US Strikes 60 Iran Targets as Brent Crude Breaks $80

17 hrs ago

Australia’s financial regulator has fired a formal warning shot at every bank, insurer, and superannuation fund under its watch. The Australian Prudential Regulation Authority’s (APRA) System Risk Outlook 2026, published on 21 May 2026, finds that artificial intelligence deployment across the $9.8 trillion in assets APRA supervises is outrunning the governance frameworks meant to control it. The finding is not theoretical. APRA’s thematic reviews have already documented specific governance failures, AI-enabled cyber incidents have appeared in the regulator’s reporting pipeline, and industry leaders from ANZ to AustralianSuper have acknowledged the gap publicly. What follows unpacks APRA’s findings, the dual risk AI now presents (as both a governance failure and a weaponised attack vector), the cases already on record, and what regulated entities should expect as APRA intensifies supervision through the remainder of 2026.

APRA’s language left little room for interpretation.

“AI and machine-learning deployment is expanding faster than the maturity of governance and control frameworks.”

Thematic reviews of data, AI, and model risk conducted across 2025-26 found that a significant proportion of reviewed entities could not demonstrate that their boards had clearly defined AI risk appetite, assigned accountability lines, or established reporting structures for AI systems. The gap was not confined to smaller institutions; APRA noted material variation across the sector.

Three categories of governance shortfall appeared repeatedly:

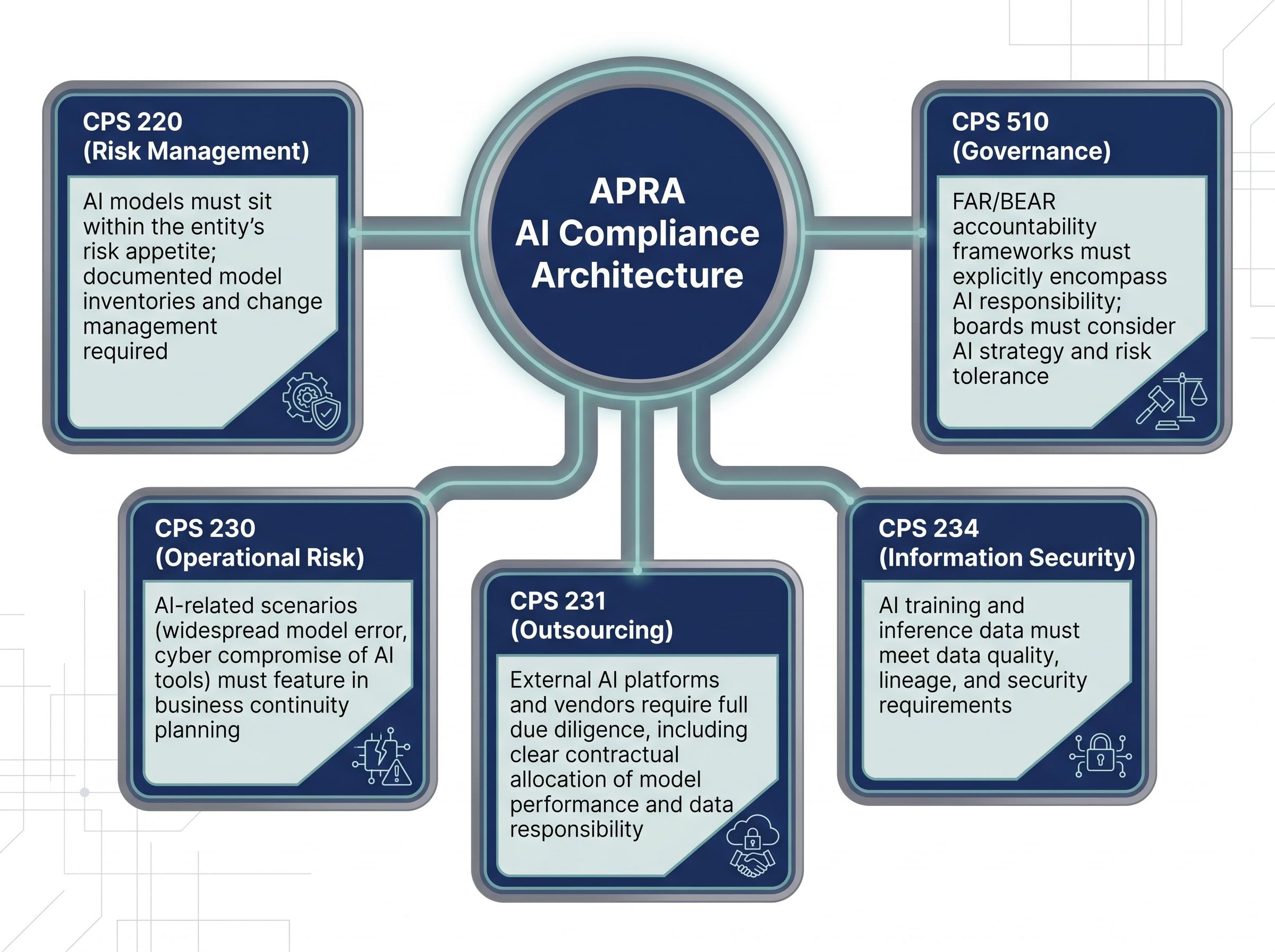

APRA stressed that it was not introducing new standards. Existing obligations under CPS 220 (Risk Management), CPS 230 (Operational Risk Management), and CPS 510 (Governance) already require what institutions are failing to demonstrate. The regulator’s position is that the deficiency is one of execution, not of regulation.

APRA’s prior letter to industry, issued in approximately April 2026, did not create an AI-specific prudential standard. Instead, it mapped five existing standards onto AI systems and told regulated entities the obligations are already in force.

APRA’s April 2026 supervisory letter had already placed the question of AI risk controls across Australian banks, insurers, and superannuation trustees squarely in the enforcement frame, warning that material inadequacies under existing prudential standards would attract intensified oversight rather than a grace period for voluntary uplift.

APRA’s letter to industry on AI, published on 30 April 2026, maps governance, cybersecurity, supplier reliance, and AI literacy obligations onto existing prudential standards, confirming that regulated entities face enforcement exposure under frameworks already in force rather than any forthcoming AI-specific standard.

The practical effect is a compliance architecture that spans governance, risk, outsourcing, information security, and board accountability. The table below summarises how each standard applies.

| Prudential Standard | Core Obligation | AI Application |

|---|---|---|

| CPS 220 (Risk Management) | Sound risk management framework | AI models must sit within the entity’s risk appetite; documented model inventories and change management required |

| CPS 230 (Operational Risk) | Operational resilience and continuity | AI-related scenarios (widespread model error, cyber compromise of AI tools) must feature in business continuity planning |

| CPS 231 (Outsourcing) | Due diligence on material outsourcing | External AI platforms and vendors require full due diligence, including clear contractual allocation of model performance and data responsibility |

| CPS 234 (Information Security) | Information security capability | AI training and inference data must meet data quality, lineage, and security requirements |

| CPS 510 (Governance) | Board and senior management governance | FAR/BEAR accountability frameworks must explicitly encompass AI responsibility; boards must consider AI strategy and risk tolerance |

Entities must also be able to provide sufficiently explainable outputs for AI-driven decisions affecting customers, particularly where those decisions involve credit, pricing, or claims and where customers are adversely affected.

APRA identified a heightened dependency on external AI platforms and vendors, with contracts that do not clearly allocate responsibility for model performance and data protection. Offshore data processing and AI development providers drew particular concern. CPS 231 and CPS 234 due-diligence obligations apply in full to these arrangements, and APRA’s thematic reviews found compliance uneven.

Vendor concentration risk amplifies each of these exposures: when a single external AI provider underpins fraud detection, credit decisioning, and compliance monitoring across multiple institutions simultaneously, a disruption at the provider level cascades in ways that no individual institution’s business continuity plan can absorb on its own.

The governance gap is only half the picture. APRA’s Outlook documented AI being used against regulated entities, not just within them.

AI-enabled phishing and impersonation attacks targeting APRA-regulated entities increased in late 2025 and early 2026. The documented incidents fall into four categories:

AI voice cloning scams costing Australians an estimated AUD 25.8 million in the first half of 2025 underscore the scale of the threat APRA documented, with scammers using generative AI to produce highly convincing impersonations that bypass verification procedures that financial institutions had previously regarded as robust.

APRA warned that generative AI tools used internally are sometimes connected to sensitive datasets “without adequate access controls, monitoring, or data-loss prevention.”

The dual exposure matters because entities that have separated their cyber risk and AI governance work streams now face a regulator that views them as two sides of the same supervisory concern.

APRA’s Outlook moved beyond aggregate findings to describe specific governance failures across sectors, each anonymised but detailed enough to illustrate the pattern.

Both cases illustrate the board oversight and model risk findings from APRA’s thematic reviews. Industry data from a 2025 KPMG Australian Banking Outlook report indicated that approximately 40% of surveyed Australian banks had a formal board-approved AI governance framework distinct from general IT governance, a figure that, if accurate, aligns with APRA’s finding that a significant proportion of entities lack the structures the regulator expects.

For the general insurer, APRA mandated formalised model-risk policies, independent validation of the pricing model, and expanded board reporting on AI system performance. APRA framed these as applications of existing CPS 220 and CPS 230 requirements, reinforcing that remediation was not about meeting a new standard but about complying with one already in force.

Responses from across banking, insurance, and superannuation confirmed APRA’s findings rather than contesting them.

A 2025 Deloitte Australia survey found only 32% of surveyed Australian banks, insurers, and superannuation funds assessed themselves as “advanced” or “leading” on AI governance. Even well-resourced institutions are acknowledging shortfalls.

Board-level AI literacy sits at the centre of APRA’s critique, with the regulator identifying over-reliance on vendor-supplied summaries as a structural conflict that prevents boards from independently challenging management risk assessments, a pattern APRA flagged explicitly in its April 2026 supervisory letter alongside warnings that Australia’s principles-based regulatory posture may not persist if governance gaps continue.

Director liability dimension “APRA’s AI expectations go beyond mere guidance and effectively set a benchmark for directors’ duties in overseeing AI,” said Dr. Maria O’Brien, Partner at King & Wood Mallesons.

APRA has declared it will intensify supervision of AI use through the remainder of 2026, including targeted reviews and potential deep-dive examinations of high-impact AI deployments in credit, pricing, underwriting, and claims.

APRA noted that AI-related incidents are “under-reported” because entities often categorise them under broader operational or cyber events, an observation that suggests internal classification practices themselves require review.

Professor Allan Fels, former ACCC Chair, called for “closer coordination between APRA, ASIC, and the ACCC” to address the regulatory overlap that AI creates across prudential, conduct, and competition frameworks (ABC News, 22 May 2026).

Three immediate priorities emerge from the Outlook for regulated entities:

The next System Risk Outlook is expected toward the end of 2026, providing the next public accountability checkpoint for whether institutions have closed the gaps APRA has now formally documented.

APRA’s System Risk Outlook 2026 has converted what many institutions treated as an emerging risk into a documented supervisory finding with named sectors, specific case studies, and a declared programme of intensified oversight. AI presents a dual challenge: internally, governance frameworks are not keeping pace with deployment; externally, AI-enabled attack tools are already appearing in APRA’s incident pipeline.

The systemic stakes are proportionate to the $9.8 trillion in assets APRA oversees. Governance failures at individual banks, insurers, or superannuation trustees carry consequences for depositors, policyholders, and fund members across the system. APRA’s deep-dive reviews are expected to produce supervisory findings by the time the next Outlook is published, likely toward the end of 2026. For boards and compliance teams, the window between warning and examination is narrowing.

Investors and compliance professionals wanting to understand the sector-wide structural dimensions of these findings will find our deep-dive into AI systemic risk across the financial sector, which examines how a single dominant AI provider failure could simultaneously impair fraud detection, credit decisioning, and compliance monitoring across the full $9.8 trillion asset base APRA oversees, and why individual institution compliance cannot close the structural gap.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

APRA AI risk refers to the governance, operational, and cybersecurity exposures that arise when banks, insurers, and superannuation funds deploy artificial intelligence systems without adequate oversight frameworks. APRA's System Risk Outlook 2026 found that AI deployment is outpacing governance maturity across the $9.8 trillion in assets it supervises, making it a formal supervisory concern rather than an emerging one.

APRA has mapped AI obligations onto five existing prudential standards: CPS 220 (Risk Management), CPS 230 (Operational Risk), CPS 231 (Outsourcing), CPS 234 (Information Security), and CPS 510 (Governance). No new AI-specific standard has been introduced; entities face enforcement exposure under frameworks that are already in force.

APRA documented failures including boards that had not defined AI risk appetite, inconsistent independent validation of high-impact credit and pricing models, and inadequate documentation of training data sources. Specific cases included a superannuation fund that misclassified vulnerable members using a biased AI model, and a general insurer whose AI pricing model lacked proper validation and accountability.

APRA documented multiple AI-enabled attack types in late 2025 and early 2026, including voice cloning used to impersonate bank staff, generative AI-crafted phishing emails targeting privileged-access employees, internal code leakage via public AI tools, and a chatbot that exposed sensitive customer health data. AI voice cloning scams alone cost Australians an estimated AUD 25.8 million in the first half of 2025.

APRA identified three immediate priorities: boards must formally document AI risk appetite, accountability lines, and reporting structures under CPS 220 and CPS 510; independent validation must be consistently applied to AI models used in credit, pricing, and claims decisions; and contracts with external AI vendors must clearly allocate responsibility for model performance, data protection, and incident notification under CPS 231 and CPS 234.