Flight Centre just cut its profit guidance by as much as 13%, and its share price went up. For most retail investors, that sentence should not make sense. On 17 June 2026, the company trimmed its FY26 underlying profit before tax (PBT) guidance to A$275-295 million, down from A$310-345 million, citing roughly A$50 million in Q4 leisure disruption tied to Middle East travel volatility. The stock rose approximately 3.4% on the day and continued climbing through the following week. Understanding why that happened is not a trivia exercise. It goes to the core of how experienced investors read price action differently from headlines. By the end of this analysis, you will know how to identify when a downgrade is already “in the price,” what the Flight Centre share price rally signals about where the market thinks the revision cycle sits, and what questions to ask before you interpret similar moves in other ASX stocks.

The downgrade that landed softer than the market feared

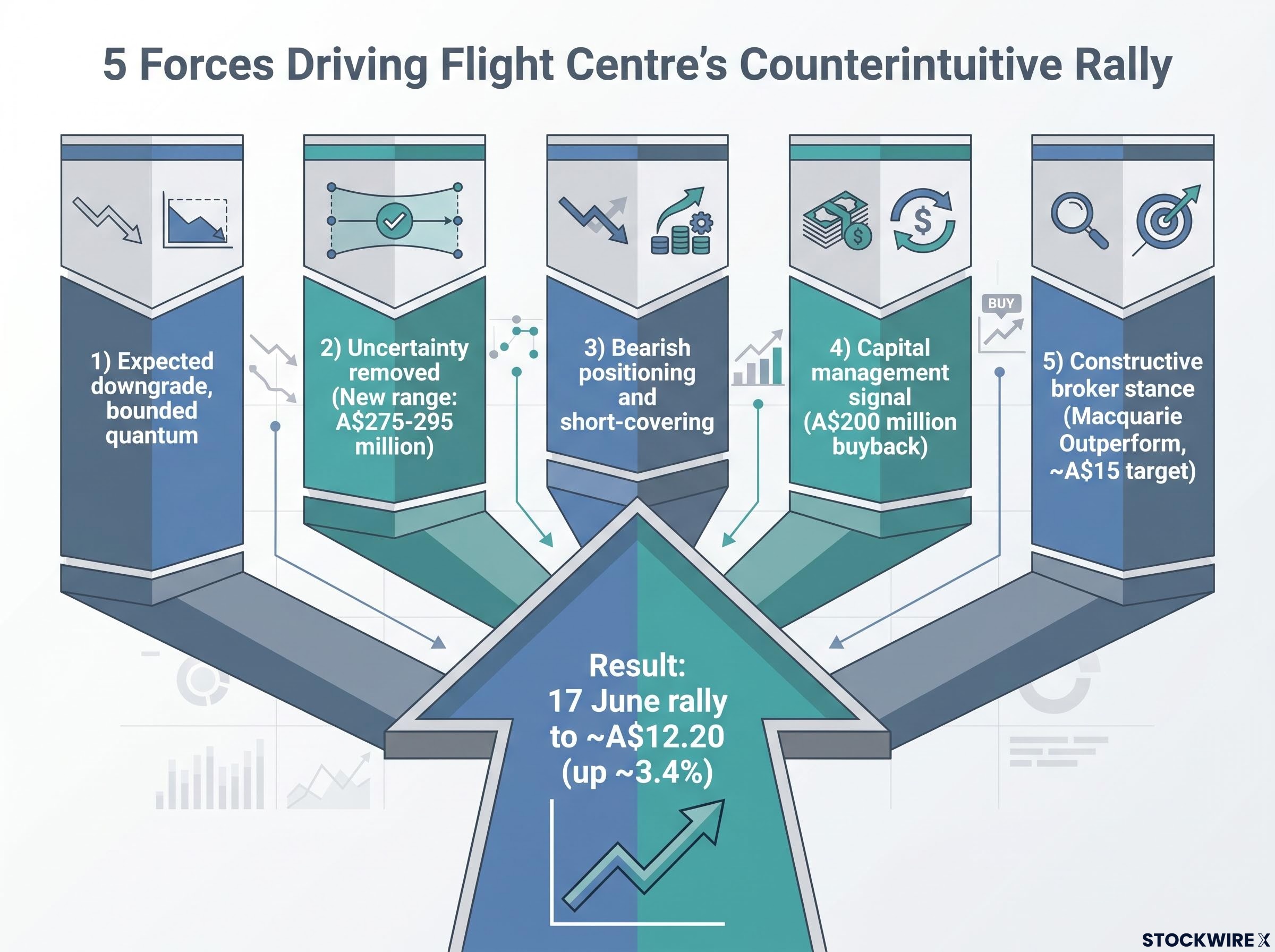

The numbers were unambiguously negative. Flight Centre lowered its FY26 underlying PBT guidance to A$275-295 million from a prior range of A$310-345 million, a cut of roughly 7-13% at the midpoint. Management attributed approximately A$50 million of the miss to Q4 leisure profit disruption from Middle East conflict.

| Item | Figure |

|---|---|

| New FY26 underlying PBT guidance | A$275-295 million |

| Prior FY26 underlying PBT guidance | A$310-345 million |

| Q4 leisure profit impact (Middle East disruption) | ~A$50 million |

| Buyback programme | A$200 million on-market |

| Announcement date | 17 June 2026 |

~A$50 million in Q4 leisure profit wiped out by Middle East travel disruption, including cancellations, reroutes, and deferred long-haul bookings.

Here is the detail the headline misses: brokers including Macquarie had already flagged to institutional clients that a downgrade was likely, even if the exact size was unknown. When the actual cut landed within the band investors had privately anticipated rather than below it, the announcement registered as relief. Simultaneously, the A$200 million on-market buyback reframed the announcement from a pure negative into a mixed signal. The gap between the prior guidance and the new range tells you the size of the known shock; the fact the market had already partially anticipated a cut tells you why that gap produced relief rather than panic.

The full details of Flight Centre’s FY26 guidance revision, including the breakdown of the Q4 leisure earnings impact by segment and the precise terms of the buyback programme, are set out in the announcement coverage published at the time of the June 2026 trading update.

When big ASX news breaks, our subscribers know first

Why a stock can rise on worse numbers

Five forces converged on the same day, and understanding them as a pattern is what separates an informed read from a confused one.

- Expected downgrade, bounded quantum. Brokers had warned clients a cut was coming. The actual number landed within the feared range rather than below it, triggering a “better than feared” relief trade.

- Uncertainty removed. For weeks, investors knew guidance had to fall but not by how much. The new A$275-295 million range converted an open-ended risk into a defined, bounded outcome. Markets reward that kind of risk clarification, even when the clarified number is lower.

- Bearish positioning and short-covering. (See below.)

- Capital management signal. The A$200 million buyback, announced alongside the cut, supports earnings per share and signals management’s confidence in longer-term value.

- Constructive broker stance. Macquarie maintained its Outperform rating with a price target of approximately A$15 or above, framing the revision as a speed bump in the post-pandemic travel recovery rather than evidence of a broken thesis.

Each force individually could produce a small positive reaction. When all five converged on 17 June, the resulting rally to around A$12.20 (up roughly 3.4%) was the market’s way of telling you that pessimism had become crowded and was now unwinding. The advance continued through at least 22 June 2026.

What short-covering means for retail investors

Short selling is the practice of borrowing shares and selling them in anticipation of a price fall, aiming to buy them back cheaper later. When news lands as “not bad enough,” short sellers must buy back shares to close their positions, and that forced buying adds upward price pressure independent of any new long investor enthusiasm. On a day when Flight Centre’s headline disappointed but the feared magnitude did not materialise, that forced buying was likely one ingredient in the 3.4% advance.

The ASX Guidance Note 8 on continuous disclosure sets out the conditions under which a listed company must immediately release market-sensitive information, including earnings guidance revisions, which is the regulatory framework that required Flight Centre to announce its FY26 PBT revision to the market on 17 June 2026.

Understanding “priced in”: the concept every ASX investor needs

A share price at any moment reflects the weighted average of all investor expectations, not just the most recently reported earnings number. Prices can fall before bad news is announced and rise when bad news merely confirms, rather than worsens, those fears.

Two scenarios produce very different outcomes:

- Structural impairment: The business model itself is damaged. Revenue sources are permanently reduced. Competitive position has deteriorated. The stock re-rates lower and stays there.

- Event-driven trough: A temporary external shock (conflict, weather, a single-quarter disruption) depresses earnings for a defined period. The business model remains intact, and earnings recover once the shock passes.

The market’s job is to figure out which scenario it is dealing with, and the price tells you its current verdict. Broker commentary framed the guidance revision as a “speed bump” in a broader post-pandemic normalisation, not a structural break.

Applying the framework to Flight Centre’s specific situation

Three features of the current downgrade support the event-driven interpretation: the disruption is conflict-related travel volatility (external, not operational), FY27 carries a potential normalisation tailwind if Middle East headwinds ease, and the corporate travel division remains unimpaired. If the market is right that this is a temporary trough rather than structural damage, the current share price is offering you exposure to a recovery that the earnings number alone would cause you to miss. The test will be subsequent trading updates confirming whether this was a one-off shock or the start of a persistent earnings squeeze.

The corporate travel division trajectory heading into FY26 Q4 was notably strong, with 23% UPBT growth on only 4% TTV growth recorded across the nine months to March 2026, meaning the guidance cut reflects a leisure-specific shock layered onto an otherwise accelerating business.

What the buyback signals about management’s own read

An on-market buyback, unlike a fixed-price tender, provides flexible and ongoing demand for the stock through normal market purchases. That ongoing bid is meaningful when the broader market is uncertain.

The pairing matters more than either announcement alone. A management team that cuts guidance and launches a A$200 million buyback simultaneously is making a statement with financial commitment, not just words.

A guidance cut paired with a buyback tells the market that management believes the share price decline into the announcement had already overshot the underlying damage to the business.

The buyback delivers three effects for remaining shareholders:

- Ongoing demand: Steady purchasing supports the share price through volatile periods.

- EPS accretion: Buying back shares at the current price raises earnings per share even if absolute earnings have been trimmed.

- Management credibility signal: Committing capital to a buyback carries more weight than verbal reassurance about the outlook.

That combination typically attracts value-oriented buyers even against a softer near-term earnings picture, and it is one of the cleaner management signals available to retail investors.

FLT share price valuation at the time of the guidance cut was already sitting near multi-year lows on a price-to-sales basis, approximately 77% below the five-year historical average of 3.42x, which helps explain why the buyback announcement landed with such credibility among value-oriented buyers.

Flight Centre versus Webjet: reading where each stock sits in the expectations cycle

The “priced in” dynamic is not universal across the travel sector. Webjet (ASX: WJL), as of late May 2026, looked optically cheap on standard valuation metrics. But analysts, including Market Index’s Kerry Sun writing on approximately 21 May 2026, flagged that adverse news flow may not have fully concluded. That places Webjet at an earlier, less resolved point in the expectations cycle.

| Criterion | Flight Centre (ASX: FLT) | Webjet (ASX: WJL) |

|---|---|---|

| Recent guidance direction | Downgraded FY26 PBT to A$275-295M | No comparable update at research date |

| Market reaction to news | Rallied ~3.4% on downgrade | No equivalent “tell” observed |

| Analyst risk flags | Constructive; Macquarie Outperform maintained | Analysts still flagging risk of further adverse news |

| Expectations cycle stage | Pessimism appears crowded; reset likely absorbed | Earlier stage; bad news may not be fully priced |

A downgrade that makes a stock fall often means expectations were still too high. A downgrade that makes a stock rise usually means expectations had already been cut by the market, and the formal guidance update has finally caught up with what investors assumed.

Webjet’s relative cheapness versus Flight Centre’s post-downgrade rally illustrates that valuation metrics and expectation-cycle positioning are two separate questions. Confusing them is a common source of timing errors for retail investors.

What Flight Centre needs to prove from here

The rally is a hypothesis, not a verdict. The current share price embeds the assumption that the Middle East disruption was a one-off shock and that FY27 will benefit from normalisation. Macquarie’s Outperform rating and price target of approximately A$15 or above provides the upside reference point for that thesis.

Two scenarios will determine whether today’s buyers paid a fair price:

- Travel demand recovers, Middle East headwinds ease, and FY27 earnings confirm the event-driven interpretation.

- Further earnings pressure emerges, suggesting the disruption is persistent or that other structural headwinds have appeared.

The announcement on 17 June came roughly two weeks before the 30 June FY26 year-end, making the full-year results and FY27 guidance the next decision points. Watch for:

- FY27 guidance range issued alongside the full-year results

- Middle East travel demand normalisation data in the Q1 FY27 trading update

- Corporate travel division trends confirming the non-leisure business remains intact

The FY27 guidance will be the most important data point for determining whether today’s buyers paid a fair price or bought into a false bottom.

For investors wanting to place Flight Centre’s revision cycle within the broader earnings pressure facing the ASX consumer discretionary sector, our full explainer on consumer discretionary sector dynamics covers the interest-rate transmission mechanism, RBA timing expectations, and why sector recovery depends on actual rate cuts rather than a pause, with FLT used as a worked example of valuation compression.

The rally is a signal, not a verdict: how to use it

Share prices move on the gap between expectations and outcomes, not on whether outcomes are good or bad in absolute terms. Flight Centre’s post-downgrade rally is a live illustration of that principle. The same framework applies whenever you encounter a stock that moves counterintuitively on news, whether in the travel sector or elsewhere on the ASX. Ask what the market had already priced in, where the positioning sat, and whether the news bounded or expanded uncertainty. The key unresolved question remains: the rally prices in recovery, and the FY27 results will be the first real evidence of whether the market’s hypothesis was correct.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.