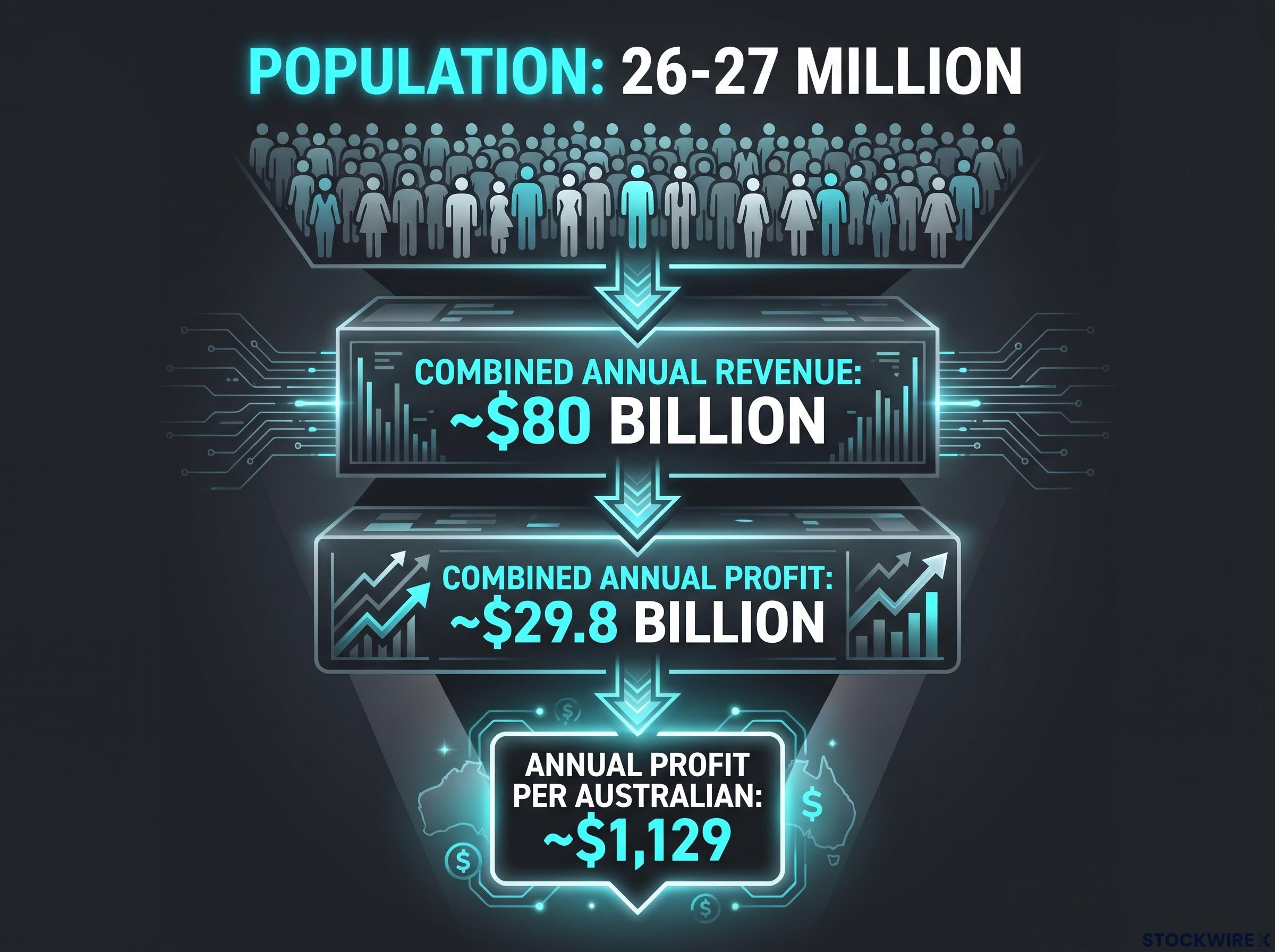

Australia’s Big Four banks collectively generate around $1,129 in annual profit for every person living in the country, a figure that spans infants and pensioners alike. That is not a rounding error or a temporary margin spike. It is what happens when an oligopoly operates inside a market that almost no foreign competitor has managed to crack.

The paradox is hard to ignore. Going back to their early 1990s listings, ANZ, Westpac, and NAB have each posted share price gains exceeding 5,000%, while CBA has surpassed 15,000%, and neither figure accounts for dividends or franking credits. Yet the consensus framing remains: mature income stocks, limited growth. The question is whether that label is about to change, and whether the catalyst is already being priced in.

Here is what the data actually tells you about where these banks sit today, whether the AI cost thesis changes the investment character of the sector, and what specific risks to weigh before acting on either view.

A protected market that almost no outsider has cracked

Australia’s Big Four banks operate inside what amounts to a sealed domestic corridor. The structural protections are specific and self-reinforcing:

- Small market population: At roughly 26-27 million people, Australia does not offer the scale that would justify a major international bank building a competing retail franchise from scratch.

- Absence of international competition: No international bank has found the Australian retail market compelling enough to mount a serious challenge, and the Big Four themselves wound back their own offshore ambitions, closing out most of their UK operations and pulling focus back to their home market, where they have remained ever since.

- Implicit government backstop: These institutions are considered too systemically important to fail, providing a regulatory stability floor that most industries simply do not enjoy.

Just four institutions together generate annual profit equivalent to roughly $1,129 for every Australian, babies included, a figure that underscores the extraordinary earnings density of this market.

Combined annual revenue across the four sits at approximately $80 billion, generating combined annual profit of approximately $29.8 billion. When a small, closed market produces that level of extraction, the structural advantage compounds in ways that are genuinely difficult for new entrants to disrupt. That is precisely why these stocks have delivered returns that look impossible on paper: the moat is not a single feature but the interaction of all three protections reinforcing each other over decades.

APRA’s ADI performance statistics for the year ending June 2024 confirm the sector’s profitability floor, with aggregate net profit after tax and return on equity figures that align with the extraordinary earnings density described above.

When big ASX news breaks, our subscribers know first

What makes these banks the backbone of Australian income portfolios

The income case is not complicated, but the mechanics matter. Because the Big Four operate in a mature domestic market with few outlets for high-return reinvestment, capital that cannot be deployed productively gets returned to shareholders instead. The result is payout ratios that rank among the highest globally, a structural outcome driven by the absence of attractive reinvestment alternatives rather than any particular boardroom generosity.

| Metric | 1H26 | FY24 | Context |

|---|---|---|---|

| Combined profit after tax | $15.2 billion | $29.9 billion | 1H26 down 2.1% on 1H25 |

| Average return on equity | 10.7% | Above 10% | CBA exceeds sector average |

The profitability floor is real: KPMG’s 1H26 analysis confirms the Big Four remain highly profitable cash-generating franchises, even as profits drift modestly lower in the near term.

How franking credits change the effective yield calculation

Franking credits are where the income story becomes personal. When an Australian company pays corporate tax on its profits, the dividends it distributes carry a tax credit reflecting that tax already paid. For most investors, this means the dividend is not taxed twice.

The gap between headline cash yield and grossed-up dividend yield is where the income story for pension-phase investors becomes structurally compelling; NAB’s $1.68 fully franked cash dividend, for instance, carries a grossed-up value of $2.40 once the attached franking credit is included, shifting the effective return calculation by more than 40%.

In pension phase, though, the mechanics are considerably more favourable. With a tax rate of zero, these investors are entitled to receive unused franking credits back from the ATO as an actual cash payment, not simply a reduction in tax owed. The practical effect is that the real yield on bank dividends for this cohort sits meaningfully higher than the headline figure implies.

This is the specific reason the Big Four dominate Australian income portfolios. It is also the reason any legislative change to franking credit refunds would be a genuine material risk to effective yields for this investor cohort, not a theoretical one. The mechanism remains current law, but it has been subject to intense political debate in recent election cycles.

The one thing holding back a sector with everything else going for it

The structural income story is strong. The growth story is not. That tension deserves honest treatment.

When it comes to capital growth, the Big Four are not where accumulation-phase investors should be anchoring their expectations. Profits are essentially flat, with combined profit after tax down 2.1% in 1H26 against 1H25, and investors seeking to compound wealth rather than draw income will generally find more traction elsewhere in the market.

Then there is the valuation question. The sector’s price-to-earnings multiples have expanded considerably from historical norms, with current multiples having approximately doubled relative to where the sector used to trade.

The persistence of elevated multiples across the sector, and particularly CBA’s P/E of approximately 28.9x versus a sector average of 18x, reflects structural factors that standard valuation models consistently fail to price forward, including oligopoly margin resilience and management quality premiums that historical earnings-based approaches cannot fully capture.

The S&P/ASX 200 Financials index returned 23.3% over the past year versus 15.8% for the broader ASX 200.

That outperformance tells you something specific: investors have already voted with capital on the AI cost thesis. The question is whether you are buying into a story that has already run, or whether the actual savings delivery still justifies current prices.

Three constraints define the ceiling:

- Marginal near-term growth: Profits are flat to slightly declining, not expanding at multiples consistent with re-rating.

- Elevated multiples versus historical norms: The margin for negative surprises is thinner than it has been in years.

- Partial AI pricing already embedded: The sector’s outperformance suggests the market has already partly priced the cost-cut thesis.

How AI turns a cost line into an earnings catalyst

Of all the sectors exposed to AI-driven automation, banking ranks among the most vulnerable to disruption from within its own cost base. A substantial share of banking employees spend their working hours on structured, repeatable tasks such as loan processing, compliance checks, document handling, customer queries, and fraud detection, functions that sit squarely in the zone where AI tools produce the fastest and most measurable efficiency gains.

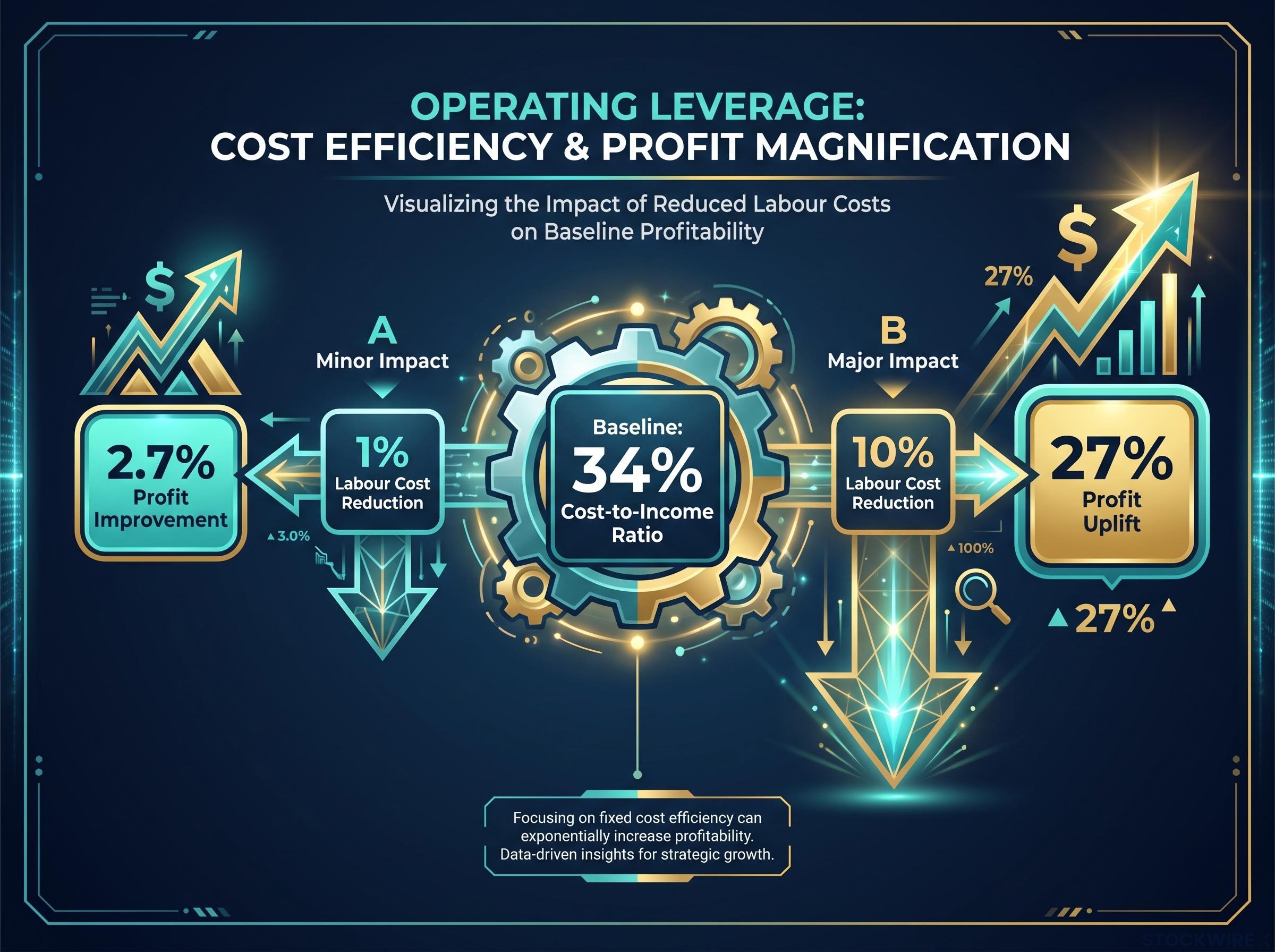

The operating leverage mechanism is what makes even modest cost savings disproportionately powerful. Here is how the arithmetic works:

- Baseline cost structure: The Big Four carry a cost-to-income ratio of around 34%, so for every dollar of revenue generated, approximately one third is absorbed by operating expenses, with labour the dominant component.

- The leverage effect: Because cost reductions fall directly to the bottom line in a high-margin lending business, trimming labour costs by 1% produces a profit improvement of roughly 2.7%, a magnification effect that stems from the structure of the model itself.

- Illustrative upper-case scenario: Carrying that logic further, a 10% reduction in labour costs would imply approximately 27% profit uplift through that same leverage. This is best understood as an illustrative stress test, not a base case.

Multiple independent research sources have sized the opportunity:

| Source | Metric | Estimated range | Time horizon |

|---|---|---|---|

| Macquarie | Annual profit gains | 3-15% | 5-10 years |

| Citi | Profit uplift | ~9% | Widespread GenAI adoption |

| McKinsey | Revenue-equivalent productivity | 2.8-4.7% of revenue | GenAI deployment period |

NAB reduced a 45-minute trust-deed review to approximately one minute using AI, while call-centre operations now handle 50% more queries with AI support and 24/7 availability.

Even the conservative end of published estimates, a 3-9% profit uplift, would be material for a sector trading at elevated multiples. But the gap between potential and delivered depends entirely on implementation. The savings are real in targeted deployments. Whether they scale across entire organisations is the question that current valuations are betting on.

The next major ASX story will hit our subscribers first

What the market has already priced, and what still needs to be delivered

The market is not waiting for AI savings to appear in profit-and-loss statements before rewarding them in share prices.

Bendigo and Adelaide Bank shares jumped 10% after announcing plans to cut its wage bill by 10% through AI-based automation, targeting savings of up to $75 million per year by 2028.

That reaction tells you the market’s sensitivity to this theme is high. NAB and other majors have framed ongoing job-cut programmes explicitly as part of a new cost-control cycle, and share prices have responded positively. The risk of being late to the trade is real, but so is the risk of paying a premium for savings that remain a management ambition rather than a delivered outcome.

The risks that could delay or dilute the thesis are specific:

- Execution risk: Past technology-led efficiency programmes in banking have frequently delivered less than promised. Adding AI tools on top of legacy systems is not the same as reducing costs.

- Regulatory and governance risk: The RBA has noted that well-governed AI applications can enhance financial stability, but enforceable standards for high-risk uses are needed. Mismanaged AI could trigger compliance cost increases that dilute savings.

- Workforce and political constraints: Macquarie’s scenario implies replacing up to 30% of staff over 5-10 years. Union, workforce management, and political scrutiny could constrain the pace.

- Franking credit policy risk: Any move to limit franking refunds for pension-phase investors would directly reduce effective yields for the cohort most reliant on bank dividends.

AI governance failures documented by APRA across the $9.8 trillion in assets it supervises, including a superannuation fund that misclassified vulnerable members and an insurer whose pricing model lacked independent validation, illustrate precisely the compliance cost risk that could dilute efficiency savings before they reach the bottom line.

Three conditions that would confirm the thesis is delivering

- Sustained cost-to-income ratio improvement: Measurable, consistent reduction in the ratio, not just AI spending announcements or pilot programme press releases.

- Disciplined capital policy: High payout ratios maintained while allowing incremental profit growth, giving investors income and total return simultaneously rather than forcing a trade-off.

- Absence of major shocks: No credit, regulatory, or governance events that add compliance costs and dilute the savings story.

Where the Big Four fit in a reassessed income portfolio

The Big Four remain among the most reliable dividend payers on the ASX. An average return on equity of 10.7% in 1H26, high payout ratios, franking credit advantages, and a structural oligopoly supporting the earnings floor confirm the income case.

But the sector does not serve every investor profile equally.

| Profile | Income case strength | AI thesis relevance | Key risk to monitor |

|---|---|---|---|

| Pension-phase income investor | Strong (franking refunds lift effective yield) | Adds optionality to an already compelling holding | Franking credit policy changes |

| Accumulation-phase investor | Moderate (franking offset, not refund) | Must justify elevated entry multiple | Valuation compression if AI savings disappoint |

For an investor already holding these banks for income, the AI thesis changes the holding rationale at the margin but does not invalidate it. For an investor considering entry at current valuations, the question is whether the AI optionality is worth paying the elevated multiple. The honest answer depends on your tax position, your time horizon, and your tolerance for a thesis that has already partially run.

Investors exploring whether current multiples are defensible at the individual stock level will find our comprehensive walkthrough of ASX bank stock valuation stress-testing useful, as it combines PE and DDM models with a qualitative checklist covering capital adequacy, arrears trends, and macro sensitivity for each major bank.

The monitoring checklist is straightforward:

- Cost-to-income ratio trajectory across reporting periods

- Credibility of headcount reduction announcements versus actual delivery

- Regulatory response to AI deployment in financial services

- Franking credit policy signals from both major parties

Macquarie’s 5-10 year timeframe for the staff replacement scenario sets the patience horizon. Should AI-driven cost reductions arrive at the scale that published research suggests, these banks could credibly transition from pure income holdings into something that also offers earnings growth, a meaningful change in how the sector is characterised and valued. That is worth monitoring. Whether it is worth paying today’s price for is a question only your specific circumstances can answer.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—