A blockade could shut down Taiwan’s semiconductor fabs in weeks. Replacing the chip supply those fabs produce would take decades. That asymmetry sits at the centre of the most consequential supply-chain vulnerability in the global economy.

This is not a niche geopolitical risk confined to defence analysts and foreign policy journals. Advanced semiconductors manufactured in Taiwan are embedded in AI data centres, automotive production lines, hospital equipment, smartphones, weapons systems, and industrial control networks. The exposure is not sectoral; it is structural, woven into the operating substrate of virtually every modern industry.

Here is the analytical framework for understanding exactly where the vulnerability sits, how rapidly it would propagate, and where policy responses currently fall short. If you hold technology, automotive, industrial, or consumer electronics exposure, the questions this analysis raises are not theoretical. They are portfolio-relevant today.

How one foundry came to hold the global chip supply

Taiwan Semiconductor Manufacturing Company (TSMC) was founded on a single insight: manufacturing chips as a service for the entire industry, neutral to designer or application. That foundry model, where a company fabricates chips designed by others, standardised process technology and made it compatible with widely used electronic design automation tools. The result was an ecosystem any chip designer could plug into.

Intel took the opposite path, integrating design and manufacturing but never standardising its processes for external customers. That limited Intel’s ability to serve the broader chip design market and left TSMC to consolidate it. Apple’s role as a demanding TSMC customer pushed the foundry to achieve leading-edge capability, and the gap widened from there.

At the time of Pat Gelsinger’s return to Intel, TSMC was producing five times Intel’s wafer volume. That gap later widened to approximately seven to one.

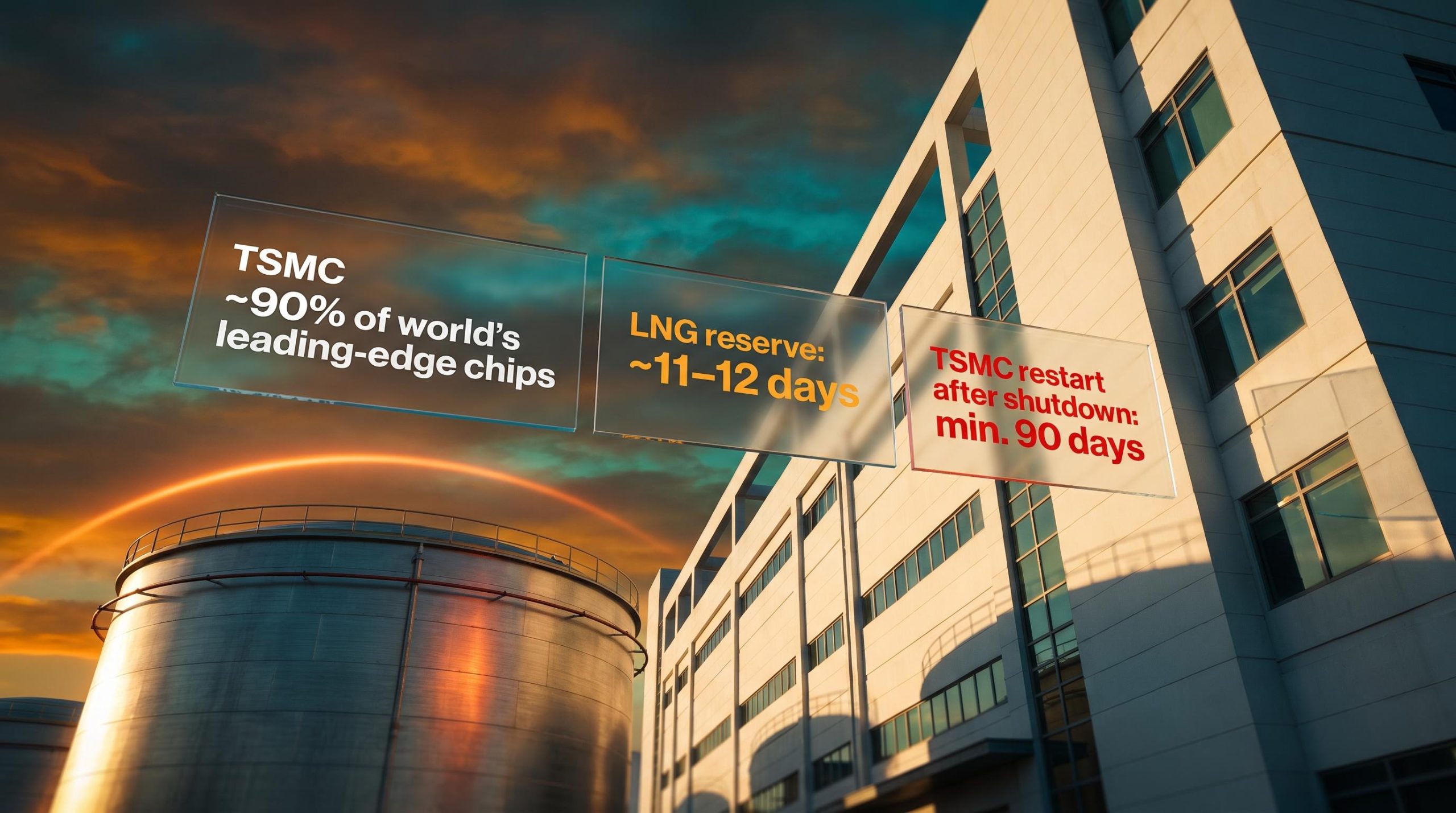

Today, TSMC produces approximately 90% of the world’s leading-edge chips (below the 5nm node, which refers to the most advanced manufacturing processes used for the fastest, most power-efficient semiconductors). Its market capitalisation has approached approximately $1 trillion. The major chip designers dependent on TSMC for leading-edge production include:

- Apple

- NVIDIA

- AMD

- Qualcomm

- Multiple other AI, networking, and mobile chip firms

That concentration figure tells you that any disruption to this single foundry is not a supply shock for one company or one sector. It is a simultaneous input failure for virtually every major technology product on the market.

The concentration risk documented in Taiwan extends across the entire AI chip supply chain, where Nvidia, TSMC, ASML, and Broadcom occupy distinct and non-interchangeable layers that collectively funnel leading-edge output through a single geographic chokepoint.

When big ASX news breaks, our subscribers know first

Taiwan’s real vulnerability is not geography, it is energy

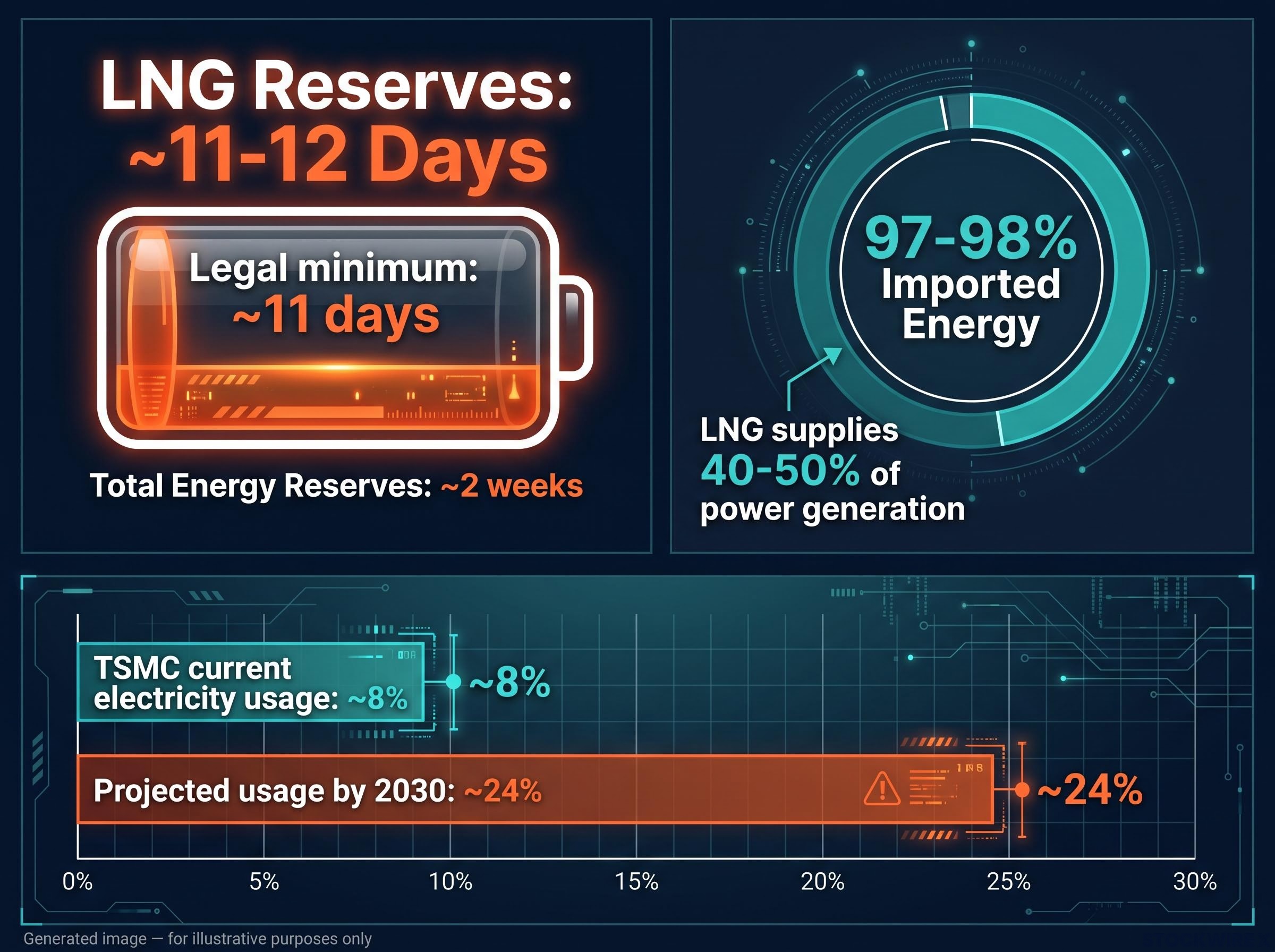

The standard framing of Taiwan risk centres on military scenarios: amphibious invasion, missile strikes, contested airspace. But the faster-acting mechanism is far more mundane. Taiwan imports approximately 97-98% of its energy, with 99.75% of petroleum arriving by sea. Its entire industrial base, including its semiconductor fabs, runs on fuel that must cross open water to reach the island.

The Atlantic Council energy resilience analysis corroborates Taiwan’s import dependence at approximately 95% of total energy needs, with over 99% of oil and natural gas arriving by sea, figures that align with the reserve constraints described here and reinforce the structural nature of the vulnerability.

Liquefied natural gas (LNG), a form of natural gas cooled to liquid for shipping, is the most acute pressure point. LNG supplies 40-50% of Taiwan’s power generation. Taiwan’s legal LNG reserve requirement sits at approximately 11 days, with current inventories generally around 12 days or marginally above. Plans call for raising this minimum to 14 days by 2027, with storage capacity potentially allowing up to 24 days of reserves (though this latter figure has not been independently confirmed).

TSMC alone consumes approximately 8% of Taiwan’s total electricity. That share is projected to approach 24% by 2030 as advanced node manufacturing scales, concentrating the energy vulnerability into a single corporate footprint.

| Energy Source | Share of Power Generation | Reserve Level | Key Vulnerability |

|---|---|---|---|

| LNG | 40-50% | ~11-12 days (legal minimum ~11) | Thin buffer; entirely import-dependent via maritime routes |

| Oil / Petroleum | Supplementary fuel and transport | Limited strategic reserves | 99.75% arrives by sea; three main ports face China |

| Total Energy Imports | 97-98% of all energy | ~2 weeks of total usage | Near-total import dependence with no domestic substitutes at scale |

Under current reserves, Taiwan could sustain approximately two weeks of energy usage without new supply.

An 11-day LNG buffer means a blockade does not need to be militarily decisive to be economically catastrophic. It only needs to hold long enough for the fuel to run out, and that window is measured in days, not months.

The blockade scenario, week by week

China does not need to launch an amphibious invasion to shut down Taiwan’s fabs. Blocking or pressuring tanker traffic into Taiwan’s energy ports, or applying diplomatic pressure on LNG exporters, achieves the same outcome on a faster timeline. China has reportedly conducted blockades of the Taiwan Strait on approximately seven occasions over the four years preceding this analysis, signalling sustained strategic intent.

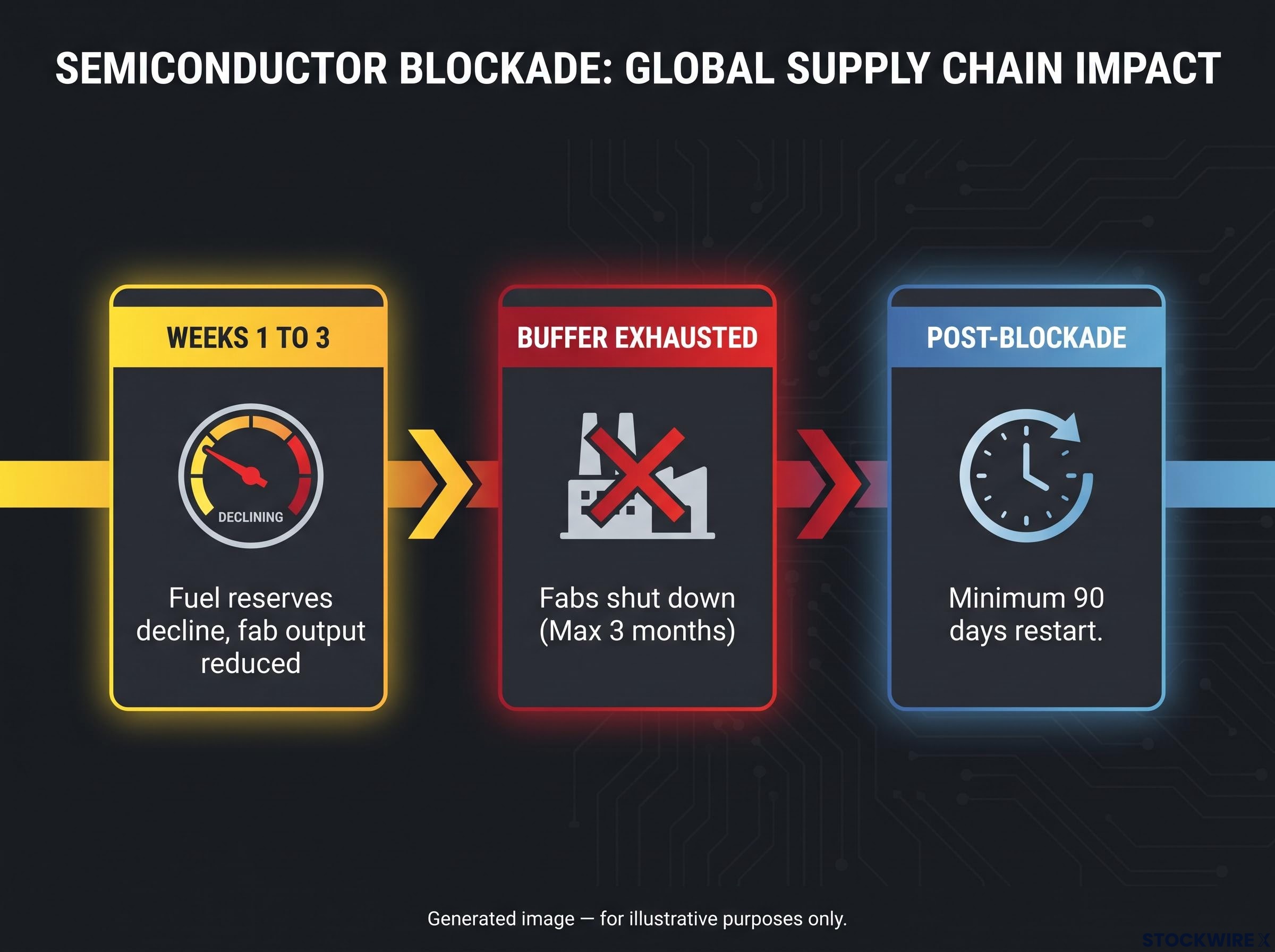

The shutdown sequence would unfold in three stages:

- Weeks one to three: Fuel reserves decline. Grid operators begin rationing, reserve margins fall, and fab output is reduced. Fabs require continuous, high-quality power to maintain cleanroom environments, temperature and humidity control, vacuum systems, and lithography tools. They cannot throttle down to intermittent power without risking contamination and loss of process control. Power rationing would likely prioritise residential and critical services, forcing fabs to scale back before national fuel reserves are fully exhausted.

- Around the point LNG and oil buffers are exhausted: Fabs must shut down or operate at capacity incompatible with leading-edge output. Expert assessments indicate Taiwan would struggle to last more than three months under a serious energy blockade without external intervention.

- Post-blockade restart: Restarting and requalifying fab operations after an uncontrolled shutdown takes a minimum of approximately 90 days before pre-crisis volumes and yields are restored. The more abrupt the shutdown, the longer and more uncertain the restart.

Restart and requalification after an uncontrolled shutdown takes a minimum of approximately 90 days, and the more abrupt the shutdown, the longer the recovery.

The 90-day minimum restart period means that even a brief, successful blockade creates a chip supply gap that outlasts the blockade itself by months. Financial markets would begin pricing that gap well before the restart is confirmed. The Taiwan Strait carries approximately half of global trade; disruption compounds far beyond chips.

What makes this shock different from previous supply crises

The 2020-2021 chip shortage is the closest reference point most investors carry. That disruption was partial and localised, affecting automotive production, consumer electronics timelines, and industrial equipment, yet it never touched leading-edge fabrication capacity at scale. A blockade-driven shutdown would be structurally different: simultaneous across all leading-edge nodes, abrupt rather than gradual, and affecting the substrate of industries that were previously insulated from chip supply risk.

Advanced semiconductors are embedded in AI accelerators, data centres, smartphones, networking gear, industrial control systems, weapons systems, telecommunications equipment, and medical devices. A leading-edge chip collapse hits all of these simultaneously, with no partial substitutes available on a short timeline.

| Crisis | Trigger | Affected Sectors | Recovery Path |

|---|---|---|---|

| 2020-2021 chip shortage | Pandemic demand shifts, localised fab disruptions | Automotive, consumer electronics, industrial | Gradual capacity ramp over 12-18 months |

| 1973 oil embargo | OPEC export restrictions | Transport, energy-intensive manufacturing | Partial substitution; uneven impact by geography |

| Taiwan blockade scenario (hypothetical) | Energy import disruption to semiconductor fabs | All sectors dependent on advanced chips simultaneously | Multi-month to multi-year; no short-term substitution |

Unlike an oil embargo, where some industries adapt faster than others, a leading-edge chip collapse hits AI, automotive, industrial, medical, and defence simultaneously with no partial substitutes available. The synchronisation of the shock is what makes it categorically different.

The comparison to the Great Depression has been raised in scenario analyses. The Great Depression involved U.S. real GDP contraction of roughly 30% and global output declines in the double-digit percentage range. “Worse than the Great Depression” is best understood as a tail-risk scenario description that captures unprecedented digital dependence and supply concentration, not a consensus economic forecast. The direction of risk is clear; the scale would depend on blockade duration, global policy response, inventory levels, and chip triage capabilities.

For investors, the relevant insight is that portfolio hedges built around past supply crises, commodity exposure, sector rotation, may not translate to a scenario where the affected input is universal and non-substitutable on a short timeline.

Geopolitical energy shocks transmit into equity markets at speeds that outpace earnings revision cycles, as South Korean equities demonstrated when the KOSPI fell 12% during the Hormuz disruption while the S&P 500 declined just 1.36%, a divergence driven entirely by energy import geography and highly relevant to how Taiwan risk would reprice chip-sector equities.

How far the CHIPS Act has actually moved the needle

The U.S. CHIPS and Science Act (2022) committed tens of billions of dollars to domestic semiconductor manufacturing and R&D, catalysing new fab construction by TSMC in Arizona, Intel’s foundry development, and Samsung’s U.S. operations. The progress is real and measurable. Around 2021, when the Act was getting underway, the U.S. accounted for roughly 12% of leading-edge semiconductor output worldwide. Since then, that figure has grown to approximately 18%.

The CHIPS Program Office progress report, published by NIST in January 2025, sets specific domestic production targets for leading-edge logic and DRAM fabrication, providing the official baseline against which the shift from 12% to 18% domestic output share can be measured.

Pat Gelsinger, providing firsthand assessment, expressed the view that supply chain resilience needs to accelerate beyond the current pace of progress.

The move from 12% to 18% is directionally correct, but it tells you that even after years of subsidised construction, the U.S. remains overwhelmingly exposed to a Taiwan disruption. The gap between current policy output and meaningful resilience is not closed in a single legislative term. A 50% domestic production share, the benchmark that would substantially reduce dependence, remains distant.

The structural requirements beyond capital that make fab diversification a multi-decade effort include:

- Grid and energy infrastructure capable of supporting massive, stable power loads

- Workforce and talent pipelines (engineers and technicians at scale)

- Local supplier ecosystems for gases, chemicals, wafers, and tools

- Regulatory and permitting timelines for new construction

Allied initiatives in Japan, Korea, and Europe mirror the U.S. push but face the same structural timeline constraints. For investors assessing companies positioned on the solution side of this risk, the policy progress confirms long-duration demand for their services without suggesting that the underlying supply-chain risk resolves quickly.

The next major ASX story will hit our subscribers first

Where this leaves investors in technology and supply-chain resilience

Taiwan semiconductor risk is a structural portfolio exposure for virtually every investor with meaningful technology, automotive, industrial, or consumer electronics holdings. The question is not whether you are exposed but where your exposure sits on the spectrum of concentration.

Firms with single-foundry dependence on Taiwan for leading-edge production face maximal disruption risk in a blockade scenario. Those with diversified manufacturing, qualified capacity outside Taiwan, or substantial strategic inventory buffers have partial mitigation. The distinction matters for how you assess individual holdings.

| Category | Taiwan Dependency Level | Risk in Blockade Scenario | Potential Mitigation |

|---|---|---|---|

| Large-cap chip designers (fabless) | Very high | Near-total supply disruption | Secondary foundry qualification; strategic inventory |

| Automotive OEMs | High (indirect) | Production line shutdowns within weeks | Multi-source chip procurement; legacy node alternatives |

| Data centre operators | High | AI accelerator and server CPU supply freeze | Extended inventory buffers; capacity pre-positioning |

| Fab equipment suppliers | Low (customer-diversified) | Short-term order disruption; long-term demand surge | Geographic diversification of customer base |

| Advanced packaging companies | Moderate | Input disruption from leading-edge chip shortage | Non-Taiwan capacity; diversified technology platforms |

Companies positioned on the solution side of this risk include:

EUV lithography is the process technology that defines the leading edge where Taiwan concentration is most acute; ASML holds a structural monopoly on this equipment with no competitor offering a comparable platform, meaning that fab equipment exposure sits on the solution side of the disruption risk without carrying direct Taiwan operational exposure.

- Fab equipment suppliers, particularly EUV lithography (where ASML is the sole supplier)

- Energy infrastructure providers for semiconductor clusters

- Specialty materials companies (gases, chemicals, wafers)

- Advanced packaging firms with non-Taiwan capacity

Tail risks are frequently underpriced until they crystallise. The structural facts that make Taiwan semiconductor risk acute are documented. Markets often treat them as low-probability background noise. If the probability assessment shifts, repricing in technology equities could be abrupt. Investors who have already mapped their exposure will be better positioned to act or hedge.

The gap that policy cannot close on a political timeline

The energy mechanism converts a blockade into a fab shutdown in weeks. Rebuilding meaningful alternative capacity takes decades. The window of maximum vulnerability is the present and the near-to-medium term.

Crisis could unfold in weeks. Meaningful diversification and resilience require decades. That mismatch is the investment thesis, regardless of how specific political scenarios evolve.

The U.S. has moved from 12% to 18% domestic leading-edge production since the CHIPS Act, with 50% as a distant benchmark. The global economy remains heavily exposed to Taiwan’s ability to maintain stable energy supplies and continuous fab operations.

“Worse than the Great Depression” is a tail-risk description, not a forecast. The actual severity of a blockade would depend on duration, global policy response, inventory levels, and chip triage capabilities. The uncertainty in the worst-case scenario does not reduce the certainty in the structural vulnerability.

Treating Taiwan semiconductor risk as a low-probability background concern is itself an investment decision with real consequences. The structural conditions making the risk acute are durable, and the diversification timeline means they will not resolve before the risk window closes. Portfolio frameworks built on the assumption that technology supply chains are resilient are resting on an assumption the evidence does not yet support.

For investors tracking how markets are already repricing Taiwan concentration risk in real time, our full explainer on TSMC’s capex reset examines why the $60-64 billion Arizona expansion programme is compressing free cash flow yields even as earnings estimates move higher, a dynamic directly relevant to valuing solution-side semiconductor positions.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and geopolitical conditions.