3 ASX Blue Chips Built for Long-Term Compounding

13 hrs ago

Most Australians will soon own a slice of SpaceX. Not because they chose to. Not because a financial adviser recommended it. Because the index said so.

SpaceX began trading on the Nasdaq on 12 June 2026, priced at US$135 per share and valued at roughly US$1.75 trillion. Within 17 days, MSCI fast-tracked it into its global indices, effective 29 June 2026. Every super fund and ETF that tracks those indices is now a forced buyer. Millions of Australians whose retirement savings sit in diversified international share options are acquiring SpaceX exposure this week without placing a single trade.

Here is how the engine behind that outcome actually works: how index inclusion operates, why a stock’s initial weighting starts small and grows over time, and what it means in practical dollar terms for your super balance. After reading, you will have a clear mental model of what passive investing does to your portfolio every time a major index is updated.

Somewhere in Geneva, a committee at MSCI updated a list. That update has more practical effect on your super portfolio this week than any investment decision you have made yourself this year.

The reason is straightforward. If your super fund tracks a benchmark like the MSCI World or MSCI All Country World Index (ACWI), it is obligated by mandate to buy any stock admitted to that benchmark. Not “invited to consider.” Obligated. The fund’s entire purpose is to replicate the index, and the index just changed.

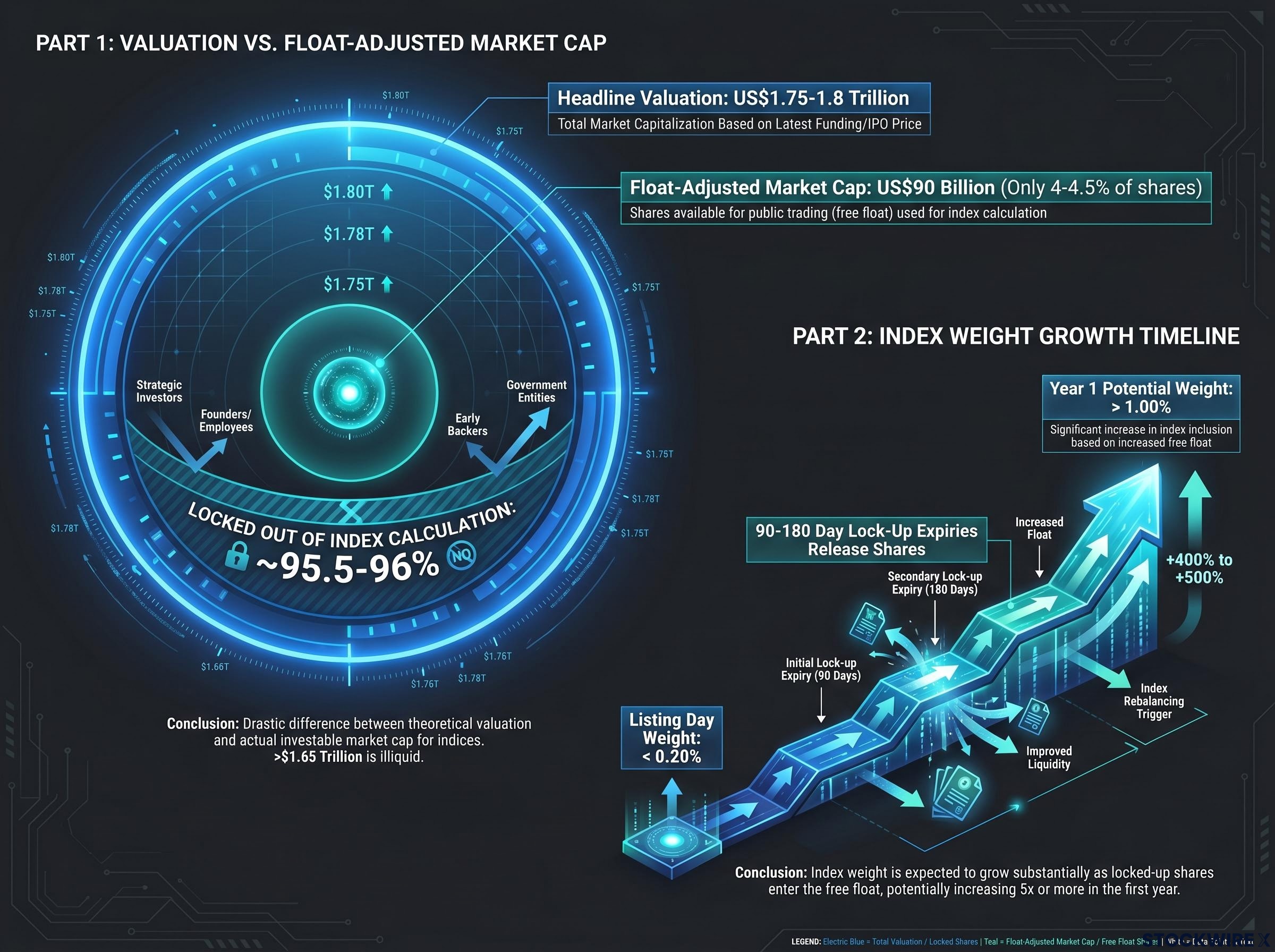

MSCI confirmed SpaceX’s addition to its standard and large-cap indices effective 29 June 2026, approximately 17 days after trading commenced on 12 June 2026. SpaceX listed on the Nasdaq under ticker SPCX at US$135 per share, with a valuation of approximately US$1.75-1.8 trillion. Post-IPO, its market capitalisation briefly exceeded US$2 trillion.

“Owning the index” means owning whatever is on the list. The list just changed, and neither you nor your fund manager had a vote. That is not an anomaly. It is precisely how passive investing is designed to work, and it governs every index rebalancing, not just this one.

An index is a rules-based list of securities that represents a defined segment of a market. The S&P 500 tracks the 500 largest US-listed companies. The MSCI World covers large and mid-cap stocks across 23 developed markets. These lists are not created or maintained by governments or regulators. They are managed by private firms whose entire business is building and licensing benchmarks.

The four names you need to know:

Australian super funds commonly track MSCI World, MSCI ACWI, and major US benchmarks through their international shares options.

Trillions of dollars globally are managed in funds that replicate these indices. When an index committee updates its list, every fund tracking that benchmark must trade to match. The buying is coordinated not by market opinion but by mandate. For you, in a default super option, the entity with the most direct influence over which international shares you own in any given month is likely an index committee you have never heard of, sitting outside Australia.

Not every IPO earns a spot on a major index. There are checkpoints, and watching SpaceX pass through them tells you exactly how the system works.

ASX 200 index inclusion follows a structurally similar two-gate logic to the MSCI process: a company must first clear listing eligibility before it can even be considered for the benchmark, and the free float minimum actually rises from 20% at listing to 30% for index qualification.

| Eligibility criterion | Typical threshold | SpaceX status |

|---|---|---|

| Trading history and liquidity | Minimum trading period, sufficient daily volume | Cleared. US$75B deal size generated heavy volume from day one. |

| Free float | Historically 10%+ of shares available for public trading | Cleared via exception. Float at listing was approximately 4-4.5%. MSCI relaxed its 10% minimum for mega-cap IPOs. |

| Profitability | Positive earnings in most recent quarter and aggregate over prior four quarters (S&P 500 rule) | Not yet cleared. SpaceX is still reporting net losses. |

| Size | Market capitalisation above index minimum | Cleared. US$1.75-1.8 trillion valuation far exceeds any size threshold. |

SpaceX cleared liquidity and size easily. Its US$75 billion deal (555.6 million shares at US$135) was one of the largest IPOs in history. Free float was trickier: only about 4-4.5% of total shares were available for public trading at listing, giving a float-adjusted market capitalisation of approximately US$90 billion against a headline valuation of US$1.75-1.8 trillion. MSCI accommodated this by relaxing its historical 10% float minimum for a listing of this scale.

The S&P 500 profitability rule remains a barrier. The index requires positive earnings in the most recent quarter and in aggregate over the prior four quarters. SpaceX is still reporting net losses. The earliest realistic window for S&P 500 inclusion is mid-2027.

That gap between the US$1.75 trillion headline valuation and the US$90 billion float-adjusted market cap is the single most important number here. It is why your initial SpaceX exposure is far smaller than the company’s fame would suggest, and why it will grow over time as the float expands.

Free-float-adjusted weighting is the mechanism that governs how much of your portfolio a newly listed stock occupies. Only shares available for public trading count toward a stock’s index weight. Insider shares locked up under post-IPO agreements, typically lasting 90-180 days or longer, are excluded from the calculation entirely.

At listing, SpaceX’s public float represented only around 4-4.5% of total shares on issue. Because index weight is calculated on the publicly tradeable portion rather than the full headline valuation, broad index funds such as the Vanguard Total Stock Market ETF (VTI) are expected to assign SpaceX a starting weight of under 0.20%, even though the company’s total valuation exceeds US$1.75 trillion.

The growth happens in stages, and each stage is predictable:

Each of those stages is calendar-based and rules-driven. Your fund does not reassess whether SpaceX is a good investment at the higher weight. It buys because the float expanded and the index weight rose accordingly.

The scale of mandatory index-driven buying that SpaceX’s inclusion requires is significant: Bloomberg Intelligence projects that passive and active benchmarked funds combined must absorb more than 50% of the company’s publicly available float, a concentration of forced demand that goes well beyond a standard large-cap addition.

Morningstar research indicates that as lock-ups expire and more shares enter the free float, SpaceX could exceed 1% weight in some broad cap-weighted indices within its first year of trading. That is a fivefold increase from the sub-0.20% starting point, driven entirely by the mechanics of float expansion and index rebalancing rather than by anyone making a fresh judgement on the company’s investment merit.

Each time a lock-up tranche releases over the next 12-24 months, the resulting float expansion triggers automatic, rules-driven purchases by index funds. Your indirect holding increases on a timetable determined by SpaceX’s capital structure, entirely independent of any investment judgement on your part or your fund manager’s.

The abstract mechanics translate into specific, if initially modest, dollar figures.

At the point of first inclusion, a broad global index fund allocates under 0.20-0.30% to SpaceX. On a $100,000 super balance invested in a global equity index option, that represents approximately $200-300 of indirect SpaceX exposure at the outset.

| Super balance | Estimated exposure at initial inclusion (under 0.20%) | Estimated exposure if weighting reaches 1% |

|---|---|---|

| $50,000 | ~$100 | ~$500 |

| $100,000 | ~$200 | ~$1,000 |

| $200,000 | ~$400 | ~$2,000 |

The near-term dollar impact is modest. But the figure grows as the free float expands, as SpaceX potentially qualifies for additional benchmarks such as the S&P 500, and if performance is strong. Over three to five years, that dollar amount can rise meaningfully without any active trades by you.

Which super options are affected? Those tracking MSCI World, MSCI ACWI, or major US broad market benchmarks are the most directly in scope. Benchmark-aware options (not purely passive, but managed to stay close to an index) may also hold SpaceX if their manager deems it necessary to avoid tracking error. Check your fund’s Product Disclosure Statement (PDS) or investment guide to confirm which benchmark your option tracks.

The $200-300 starting figure matters less than what it represents: a decision made by an index provider that your super fund is obligated to implement. That pattern will repeat in larger increments every time SpaceX’s float expands and the index is rebalanced.

For most Australians in default diversified super options, the SpaceX exposure change is not a reason to switch funds or take any urgent action. The initial dollar figure is small, and the inclusion process is functioning exactly as designed.

The real value of understanding how index inclusion works is longer-term. It changes how you think about what “passive investing” actually means. When you choose a benchmark-linked option in your super, you are not choosing a fixed basket of shares. You are delegating the composition of your portfolio to whichever index committee manages that benchmark. Every time the list changes, your portfolio changes with it.

If you want to understand your specific exposure, three steps will get you there:

Understanding this process equips you to evaluate every future major IPO inclusion, not just this one. It also gives you a more accurate basis for any conversation with a financial adviser about what your “passive” super option is actually doing on your behalf.

For investors who want to apply this process to their existing super option, our dedicated guide to evaluating fund benchmarks walks through a five-step due diligence checklist that covers benchmark identification, fee term review, and how to spot structures where the hurdle rate understates the fund’s actual risk level.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Index inclusion is rules-based and continuous. The lists that define your super portfolio are updated regularly, sometimes on a fast-track timeline measured in days. That means passive portfolios are never truly static. They change every time a company goes public at sufficient scale, every time a float expands, and every time an index committee reviews its eligibility criteria.

This is neither good nor bad by design. It is simply how the system works. The question worth asking is whether the benchmark your super tracks still aligns with how you want your retirement savings managed, and whether you understand what choosing “passive” actually delegates.

Today it is SpaceX: MSCI fast-tracked inclusion effective 29 June 2026, with anticipated S&P 500 eligibility from mid-2027 at the earliest, and ongoing float expansion over one to two years. Next year it will be a different company. The mechanics will be identical. Float expands, index weight rises, passive funds buy more, your exposure grows.

Index concentration risk is a structural feature of cap-weighted benchmarks, not a temporary condition: five mega-cap stocks controlled approximately 23% of the broad US market index as of mid-April 2026, a level that has surpassed the historical concentration peak of the 1930s and amplifies moves in both directions for passive holders.

“Choosing passive investing is itself an active decision. The question is which committee you are delegating to.”

When a stock lists and meets an index provider's eligibility criteria (size, liquidity, and free float thresholds), the index committee adds it to the benchmark at its next scheduled or fast-tracked rebalancing. Every fund mandated to replicate that index must then buy the stock to match the new composition, regardless of any investment opinion on the company.

Index weight is calculated on the float-adjusted market capitalisation, meaning only publicly tradeable shares count. At listing, SpaceX's public float was approximately 4-4.5% of total shares, giving a float-adjusted market cap of around US$90 billion against a headline valuation of US$1.75-1.8 trillion, which is why broad index funds are assigning it a starting weight of under 0.20%.

At initial inclusion, a super balance of $100,000 invested in a global equity index option would hold approximately $200-300 of indirect SpaceX exposure. That figure is expected to grow as lock-up periods expire, the float expands, and SpaceX's index weight rises, potentially exceeding 1% in some broad indices within the first year of trading.

The S&P 500 requires a company to have positive earnings in its most recent quarter and in aggregate over the prior four quarters. SpaceX is still reporting net losses, so the earliest realistic window for S&P 500 inclusion is mid-2027 at the earliest, even though its market capitalisation far exceeds the size threshold.

You cannot remove a single stock from an index-linked option, but you can switch to a different investment option within your fund that tracks a different benchmark or uses an active mandate that is not obligated to hold SpaceX. Check your fund's Product Disclosure Statement to confirm which benchmark your current option tracks before making any change.