A strange contradiction defines the Australian market outlook as of June 2026. The headline equity index projects stability with positive daily movements, yet underlying property and domestic cyclical sectors face their most severe test since 2020. This tension became impossible to ignore when preliminary auction clearance rates plunged to 47% last week.

The domestic equity market is currently caught between two powerful, opposing forces. A definitive housing downswing is actively destroying consumer wealth effects and restricting discretionary spending across the economy. Simultaneously, large publicly listed corporations are executing aggressive and sometimes painful restructurings to defend their profit margins against these exact economic headwinds.

What follows gives you a clear framework for identifying which parts of the market are hiding fundamental weakness behind strong index performance. It also details how you can spot the specific companies successfully future-proofing their operations against the domestic slowdown.

The mechanics of the 2026 property downturn and REIT valuations

The Australian housing sector is demonstrating clear signs of a cyclical contraction. You can see this deterioration clearly in the latest real estate metrics, which point to a definitive buyer’s market.

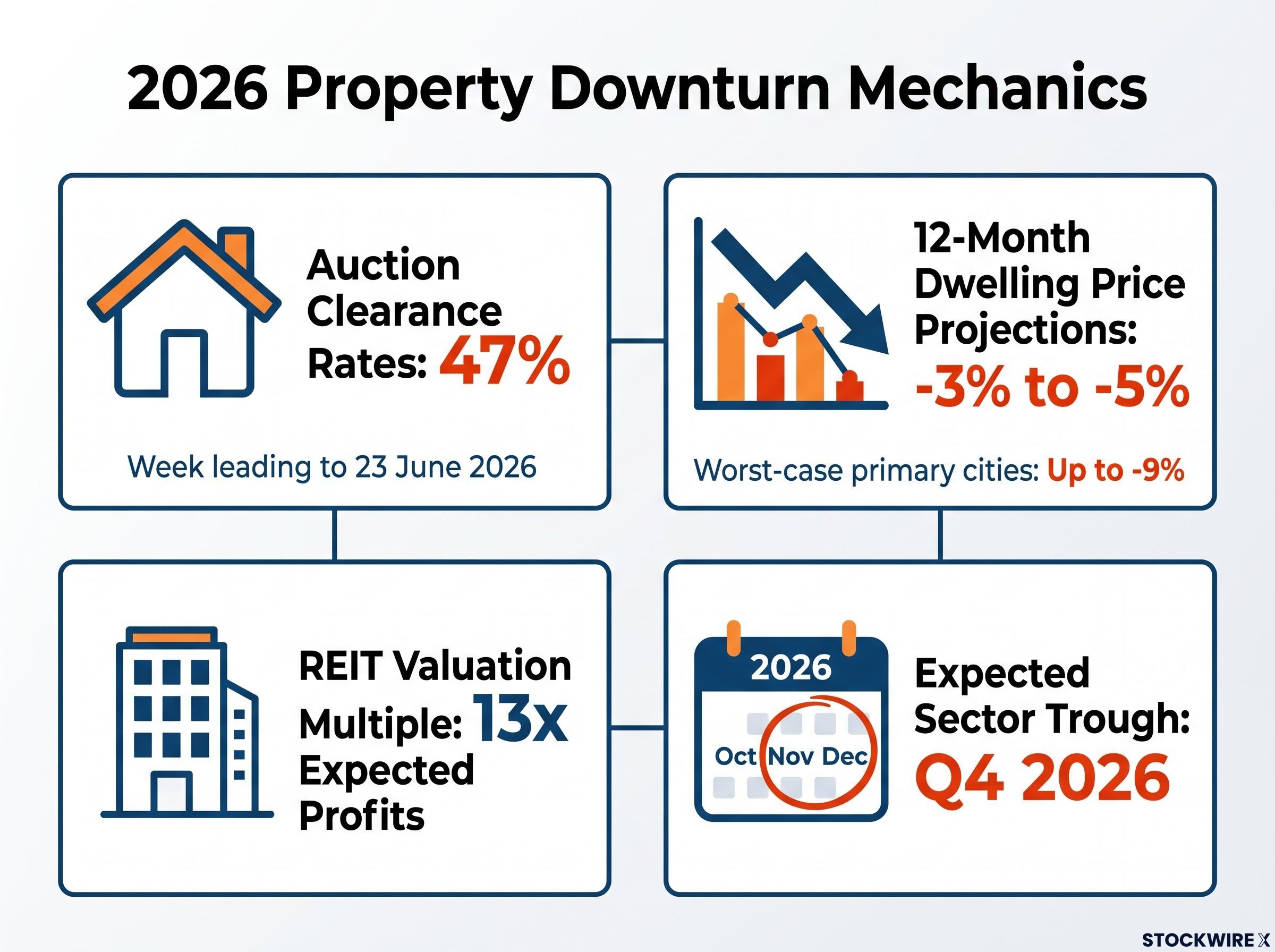

Initial clearing rates at housing auctions dropped to 47% during the seven days leading up to 23 June 2026. Analysts project that dwelling prices across the country are set to drop between 3% and 5% in the upcoming 12 months, while worst-case models suggest potential falls of up to 9% within primary city markets. * Listed real estate vehicles currently trade at a multiple of approximately 13 against expected future profits, placing their pricing a full two standard deviations underneath historical averages.

This macro weakness translates directly into pricing pressure for listed property developers and Real Estate Investment Trusts (REITs). The market is pricing in the expectation of lower asset values, but net asset value estimates often lag behind real-time auction clearance declines.

The RBA Financial Stability Review on household resilience quantifies the degree to which elevated mortgage debt is suppressing consumer spending capacity, providing the macroeconomic scaffolding that explains why discretionary retail and construction businesses are bearing the brunt of the current contraction.

These deeply discounted multiples on property trusts look tempting on a screen. However, you must recognise these as familiar late-cycle value traps where earnings estimates have not yet caught up to the reality of the credit cycle. Earnings downgrades and capitalisation rate pressure typically drive sentiment lower before the fundamentals fully bottom out.

Sector Trough Warning Market experts recommend holding off on buying major housing-linked property funds until the downturn nears its end, pointing to the final quarter of 2026 as the likely bottom for the industry.

Understanding the depth of this housing contraction prevents you from catching a falling knife in property-linked equities. It establishes the baseline economic reality that will drive the rest of the market’s behaviour over the next six months.

When big ASX news breaks, our subscribers know first

Educational breakdown: Why index optics are masking underlying market pain

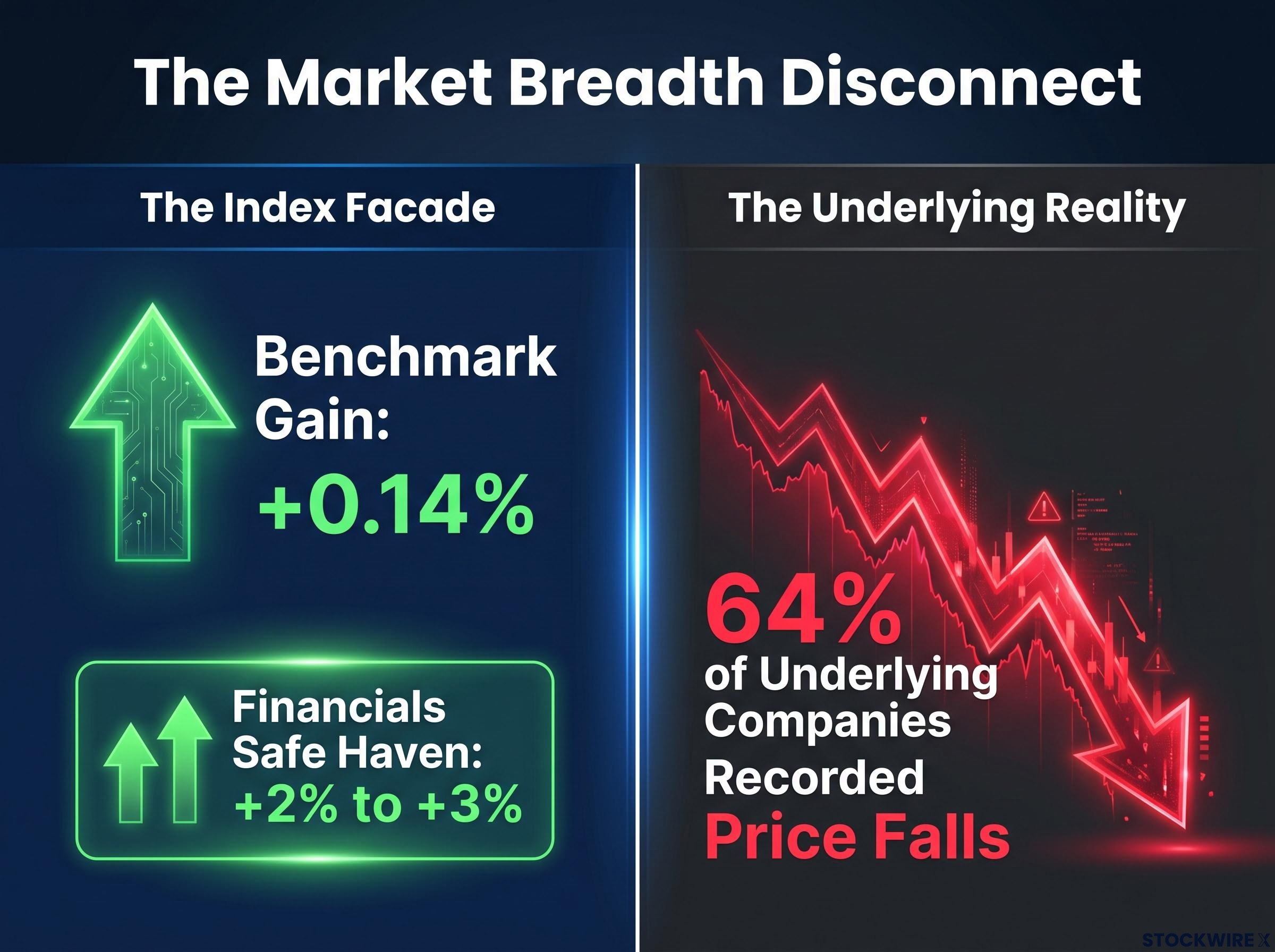

Market breadth measures how many individual stocks are participating in a broader market move. It contrasts sharply with market-capitalisation weighted indices, where the largest companies dictate the headline performance regardless of what the majority of businesses are experiencing.

A recent trading session perfectly illustrated this divide, as the primary local share benchmark posted a minor gain of 0.14%. Underneath this facade of steadiness, however, 64% of the underlying companies recorded price falls.

A deeper dive into ASX market breadth data confirms this structural divergence, revealing that the vast majority of constituents are trading significantly below their annual highs while a few mega-cap names artificially prop up the headline index.

The safe haven illusion in financials

The banking and financial sectors are acting as relative safe havens, driving that top-heavy index performance. Shares in financial institutions climbed between 2% and 3% across a recent week of trading, shrugging off their usual vulnerability to property market fluctuations.

Investors are treating these major banks as well-capitalised dividend payers that still benefit from elevated interest margins. This creates severe performance dispersion between large-cap defensive stocks and small-cap domestic cyclicals, such as discretionary retail and construction businesses.

You cannot rely on the main ASX benchmark to tell you how your individual holdings are performing. A handful of major banks are currently camouflaging widespread weakness across smaller, domestically focused businesses. This knowledge equips you to look under the hood of market returns rather than assuming a diversified portfolio is safe simply because the evening news reports a rising index.

Margin defence and the era of aggressive footprint rationalisation

Faced with slowing growth, major domestic listed entities are reorganising their operations to protect their profitability. Management teams are actively sacrificing short-term optics to ensure long-term viability. They are taking immediate, painful write-downs to improve future returns rather than merely playing defensive damage control.

When you see a company taking a massive one-off restructuring charge right now, you should evaluate their underlying motive. You need to determine whether they are structurally fixing their unit costs or simply bleeding cash in a dying division.

| Company | Specific Action Taken | Financial Impact | Strategic Reality |

|---|---|---|---|

| Reliance Worldwide | Terminated Australian brass facilities | $9 million USD annual uplift vs $100 million to $110 million USD hit | Sacrificing domestic operations for structural cost improvement |

| Metcash | Reorganising hardware division | 2.4% underlying NPAT decrease to $268.8 million AUD | Defensive damage control amid consumer down-trading |

Sacrificing domestic goodwill for global scale

Reliance Worldwide serves as a prime example of proactive margin defence. The plumbing systems manufacturer is terminating its Australian brass component production to optimise its global footprint.

Shutting down these facilities will generate a yearly gross profit boost of $9 million USD, but it comes at the cost of an isolated write-off spanning from $100 million to $110 million USD. The company is pursuing higher Return on Invested Capital (ROIC) over maintaining local production, accepting a large immediate charge to lower future unit costs.

Navigating consumer down-trading in retail

Companies highly exposed to consumer down-trading face a different operational reality. Metcash announced a drop in its core post-tax profits to $268.8 million AUD, driven by sustained headwinds impacting its hardware operations.

This widespread consumer retreat aligns with broader macroeconomic indicators confirming a per capita recession, as rising essential costs and historically low confidence levels heavily restrict discretionary spending across the domestic economy.

The distribution conglomerate is balancing immediate margin defence with the need for selective investment. The enterprise is striving to keep shareholders onside during these tough economic times by upholding its total annual payouts at 18 cents for each share held.

Securing future revenues and managing idiosyncratic risks

While some companies focus on defensive cost-cutting, others are pursuing offensive revenue security. In an environment where domestic earnings are highly uncertain, your portfolio gains significant resilience from companies holding hard-contracted revenue streams extending into the next decade.

The extreme value of locking in long-dated export revenues becomes clear when the domestic cycle is contracting. Iluka Resources just locked in an electric vehicle supply deal ensuring baseline sales worth $155 million USD. The arrangement guarantees the delivery of 1,200 tonnes of magnetic oxides across a four-year window starting in 2028, providing the mineral sands business with a buffer against domestic financial instability.

Conversely, highly valued technology and growth names are proving exceptionally vulnerable to non-operational news and governance risks. In a bifurcated market, investors have zero tolerance for key-person risk.

WiseTech Global suffered a steep single-day stock plunge of 18.4%, landing at $30.08 AUD. Unverified press rumours regarding the personal legal affairs of its leadership sparked this harsh sell-off, highlighting just how quickly market mood can detach from core business performance.

Valuation Premium Lesson The current market demands a clear separation between headline key-person risk and underlying business model risk. Investors place a massive safety premium on contracted future cash flows while severely penalising any governance uncertainty.

Tactical capital allocation in a bifurcated environment

You must position your capital to survive the immediate domestic contraction while keeping enough powder dry to buy high-quality assets when the expected market trough finally arrives. The current environment heavily punishes impatience and rewards those who wait for valuations to reflect economic realities.

This patience requires investors to monitor how interest rates drive REIT valuations, as the cost of debt financing and yield competition with government bonds will dictate the pace of any eventual recovery in the commercial property sector.

This requires synthesising the macro housing realities and micro corporate actions into a concrete portfolio strategy. The following sequential framework helps you navigate the current volatility.

- Delay exposures: Exercise patience regarding housing-linked equities and REITs until the expected real estate stabilisation timeline arrives in Q4 2026.

- Favour agility: Target companies proactively restructuring their cost bases or securing Iluka-style offtake agreements that lock in long-term demand.

- Lean into quality: Be highly selective regarding large-cap defensives, ensuring you do not overpay for the perceived safety of major financials.

- Manage liquidity: Maintain sufficient cash reserves to capitalise on market over-reactions and acquire fundamentally sound assets when sentiment bottoms.

Applying these steps translates complex market analysis into actionable portfolio management. It prevents you from committing capital prematurely while positioning you for the eventual cyclical recovery.

Calibrating risk for the remainder of the year

The core tension between stable index optics and underlying economic reality will define the Australian market over the next six months. The true test for domestic equities remains management’s ability to defend profit margins without destroying long-term operational capacity.

Passive index investing currently masks significant sectoral risks, making active management a necessity rather than an option. Your success depends on looking past the headline index numbers to identify which companies are genuinely prepared for the slowdown.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.