According to Bank of America’s own analysis, June core CPI recorded a monthly fall that has occurred on only seven occasions since 1985. Headline CPI came in 0.4% below its prior level on a month-over-month basis, falling short of consensus forecasts. For most of Wall Street, that was a green light to soften rate forecasts.

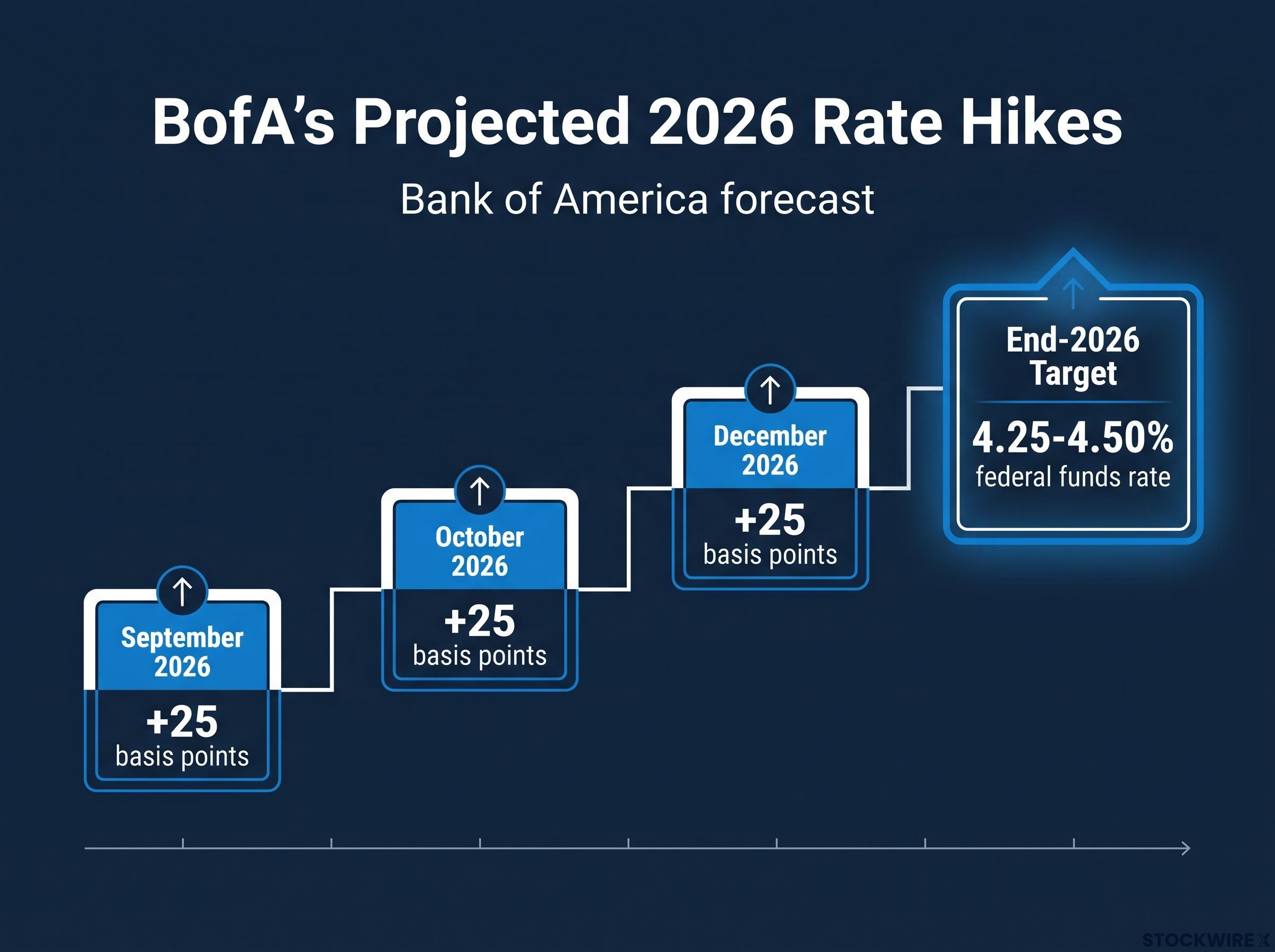

BofA went the other way. On 17 July 2026, Aditya Bhave and his team at BofA Global Research published a client note reaffirming a call for 75 basis points of Fed rate hikes before year-end, spread across three consecutive meetings. The bank is not hedging. It is not waiting for confirmation. It is telling clients that the soft print changed the near-term pressure but not the destination.

The gap between what markets are pricing (roughly 40-42 basis points of tightening) and what BofA is forecasting (a minimum of 75 basis points) is not a rounding error. It is a structural positioning question for anyone holding rate-sensitive assets into the second half of 2026. Here is what the inflation data, the new Fed Chair’s incentive structure, and the market pricing gap actually tell you about where rates are headed and what that means for your positioning decisions.

One soft print, one firm call: what BofA actually said

The sequence matters. June CPI landed soft. Core CPI declined on a monthly basis. The bank adjusted its June core PCE (personal consumption expenditures, the Fed’s preferred inflation gauge) tracking estimate to 0.15% month-over-month, bringing it down from earlier projections. By conventional logic, this is the point where a bank dials back its hawkish stance.

The June CPI miss that prompted markets to soften rate forecasts is precisely the print BofA’s team worked through before reaffirming its hiking call, treating a 0.0% monthly core reading as insufficient to alter a structural inflation view anchored on 3.3% core PCE.

BofA did the opposite. The 17 July client note, authored by Aditya Bhave’s team, reaffirmed the full hiking path:

- September 2026: +25 basis points

- October 2026: +25 basis points

- December 2026: +25 basis points

- End-2026 target: federal funds rate of 4.25-4.50%

BofA placed its June core PCE tracking at 0.15% month-over-month, a figure that came in below earlier projections in the wake of the softer-than-expected CPI reading.

This represents a documented reversal from the bank’s earlier stance. Earlier in 2026, BofA had expected two rate cuts, with its analysis suggesting Chair Warsh could use cooling inflation data to justify easing. That expectation is gone.

The soft June print reduced near-term pressure on the Fed, but it did not change BofA’s year-end destination. For your positioning, the precise lift-off meeting matters less than where the policy rate ultimately lands. BofA is telling you the answer is 4.25-4.50%, and one month of cooperative data did not move that number.

When big ASX news breaks, our subscribers know first

Why BofA thinks 3.3% core PCE is the real story

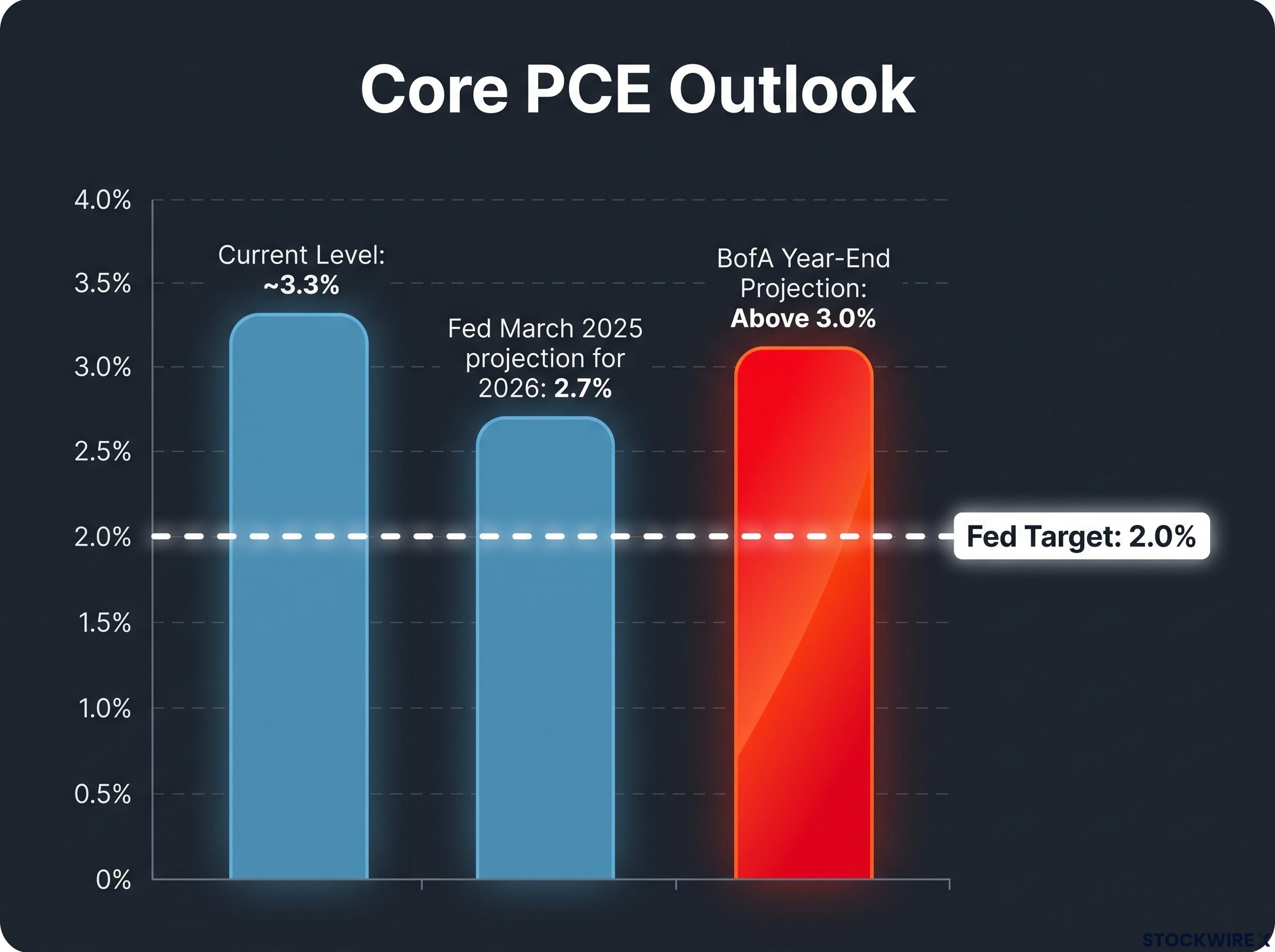

A single monthly CPI print tells you what prices did in one month. Core PCE running at approximately 3.3% year-over-year tells you what inflation is doing structurally. BofA’s analysis anchors on the latter, and the distinction between the two is where the bank’s conviction sits.

Core PCE measures the price changes in goods and services consumed by individuals, excluding volatile food and energy categories. The Fed uses it as its primary inflation gauge because it captures underlying price trends more reliably than the headline CPI that dominates news coverage. When core PCE is running at 3.3% against a 2% target, the gap is not subtle.

BEA’s core PCE index strips out volatile food and energy prices to produce the inflation measure the Fed formally targets, which is why a sustained reading of 3.3% on this gauge carries more policy weight than any single month of headline CPI data.

BofA projects core PCE will rise toward 3.5% before stabilising above 3% by year-end, not falling below it. The bank pushed back firmly against client views that recent price pressures stem from temporary or isolated factors, characterising the current inflation backdrop as structurally elevated rather than cyclically driven.

What the housing disinflation fade means

Much of the cooling narrative in recent months has rested on housing disinflation, the gradual easing of shelter costs that had been a major inflation driver. BofA assesses that this component is fading, which removes one of the most cited arguments for near-term PCE deceleration. If the one component markets were counting on to pull inflation lower is losing its disinflationary force, the 3.3% figure does not just persist; it risks moving higher.

| Metric | Current level | Fed target | BofA year-end projection |

|---|---|---|---|

| Core PCE (YoY) | ~3.3% | 2.0% | Above 3.0% |

| Headline PCE (YoY) | ~3.5% | 2.0% | ~3.5% |

| Federal funds rate | 3.50-3.75% | N/A | 4.25-4.50% |

Even the Fed’s own March 2025 projections placed the median 2026 PCE forecast at 2.7%, well above its 2% objective. BofA’s read is that the Fed’s own numbers already acknowledge persistence; the bank simply takes the argument further. If you are treating one soft monthly print as confirmation of a dovish pivot, BofA is telling you the component dynamic you are relying on is already reversing.

The Warsh factor: why the new Fed Chair’s incentives point toward hikes

Kevin Warsh is now serving as Federal Reserve Chair, confirmed by a BofA Private Bank Washington update. His first FOMC meeting on 17 June 2026 held rates steady at 3.50-3.75%, and his congressional testimony stressed a determination to restore price stability alongside a broadly constructive view on productivity growth, without introducing any fresh policy direction.

What BofA’s client note does is read the institutional incentives sitting beneath the public statements. The bank’s analytical inference, and this should be understood as interpretive commentary rather than a direct public statement from BofA, is that Warsh holds “low-cost, high-reward” incentives to raise rates.

Warsh’s communication regime, which explicitly abandoned forward guidance at the June press conference and withheld his own dot plot projection, is the reason BofA is reading institutional incentives and congressional testimony rather than waiting for explicit rate-path signals from the Chair himself.

BofA’s analytical interpretation: the bank sees Warsh as having strong strategic grounds for tightening promptly, since moving early on rates would build his inflation-fighting credibility while keeping him at arm’s length from an inflation problem that predates his tenure.

The logic is institutional rather than ideological. A new Fed Chair who tightens early establishes inflation-fighting credentials. If inflation subsequently moderates, the tightening gets partial credit. If inflation persists despite tightening, the Chair is seen as having acted rather than waited. The asymmetry favours action.

BofA’s reading of the testimony found nothing to suggest the recently created Fed task forces would provide cover for deferring rate increases. The three key takeaways from BofA’s reading of the testimony:

- Commitment to price stability was reiterated without qualification

- No new policy direction or forward guidance was introduced

- Nothing in the testimony pointed to task forces being used as a reason to hold off on tightening

This tells you something important about BofA’s hiking call: it is not purely a function of inflation data. It also reflects a read on the person now holding the lever, and that adds a layer of conviction that pure data-watching cannot replicate. Understanding why a new Fed Chair might be predisposed toward tightening, independent of the data, changes how you should read Warsh’s future communications and the probability you assign to the hiking path materialising.

Markets are pricing roughly half of what BofA expects

By mid-July 2026, BofA’s own assessment put market-implied tightening at close to 40 basis points, while LSEG data pointed to a figure of around 42 basis points. Against those readings, BofA’s own forecast stands at a minimum of 75 basis points of cumulative hikes.

That is a gap of roughly 33-35 basis points. Markets are pricing roughly half the tightening BofA considers necessary.

| Scenario | Implied hikes | End-2026 fed funds range |

|---|---|---|

| Market pricing (mid-July 2026) | ~40-42 bp | ~3.90-4.17% |

| BofA forecast | 75 bp (minimum) | 4.25-4.50% |

| Gap | ~33-35 bp | Significant repricing risk |

The backdrop sharpens the concern. Despite core PCE running at approximately 3.3% and a resilient labour market, the policy rate was 75 basis points lower than a year prior as of mid-2026. BofA argues this makes the market’s current pricing structurally insufficient; policy is already looser than a year ago while inflation is running well above target.

BofA’s baseline includes no easing before 2028, meaning the higher rate level, if achieved, is expected to persist through the entirety of 2027.

If BofA’s forecast proves closer to reality than current market pricing, the repricing event hits rates, yield curves, and risk assets as the September-December 2026 window approaches and the Fed’s path becomes less ambiguous. A 35-basis-point gap between market pricing and a major institution’s documented forecast is not an abstract analytical disagreement. It is a repricing risk that you need to account for before the September FOMC meeting.

The next major ASX story will hit our subscribers first

What BofA’s call means for portfolio decisions in the second half of 2026

BofA’s own framing distinguishes between two questions: which meeting produces the first hike, and whether the full 75 basis points materialises. The bank is clear that the second question is more consequential for positioning. Whether the first move comes in September or later changes the calendar; whether rates reach 4.25-4.50% changes the maths on every rate-sensitive position.

Three variables will most visibly test BofA’s forecast before the September FOMC:

- Subsequent PCE prints: Watch whether core PCE at 3.3% year-over-year proves sticky or begins to soften. This is the single most important data input for the hiking thesis.

- Warsh’s forward guidance: Any communications from the Fed Chair in August or September will signal whether the institutional incentive BofA identified is translating into policy positioning.

- Market repricing progress: Track whether the 40-42 basis point implied pricing begins closing the gap toward BofA’s 75 basis point forecast ahead of September. Early repricing tells you the market is catching up to the view.

The asymmetry in positioning is worth noting:

- If BofA is correct: Underweight-duration and rate-sensitive positioning outperforms. The repricing hits fixed income hardest.

- If markets are correct and hikes do not materialise: The cost of hedging against further tightening is relatively contained, particularly given how low implied volatility has been.

The most actionable takeaway from BofA’s analysis is not whether to believe the 75 basis point forecast wholesale. It is how to size the risk that markets are underpricing tightening, because even a partial repricing toward BofA’s view moves assets.

Duration risk in a hiking cycle is the most direct transmission mechanism from BofA’s forecast to portfolio outcomes; a 75-basis-point move from 3.50-3.75% to 4.25-4.50% reprices long-duration bonds materially more than the 40-42 basis points markets are currently discounting into prices.

Timing is secondary; the destination is the debate

BofA’s call rests on four pillars: core PCE at 3.3%, fading housing disinflation, a new Fed Chair with institutional incentives to tighten, and a market pricing only half the projected hiking path. Not all four need to hold for the thesis to carry weight. Even if the first hike slips past September, the destination, 4.25-4.50% by year-end, remains the variable that reprices portfolios.

The July FOMC decision, while a near-term data point, is not the test of BofA’s thesis. The test is whether core PCE remains sticky into Q3, and what Warsh signals in August and September communications. Those two inputs will determine whether the 33-35 basis point gap between market pricing and BofA’s forecast closes, widens, or stays uncomfortably open.

The positioning window is now. BofA’s baseline calls for no rate cuts in 2027 and no easing before 2028. If that path materialises, investors who waited for September to confirm or deny the call will have already missed the adjustment period. Watch the PCE prints, watch Warsh, and treat the gap between market pricing and BofA’s forecast as the risk variable to size, not a debate to spectate.

For investors wanting to understand the internal Fed dynamics that complicate any single-institution forecast, our full explainer on FOMC committee fractures examines how the April dissent record reshapes the reliability of forward guidance and which asset classes face the sharpest repricing if the committee’s internal divisions persist into the September meeting.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements regarding BofA’s forecasts and projected rate paths are speculative and subject to change based on market developments and Federal Reserve policy decisions.