Why Short Squeezes Send Stocks Parabolic and Then Collapse

2 hrs ago

On 4 March 2026, trading halts hit both the KOSPI and KOSDAQ simultaneously. A dual-market circuit breaker activation of this kind is rare enough that it immediately signalled something beyond an idiosyncratic sell-off. The stress was systemic.

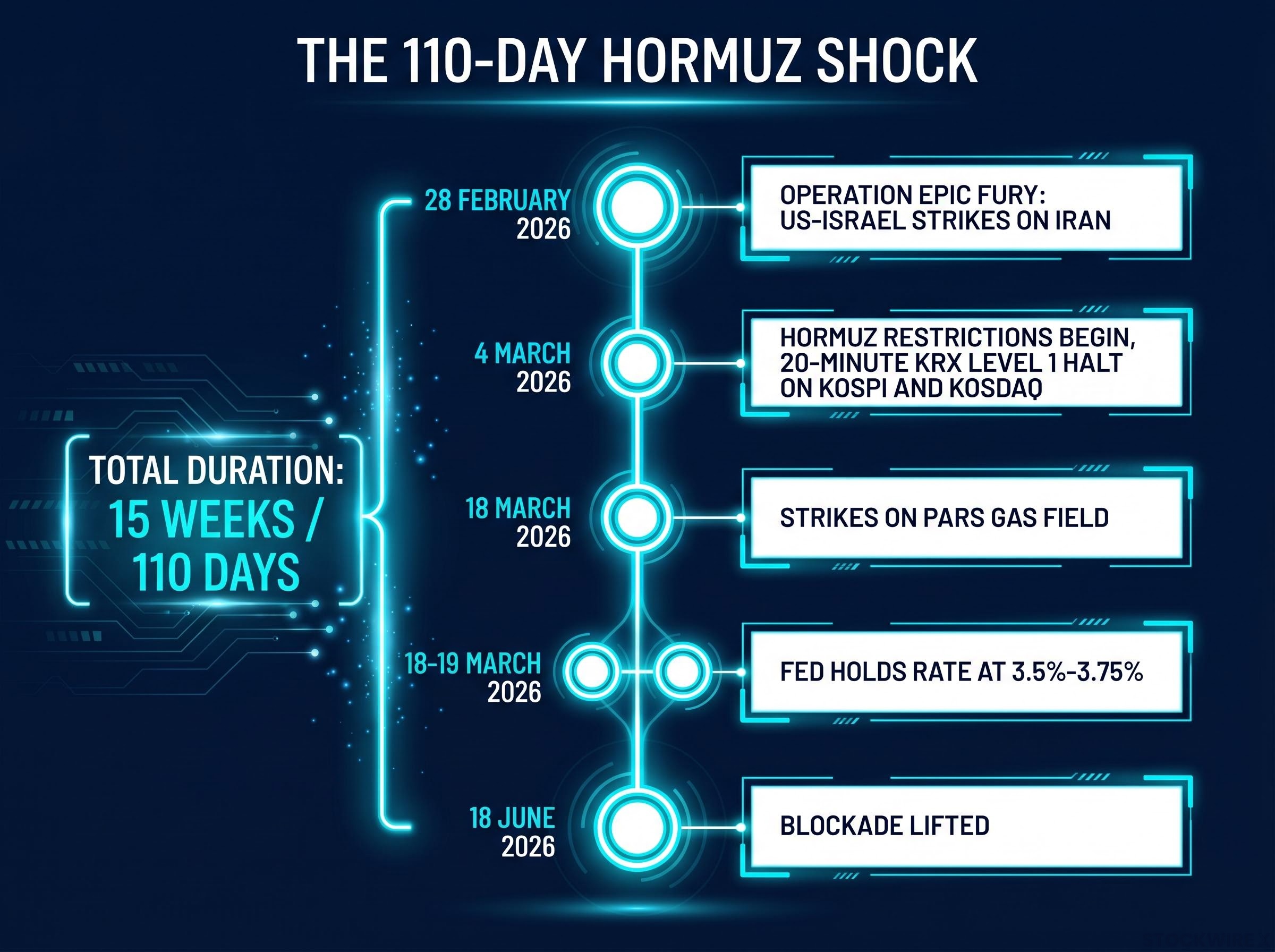

The US-Israel strikes on Iran, initiated on 28 February 2026 under Operation Epic Fury, and the subsequent restrictions on Strait of Hormuz shipping exposed a structural vulnerability that most equity portfolios price as a tail risk rather than a central one. For Asia-Pacific investors, the 110 days between the first strike and the 18 June de-escalation became a live case study in how geopolitical risk transmits through energy-dependent economies and into equity prices.

This analysis traces the mechanism by which a military trigger 5,000 kilometres from Seoul and Tokyo produced double-digit index losses, circuit breaker activations, and concentrated sector collapses. It draws out the repeatable structural lessons for investors carrying Asia-Pacific exposure.

Before the economics, the geography. The Strait of Hormuz is 21 miles wide at its narrowest point. Every tanker transiting between the Persian Gulf and open ocean passes through it. There is no alternative route.

The numbers that define the exposure are difficult to overstate:

EIA Hormuz transit data covering the first half of 2025 recorded average flows of 20.9 million barrels per day through the strait, equivalent to roughly 20% of global petroleum liquids consumption, with 89% of that crude and condensate volume destined for Asian markets, a distribution that maps directly onto the concentrated equity losses observed in Seoul and Tokyo during the 2026 disruption.

Japan’s 90%-plus crude import dependency on Hormuz routing makes the chokepoint a near-total single point of failure for the country’s energy supply.

When Iran declared restrictions on Hormuz traffic effective approximately 4 March 2026, the disruption was not a rumour or a threat. Vessels were rerouted via longer, costlier alternatives. Shipping was physically constrained.

What separated this episode from shorter Middle East flare-ups, where markets tend to recover within days, was duration. The restrictions persisted for approximately 15 weeks, from early March through 18 June 2026. That window was long enough to exhaust inventory buffers, force real supply chain rerouting, and trigger structural repricing rather than temporary volatility.

The 18 March 2026 escalation day, when further strikes targeted Iranian assets including the Pars gas field area, provides the cleanest comparative snapshot. On that single session, the divergence between Asian and Western markets was not marginal. It was structural.

| Index | Move | Period |

|---|---|---|

| KOSPI | -12% | Crisis period, March 2026 |

| Nikkei 225 | -6.3% | Post-outbreak decline, February-March 2026 |

| DAX 40 | ~-8% | February-March 2026 window |

| S&P 500 | -1.36% | 18 March 2026 |

| Dow Jones | -1.63% | 18 March 2026 |

| Nasdaq | -1.46% | 18 March 2026 |

| STOXX 600 | -0.7% | 18 March 2026 |

The gap between a -12% KOSPI drawdown and a -1.36% S&P 500 decline on the same geopolitical event is not noise. It is a function of energy import geography.

Europe sits in between, and the DAX 40’s approximately -8% drawdown across the crisis window reflects a more mixed picture. Post-2022 diversification away from Russian gas, toward LNG imports and accelerated renewables buildout, partially insulated European markets. Some travel and chemical sector names even posted gains during the broader turmoil. The sector damage in Europe was heterogeneous; in Korea and Japan, it was concentrated and severe.

Semiconductor equities are not purely technology risk assets. They carry embedded energy and macro sensitivity that standard sector classification understates. The Hormuz disruption exposed this through four distinct channels:

The Korea Exchange (KRX) activated Level 1 circuit breakers on both the KOSPI and KOSDAQ on 4 March 2026, halting trading for 20 minutes. Simultaneous dual-market activation is rare and signals systemic rather than idiosyncratic stress.

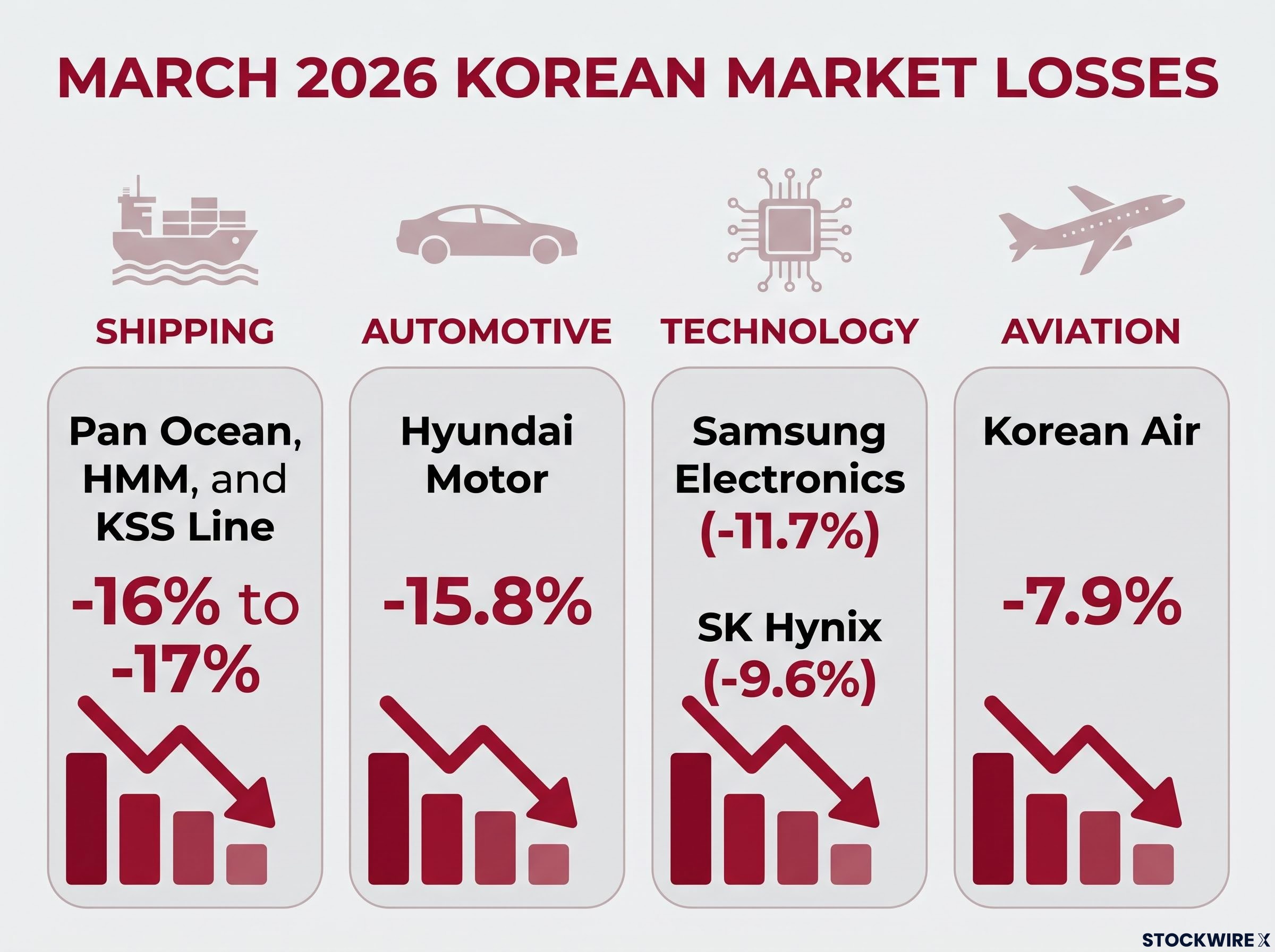

The price data confirms that the transmission channels operated across sectors, not just within semiconductors. Samsung Electronics fell -11.7%. SK Hynix declined -9.6%. Hyundai Motor dropped -15.8%, and Korean Air lost -7.9%.

The shipping sector absorbed the most direct operational hit. Pan Ocean, HMM, and KSS Line each fell between -16% and -17%, reflecting the immediate cost of Hormuz rerouting on companies whose margins are directly tied to freight economics.

Investors who model Samsung or SK Hynix purely as demand-cycle plays will systematically underprice their vulnerability to Middle East supply disruptions. These are technology positions with meaningful energy risk embedded in their cost structures.

The same energy-transmission logic produced semiconductor sell-offs across multiple markets simultaneously, with Samsung Electronics falling roughly 8.6% and ASML declining approximately 4.5% on the same session in May 2026, confirming that the sector’s vulnerability to Hormuz disruptions is not confined to Korean fabs but extends to the global chip supply chain.

Understanding how a military strike in the Persian Gulf becomes a -12% equity drawdown in Seoul requires tracing a sequential chain. Each link is distinct, and the chain only produces severe market outcomes when all links activate:

Duration is the variable that determines whether this chain produces a temporary dip or a structural re-rating. Short disruptions allow inventory drawdowns and forward hedges to absorb the shock. When disruptions last 15 weeks, as this one did, inventories deplete, hedges expire, and the cost absorption becomes permanent enough to force earnings revisions.

The Federal Reserve held its benchmark rate at 3.5%-3.75% at its 18-19 March 2026 meeting, as energy-driven inflation complicated the path to monetary easing.

This rate hold illustrates the compounding second-order effect. Rising energy costs feed inflation, which constrains the central bank’s ability to cut rates, which tightens financial conditions, which applies additional downward pressure on equity valuations. For energy-import-dependent economies carrying dollar-denominated energy costs, the stagflation channel (simultaneous stagnant growth and persistent inflation) amplifies the direct energy cost hit.

Energy-driven inflation and rate policy interact in ways that compound the direct equity impact: when oil costs raise headline CPI, central banks operating under a look-through posture face pressure to signal tightening rather than easing, which tightens financial conditions and applies a second layer of downward pressure on equity multiples in the same markets already absorbing higher energy costs.

The structural asymmetry between KOSPI -12% and S&P 500 -1.36% on the same geopolitical event is the quantitative case for treating Strait of Hormuz disruption risk as a central rather than peripheral factor in any portfolio with meaningful Korean or Japanese equity exposure.

Japan and South Korea’s 90%-plus Hormuz dependency makes this a non-diversifiable systemic risk within Asian equity allocations. Diversifying across Korean sectors does not hedge it. Diversifying across Korean and Japanese markets does not hedge it. The risk is geographic and structural.

The Brent-Dubai benchmark divergence that emerged during the crisis, with Dubai crude reaching approximately $260 per barrel against a Brent price near $108, represents a structural analytical failure point for any cost model built on the global headline benchmark, as Asian refiners, current account projections for Japan and South Korea, and energy-sector earnings estimates were each priced using a figure that understated actual import costs by 140-170%.

Three categories of hedging instruments address distinct channels of the transmission mechanism:

The Europe-versus-Asia comparison also offers a structural relative value framework. European markets, with greater energy diversification following the post-2022 pivot away from Russian gas, demonstrated materially lower sensitivity to the same Hormuz shock. This asymmetry is a positioning input, not merely a post-hoc observation.

The blockade lifted approximately 18 June 2026, following a memorandum of understanding. The immediate crisis resolved. The underlying structural exposure did not.

For investors wanting to trace how the de-escalation actually transmitted into equity prices, our full explainer on the US-Iran truce and Asian equity recovery covers the KOSPI’s 4.6-5.6% single-session rally, the lagged recovery in VLCC hire rates, and the unresolved nuclear track that places a structural ceiling on how far the geopolitical risk premium can decompress.

Five lessons from this episode form an integrated framework for evaluating future geopolitical shocks involving energy supply routes:

The lesson is not to avoid Asian equities when Middle East tensions rise. The lesson is that a specific, identifiable structural dependency produces a quantifiable response function. Investors who model it, hedge it, and incorporate it into position sizing before the next disruption will carry a structural advantage over those who continue to treat it as an unforeseeable shock.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and the analytical framework presented here is subject to revision as geopolitical and market conditions evolve.

Geopolitical risk in the stock market refers to the threat that political instability, military conflict, or international tensions will disrupt economic activity and compress equity valuations. When a geopolitical event restricts a critical supply route like the Strait of Hormuz, the resulting cost increases, demand uncertainty, and risk-off sentiment can reprice equities sharply, particularly in energy-import-dependent markets like South Korea and Japan.

The gap between a -12% KOSPI drawdown and a -1.36% S&P 500 decline on the same geopolitical event reflects a structural difference in energy import geography. South Korea routes over 90% of its crude oil imports through the Strait of Hormuz, making it far more exposed to supply disruptions there than the United States, which has substantial domestic energy production.

Semiconductor equities carry embedded energy sensitivity through at least four channels: higher power costs compressing fab margins, elevated logistics costs from supply chain rerouting, reduced demand expectations as oil shocks raise recession risk, and risk-off selling that hits high-beta technology names disproportionately. During the 2026 disruption, Samsung Electronics fell 11.7% and SK Hynix declined 9.6%, illustrating that chip stocks are energy-sensitive positions regardless of their sector classification.

Simultaneous circuit breaker activation across two markets, as occurred on the KOSPI and KOSDAQ on 4 March 2026, is a rare event that signals systemic rather than idiosyncratic stress. It indicates that selling pressure is broad-based and structural rather than confined to a single sector or company.

Three main categories address distinct transmission channels: downside index options on KOSPI and Nikkei 225 futures provide direct market protection; long crude oil positions act as a natural correlation hedge that appreciates when supply disruptions drive oil prices higher; and currency hedges protect against yen and won depreciation, which is a predictable secondary effect of sustained energy inflation in import-dependent economies.