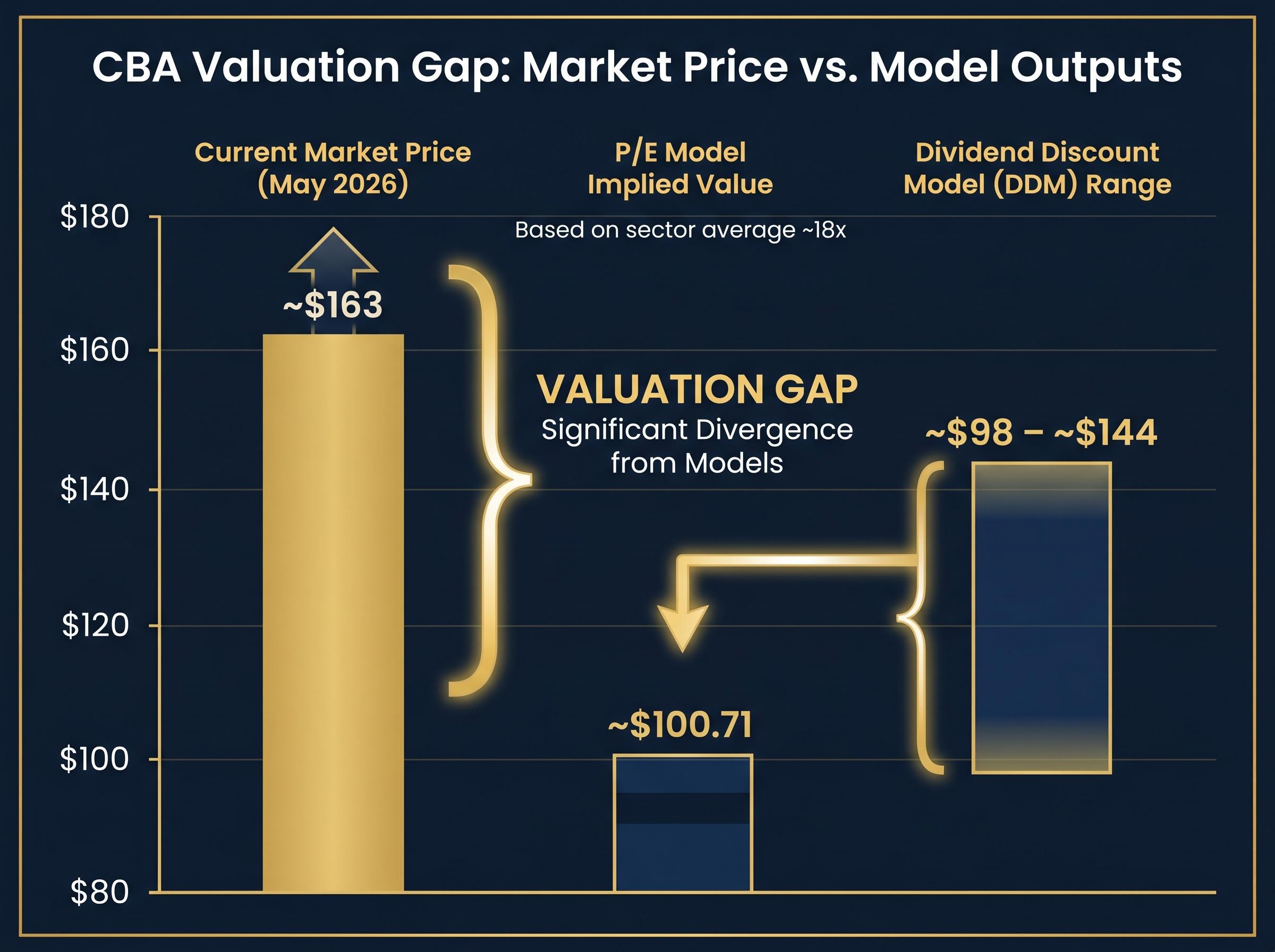

Commonwealth Bank of Australia shares were trading at approximately $163 in May 2026, yet every major broker covering the stock maintained either a sell or underweight rating. Morgan Stanley reiterated its underweight call. Goldman Sachs held a sell. The quantitative case was clear: the numbers said the stock was expensive. Yet CBA remained the most widely held bank on the ASX, and capital continued flowing in.

The disconnect between model output and market behaviour is not irrational noise. It reflects a set of qualitative and structural factors that standard bank stock valuation tools simply do not have inputs for. This article explains what those factors are, why they carry real economic weight, and how Australian investors can weigh them against quantitative signals when assessing ASX bank stocks. CBA serves as the primary case study, with reference to ANZ and Macquarie Group where the contrast sharpens the analysis.

Why the numbers alone give you an incomplete picture of CBA

Two widely used valuation approaches produce estimates well below CBA’s current share price. The gap is persistent, and the models cannot resolve it internally.

- Price-to-earnings method: CBA’s FY24 earnings per share of $5.63 and a P/E of 28.9x at approximately $163 sit far above the sector average of roughly 18x. Applying the sector-adjusted multiple implies a value of approximately $100.71.

- Dividend discount model: Depending on growth and discount rate assumptions, DDM outputs cluster between approximately $98 and $144, still below the market price across most reasonable input ranges.

Both methods rely on historical earnings, dividend flows, and sector averages. They measure what has already happened and what similar companies have delivered. They are not designed to capture structural franchise advantages, management quality differentials, or the defensive earnings characteristics of an oligopolistic banking market.

The five macro and qualitative factors that determine whether an Australian bank valuation holds up under real-world conditions, covering income structure, property exposure, unemployment trajectory, management discipline, and arrears trends, give investors a replicable sequence for stress-testing any model output against the current environment.

Goldman Sachs described CBA as “best-in-class on returns and capital generation” in February 2025, yet maintained a sell rating. Morgan Stanley reiterated its underweight call in May 2025, acknowledging CBA’s franchise strength while warning the risk-reward “looks poor at current multiples.”

That tension, between acknowledged quality and a sell recommendation, is the article’s starting point. The models are not wrong. They are measuring a different thing than what the market is pricing. The investor’s task is to understand both.

When big ASX news breaks, our subscribers know first

The oligopoly premium: how Australia’s banking structure props up valuations

Australia’s banking market is concentrated among four major institutions: CBA, ANZ, NAB, and Westpac. This oligopolistic structure is not merely an observation about market share; it is a valuation input with measurable earnings consequences.

International banks have struggled to crack Australian retail banking in any meaningful way. HSBC, despite its global scale and decades of local presence, has not materially penetrated the domestic retail deposit or mortgage market. The barriers are structural: stringent regulatory capital requirements, deeply entrenched consumer brand loyalty, and distribution networks that took decades to build.

The oligopoly also self-reinforces through consolidation. ANZ’s acquisition of Suncorp Bank, approved with conditions, was designed to narrow CBA’s retail scale advantage in Queensland. Rather than a new competitor entering the market, an existing major absorbed a regional player, further concentrating the system.

Morgan Stanley’s April 2025 sector note acknowledged that CBA “still dominates in mainstream retail banking” even as Macquarie expands in deposits and mortgages. The competitive moat is real.

What the oligopoly means for margin resilience

High barriers to entry allow the majors to sustain net interest margins that would be competed away in a more fragmented market. The specific barriers are durable:

- Regulatory capital requirements that impose substantial entry costs on any new retail banking entrant

- Brand entrenchment across deposit and mortgage products, reinforced by decades of customer relationships

- Distribution scale in branch networks, digital platforms, and broker channels that cannot be replicated quickly

This margin resilience is a genuine economic input, but the P/E model captures it only indirectly through historical earnings. It does not project it forward. The oligopoly premium partially explains why the entire sector trades above global banking averages, though it does not, by itself, explain why CBA trades at a premium to its own peers.

Management quality and post-Royal Commission risk culture as valuation inputs

Markets price management quality through its effect on risk premiums. A bank with credible, stable leadership and a demonstrated track record of risk culture improvement commands a lower required return from equity investors. Mechanically, a lower required return supports a higher P/E multiple.

At CBA, the specific evidence base centres on CEO Matt Comyn’s post-Royal Commission leadership. An AFR profile in August 2024 credited Comyn with restoring CBA’s reputation through a sustained focus on risk culture, remediation, and technology investment. APRA acknowledged in October 2024 that the majors, including CBA, had strengthened their boards and risk frameworks since earlier enforcement actions.

CBA’s APRA Enforceable Undertaking, which the bank formally satisfied in September 2022, required measurable improvements to governance, culture, and risk management frameworks following the 2018 Prudential Inquiry, providing the concrete regulatory baseline against which Comyn’s post-Royal Commission risk culture improvements are assessed.

Analyst commentary makes the connection to valuation explicit. Airlie Funds Management stated in March 2025 that CBA had the “best management execution track record among majors,” citing this as a qualitative premium justifier. UBS noted in August 2024 that CBA’s “conservative risk culture relative to peers” was a factor supporting its elevated multiple.

Airlie described CBA as “the bank you’d most want to own long term,” but added that “at current prices we struggle to justify adding to it.” The quality is not in dispute. The price paid for it is.

For investors seeking to assess management quality from publicly available information, four observable proxies provide a reasonable starting point:

- Regulatory outcomes: enforcement actions, remediation timelines, APRA commentary on risk governance

- Capital discipline: consistency of dividend policy, CET1 capital ratios, approach to buybacks

- Remediation progress: pace and completeness of addressing legacy conduct issues

- Analyst commentary on execution: specific references to management track record in broker research notes

These are not perfect proxies, but they convert an abstract qualitative concept into something an investor can monitor over time.

Management culture and governance quality are not soft signals: remediation bills, regulatory fines, and capital overlays from cultural failures have historically dwarfed years of accumulated earnings at Australian banks, making the qualitative track record assessment a material input rather than an optional supplement to quantitative modelling.

Revenue mix and the shift beyond mortgage interest income

Revenue mix matters for bank valuation because a bank with diversified, fee-based non-interest income is generally valued more highly than a pure mortgage lender. Fee income is less sensitive to interest rate cycles and credit conditions, which reduces earnings volatility and, in theory, justifies a growth premium.

CBA’s strategic pivot targets exactly this advantage. Following its exit from most legacy wealth management businesses, the bank has redirected investment toward digital ecosystem services, payments, merchant acquiring, and small business platforms. CEO Comyn articulated the strategy in November 2024, describing a “broader digital ecosystem” around the CommBank app, including partnerships in retail, energy, and small business services.

CBA’s FY24 results in August 2024 showed fee and commission income from payments and digital services becoming a more visible revenue driver. Management described these as “higher-growth, capital-light revenue streams” compared with traditional mortgages.

| Revenue Type | Description | Valuation Sensitivity | CBA Status (2025-2026) |

|---|---|---|---|

| Net Interest Income | Mortgage-heavy, rate-cycle dependent | High sensitivity to RBA cash rate and credit growth | Still dominant share of group revenue |

| Fee and Commission Income | Payments, merchant acquiring | Lower rate sensitivity, higher competition risk | Growing, increasingly visible in results |

| Digital/Platform Income | Ecosystem partnerships, data-driven offers | Capital-light but unproven at scale | Early stage, strategic priority |

| Wealth Management | Traditional financial advice, insurance | N/A | Exited (Colonial and related businesses sold) |

The limits of the platform economics argument

The sceptical counterpoint is worth taking seriously. Macquarie Equities noted in January 2025 that CBA’s payments and digital services strategy could “gradually lift” non-interest income as a share of group revenue, but did not view it as a “near-term game-changer.” An AFR columnist described the digital push in December 2024 as “an attempt to justify its valuation premium,” arguing that non-interest income growth has been “respectable but not yet transformational” in group earnings terms.

Fintechs and global payment networks are also competing in these spaces, reducing the assumption that CBA can build an uncontested moat in digital services. Revenue mix is a forward-looking valuation input that the P/E model, which uses historical earnings, cannot capture. Whether CBA’s digital strategy eventually moves the earnings needle remains an open question, and investors should treat platform economics claims cautiously until the numbers provide confirmation.

Property market conditions, household debt, and the macro exposure every model assumes away

CBA’s mortgage book concentration means its earnings are materially exposed to Australian residential property prices and household debt levels. Most valuation models implicitly assume the current credit environment persists. That assumption deserves scrutiny.

The macro conditions as of mid-2026 are specific. Australian unemployment stood at 4.3% in March 2026, based on ABS data. The RBA cash rate remained at 4.35% following the Board’s early May decision. The household debt-to-income ratio sat at approximately 180-190% of disposable income, according to the RBA’s April 2025 Financial Stability Review, a level described as “very high by international standards.”

| Macro Variable | Current Condition (mid-2026) | Implication for CBA Earnings |

|---|---|---|

| Cash Rate | 4.35% | Margin support, but loan growth subdued |

| Unemployment | 4.3% | Arrears benign, but labour market softening |

| Household Debt Ratio | ~180-190% DTI | Amplifies sensitivity to any employment shock |

The RBA’s April 2025 Financial Stability Review concluded that the major banks remained well capitalised and loan arrears were low, but warned they are “exposed” to a severe housing downturn given their large housing loan books.

The RBA Financial Stability Review from April 2025 documented that the major banks remained well capitalised and arrears were contained, but specifically flagged their concentrated exposure to housing loans as a vulnerability under a severe downturn scenario, a warning that sits directly behind the macro risk arguments advanced by analysts concerned about CBA’s premium multiple.

The two risk scenarios outlined by AFR equity strategists in March 2026 capture the bind. If the RBA keeps rates higher for longer, loan growth remains subdued and household stress slowly rises, capping bank earnings growth. If rate-cut expectations are brought forward because the economy weakens, banks could face both margin compression and rising bad debts simultaneously.

Milford Asset Management warned in April 2025 that “if unemployment ticks up or house prices soften, CBA’s premium multiple could compress.” Strategists argued CBA is “most exposed from a valuation standpoint” because its premium multiple would be hardest to sustain in a downturn. These are not abstract risks. They are the specific conditions under which the gap between model output and market price could close rapidly.

The next major ASX story will hit our subscribers first

Putting qualitative factors to work: a checklist before you trust the model

The four qualitative dimensions covered in this article, oligopoly structure, management quality, revenue mix, and macro exposure, can be synthesised into a practical assessment sequence. This checklist sits alongside quantitative model output, not as a replacement but as a necessary companion.

Applied to CBA as of mid-2026, the checklist produces a mixed but specific picture. The structural premium from Australia’s oligopolistic banking market is real and durable. The management quality premium under Comyn is well documented by analysts but, per most broker commentary, already priced in. Revenue mix diversification is a work in progress with credible strategic logic but limited earnings impact so far. Macro exposure, specifically to housing and household debt, is the largest unpriced risk at current multiples.

The checklist itself:

- Assess structural moat and oligopoly durability

- Review competitive entry attempts and outcomes

- Monitor consolidation activity (e.g., ANZ-Suncorp)

- Check deposit and mortgage market share trends

- Evaluate management track record and risk culture signals

- Review APRA commentary and regulatory outcomes

- Track capital discipline and dividend consistency

- Read analyst notes specifically referencing execution quality

- Examine revenue mix direction and credibility of non-interest income growth

- Compare non-interest income as a percentage of total revenue over time

- Assess competitive threats from fintechs and global platforms

- Evaluate whether management’s digital strategy claims are supported by results

- Form a view on macro exposure

- Monitor unemployment trends, RBA rate path, and household debt metrics

- Assess mortgage book concentration relative to peers

- Consider how a property price correction or employment shock would affect the earnings base

The contrast with peers sharpens the framework. ANZ offers a lower starting valuation with execution upside from the Suncorp integration, but carries meaningful integration risk. Macquarie’s diversified earnings model, driven more by asset management, infrastructure, and markets than by domestic retail banking, makes it “a more global, higher-beta play,” per ABC News reporting in February 2025. Plato Investment Management noted in September 2024 that on total return metrics, ANZ and NAB appeared more attractive than CBA at then-current valuations. Investors comparing ASX bank stocks need qualitative checklists tailored to each company’s specific profile, not a single universal model.

ASX 200 concentration risk compounds this dynamic for investors who hold CBA within a broader index portfolio: with financials and materials together accounting for more than 50% of the index by market-cap weight, an additional individual bank position can silently push total bank allocation well above 40-50% of a domestic equity portfolio without any deliberate decision to overweight the sector.

The valuation gap will not close until the macro does

CBA’s qualitative advantages are genuine, well documented, and correctly identified by the analysts who simultaneously rate the stock a sell. Morgan Stanley, Goldman Sachs, UBS, and J.P. Morgan all acknowledge the franchise quality, the management track record, and the structural moat. The consensus view is that these advantages are already more than priced in at current multiples.

The asymmetry at a premium valuation is the point most holders underappreciate. Disappointing earnings or a macro surprise, whether rising unemployment or a property price correction, would compress CBA’s multiple faster and harder than it would compress a stock already trading near fair value. As a fund manager told The Australian in February 2026, “CBA in particular is vulnerable to any disappointment on earnings or the macro front because of its premium.”

The RBA’s May 2026 Statement on Monetary Policy indicated rate cuts are not expected until 2027 at the earliest, keeping the macro environment tight and reducing the scope for a near-term re-rating of bank multiples.

Airlie Funds Management described CBA’s valuation as one that “leaves no room for error on credit quality or margin trends.”

Models are not wrong about CBA. They are measuring what can be quantified: historical earnings, dividend flows, sector comparisons. The market is pricing something else: franchise durability, management confidence, and an implicit bet that the macro environment holds. The investor’s task is to understand both inputs and decide whether the gap between the two represents a justified premium or a risk they are not being compensated to carry.

For investors who want to apply a structured quantitative and qualitative framework to any ASX bank position, our dedicated guide to valuing bank stocks beyond the PE ratio covers a six-check sequence spanning ROE versus cost of equity, price-to-book against forward ROE, NIM sensitivity, arrears trends, CET1 ratios, and deposit share, with all data sourced from publicly available ASX results and APRA quarterly statistics.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.