TSMC just upgraded its 2026 revenue growth guidance to slightly above 40% and announced what U.S. officials are calling the largest single foreign direct investment in American history. Semiconductor stocks sold off in premarket trading anyway.

That is not a contradiction. It is a repricing.

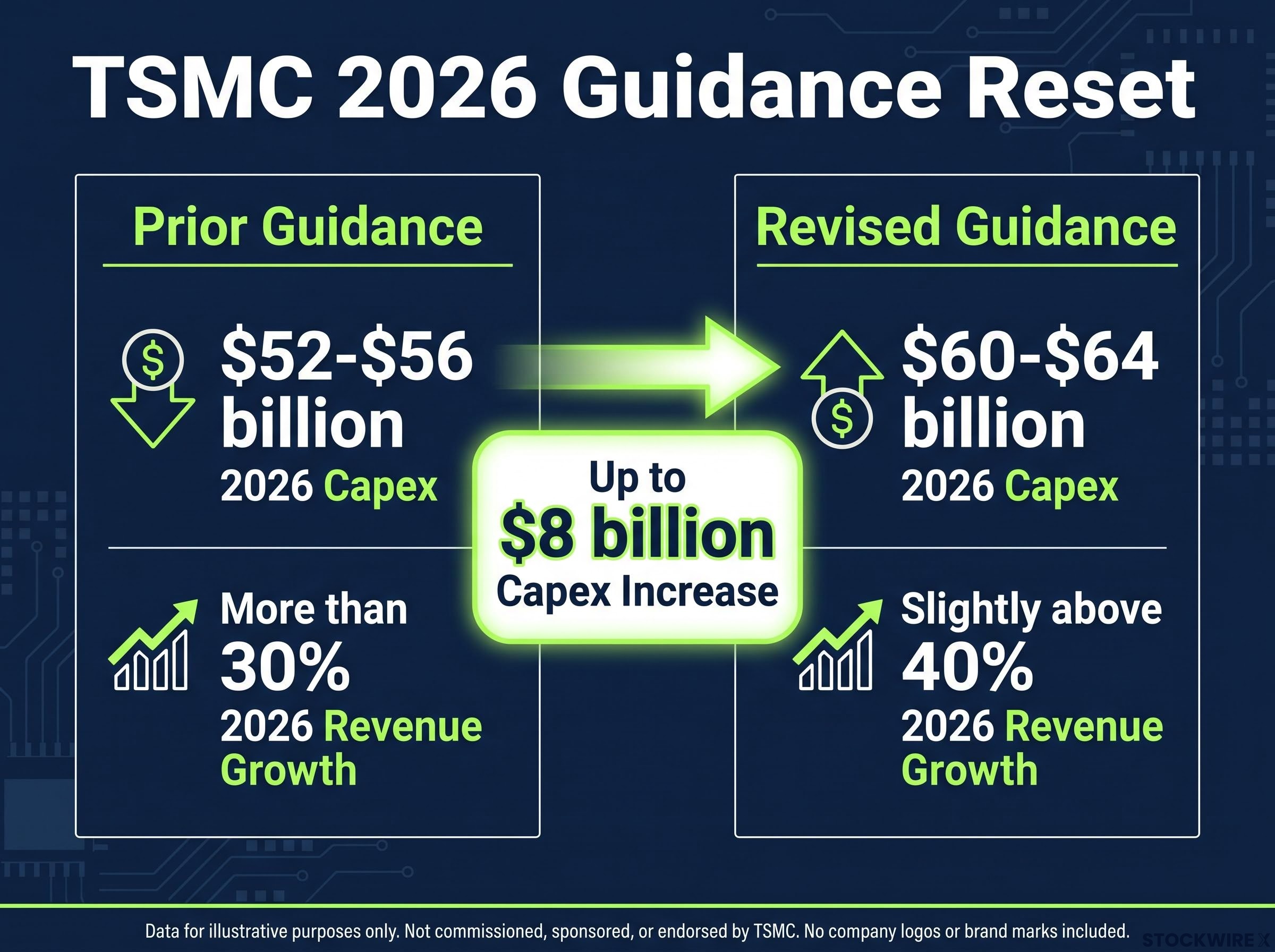

TSMC’s July 16, 2026 earnings release delivered a simultaneous revenue guidance upgrade and a capital expenditure reset to $60-$64 billion, alongside a $100 billion Arizona commitment. The market looked at both numbers, trusted the revenue story, and then recalculated how much of that revenue would actually convert to cash for shareholders. The answer came back lower than the prior multiple assumed.

Here is what the selloff is actually measuring, and what it means for how you think about chip stocks right now.

The capex reset behind the headlines

The numbers tell the story before any interpretation is required. TSMC revised its 2026 capital expenditure guidance upward, moving from a previous ceiling of $52-$56 billion to a fresh range of $60-$64 billion, adding as much as $8 billion to planned spending in one announcement.

| Metric | Prior guidance | Revised guidance |

|---|---|---|

| 2026 capex | $52-$56 billion (upper bound) | $60-$64 billion |

| 2026 revenue growth | More than 30% | Slightly above 40% |

The Arizona commitment extends an existing U.S. expansion programme to approximately $165 billion in total announced investment. The new $100 billion tranche funds:

- Three additional fabs, bringing the Arizona site from three to six total

- Two advanced packaging facilities

- One major R&D centre

TSMC’s chair explicitly acknowledged that U.S. fabs cost materially more to build and operate than equivalent facilities in Taiwan. That cost differential is not a policy footnote. It directly signals that the company is front-loading construction spending on higher-cost soil, which means less cash returning to shareholders and more uncertainty around margin trajectories for the next several years.

The CHIPS Act funding awarded to TSMC Arizona, totalling up to $6.6 billion in direct federal support, further complicates the pure return-on-capital calculation for U.S. fabs, since federal incentives partially offset higher construction costs but introduce their own compliance obligations and domestic-content requirements.

When big ASX news breaks, our subscribers know first

Why strong guidance still triggered a selloff

TSMC raised its full-year 2026 revenue growth outlook to slightly above 40%, a meaningful step up from its earlier projection of more than 30%. Management described AI demand as “extremely robust” in its own words. The stock still fell in premarket trading, and so did every major semiconductor name alongside it.

The revenue story behind the selloff is anchored in genuine outperformance: TSMC’s record Q2 2026 earnings confirmed a 77% year-over-year surge in net profit, accelerating from the 58.3% growth posted in Q1 2026 and establishing that AI chip demand is still building rather than plateauing.

Adam Crisafulli of Vital Knowledge coined the phrase “beat-and-worry” to describe the session: a situation in which record historical results are overshadowed by the market’s concern about what the forward-looking financial resets imply for cash generation.

That framing captures precisely what happened. Sophisticated investors in capital-intensive businesses focus less on reported earnings and more on free cash flow (FCF), the cash a company generates after paying for its operations and capital spending. FCF is what funds buybacks, dividends, and the returns that justify a premium valuation.

When capex rises by up to $8 billion in a single revision, every dollar of that increase is a direct drain on near-term cash available to shareholders. Depreciation from new fabs then compounds that drain for years before utilisation peaks.

Management cited two demand drivers underpinning the guidance upgrade:

- Agentic AI as a catalyst for a revival in CPU demand running in parallel with GPU accelerators across data centre infrastructure

- Continued strength from hyperscaler and cloud customers deploying AI infrastructure at scale

The revenue story is real. What the market is telling you is that it trusts the top line but is discounting the quality of those revenues, because capex intensity means that revenue will not convert to cash at the rate the prior multiple assumed. That distinction changes how you evaluate any “buy the dip” impulse.

What free cash flow compression actually means for chip valuations

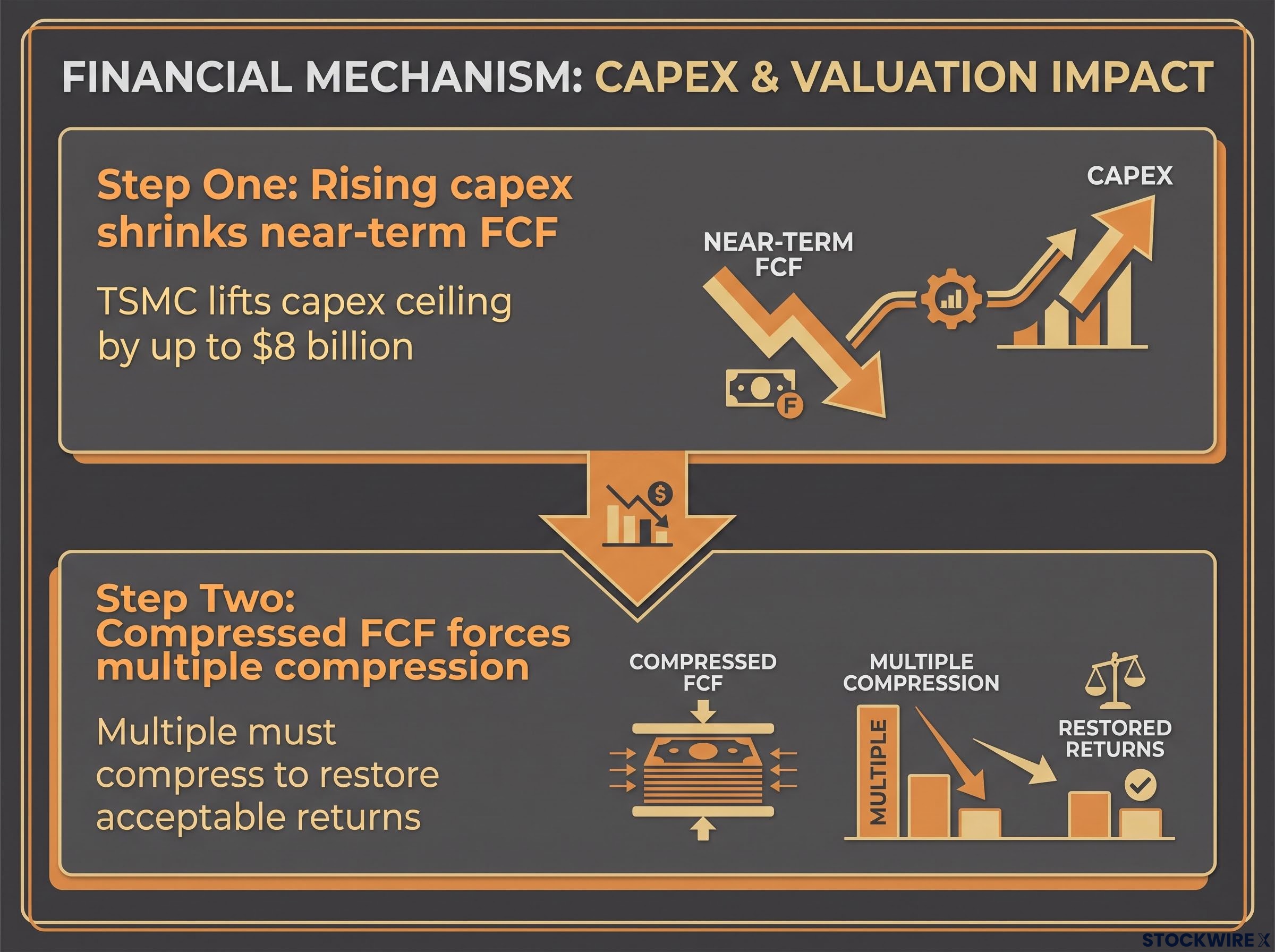

The mechanism runs in two steps, and each one is an inevitable consequence of the previous.

Step one: rising capex shrinks near-term FCF. Every incremental dollar of fab construction is a dollar that does not reach shareholders today. When TSMC lifts its capex ceiling by up to $8 billion, FCF forecasts drop by a corresponding amount, pushing implied FCF yields down at current prices.

Step two: compressed FCF forces multiple compression. Investors who own a stock trading at a premium multiple expect a specific FCF yield to justify that premium. When that yield drops because capex rose, the multiple must compress to restore acceptable returns, even if revenue and earnings-per-share estimates are moving higher.

One analyst noted that a premium-valued company expanding its capex budget forces the market to revise its expectations for future cash returns, with the resulting reduction in anticipated free cash flow providing grounds for the stock’s valuation to de-rate in the near term.

TSM shares ended July 15, 2026 at $419.48, having risen approximately 71% across the prior twelve months, with a total market capitalisation of roughly $1.96 trillion. A stock that has gained 71% in a year carries a valuation that assumes a specific future cash generation profile. When that profile is reset lower, even a small change in assumptions produces meaningful price adjustments at elevated multiples.

The cost-geography amplifier

The front-loaded nature of construction spending creates a timing mismatch that the market prices immediately: costs are incurred now, revenue from new capacity ramps years later. That mismatch is amplified when incremental capex targets higher-cost geographies.

TSMC’s own chair acknowledged that U.S. fab construction and labour costs are structurally higher than in Taiwan. The return on invested capital for the Arizona expansion is therefore less certain than for equivalent Taiwan capacity, which means the FCF compression is not just larger than a Taiwan-based buildout would produce; the confidence interval around it is wider.

How the ripple hits NVIDIA, AMD, Intel, and Micron differently

The premarket declines on July 16, 2026 were not uniform panic. Each name dropped for a specific reason, and those reasons have different durability.

Ranked by size of premarket decline, largest to smallest:

- AMD: approximately 2.7%

- Micron: approximately 2.4%

- Intel: approximately 1.9%

- NVIDIA: approximately 1.3%

| Company | Premarket move (July 16 2026) | Primary exposure mechanism |

|---|---|---|

| NVIDIA | Down ~1.3% | Potential wafer cost pass-through as TSMC’s cost base rises; sector-level multiple reset |

| AMD | Down ~2.7% | Allocation risk and pricing pressure with less purchasing leverage than NVIDIA |

| Intel | Down ~1.9% | Widening manufacturing sophistication gap; independent FCF compression from own capex |

| Micron | Down ~2.4% | Sympathy trading; no direct TSMC dependency |

NVIDIA faces a tension between the bullish fundamental case (more TSMC capacity means more chips shipped) and the near-term repricing logic (potential cost pass-through, sector-level multiple reset). AMD’s largest percentage drop signals that the market is pricing in both cost pass-through risk and weaker purchasing leverage relative to NVIDIA, making its decline a differentiated signal rather than generic sector weakness.

Intel runs its own fabs but still outsources some advanced chips to TSMC. The massive Arizona investment widens the perceived gap in manufacturing sophistication and scale. Intel’s own ambitious capex plans mean the FCF compression logic applies to it independently.

Micron is a memory manufacturer with different supply-demand dynamics and fab economics. It does not rely on TSMC for core production and is not directly affected by Arizona logic-fab costs. Its 2.4% decline is sympathy trading, a meaningfully different signal for investors evaluating that name specifically.

The next major ASX story will hit our subscribers first

Cyclical industry or secular AI story: what TSMC’s bet is really testing

The selloff is also a referendum on an unresolved question, and investors on both sides have legitimate evidence.

Evidence for secular strength:

- TSMC’s guidance upgrade to slightly above 40% revenue growth reflects genuine demand

- Management cited agentic AI specifically as a new demand vector alongside hyperscaler deployments

- TSMC manufactures the overwhelming majority of the world’s leading-edge logic chips, giving it unrivalled visibility into structural demand

Cyclical risk factors:

- Fabs announced today may take several years to reach full utilisation; depreciation and fixed costs begin before revenues peak

- If AI spending decelerates for any reason, whether macro headwinds, technology transitions, or enterprise adoption hurdles, the industry faces overcapacity against a historically large fixed-cost base

- The sheer scale of TSMC’s U.S. commitment amplifies the cost of being wrong on demand timing

The agentic AI signal worth watching

TSMC management cited agentic AI specifically as a driver of renewed CPU demand alongside GPUs. Agentic AI refers to autonomous AI systems that execute multi-step tasks, and they require sustained compute at inference time, not just during training. That creates a different and potentially more durable demand profile than training-only workloads, suggesting a broader hardware demand story than the GPU-centric narrative that dominated 2024 and 2025.

Agentic AI workload demand favours CPU architecture for sequential reasoning and agent orchestration tasks, with industry estimates placing 35-45% of inference workloads as CPU-bound, a dynamic that helps explain why TSMC management cited agentic AI as a catalyst for CPU demand revival alongside continued GPU accelerator growth.

The Arizona commitment functions as a live capital-cycle test rather than resolving the debate. If the U.S. build delivers attractive long-term returns, the secular narrative is validated. If not, this investment will be remembered as a late-cycle overinvestment in a still-cyclical industry. The unresolved tension is precisely the risk the market is pricing, and investors who demand resolution before acting may be waiting for a signal that will not arrive until after the key decision window has passed.

What the selloff changes, and what it does not

Long-term AI demand remains the structural driver. TSMC’s guidance upgrade and management commentary both reinforce this, and the Arizona investment itself reflects confidence in demand durability.

What has changed is the near-term financial framework. FCF is lower than prior models assumed. Execution risk is elevated across three specific categories:

- U.S. fab construction costs and yield ramp timelines

- TSMC margin trajectory as Arizona facilities enter service

- AI capex growth rates at major hyperscalers relative to TSMC capacity additions

The operative valuation lens has shifted from AI-exuberance pricing toward capital-cycle-aware pricing. The question is not whether AI demand is real, but whether current semiconductor valuations already reflect the FCF compression and execution risk that the Arizona programme introduces.

Investors who treat this selloff as either a reflexive buying opportunity or a reason to exit semiconductors entirely are both responding to the wrong signal. The analytical question is whether the new risk profile is priced in, not whether the long-term thesis is intact. Those are different questions, and they produce different answers.

Free cash flow yield evidence and positioning data complicate the simple bubble narrative: Bank of America’s Savita Subramanian documented semiconductor earnings revisions above 20% in 2026 alongside active long-only overweights at roughly half the 2017 cycle peak, suggesting the sector is elevated but not at the positioning extremes that have historically preceded sharp corrections.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.