Global REITs are trading nearly 30% cheaper than historical levels relative to global equities, yet most investors cannot name the four specific mechanisms through which interest rates drive that valuation gap. With the Federal Reserve holding rates at approximately 3.75%, the European Central Bank at 2.15%, and the Bank of Canada at 2.25% as of early 2026, the relationship between rate movements and REIT pricing is no longer an abstract exercise. The same mechanics that create opportunity in a cutting cycle also create concentrated risk when rates reverse, and leverage amplifies both directions. This article decodes all four interest rate transmission channels that move REIT valuations, explains the underlying mechanics of each in plain terms, and maps the full spectrum of REIT-specific risks so readers can evaluate any allocation with a complete picture, not just the tailwind narrative.

What makes REITs structurally different from ordinary equities

REITs are not simply property stocks listed on an exchange. Their legal architecture creates a structural sensitivity to interest rates that ordinary equities do not share, and understanding that architecture is what makes the four rate channels feel logical rather than arbitrary.

Three characteristics set REITs apart:

- Mandatory income distribution: Most jurisdictions require REITs to distribute 90% or more of taxable income as dividends, leaving minimal retained earnings for reinvestment.

- Long-duration debt financing: Property assets are financed over extended terms, meaning REITs carry debt structures directly exposed to long-term borrowing rates.

- Repeated capital market access: Because most income flows out as dividends, REITs must return to equity and debt markets repeatedly to fund growth, making them persistently sensitive to credit conditions and investor appetite.

The income distribution requirement and its consequences

The 90% distribution threshold is what creates the dividend yield benchmark dynamic covered in later sections. It forces REITs to pay out nearly all taxable income, which means their share prices are evaluated by income-seeking investors against alternative yield instruments, particularly government bonds. This is not a feature shared by growth equities that retain and reinvest earnings.

The structural architecture that makes REITs sensitive to bond yields also makes them a natural fit within yield-focused investment strategies, though a decade of backtested return data shows that dividend-prioritising portfolios have historically underperformed total return approaches by a margin that compounds materially over 20-year horizons, a trade-off REIT investors benchmarking against government bond yields should factor into their return expectations.

Long-duration debt and repeated capital market access

Property assets financed over 10- to 20-year terms mean REITs lock in borrowing costs for extended periods, but each refinancing event creates fresh exposure to prevailing rates. Singapore’s Monetary Authority (MAS) revised the aggregate leverage limit for REITs to 50% in late 2024 (up from 45%), with a minimum interest coverage ratio of 1.5 times, a concrete recognition of how central leverage is to REIT risk. Analysts have identified leverage as the single most significant risk factor in REIT returns, outperforming other variables such as cash flow volatility in asset pricing models.

The MAS leverage rationalisation for REITs, effective November 2024, consolidated the aggregate leverage limit at 50% and introduced a minimum interest coverage ratio of 1.5 times, codifying in regulatory requirements the same balance sheet constraints that analysts identify as the primary determinant of REIT return variability.

Repeated equity and debt issuance means investor sentiment and credit spreads directly affect growth capacity. When credit conditions tighten, the cost of funding new acquisitions rises, and when they loosen, REITs can grow more cheaply. This structural dependence on external capital is what makes interest rate movements matter to REITs in ways they do not matter to a software company sitting on retained earnings.

When big ASX news breaks, our subscribers know first

Channel three and four: cost of capital compression and the yield competition with bonds

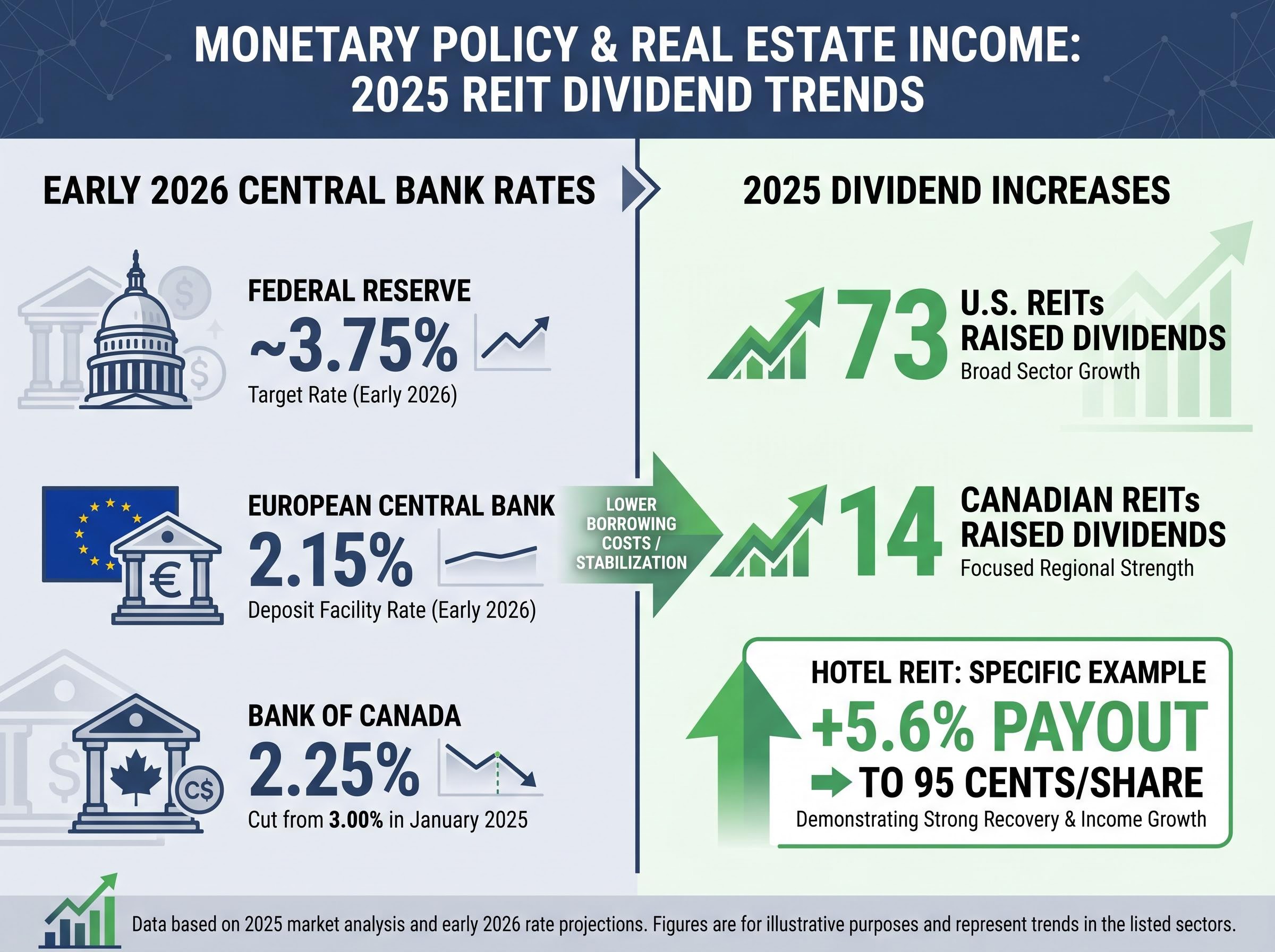

Lower borrowing costs hit REIT balance sheets directly. When rates fall, the cost of refinancing existing debt declines, reducing interest expense and improving the pool of income available for distribution. This is the cost-of-capital channel, and its effects showed up clearly across 2025 dividend activity.

- 73 U.S. REITs raised dividends in 2025, with lower interest rates directly supporting these decisions by easing debt service costs and improving distributable income.

- 14 Canadian REITs raised dividends in 2025 following Bank of Canada cuts that brought the policy rate to 2.25% by April 2026.

- A hotel REIT increased total payouts by 5.6% to 95 cents per share for the full year, reflecting the operational benefit of lower financing costs.

The second channel operates on the investor side. REIT dividend yields are conventionally benchmarked against long-term government bond yields. When bond yields fall, REIT dividends become relatively more attractive to income-seeking investors, increasing demand for REIT shares and lifting prices. This yield competition dynamic means that even without any operational improvement, REIT share prices can rise simply because the alternative source of income, government bonds, has become less generous.

The REIT yield premium over government bonds is not static: Waypoint REIT’s 6.9% distribution yield against a 4.7% ten-year bond rate in early 2026 represents the kind of income spread that the yield competition channel predicts should attract income-seeking capital, though the 14.5% discount to net tangible assets also shows that market pricing does not mechanically close that gap without additional catalysts.

Both channels strengthen during a rate-cutting cycle. Both reverse sharply if rates rise unexpectedly. The symmetry is worth holding in mind: the same mechanics that lifted 73 U.S. REIT dividends in 2025 would compress distributable income and reduce yield competitiveness in a hiking cycle.

The table below provides the central bank rate context in which these dividend increases occurred.

| Central Bank | Rate as of Early 2026 | Direction Since 2024 |

|---|---|---|

| Federal Reserve | ~3.75% | Multiple cuts through 2025 |

| European Central Bank | 2.15% | Cut 0.25% in June 2025; further reductions |

| Bank of Canada | 2.25% | Cut from 3.00% (January 2025) to 2.25% |

| Reserve Bank of Australia | Easing cycle underway | Rate reductions initiated |

Channel one and two: how rates signal the economic outlook and reset asset values

A single rate cut carries two simultaneous messages, and both move REIT valuations in the same direction.

- The economic outlook signal. Long-term interest rates reflect investor consensus on future economic growth and inflation. A sustained fall in rates signals anticipated economic deceleration. Historically, this environment has correlated with REIT outperformance because their contractual rental income and defensive dividend characteristics become more valuable when growth is scarce.

- The discount rate effect. Future REIT cash flows are worth more in present-value terms when the rate used to discount them falls. The 10-year U.S. Treasury yield serves as the primary benchmark for this calculation. A lower reading lifts assessed valuations even before any operational improvement occurs, purely through the mathematics of discounted cash flow.

These two channels operated simultaneously during the rate-cutting cycle of 2024-2026, creating compounding upward pressure on REIT valuations. The economic signal said growth was slowing (making REIT income more attractive on a relative basis), while the discount rate reset said the same cash flows were worth more in today’s terms.

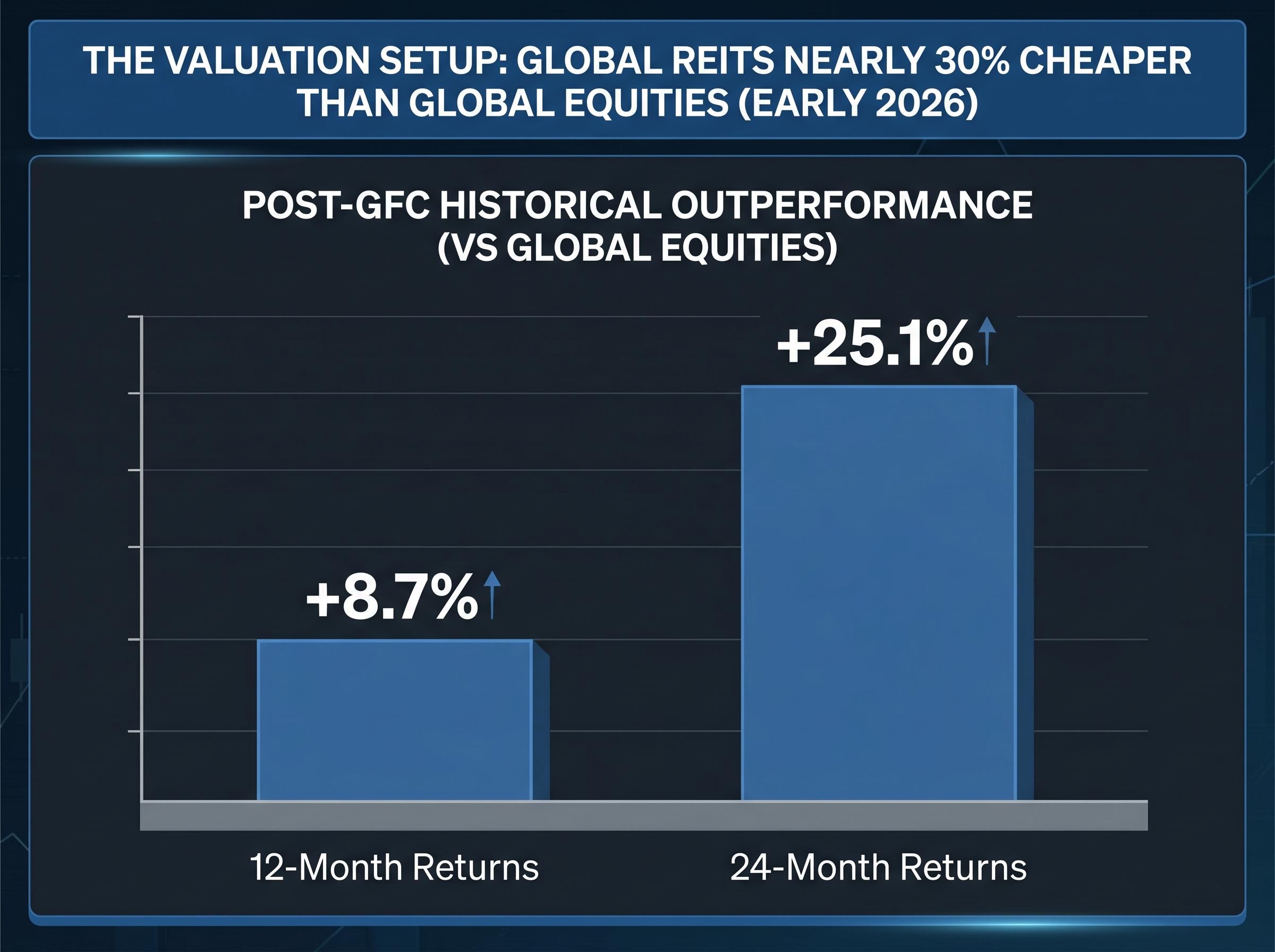

When global REITs previously traded at comparable discounts to global equities (approximately 30% cheaper), subsequent 12-month REIT returns outpaced global equities by 8.7% and 24-month returns by 25.1%, based on post-Global Financial Crisis (GFC) data.

This pattern matters because it explains why REIT valuations can rise sharply even in a weakening economy, something that appears counterintuitive to investors who treat falling rates as a warning signal rather than a REIT catalyst. Both channels are active right now: global REITs are trading nearly 30% cheaper than historical levels versus global equities as of early 2026, echoing the setup that preceded prior outperformance cycles.

The risks that the rate tailwind does not eliminate

A favourable rate environment does not remove the risks specific to owning REITs. The four channels described above can be overridden by property-level deterioration, market-level shocks, or structural shifts that operate independently of central bank decisions.

Property-level and operational risks

- Occupancy and rental variability. Vacancy rates can rise if tenants downsize or exit, and rental pricing is subject to supply and demand imbalances in local markets. Zoning changes and rent controls can further compress income.

- Property taxation and environmental legislation. Rising property taxes and tightening environmental compliance requirements add to operating costs.

- Climate and insurance cost inflation. Insurance cost spikes and extreme weather events represent a growing structural expense, particularly in coastal U.S. regions, Australia, and Southeast Asian markets.

- Leverage amplification. Higher leverage magnifies both upside and downside sensitivity to rate changes. The MAS leverage limit of 50% with a 1.5 times interest coverage ratio illustrates how regulators recognise this risk. Near-term debt maturities create refinancing exposure if credit conditions tighten unexpectedly.

- Tariff-driven construction costs. Increases on aluminium, steel, and lumber raise development costs for REITs with active pipelines.

Market-level and macro risks

- Equity market sell-offs. REITs as listed securities face broad risk-off events regardless of underlying property fundamentals. Singapore REITs fell 3% and Australian REITs fell 4.6% during a yen-carry trade unwind, illustrating how currency dynamics can drag REIT prices lower even when property income is stable.

- Geopolitical volatility. Middle East escalation, yen carry trade dynamics, and U.S. dollar weakening all affect global investor returns from REIT holdings.

- Stagflation. If growth slows while inflation remains elevated, REITs face a particularly difficult environment: weaker tenant demand combined with rising operating costs and potentially higher discount rates.

- Dividend variability. Distributions are not guaranteed. Companies may reduce or discontinue dividends without notice if occupancy falls, operating costs rise, or refinancing becomes more expensive. The income stream is not bond-like in its certainty.

- Labour market conditions. The U.S. unemployment rate at approximately 4.3% as of March 2026 provides context for office and retail demand, where a weakening labour market could reduce tenant absorption.

Sectors within REITs do not all move together

Treating REITs as a monolith misses the internal differentiation that often determines actual returns. Rate sensitivity, growth drivers, and risk profiles vary substantially by property type.

ISM Manufacturing PMI readings of 52.7 in April 2026 and 52.4 in February 2026 indicate expansion rather than contraction, creating a more constructive backdrop for industrial and logistics REITs than some recession-risk narratives suggest.

Office and retail/mall REITs, now at lower weightings in major benchmarks, face ongoing structural headwinds from remote work adoption and shifting consumer behaviour. Data centre and healthcare REITs have demonstrated relative resilience even in broad sell-offs, supported by the contractual, long-term nature of their leases and secular demand from AI infrastructure investment and ageing populations, though a deep recession could override even these defensive characteristics.

Retail REIT sub-sector performance in Australia illustrates this divergence in sharp relief: Scentre Group and Vicinity Centres are operating at 99.8% and 99.6% occupancy respectively in 2026, posting positive leasing spreads of 3.3%-4.6%, while office-focused peers like Dexus have flagged delayed recovery, confirming that a falling rate environment does not lift all property types uniformly.

Higher construction costs from tariff-driven material price increases, while a risk for development-heavy REITs, paradoxically benefit existing asset owners by suppressing new competitive supply. This dynamic varies significantly by sub-sector.

| Sub-Sector | Current Structural Tailwinds | Key Risk Factors |

|---|---|---|

| Data Centres | AI and cloud infrastructure demand; long-term leases | Tariff risk on non-exempt components; energy cost inflation |

| Industrial/Logistics | Manufacturing PMI expansion; e-commerce fulfilment demand | Cyclical exposure if recession materialises; construction cost pass-through |

| Office | Limited new supply supporting existing asset values | Remote work structural shift; tenant downsizing; high vacancy rates |

| Retail/Mall | Reduced benchmark weighting reflects repositioning | Consumer spending sensitivity; e-commerce displacement; labour market risk |

Rate cycles turn, and REIT investors need to be ready for both directions

All four channels described in this article are bidirectional. The cost-of-capital compression that lifted 73 U.S. REIT dividends in 2025 reverses when borrowing costs rise. The yield competition that draws income seekers away from bonds reverses when bond yields climb. The discount rate effect that inflates present values reverses when Treasury yields increase. The economic signal that favours defensive income reverses when growth accelerates and capital rotates toward cyclicals.

The current environment, featuring falling real yields, depressed valuations echoing post-GFC setups, and improving real estate capital markets, has historically preceded REIT outperformance cycles. Post-GFC data showed 8.7% and 25.1% outperformance at comparable valuation discounts over 12 and 24 months respectively. Global REITs remain nearly 30% cheaper than historical levels versus global equities as of early 2026.

Inflation uncertainty, however, complicates the forward path. AI-driven energy demand, elevated fiscal deficits, immigration-driven labour market tightness, and tariff pass-through all represent sources of sticky inflation that could slow the cutting cycle or reverse it.

The risk that makes the current setup asymmetric is not a gradual rise in borrowing costs but a commodity-driven inflation shock that forces central banks to abandon their cutting cycles entirely; rate reversal scenarios driven by sustained oil prices above $100 per barrel have already repriced Fed, ECB, and Bank of England expectations simultaneously in 2026, compressing the window in which all four channels operate in REITs’ favour.

Four variables deserve ongoing monitoring:

- Real yield movements (not just policy rates), which capture the inflation-adjusted cost of capital that drives REIT valuations.

- Debt maturity profiles of individual REITs, which determine refinancing exposure timing.

- Sector-level supply dynamics, which dictate whether new construction will dilute existing asset values.

- Dividend coverage ratios, which signal the sustainability of current distributions before cuts are announced.

The four channels and the risk taxonomy presented here are not a buy signal. They are an analytical framework that applies in any rate environment, whether rates are falling, rising, or holding steady.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.