Memory share gains: the memory cycle extends further than consensus models, and ASML captures a growing share

- High NA EUV adoption: next-generation tools deliver cost and throughput advantages compelling enough to accelerate customer uptake

When big ASX news breaks, our subscribers know first

What ASML actually is (and why its monopoly position matters here)

ASML Holding NV is the sole global supplier of extreme ultraviolet (EUV) lithography equipment, the machines that print the finest circuit patterns on advanced semiconductors. EUV lithography uses extremely short wavelengths of light to etch transistor designs onto silicon wafers, and no other company produces a commercially viable alternative. Every leading-edge logic chip from TSMC, Samsung, and Intel, and every advanced memory chip from producers including SK Hynix, depends on ASML equipment reaching their fabs.

That dependency extends to the AI supply chain. Nvidia’s most advanced GPUs are manufactured on TSMC nodes that require multiple EUV lithography steps. The Foundry and Logic segment accounted for an estimated 62% of ASML’s product revenue in 2026, and national semiconductor investment programmes from the United States, Europe, Japan, and South Korea are all adding fab capacity that feeds directly into ASML orders.

The order backlog stood at approximately €38 billion as of Q3 2025, the last explicitly quantified figure from the company, with end-2025 backlog characterised as covering more than a full year of 2025 sales (above €32.7 billion). ASML trades at approximately 40-45x forward earnings versus 20-25x for the broader European semiconductor equipment peer group, a premium consistently attributed to this monopoly position.

The table below summarises where each major customer stands on ASML’s next-generation High NA EUV platform:

| Customer | Status | Node Target | Delivery Timeline |

|---|---|---|---|

| Intel | Confirmed lead customer; first EXE:5000 shipped | 14A-class processes | First tool shipped December 2023; installed in Oregon |

| TSMC | Orders placed per third-party reports | Post-N2 nodes | Second half of decade; no specific install date confirmed |

| Samsung | Purchase orders reported by Korean trade press | Post-2 nm | First deliveries expected approximately 2027-2028 |

| SK Hynix | In discussions for DRAM applications | Future DRAM nodes | No confirmed orders; possible pilot in late 2020s |

Inside ASML’s growth pillars: optimistic capacity projections, an extending memory cycle, and High NA economics

UBS’s €1,900 target is not built on a single argument. It rests on three theses, each independently underwriting a portion of the upside, meaning the investment rationale does not collapse if one pillar weakens:

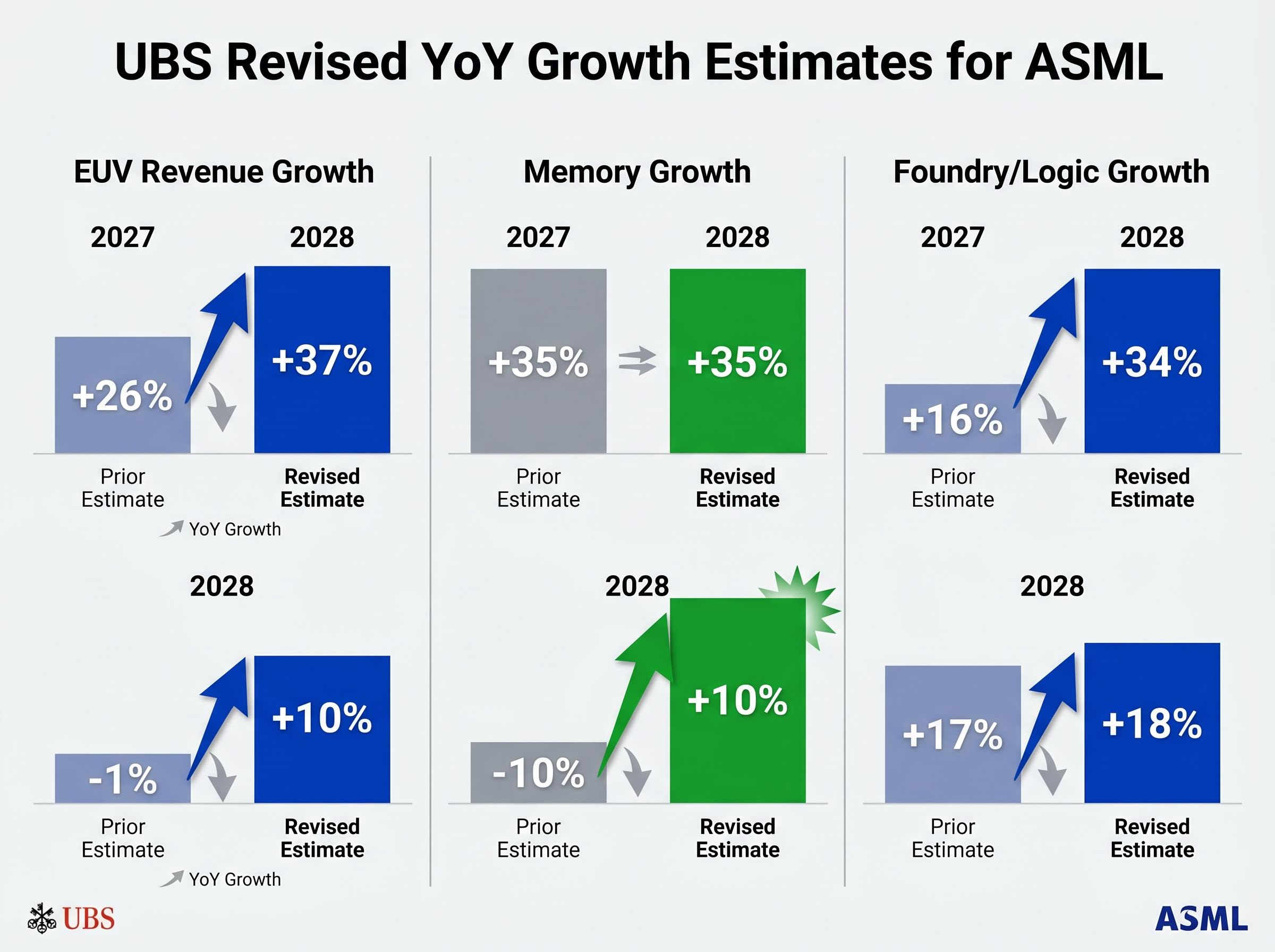

- Optimistic capacity projections. ASML’s public guidance targets approximately 80 EUV units for 2027. UBS contends that throughput improvements and upgrade potential mean real EUV output capacity could exceed 100 units, which would represent approximately a 65% year-over-year increase in leading-edge capacity. If the demand exists, and UBS believes it does, the revenue upside from those additional units is not yet in consensus models.

- Extending memory cycle. The memory cycle is expected to remain extended through 2028 due to supply constraints, with ASML gaining share in memory lithography as DRAM nodes advance to architectures requiring more EUV layers. UBS held its 2027 memory segment growth estimate at +35% year-over-year and raised 2028 from -10% to +10%, a revision that signals cycle extension rather than peak-and-fade.

- High NA adoption economics. The strongest structural argument. High NA delivers 20-40% cost savings on the most patterning-intensive layers and throughput gains exceeding 100% versus most alternatives (approximately 80% versus LELE patterning specifically), making the commercial case for adoption over the next two to three years increasingly difficult for leading chipmakers to defer.

High NA EUV: the patterning step change that changes the maths

High NA EUV operates at 0.55 numerical aperture versus 0.33 NA on standard EUV systems, enabling finer resolution that eliminates the need for double and triple patterning steps. The commercial logic is direct: chipmakers currently running ALD multi-patterning steps at approximately 30 wafers per hour can replace those steps with High NA EUV and capture both cost and throughput gains simultaneously.

High NA EUV delivers more than 100% throughput improvement versus most alternative patterning approaches, according to UBS, making the adoption case less about technical ambition and more about manufacturing economics.

Intel is the confirmed lead customer, with the first TWINSCAN EXE:5000 shipped in December 2023. TSMC has placed orders according to third-party reports, and Korean trade press has reported Samsung orders for post-2 nm nodes with deliveries expected around 2027-2028. SK Hynix remains in discussions for future DRAM applications.

UBS’s revised revenue forecasts: the numbers behind the €1,900 target

The scale of UBS’s forecast revisions separates this from an incremental upgrade. The bank raised its 2027 EUV revenue growth estimate to 37% year-over-year from a prior 26%, and flipped its 2028 EUV forecast from -1% to +10% year-over-year. That 2028 revision is the single most telling number in the note: it signals UBS is not just upgrading a cyclical peak but arguing the cycle extends further and deeper than the market currently prices.

| Segment | 2027 Prior Estimate | 2027 Revised | 2028 Prior Estimate | 2028 Revised |

|---|---|---|---|---|

| EUV Revenue Growth (YoY) | +26% | +37% | -1% | +10% |

| Memory Growth (YoY) | +35% | +35% | -10% | +10% |

| Foundry/Logic Growth (YoY) | +16% | +34% | +17% | +18% |

The 2028 memory revision, from -10% to +10%, is the most contrarian element of the UBS view, implying that the memory lithography cycle extends well beyond what consensus models assume.

UBS expects the 1d DRAM ramp-up phase in 2027-2028 to be more lithography-intensive than previously modelled, adding further upside to system demand. For context, ASML reported full-year 2025 net sales of €32.7 billion and has guided 2026 revenue of €34-36 billion, meaning these revised growth rates apply to an already-expanding revenue base.

The AI capex cycle driving semiconductor demand growth has a documented 18-24 month lag between hyperscaler capital commitment and revenue recognition at equipment suppliers, a structural timing gap that makes 2027-2028 revenue forecasts particularly sensitive to whether current capex commitments translate into production-scale deployments on schedule.

Where the consensus sits and what the bear case looks like

UBS is not the only bull. The broader consensus already rates ASML a Buy, with an average 12-month target of approximately €1,120-1,130 according to MarketScreener data as of 22 May 2026. TipRanks reports a “Strong Buy” consensus from more than 20 covering analysts on the US-listed ADR, with an average target of approximately $1,185. Morgan Stanley raised its target to €1,300 on 30 April 2026. Goldman Sachs lifted to €1,250 on 8 May 2026. J.P. Morgan holds at €1,200.

The distinction is magnitude. UBS’s €1,900 sits €600 above the next-highest major target. The consensus is already bullish, which means the UBS call is not a contrarian upgrade from neutral but a far-outlier target from an already-crowded bull camp.

The bear case centres on three identifiable risks:

- Export control tightening. EUV remains prohibited to China, advanced DUV requires case-by-case licensing, and as of April 2025, US officials continued pressing the Netherlands and Japan for further restrictions. Additional DUV curbs would directly hit near-term revenues.

- High NA adoption delay. If TSMC and Samsung defer confirmed installation timelines, the adoption thesis loses its near-term revenue contribution.

- Capex cycle normalisation. Morningstar maintains a Wide Moat rating but characterises the stock as trading above its fair value estimate. A compression in the 40-45x forward earnings multiple toward sector averages would significantly reduce the path to €1,900.

China export control risk for ASML is structurally distinct from trade-negotiable tariff arrangements because the controls are grounded in US national-security law with bipartisan Congressional backing, placing them outside the jurisdiction of any bilateral trade summit and making incremental de-escalation an unreliable base case for near-term revenue recovery.

The BIS semiconductor equipment export controls introduced in December 2024 added 24 categories of semiconductor manufacturing equipment to the restricted list, establishing the regulatory baseline from which any further Dutch or Japanese alignment on DUV licensing would build.

The real test comes in 2027: how to watch this thesis play out

A price target only holds value if the assumptions behind it can be monitored. Three signposts will determine whether UBS’s €1,900 thesis is tracking:

- EUV unit shipments in 2027. This is the primary validation trigger. UBS projects EUV demand growth of 25-30% year-over-year in 2027. If ASML ships above 90-100 units, the capacity thesis holds. If shipments stay near the guided 80 units, the premium in UBS’s target collapses. The 2026 revenue guidance of €34-36 billion provides the baseline from which 2027 growth must be judged.

- High NA order expansion. TSMC and Samsung moving from reported orders to confirmed installation timelines before end-2026 would substantiate the adoption thesis. Absence of those confirmations by year-end would weaken it.

- China policy risk. Further DUV licensing restrictions represent the key exogenous variable. Any new statutory curbs would test whether the non-China demand base absorbs the shortfall, or whether near-term revenue forecasts require downward revision.

The concrete impact of export controls on chip revenue is visible in real time through Nvidia’s experience: approximately 10 Chinese firms hold US clearance to purchase H200 units yet no deliveries have occurred as of late May 2026 because Beijing has not issued its own required approval, a dual-approval deadlock that illustrates how geopolitical constraints can freeze demand that is technically permitted.

With shares near €1,075, the implied upside to UBS’s target sits at approximately 75-78%. That is a bet on structural scarcity in advanced semiconductor manufacturing, not a short-term momentum trade.

Morningstar describes ASML as having the least cyclical earnings profile among capital equipment names in its coverage universe, a characterisation that underpins why UBS frames the premium valuation as justified rather than stretched.

The €1,900 target is a conviction call on technology that has no substitute, a backlog that extends years into the future, and demand reinforced by AI investment, government-backed fabs, and the next generation of memory production. The bar for validating it is high, but it is also specific, and the next 18 months of shipment data, order confirmations, and policy decisions will determine whether the market agrees.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including analyst price targets and revenue forecasts, are speculative and subject to change based on market developments and company performance.