Why AI Is Splitting Semiconductor Stocks From the Rest of Tech

2 hrs ago

A UK Prime Minister resigns, and equities go up. That is not a misprint, and it is not a coincidence.

Four days ago, Keir Starmer announced his resignation as Prime Minister, triggering a Labour leadership contest that has already elevated Andy Burnham as the dominant front-runner. The kneejerk political read is turbulence. The market read, on 22 June 2026, was rather different: the FTSE 100 closed up approximately 0.72%, gilt yields moved only marginally and in line with European peers, and sterling stabilised without any disorderly depreciation. That divergence between political alarm and market calm is the story worth understanding.

This piece unpacks the mechanism behind that reaction, separates the concrete Burnham policy risks from the speculative ones, and gives you a practical framework for tracking whether the constructive signal holds or starts to break down. Here is what the data actually tells you about how UK politics and the stock market interact during leadership transitions, and why the distinction matters for positioning.

Start with what the instruments did, because the numbers tell a more precise story than the headlines.

The FTSE 100 closed up approximately 0.72% on 22 June 2026, with financials leading the advance. Ten-year gilt yields rose by roughly 1 basis point to around 4.85%. Sterling dipped initially but stabilised without any sharp or sustained divergence from peer currencies.

| Metric | Value / Movement | European Context | Interpretation |

|---|---|---|---|

| FTSE 100 | +0.72% | In line with positive European equity sessions | No UK-specific sell-off; financials led |

| 10-year gilt yield | +~1bp to ~4.85% | European bond yields also rose on the day | Routine rates move, not idiosyncratic UK stress |

| Sterling | Initially lower, then stabilised | No sharp divergence from peer currencies | Orderly adjustment, not a credibility event |

The gilt yield observation is the critical one. European bond yields moved higher on the same day, which means the UK move was not isolated. This was not a credibility event; it was a routine session in which the political headline was subordinate to the broader rates environment.

UK gilt yield mechanics during political events are less alarming than they appear: the government’s 13.9-year average debt maturity buffer means that a 25-40 basis point spike on a leadership headline moves the annual interest bill only marginally, which is part of why the bond market’s reaction to the Starmer resignation stayed within the bounds of a routine session.

UK gilt yields had already fallen considerably in the weeks before the resignation, confirming markets were processing the transition well before the formal announcement.

That prior decline tells you the formal event was a confirmation rather than a shock. Investors who anchored on the political alarm would have misread the direction of travel on the day.

The reaction on 22 June was counterintuitive only if you think of political change as inherently destabilising. In practitioner finance, the principle runs differently: markets struggle more with open-ended uncertainty than with quantifiable risk, even when that risk is negative.

There is a useful distinction here. Uncertainty is what you cannot model: who will be PM in three months, and what will they do? Risk is what you can model: a range of plausible tax rates, spending commitments, or regulatory shifts from a known leader. Once the leadership path becomes clearer, even if the new leader is perceived as more interventionist, investors can shift from discounting unknowns to discounting scenarios. That shift typically supports risk assets.

The divergence between alarming headlines and orderly market behaviour is not unique to UK political transitions; the recurring pattern of geopolitical risk and market calm has been documented across multiple recent episodes, with markets consistently processing headline shocks as probability-adjusted inputs to future earnings rather than as proportional threats to equity valuations.

Fisher Investments frames this directly: what drives prices is the divergence between what investors expected and what actually materialises, with markets reacting to the substance of policies rather than to the individuals who champion them. The resignation confirmed what markets had been pricing. It did not introduce new information.

This is where the expectations bar matters. Widespread analyst warnings about a potential leftward lurch under Burnham set a deliberately cautious tone across UK-focused commentary. That commentary, in aggregate, lowered the hurdle for outcomes to disappoint.

The result is that a merely incremental policy outcome, measured against that bar, would likely be processed as a positive surprise by UK risk assets. For you as an investor, this mechanism means the loudest political commentary often represents the worst time to act on it. By the time headlines are pricing maximum risk, the market may already be looking through to the resolution.

So what do we actually know about what Burnham would do? Less than the commentary implies.

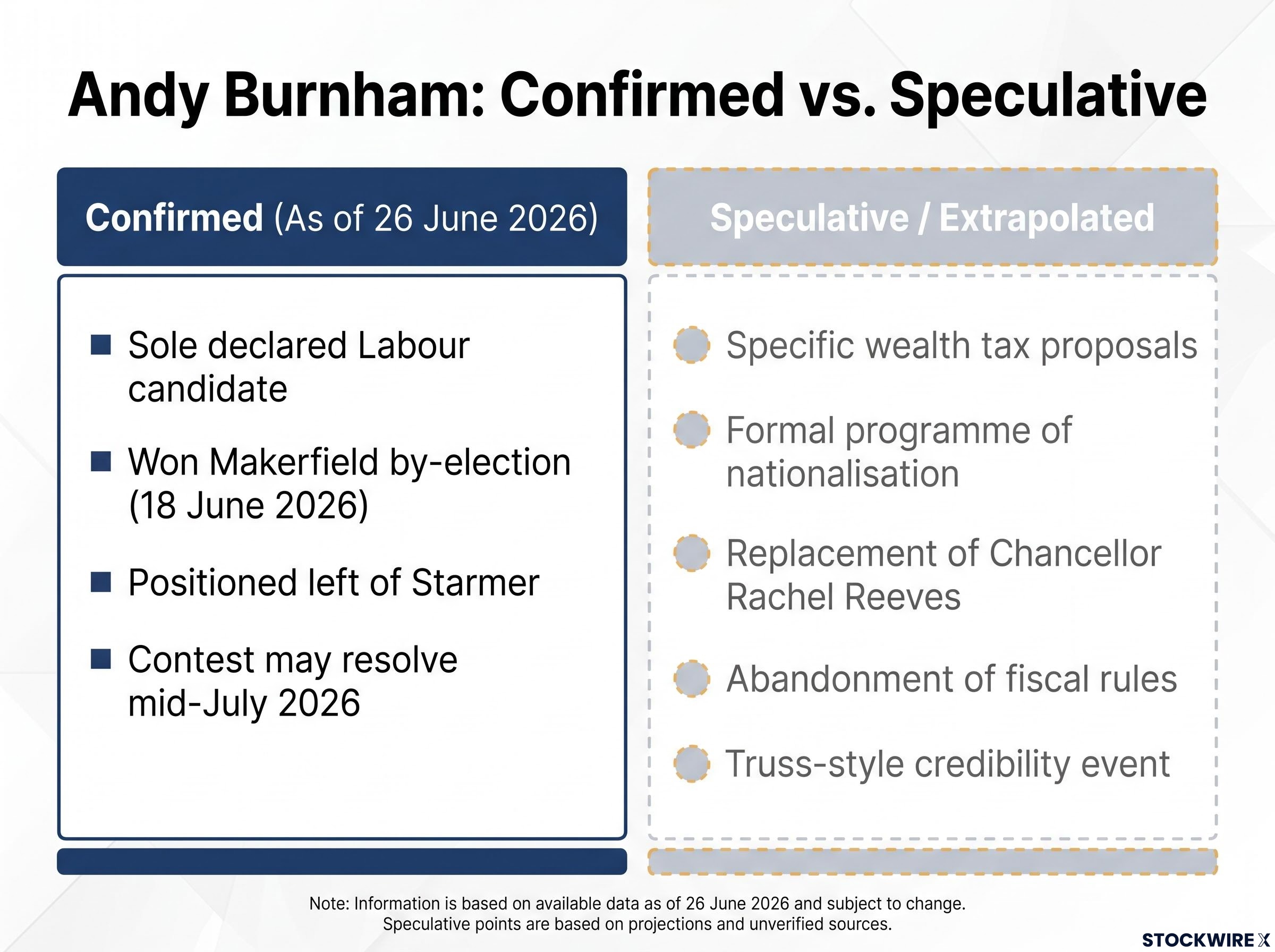

As of 26 June 2026, Andy Burnham is the only declared candidate for the Labour leadership. He won the Makerfield by-election on 18 June 2026, has received widespread endorsements, and the contest could resolve as early as mid-July 2026. He is broadly positioned to the left of Starmer. Those are the confirmed facts.

Now compare them with what is being extrapolated.

| Confirmed | Speculative / Extrapolated |

|---|---|

| Sole declared candidate with widespread endorsements | Specific wealth tax proposals (derived from past informal remarks, not campaign commitments) |

| Makerfield campaign largely devoid of detailed policy announcements | A formal programme of nationalisation or aggressive fiscal expansion |

| Background as Greater Manchester metro mayor and former cabinet minister | Replacement of Chancellor Rachel Reeves with a more fiscally expansive successor |

| Ideologically positioned to the left of Starmer | Abandonment of existing fiscal rules or framework |

| Leadership contest may resolve by mid-July 2026 | A Truss-style bond market credibility event under Burnham |

The market-relevant question is not whether Burnham is ideologically left of Starmer. He is. The question is whether he has announced policies that would materially reprice UK fiscal credibility. As of now, he has not.

Conflating ideological positioning with concrete policy risk is a common analytical error that can lead to premature de-risking. Knowing where the genuine uncertainty ends and the extrapolation begins is a direct input into how you size positions.

Even if Burnham personally preferred a more radical fiscal stance, the system he would operate within limits how far he could move. That structural reality is part of why the market’s calm reaction on 22 June makes sense.

Three institutional constraints define the ceiling on policy radicalism:

The Bank of England gilt market crisis analysis of the 2022 episode documents how liability-driven investment fund forced sales amplified the initial yield spike into systemic stress, a transmission mechanism that required emergency intervention and set the template for how quickly bond market credibility can deteriorate when fiscal policy surprises investors.

In 2022, the Truss mini-budget produced a genuine credibility event: disorderly gilt yield spikes, a sharp sterling sell-off, and direct IMF commentary. On 22 June 2026, nothing remotely comparable occurred. Gilt yields moved 1 basis point in line with European peers. That comparison tells you the market is not treating this transition as a fiscal credibility risk.

Fisher Investments views the most probable outcome as broadly unchanged economic policy, which given the volume of warnings about a hard-left pivot, would land as a better-than-feared result for markets. Understanding these guardrails tells you that the range of realistic policy outcomes under Burnham is narrower than the commentary suggests, and the probability-weighted market impact is narrower too.

The constructive reading of the 22 June price action is supported by the evidence so far. But it is conditional, not permanent. Here is what to watch over the next six weeks as the leadership contest approaches resolution.

These watchpoints give you a way to distinguish between noise that can be held through and genuine regime-shift signals that warrant repositioning, rather than reacting to every political headline as if it carries equal weight.

Tracking policy-driven market risk across the six-week leadership contest window requires the same attribution discipline applied to other political events in 2026: distinguishing whether a given move in gilts or sterling is domestically generated or part of a broader European rates and currency shift that would have occurred regardless of UK headlines.

The Starmer resignation currently looks like a clearing event rather than a market shock. That reading is not a prediction; it is supported by specific price action. The FTSE 100 rose 0.72%, gilts were stable relative to peers, and sterling was orderly. Those are facts, not projections.

The constructive view depends on conditions being maintained: fiscal rules staying intact, gilt and sterling stability continuing relative to European peers, and policy announcements remaining within the range of incremental rather than radical. If Burnham abandons existing fiscal anchors, or if a more radical figure unexpectedly enters the contest, the thesis requires revisiting.

UK equity structural underperformance relative to global indices predates the current leadership transition by a decade, with domestic institutional ownership collapsing from roughly 80% to 42% since the early 1990s and the sector mix tilting progressively toward old-economy stocks; any re-rating argument must account for those baseline headwinds, not only the near-term political resolution.

The transferable lesson is broader than this single episode. Political alarm and market opportunity often coincide because headlines create uncertainty premiums that resolve when the unknown becomes known. Fisher Investments identifies the central scenario as one where policy direction remains largely unchanged, a result that would exceed the low bar set by current commentary. Recognising that pattern in real time, rather than after the fact, is a repeatable analytical edge.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and political outcomes.

—

Markets rallied because the resignation resolved open-ended uncertainty rather than introducing new risk. The FTSE 100 rose 0.72% on 22 June 2026 because investors could shift from discounting unknowns to pricing a defined range of scenarios under a known leadership contest timeline.

Uncertainty is unquantifiable, such as not knowing who will lead or what they will do, while risk is a defined range of probable outcomes that investors can model and price. Markets tend to struggle more with uncertainty than with quantifiable risk, even when that risk is negative.

As of 26 June 2026, Burnham had not announced concrete policies that would materially reprice UK fiscal credibility. Wealth tax proposals and nationalisation programmes widely cited in commentary are extrapolated from past informal remarks, not formal campaign commitments.

A genuine credibility event produces UK-specific gilt yield spikes that diverge sharply from European peers, as occurred during the 2022 Truss mini-budget. On 22 June 2026, gilt yields rose just 1 basis point in line with European bond markets, confirming a routine session rather than a stress event.

The three key warning signs are: UK gilt yields or sterling diverging sharply from European peers once policy details land, fiscal rules being quietly dropped from Burnham's campaign messaging, and UK assets decoupling negatively from global peers across multiple sessions rather than in a single-day reaction.