You wake up, open your brokerage app, and the screen is red. Not a little red. The kind of red that makes you check whether something broke overnight. Then you see the headline: “Yen carry trade unwind accelerates” or “Japan confirms fresh currency intervention.” Your thumb hovers over sell.

This moment has played out repeatedly over the past two years, and it will play out again. Two stories about the yen circulate in cycles, each internally coherent, each treated as urgent, and each with a track record of failing to produce the outcome it predicts. The first says government yen-buying interventions can stabilise the currency. The second says yen strengthening triggers a cascading carry-trade unwind that crashes global equities. Both move markets. Neither has delivered on its promise at the medium-term horizon.

Here is a structural framework for reading these stories clearly. The next time a yen headline lands on your screen, you will know which three questions to ask before touching your portfolio, and why the answers matter more than the headline itself.

The two yen stories markets keep telling themselves

The catastrophic carry unwind narrative runs like this: the yen appreciates sharply, and investors holding yen-funded positions in higher-yielding overseas assets face rising repayment costs, forcing them to liquidate those positions, and equity markets crash in a cascade. It is a clean story. It has a trigger, a mechanism, and a punchline.

The currency intervention narrative is equally tidy: the Japanese government steps in, buys yen on the open market, sets a floor, and the weakening trend reverses. Crisis managed, stability restored.

Both stories have genuine short-term market-moving power, precisely because they are internally coherent. In a fast-moving market, coherence is often enough to move prices, even when the underlying premise is weak.

Market pricing ahead of the hike captured a dynamic the current article’s framework anticipates: prediction markets assigned a 95-98% probability to the June 25-basis-point move, yet the Nikkei 225 still surged approximately 5.4% on the eve of the decision as investors focused on forward guidance over the rate step itself, illustrating how narrative heat can move prices independently of fundamentals.

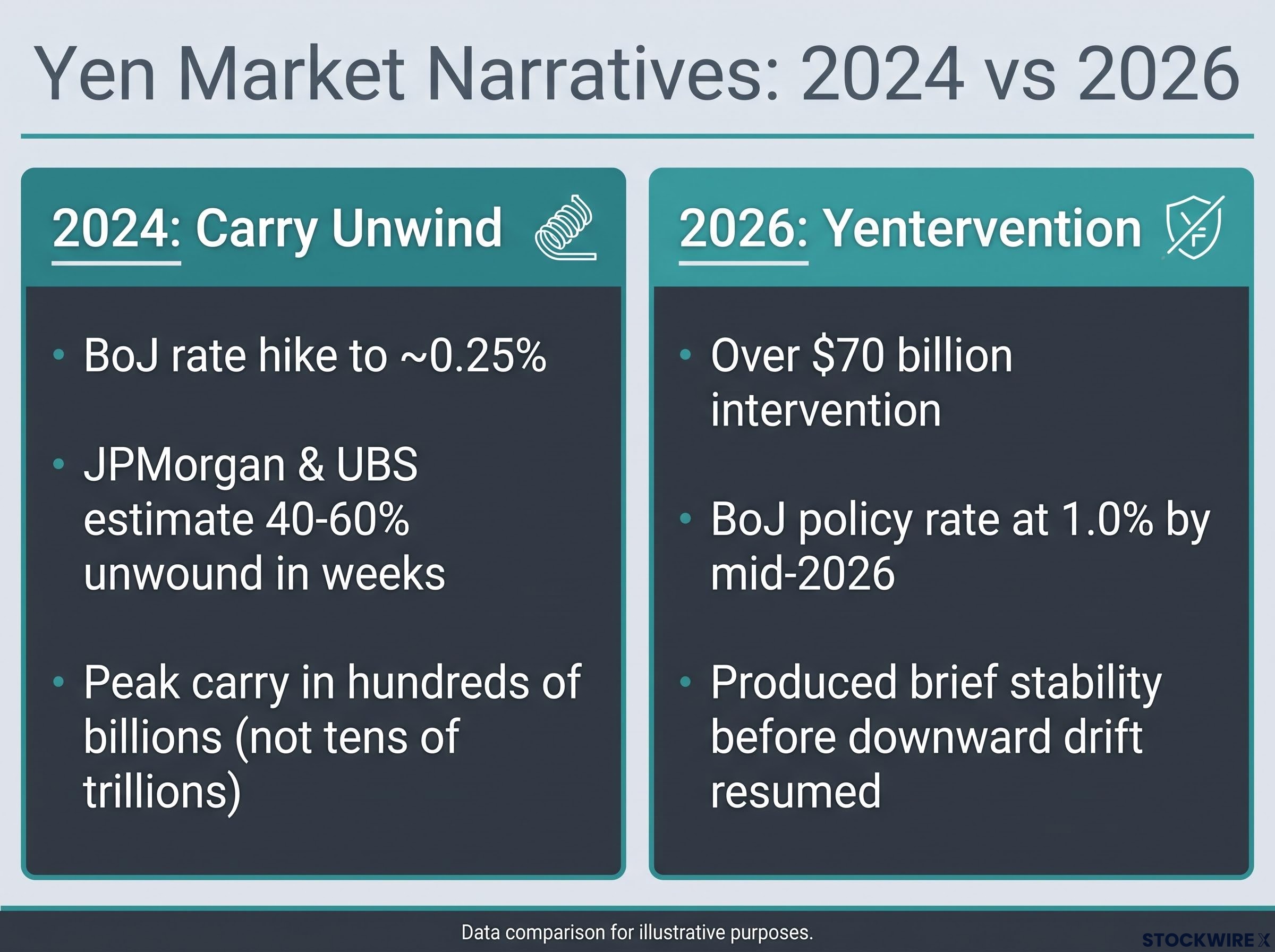

- Catastrophic carry unwind: Predicts cascading global equity sell-offs when yen strengthens. Track record: the 2024 unwind produced sharp volatility but resolved within weeks without structural breakdown.

- Heroic yentervention: Predicts durable currency stabilisation after government purchases. Track record: the 2026 intervention exceeded $70 billion and produced brief stability before the yen resumed its downward drift.

Why both beliefs share the same weakness

Both narratives assume a level of control over yen direction, either by governments or by the mechanics of carry unwinding, that the data consistently fails to support. The rest of this analysis unpacks why that assumption keeps breaking down, and what to watch instead.

When big ASX news breaks, our subscribers know first

What the 2024 carry-trade episode actually showed

In mid-2024, the Bank of Japan (BoJ) surprised markets with rate hikes to approximately 0.25% and signalled reduced bond-buying. The move narrowed rate differentials between Japan and the United States and pushed the yen sharply higher. That triggered a rapid unwind of yen-funded carry positions and a notable global equity sell-off.

The immediate reaction was severe. Volatility spiked across both US and Japanese equities. Some analysts described the episode as the unwinding of “the biggest carry trade the world has ever seen.”

“The biggest carry trade the world has ever seen.”

The label was dramatic. The numbers told a more measured story. JPMorgan and UBS strategists estimated that roughly 40-60% of speculative carry positioning had already been unwound within a couple of weeks. Peak dollar-yen carry, according to multiple strategist estimates, sat at hundreds of billions of dollars, not tens of trillions.

The BIS analysis of the 2024 carry trade unwind corroborates the scale question directly, noting that while deleveraging pressures were real and measurable, the episode’s systemic implications were constrained by the trade’s concentration among speculative rather than systemically critical market participants.

| Phase | What happened | Key data point |

|---|---|---|

| Trigger | BoJ surprise rate hike to ~0.25%, reduced bond-buying | Narrowed US-Japan rate differential |

| Immediate response | Rapid carry unwind, global equity sell-off | 40-60% of speculative positioning unwound in weeks (JPMorgan, UBS) |

| Resolution | Equity markets recovered; no cascading liquidation | Peak carry estimated at hundreds of billions, not tens of trillions |

Those scale figures matter for you directly. They reframe what “biggest carry trade in history” actually means in dollar terms: large enough to cause real short-term pain, but not large enough to destabilise global capital markets. The 2024 episode is the most recent stress test of the catastrophic unwind narrative, and its resolution gives you a concrete precedent the next time the same story circulates.

The mechanics behind the trade (and why its reach is limited)

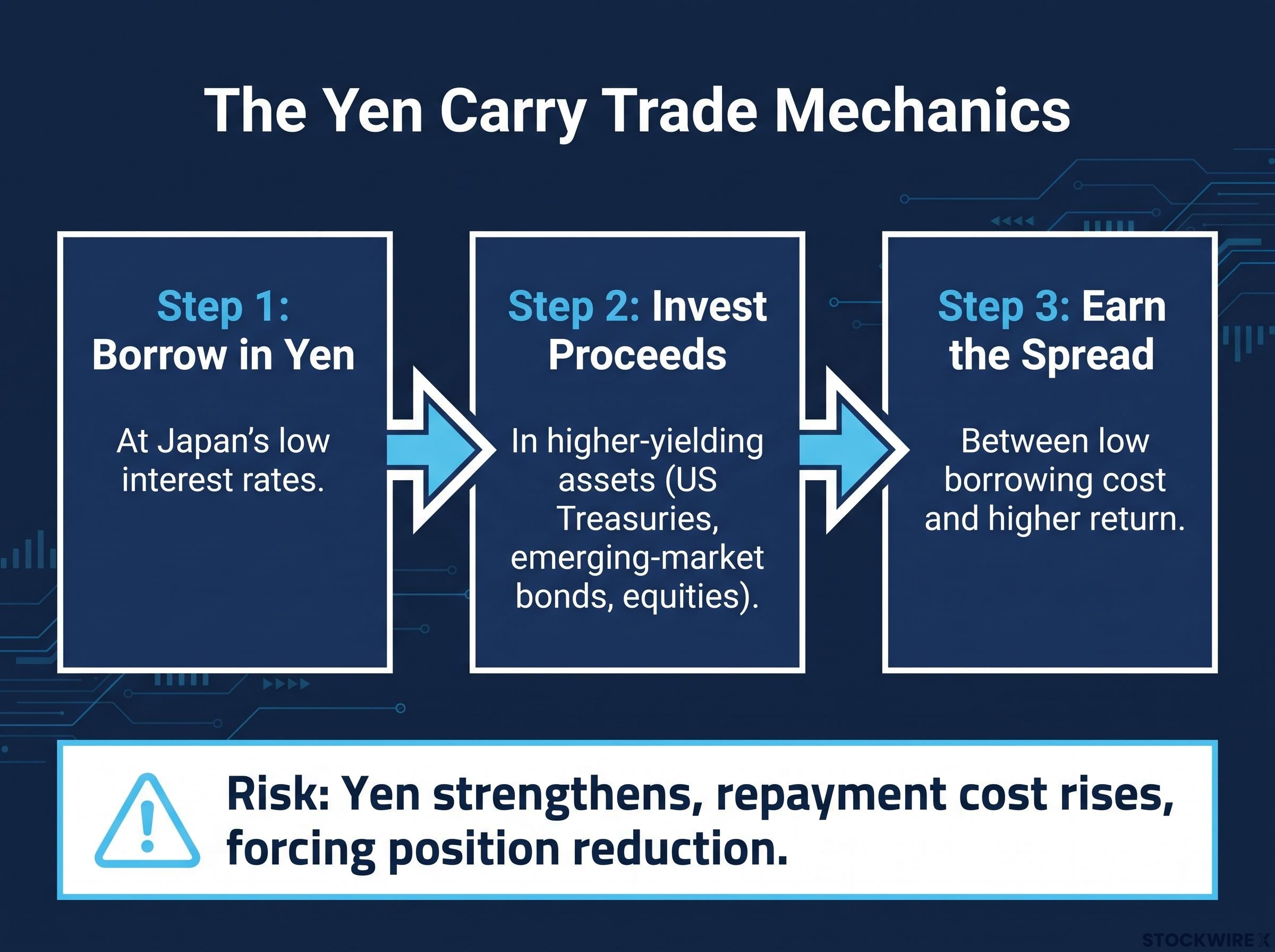

The yen carry trade works in three steps:

- Borrow in yen at Japan’s low interest rates.

- Invest the proceeds in higher-yielding assets elsewhere (US Treasuries, emerging-market bonds, equities).

- Earn the spread between the low borrowing cost and the higher return, while absorbing the risk that the yen strengthens against your investment currency.

When the yen does strengthen, the trade becomes painful. The cost of repaying the yen-denominated loan rises in foreign-currency terms, which forces position reduction. That forced selling is the mechanism behind every “carry unwind crashes markets” headline.

The yen carry trade mechanics that generate this pressure are more entrenched than a single rate hike can neutralise: with the BoJ at 1.0% and the Fed’s target range still at 3.5%-3.75%, a carry spread of roughly 2.5%-2.75% continues to make yen-funded investing structurally attractive to leveraged participants.

Why scale and concentration define the risk ceiling

The question that separates tactical volatility from structural risk is where the trade actually lives. The yen carry trade is concentrated in a specific population of leveraged, speculative investors. It is not woven through global pension funds, retail brokerage accounts, or bank balance sheets at scale. That concentration is why unwinds hurt that population acutely but do not automatically ripple into a broader systemic crisis.

A 2025 MarketWatch roundtable concluded there was “no evidence for a big position overhang in the yen.” Multiple strategist estimates place the trade’s footprint at hundreds of billions, not the tens of trillions that would be required for a genuinely systemic event. The carry trade dynamic, while periodically valid, is considered to have minimal systemic relevance compared to its historical peak in the mid-2000s.

Episodic stress is real. Systemic breakdown from yen carry dynamics has not materialised. That distinction tells you how much weight to put on the next alarming headline.

Why yentervention keeps falling short

Earlier in 2026, Japan confirmed at least one intervention operation exceeding $70 billion. A brief period of yen stability followed, after which the currency turned lower again as underlying market forces reasserted themselves. The same pattern had played out in 2024, when multiple rounds of direct yen purchases as the currency slid toward 160 per dollar produced short-term relief but no medium-term trend reversal.

The structural reason is captured by the impossible trinity, a macroeconomic framework that says a country cannot simultaneously maintain all three of the following:

- Open capital markets: Money flows freely across borders (Japan has this).

- An independent central bank: The BoJ sets monetary policy based on domestic conditions, not currency defence (Japan has this).

- A managed exchange rate: A durably defended level for the yen (Japan is trying to have this, and failing).

Japan has chosen the first two. That makes the third structurally unsustainable without a fundamental policy trade-off. As long as rate differentials between Japan and the US remain wide, with the BoJ policy rate at 1.0% by mid-2026 and still deeply negative in real terms, intervention amounts to adding government yen purchases into a vast ocean of global foreign-exchange activity. It buys time. It does not reset fundamentals.

The unilateral intervention record from the 2026 campaign illustrates the ceiling on this approach in concrete terms: Japan deployed a record 11.7349 trillion yen and USD/JPY still reached 162.40 on 29 June 2026, its weakest level since 1986, as underlying carry selling pressure absorbed every official purchase.

Intervention buys time; it does not reset fundamentals. Unless the underlying policy context has genuinely shifted, the yen’s direction will reassert itself.

The political pressure behind the policy

Japan’s transition from decades of deflation to consistent, moderate inflation has made yen weakness politically costly. A weaker yen raises import costs for energy and food, hurting households directly. Prime Minister Sanae Takaichi‘s cost-of-living relief measures in the upcoming budget reflect the political dimension now being addressed domestically rather than solely through FX operations.

A three-question framework for the next yen scare

The evidence from 2024 and 2026 condenses into three diagnostic questions you can ask in real time when a yen headline moves markets:

| Question | What to look for | What a “no” implies |

|---|---|---|

| Is there evidence of a large, concentrated, one-way carry position? | Positioning data from major banks; roundtable findings like the 2025 MarketWatch panel showing “no evidence for a big position overhang” | Systemic risk is limited regardless of headline severity |

| Is the intervention unilateral or multilaterally coordinated? | Whether multiple central banks are aligned (Plaza Accord-style) vs. Japan acting alone (2024, 2026 pattern) | Unilateral action buys days or weeks; it does not set a durable floor |

| Have the underlying fundamentals actually changed? | BoJ rate trajectory, US-Japan rate differential, Japan’s fiscal stance, inflation path | Any market reaction is likely episodic, not structural |

The framework’s value is not prediction. It routes your attention toward the variables that actually drive medium-term yen direction, away from the narrative heat that drives short-term price moves.

Tracking carry trade warning signals in real time requires watching the JGB yield trajectory alongside USD/JPY technicals, not just BoJ policy headlines; Bank of America’s CTA trigger mapping estimates that a roughly 3% S&P 500 decline could release approximately $100 billion in programmatic selling, amplifying any unwind far beyond the carry trade’s direct participants.

Yen dynamics are real. The catastrophic version is not. Calibrate, do not dismiss.

If you can ask these three questions when a yen scare hits, you are far less likely to make a reactive portfolio decision based on a headline that sounds alarming but lacks structural support.

The next major ASX story will hit our subscribers first

What the pattern means for portfolios navigating recurring yen volatility

The analysis above translates into four practical postures for your portfolio:

- Treat carry-trade panic as a volatility story, not an existential portfolio threat. The 2024 episode, characterised at peak fear as the largest carry trade ever seen, resolved without a structural breakdown. The disruption was real but historically self-limiting.

- View yentervention announcements as sentiment and timing factors, not macro regime changes. The 2026 intervention pattern (brief stability, trend resumes) confirms the structural dynamic has not changed.

- Focus on fundamentals over narrative. The BoJ’s rate trajectory, the US-Japan rate differential, and Japan’s fiscal stance drive medium-term outcomes. Headlines do not.

- Use yen-driven sell-offs to review diversification and risk tolerance, not to make thematic bets on the carry trade itself. Institutional commentary consistently frames any renewed unwind as likely modest relative to the dramatic stories circulating on social media.

For US investors specifically, yen volatility is more likely to be a distraction from your core asset allocation than a signal to restructure it. The exception: if the three-question framework flags a genuine fundamental shift (coordinated intervention, a material BoJ policy pivot, evidence of a large concentrated position), that changes the calculus. Until then, patience and framework-based assessment are the appropriate responses.

Japanese CFOs have flagged increasing difficulty hedging currency risk, which is a real corporate earnings consideration. But corporate hedging challenges in Tokyo do not automatically translate to systemic portfolio risk in New York.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Reading the next yen headline with clearer eyes

Both the catastrophic carry narrative and the heroic intervention narrative repeatedly overstate the durability of their predicted outcomes. The empirical record across 2024 and 2026 supports this consistently. Neither story has delivered on its medium-term promise, even as both continue to move prices in the short term.

The three-question framework is the durable takeaway: not a prediction tool, but an attention-routing device that moves you toward fundamentals and away from narrative heat. As long as the BoJ normalises gradually, rate differentials with the US remain wide, and Japan’s fiscal stance stays expansionary, the conditions that make both narratives structurally unreliable will persist.

The same framework applies to the next episode, whenever it arrives. The headlines will feel urgent. The structure underneath them will not have changed.

Forward-looking statements in this article are speculative and subject to change based on market developments, policy decisions, and macroeconomic conditions.