How the US Government Became Intel’s Investor and Deal Broker

52 mins ago

Intel shares have risen more than fourfold since March 2025. That is not a statistic that invites the word “cheap.” A stock that has quadrupled is not a turnaround opportunity; it is a turnaround that has already happened, at least in price terms. The question facing anyone assessing INTC today is fundamentally different from the one investors answered at the lows.

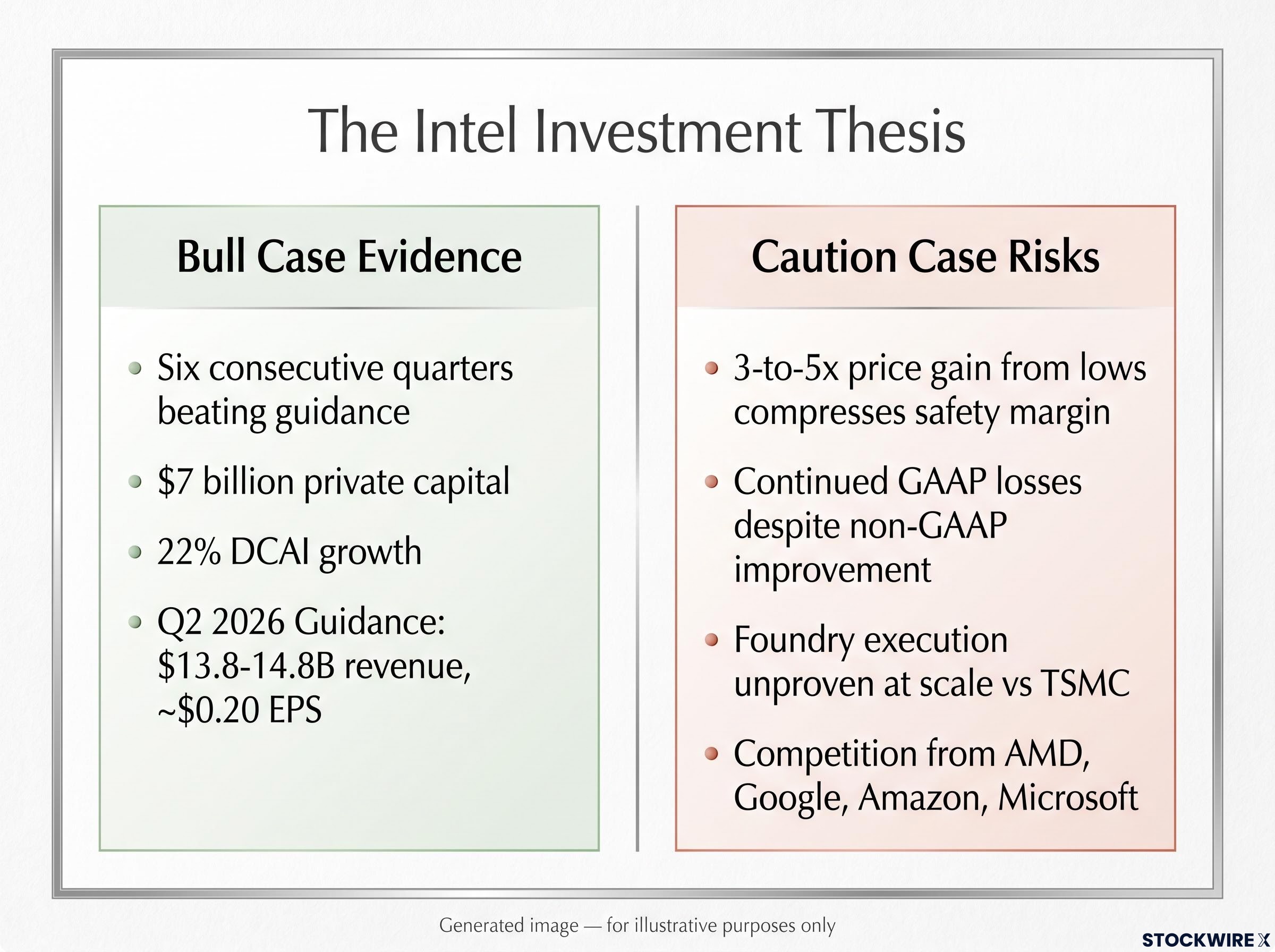

The shift is grounded in specifics: Lip-Bu Tan’s appointment as CEO, six consecutive quarters of beating Intel’s own revenue guidance, a combined $7 billion in private capital from Nvidia and SoftBank, and a 22% year-over-year surge in Data Centre and AI revenue from Q1 2026. These are not speculative catalysts. They are reported results. The question is whether they justify the price that now sits on top of them.

Here is a structured way to assess that question, covering the operational evidence, the capital signals, the financial results, and the risks that remain unresolved at current levels.

When Lip-Bu Tan took the CEO role in March 2025, Intel was strategically adrift. The company was losing ground in data-centre CPUs to AMD, lagging in process technology, and carrying a management structure that Tan himself publicly described as “slow-moving and bloated.”

The restructuring that followed was specific and sequential:

Tan framed 2025 as a “defining year” for Intel. By the time Q1 2026 results landed, the company had beaten its own revenue projections for six consecutive quarters.

That pattern tells you something specific. A company that consistently beats its own guidance is not just performing well; it is setting credible internal targets and hitting them. That is a different, and more investable, profile than a company that routinely over-promises and under-delivers. For anyone evaluating the durability of this rally, the consistency of execution under Tan is the input that deserves the most weight.

The broader category of AI infrastructure stocks, spanning optical interconnects, semiconductor compute, and power infrastructure, rewarded companies across the full data-centre stack in 2025, not only GPU designers, a dynamic that contextualises Intel’s 84% stock gain that year as part of a structural infrastructure re-rating rather than purely company-specific momentum.

Nvidia and SoftBank committed a combined $7 billion to Intel. The headline figure matters, but the composition matters more.

Nvidia agreed to purchase approximately $5 billion of Intel common stock at roughly $23.28 per share, equating to around a 4% stake. Regulators approved the deal, which was completed by end-2025. The two companies plan to collaborate on custom data-centre and PC products, explicitly linking the investment to Intel’s manufacturing role.

SoftBank invested $2 billion at approximately $23 per share, framing the move as part of its long-term vision to enable the AI revolution and accelerate access to advanced infrastructure.

| Investor | Amount | Price per share | Approximate stake | Stated rationale |

|---|---|---|---|---|

| Nvidia | $5 billion | ~$23.28 | ~4% | Custom data-centre and PC product collaboration; manufacturing partnership |

| SoftBank | $2 billion | ~$23 | Not disclosed | AI revolution enablement; advanced infrastructure access |

Nvidia-Intel collaboration scope: The planned partnership covers custom data-centre and PC products, explicitly positioning Intel as a manufacturing partner for Nvidia, not merely a legacy competitor. This is the detail that distinguishes the investment from a passive financial stake.

When a direct competitor commits $5 billion and formalises a manufacturing partnership, it tells you that Intel’s foundry capability is being taken seriously by someone with the technical knowledge to evaluate it accurately. That is a materially different signal than an institutional fund adding a position. It does not eliminate foundry execution risk, but it changes the probability weighting.

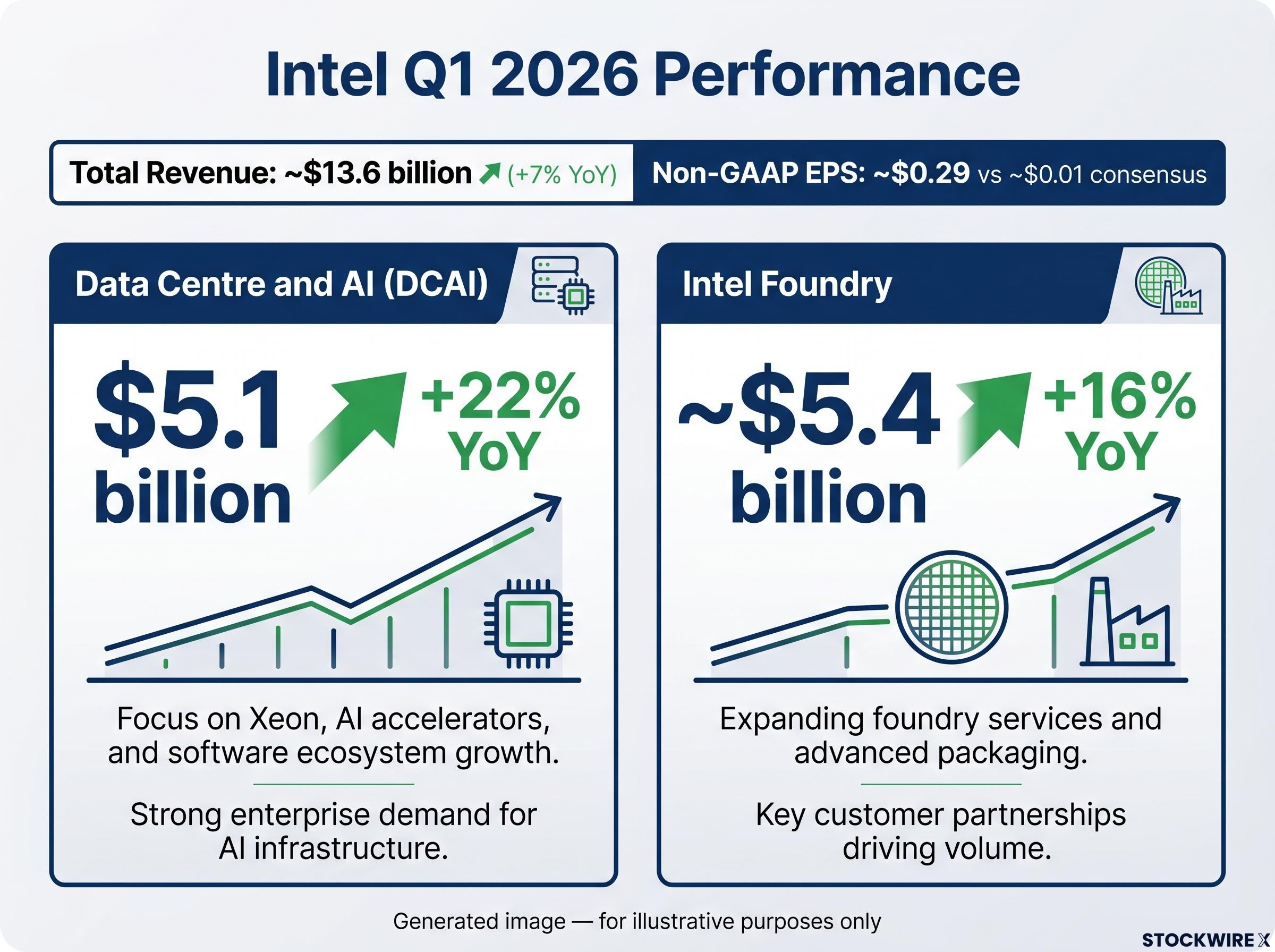

Intel reported Q1 2026 total revenue of approximately $13.6 billion, up roughly 7% year-over-year and ahead of Wall Street expectations. Non-GAAP earnings per share came in at approximately $0.29, against expectations of roughly $0.01. The post-earnings share price surged 15-24%.

Six consecutive quarters. As of Q1 2026, Intel had beaten its own revenue projections for six straight quarters, the clearest available measure that management is now setting achievable targets and exceeding them consistently.

The headline beat is striking, but the segment-level detail is where the investment story actually lives.

| Segment | Q1 2026 revenue | Year-over-year change | Versus consensus |

|---|---|---|---|

| Data Centre and AI (DCAI) | $5.1 billion | +22% | Beat (consensus ~$4.4 billion) |

| Intel Foundry (incl. intersegment) | ~$5.4 billion | ~+16% | Beat |

| Total revenue | ~$13.6 billion | +7% | Beat |

The Data Centre and AI segment posted $5.1 billion in quarterly revenue, a 22% year-over-year rise, with Xeon processor demand as the primary driver. According to the Wall Street Journal, Google Cloud committed to a substantial Xeon CPU purchase, pointing to stronger product performance under Tan’s leadership as its rationale. Foundry revenue growth of approximately 16% signals early momentum in Intel’s push to manufacture chips for external customers.

Then there is the counterweight. Despite the non-GAAP improvement, Intel continued to record a GAAP net loss, with results burdened by restructuring charges and depreciation from large capex cycles.

That gap between a $0.29 non-GAAP EPS beat and a GAAP net loss is the single most important tension in the investment case right now. It tells you the operational engine is improving, but the financial structure is still absorbing the cost of transformation. How much patience you have for that gap to close is a personal risk-tolerance question, not an analytical one.

Intel guided Q2 2026 revenue to $13.8-14.8 billion with adjusted EPS of approximately $0.20.

The bull case detailed above is genuine. None of what follows undercuts it. What it does is identify the risks that remain unresolved at a price that has already risen three to five times from early-2025 lows.

Semiconductor valuation multiples across the sector in 2026 reveal a striking internal contradiction: Micron trades below 9x forward earnings while Intel sits near 101x, nearly three times its own dot-com-era peak, meaning the headline rally masks fundamentally different risk profiles depending on which name an investor holds.

These two risks are analytically distinct and conflating them leads to confused conclusions.

Foundry execution is an internal question: can Intel manufacture at TSMC-comparable quality and scale? Nvidia’s stake improves the optics but does not guarantee yield, cost, or reliability outcomes. The difference between a promising foundry roadmap and a proven high-volume manufacturing business is measured in years of execution and sustained customer wins.

Competitive intensity is an external question: even if Intel can manufacture effectively, will customers choose its products? Google TPUs, Amazon Graviton and Trainium, and Microsoft Maia represent custom silicon alternatives that can displace standardised x86 workloads at scale. Intel’s 22% DCAI growth is occurring in the context of intense competition from both traditional rivals and vertically integrated customers.

Political and regulatory scrutiny adds a further layer. Tan has faced criticism from former President Trump and scrutiny over alleged ties to Chinese entities, underscoring that Intel’s role as a national semiconductor champion makes it a lightning rod for geopolitical tension.

At a fourfold gain from the lows, each of these unresolved risks carries more downside consequence for someone entering at today’s price than it did for someone who bought at the starting point.

If you are evaluating Intel as an investment, the Data Centre and AI segment is the number to watch. Here is why, broken into the logic that matters for interpreting future earnings releases:

AI infrastructure spending across the four largest hyperscalers reached $130 billion in Q1 2026 alone, with full-year 2026 projections at $725 billion, creating the demand environment that makes Intel’s 22% DCAI revenue growth plausible rather than anomalous.

The bull case has real evidence behind it:

The caution case has real evidence behind it too:

Forward anchor: Q2 2026 guidance sits at $13.8-14.8 billion in revenue with adjusted EPS of approximately $0.20. This is the next data point that will tell you whether the operational trajectory is holding.

The honest framing for an investor considering Intel today is that the easy money has been made. What remains is a bet on whether management can convert demonstrated operational progress into durable earnings growth over a three-to-five year horizon. That is a qualitatively different risk than buying a cheap, unloved stock.

The specific evidence points that would shift the balance either way: a sustained move toward GAAP profitability, large repeat foundry customer announcements, and continued DCAI outperformance in Q2 2026 and beyond. Those are the inputs worth watching before committing new capital.

For investors wanting to understand what the Apple deal actually confirms about Intel Foundry’s commercial readiness, our full explainer on the Apple-Intel foundry agreement covers the specific process node, volume timeline, and TSMC capacity comparison that define the execution bar Intel must clear for the relationship to expand beyond entry-level chips.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Intel's Data Centre and AI (DCAI) segment covers server CPUs like the Xeon franchise, AI accelerators, and related components sold to cloud providers and hyperscalers. It posted $5.1 billion in Q1 2026 revenue, up 22% year-over-year, making it the clearest indicator of whether Intel is winning in the high-margin, structurally growing part of the market rather than defending legacy share.

Nvidia agreed to purchase approximately $5 billion of Intel common stock at around $23.28 per share, acquiring roughly a 4% stake, as part of a planned collaboration on custom data-centre and PC products that explicitly positions Intel as a manufacturing partner. The investment signals that Intel's foundry capability is being taken seriously by a company with the technical expertise to evaluate it accurately.

In Q1 2026, Intel reported non-GAAP EPS of approximately $0.29 against expectations of roughly $0.01, but continued to record a GAAP net loss due to restructuring charges and depreciation from large capital expenditure cycles. That gap shows the operational engine is improving while the financial structure is still absorbing the cost of transformation.

After a fourfold gain from March 2025 lows, the key unresolved risks include foundry execution at scale (Intel has not yet proven it can match TSMC on yield, cost, and reliability at high volume), continued GAAP losses despite non-GAAP improvement, aggressive competition from AMD and hyperscaler custom silicon, and a valuation near 101x forward earnings that compresses the margin of safety for new entrants.

Investors should track DCAI revenue growth before the headline EPS figure, because it signals whether Intel's strategic bet on AI infrastructure is landing with real customers. Intel guided Q2 2026 revenue to $13.8-14.8 billion with adjusted EPS of approximately $0.20, making that the next concrete data point for assessing whether the operational trajectory is holding.