Why Governance and Communication Drive Post-IPO Value

7 hrs ago

Most Australian investors know they should be diversified, but building and maintaining a diversified portfolio typically means buying multiple ETFs, tracking different markets, deciding on bond allocations, and rebalancing manually when markets drift. The Vanguard Diversified High Growth Index ETF (ASX: VDHG) is designed to collapse all of that into a single ASX trade.

VDHG has become one of the most discussed single-fund solutions among Australian retail investors precisely because it sidesteps the complexity problem. It holds a globally diversified mix of equities and bonds, rebalances automatically, and charges 0.27% per annum for the privilege. For investors who want a growth-focused portfolio without managing multiple moving parts, it warrants serious attention.

By the end of this piece, you will understand exactly how VDHG is constructed, what it holds, who it genuinely suits, and where its limits are, so you can decide whether it belongs in your portfolio or whether a different approach better matches your circumstances.

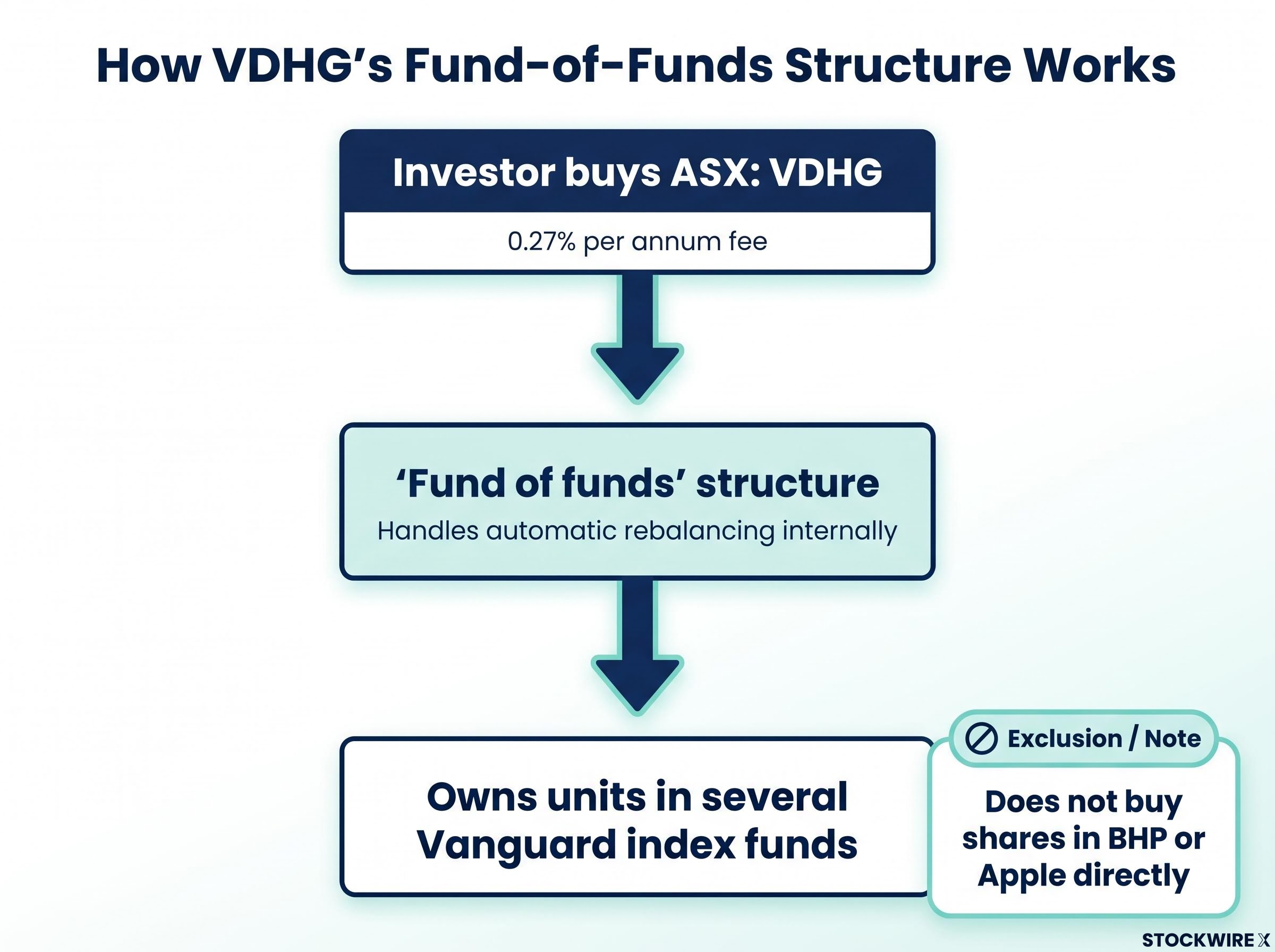

If you assume VDHG works like any other ETF on the ASX, the mechanics will surprise you. Most ETFs track a single index: one fund buys Australian shares, another buys global bonds, another tracks the S&P 500. VDHG does something structurally different. It is a “fund of funds,” meaning it holds units in several underlying Vanguard index funds rather than individual shares or bonds directly.

The mechanics behind how ETFs work on the ASX, including how units are created, how market prices track underlying net asset value, and how brokerage executions differ from managed fund applications, form the foundation for evaluating any listed fund, including a fund-of-funds structure like VDHG.

The name itself tells you what you are getting:

VDHG was launched on 20 November 2017 by Vanguard Investments Australia Ltd (ABN 72 072 881 086 / AFS Licence 227263). Its investment objective is to track the weighted average return of the indices of the underlying funds in proportion to the strategic asset allocation, before fees, expenses, and tax. The management fee sits at 0.27% per annum.

When you buy a unit of VDHG, you are not buying shares in BHP or Apple directly. You are buying into a vehicle that itself owns units in several Vanguard index funds, each tracking a different market or asset class.

This is where the simplicity advantage originates. Vanguard manages all allocation and rebalancing internally at the VDHG level. You are not evaluating individual holdings; you are evaluating whether Vanguard’s allocation decisions align with your goals.

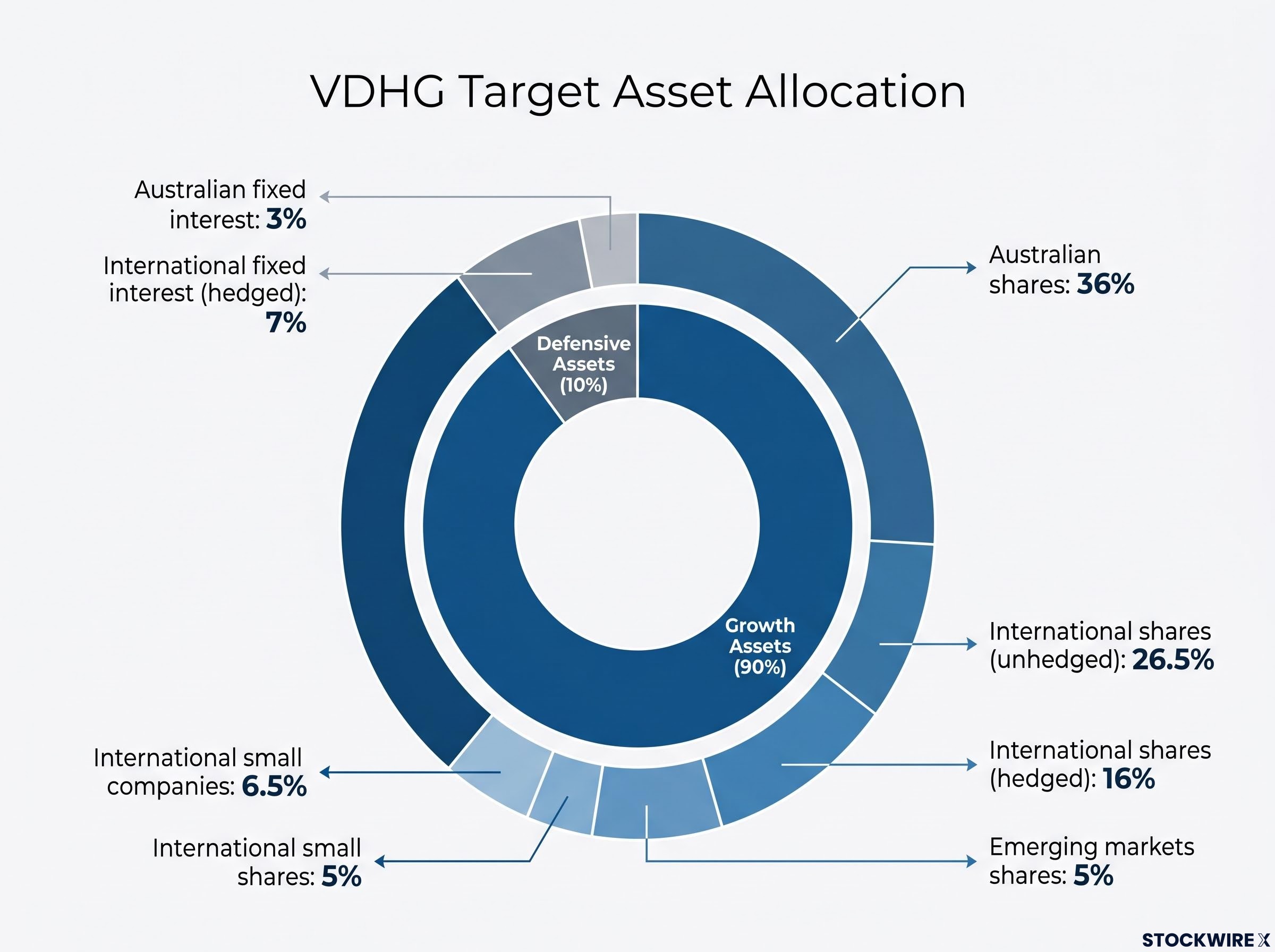

The governing principle: 90% growth assets, 10% defensive assets. This split determines VDHG’s risk profile, return potential, and behaviour during market downturns.

The 90% growth allocation is spread across Australian and international equities. The 10% defensive allocation sits in bonds. Understanding exactly how those buckets break down tells you what you actually own.

| Asset Class | Target Weight |

|---|---|

| Australian shares | 36% |

| International shares (unhedged) | 26.5% |

| International shares (hedged) | 16% |

| International small companies | 6.5% |

| Emerging markets shares | 5% |

| International fixed interest (hedged) | 7% |

| Australian fixed interest | 3% |

The 36% weighting to Australian shares means your VDHG holding is more concentrated in the Australian economy than global market capitalisation would suggest. If your super, your property, and your income are all tied to the Australian economy, that home-market tilt may be compounding your domestic exposure in ways you have not accounted for.

The 90% equity weighting also means VDHG will fall materially when equity markets fall broadly. This is a growth fund, not a balanced one.

The bond allocation, split between 7% international fixed interest and 3% Australian fixed interest, is designed to moderate volatility rather than eliminate drawdowns. In a mild correction, bonds may cushion the impact slightly. In a severe equity sell-off, a 10% defensive allocation provides limited protection. You should not expect the bonds inside VDHG to shield you significantly if global equities drop 20% or more.

If you hold only ASX-focused investments, you might feel diversified across banks, miners, healthcare, and retail. The structural problem is that Australia represents a small fraction of global market capitalisation, and the ASX is concentrated in relatively few sectors, particularly financials and materials.

ASX sector concentration in financials and materials is a structural feature of the domestic index, not an accident, and it means that an investor holding only Australian equity ETFs carries meaningful exposure to bank credit cycles and commodity price volatility regardless of how many local funds they hold.

Australia’s share market represents a small fraction of the world’s total investable market. Holding only ASX exposure means missing the majority of global investment opportunities.

VDHG addresses this directly. Its international equity exposure, when combined, accounts for approximately 54% of the portfolio:

That international allocation gives you access to major technology firms, global consumer brands, and healthcare multinationals that simply are not available on the ASX. If more than half of VDHG’s weight sits in international equities, a portfolio holding only ASX ETFs would be missing the majority of the world’s investable market. VDHG is partially designed to correct that gap.

This matters particularly if your income, superannuation, and property are already heavily tied to the Australian economy. Your global equity exposure through VDHG may be the only meaningful international diversification in your financial life.

Knowing what VDHG holds is one thing. Understanding what it does for you operationally is where the practical value becomes concrete.

Vanguard handles all rebalancing internally, periodically restoring the portfolio to its target allocation as market movements cause drift. If Australian shares rally and push from 36% to 40% of the portfolio, Vanguard adjusts the balance without you placing a single trade.

The alternative is managing this yourself. With a multi-ETF portfolio, you monitor drift across five or six funds, calculate rebalancing trades, and execute them manually. Each trade involves a decision, and each decision creates an opportunity to second-guess your allocation, chase a hot sector, or delay a rebalance because you feel the market will keep running.

With VDHG, your decisions reduce to three:

The behavioural benefit is real. Automatic rebalancing removes the temptation to tinker, chase themes, or react emotionally to short-term market moves, all of which tend to harm long-term outcomes.

Building a similar allocation with individual index ETFs can sometimes produce a marginally lower total management cost. Some investors save a few basis points by assembling their own mix.

Total cost of ETF ownership extends beyond the headline management expense ratio to include tracking difference, bid-ask spread, and brokerage commissions, all of which compound over long holding periods and should be factored into any cost comparison between a single-fund solution like VDHG and a self-assembled multi-ETF portfolio.

But the cost comparison is incomplete if you only look at fees. You also need to account for the time spent monitoring, the effort of executing rebalancing trades, and the behavioural risk of making poorly timed changes. For most retail investors, the real cost of managing multiple ETFs is not the slightly lower fee but the decision-making burden. VDHG’s 0.27% annual charge covers the allocation and rebalancing service, and for many investors, that is a cost well justified by the discipline it enforces.

Understanding the fund is one thing. Locating yourself relative to it is what actually matters for your decision.

Vanguard positions VDHG as a fund for investors with a 7+ year investment horizon.

| VDHG suits you if… | VDHG may not suit you if… |

|---|---|

| You have a long investment horizon (7+ years) | You need your money within a few years |

| You are comfortable holding through significant drawdowns | You need capital preservation or cannot tolerate sharp falls |

| You prefer a hands-off, automated approach | You want control over your specific asset allocation |

The investor who genuinely benefits from VDHG is typically in the wealth-accumulation phase: building long-term savings, comfortable letting a mostly-equity portfolio ride through market cycles, and willing to accept that simplicity means surrendering control over the specific mix.

The investor who struggles with VDHG is someone whose circumstances conflict with its design. If your investment horizon is shorter than seven years, or your financial situation means you cannot afford to hold through a significant drawdown without selling, VDHG’s 90% equity weighting is likely too aggressive for your circumstances, regardless of how appealing the simplicity is.

The no-customisation limitation is worth sitting with. You cannot adjust VDHG’s allocation. If you want more bonds, a different regional tilt, or to exclude specific sectors, you would need to build your own portfolio or add other funds around it. That is a genuine constraint, not a minor quibble, for investors with specific needs.

VDHG delivers global diversification, automatic rebalancing, and a growth-oriented allocation in one ASX trade for 0.27% per annum. That value proposition is straightforward and, for the right investor, genuinely powerful.

The limitations are equally straightforward: no customisation, full exposure to broad market downturns, and a fixed allocation that may not suit everyone.

VDHG is a strong candidate if you:

VDHG warrants reconsideration if you:

The question is not whether VDHG is a good fund in the abstract. It is whether its specific design, its fixed 90/10 allocation, its global scope, and its hands-off structure, matches the way you actually want to invest and the timeline you are genuinely working within.

Assess your time horizon and risk tolerance honestly. Consider consulting a licensed financial adviser for guidance specific to your circumstances. Vanguard Investments Australia Ltd (ABN 72 072 881 086 / AFS Licence 227263) is the product issuer, and you should refer to the product disclosure statement before investing.

Vanguard Australia’s product disclosure statements for diversified index ETFs, including VDHG, set out the fund’s investment objectives, fee structure, and underlying allocation in the detail required before making an investment decision.

This article is for informational purposes only and should not be considered financial advice. Past performance does not guarantee future results. Investors should conduct their own research and consult with financial professionals before making investment decisions.

VDHG is a fund-of-funds listed on the ASX that holds units in several underlying Vanguard index funds, giving investors a globally diversified portfolio with 90% growth assets and 10% defensive assets in a single trade for a 0.27% annual management fee.

VDHG allocates across Australian shares (36%), international shares both hedged and unhedged (42.5% combined), international small companies (6.5%), emerging markets shares (5%), international fixed interest (7%), and Australian fixed interest (3%).

Vanguard manages all rebalancing internally at the VDHG level, periodically restoring the portfolio to its target allocation as market movements cause drift, so investors never need to place rebalancing trades themselves.

VDHG is best suited for investors with a 7-plus year investment horizon who want broad global and domestic equity exposure, are comfortable holding through significant market drawdowns, and prefer a hands-off, automated portfolio approach.

VDHG offers no ability to customise the asset allocation, carries full exposure to broad equity market downturns through its 90% growth weighting, and is not appropriate for investors who need capital within a few years or require a more defensive portfolio.