Gold Bounces 0.8%, but the Fed and Dollar Hold the Ceiling

1 hr ago

The largest initial public offering in history debuted on Nasdaq ten days ago, raised approximately USD 75 billion in a single session, and is already trading well above its offer price. For Australian investors watching the ticker from the other side of the Pacific, the question is not whether SpaceX has built something extraordinary. It is whether the excitement surrounding the SpaceX IPO is a reason to buy or a reason to pause.

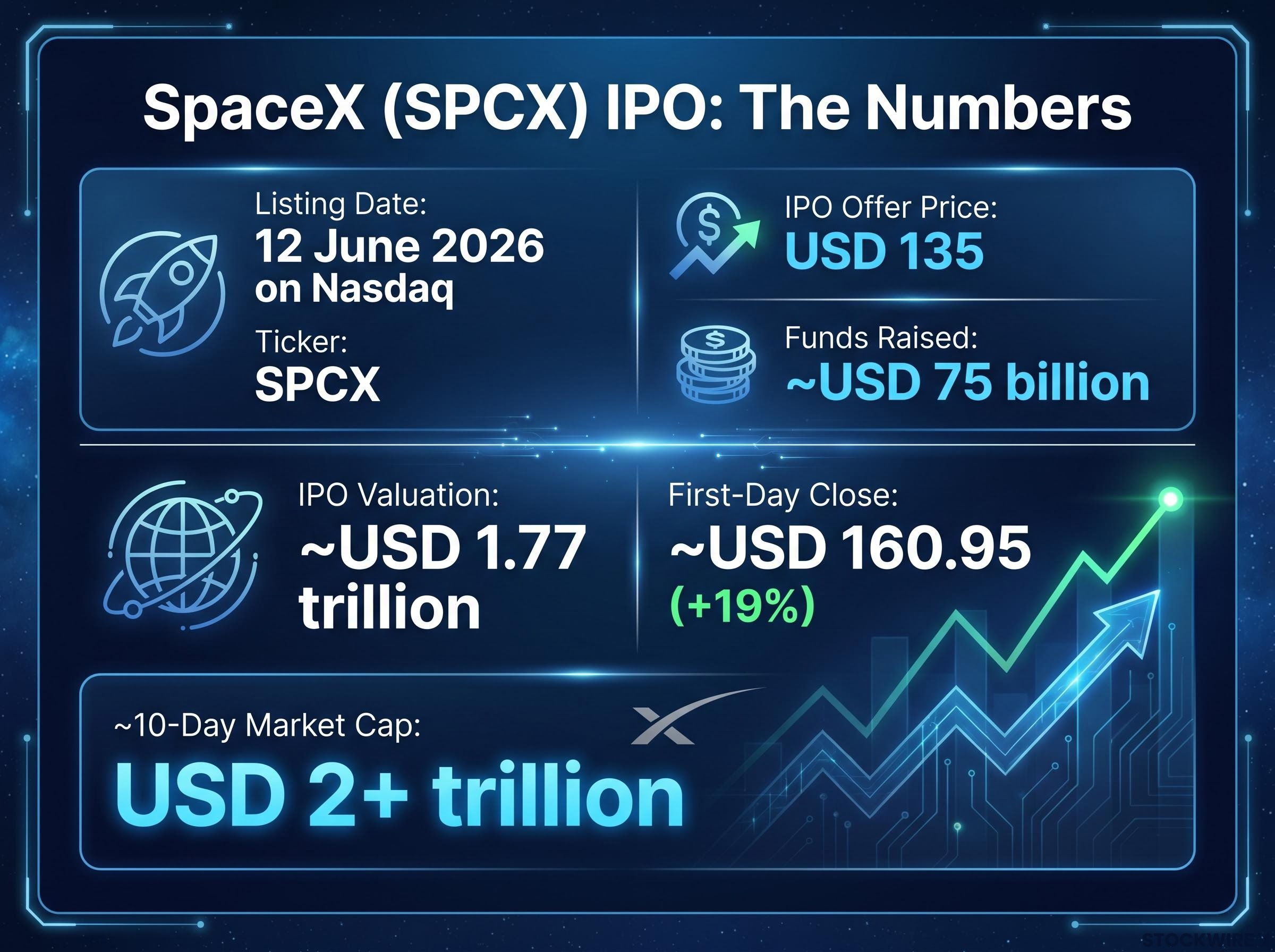

SPCX began trading on 12 June 2026 and has attracted enormous retail attention in Australia, with platforms including nabtrade publishing dedicated FAQ resources to handle investor enquiries. A first-day gain of roughly 19%, a market capitalisation already past USD 2 trillion, and wall-to-wall media coverage mean this is not a typical listing. The price already reflects extraordinary expectations. What follows works through what Australian investors actually need to know before placing an order: how to access the stock, what the valuation implies, how it fits in a portfolio, and why the rush to buy deserves scrutiny.

On 12 June 2026, SpaceX began trading on Nasdaq under the ticker SPCX at an offer price of USD 135 per share, implying a valuation of approximately USD 1.77 trillion. The listing raised approximately USD 75 billion, making it the largest IPO in history by both proceeds and market value at debut.

| Metric | Figure |

|---|---|

| Listing date | 12 June 2026, Nasdaq |

| Ticker | SPCX |

| IPO offer price | USD 135 per share |

| IPO valuation | ~USD 1.77 trillion |

| Funds raised | ~USD 75 billion |

| First-day open | ~USD 150 |

| First-day close | ~USD 160.95 (+19%) |

| ~10-day market cap | USD 2+ trillion |

A 19% first-day gain on a USD 1.77 trillion listing. That figure is not just a headline; it is a measure of how much optimism was already priced in before a single quarterly earnings report as a public company.

The record scale matters, but so does its implication. Investors buying SPCX today are not acquiring an overlooked or undervalued asset. They are paying a consensus premium for a widely anticipated story, and the distinction between “historic achievement” and “attractive entry price” is where careful analysis begins.

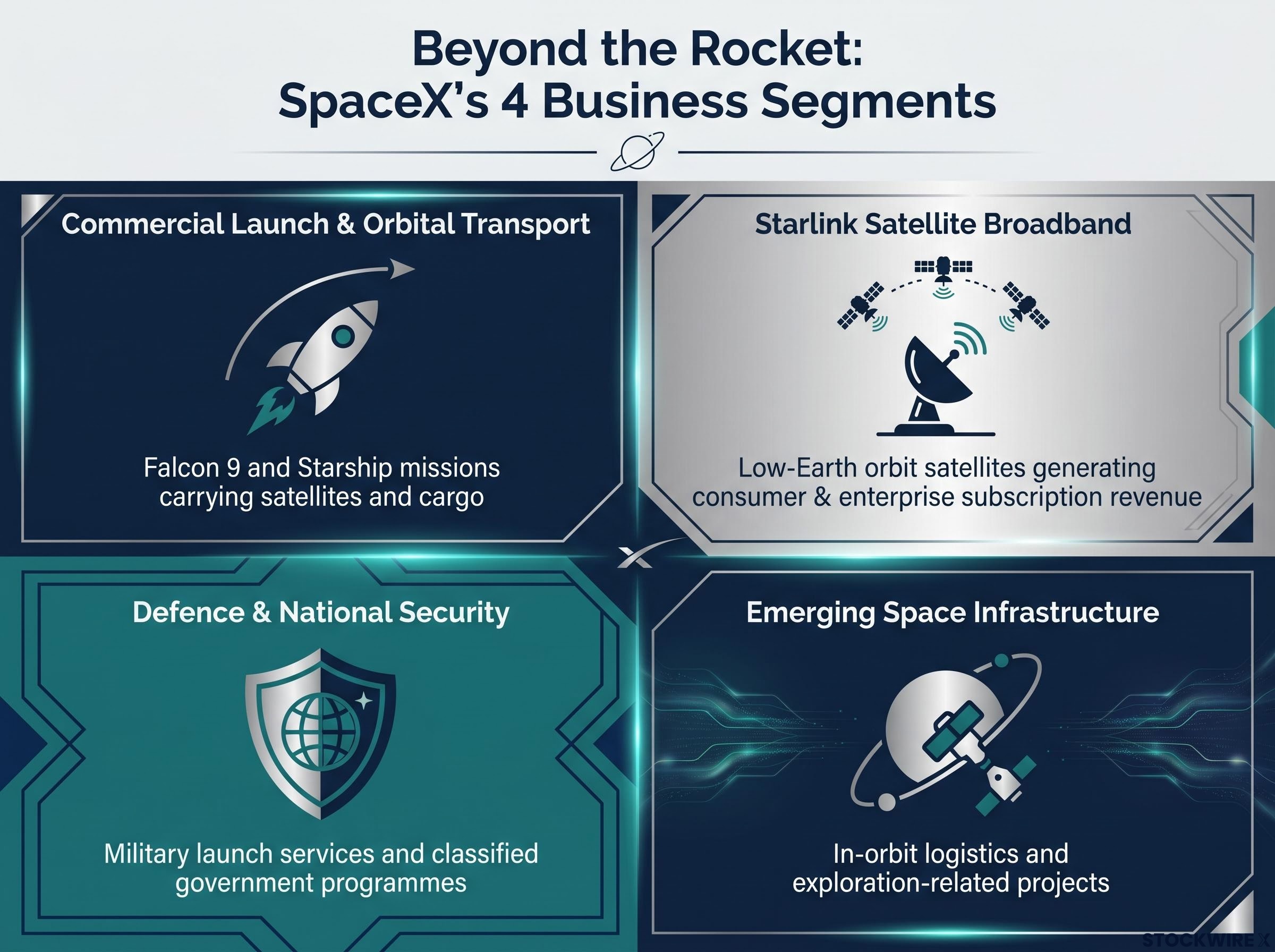

Most retail investors arrive at SPCX with a mental model built from rocket launch footage. The actual business is considerably broader, and the part that matters most to the valuation is not the part most people picture.

SpaceX operates across four distinct segments:

Starlink is the segment that drives the bulk of the valuation thesis. Unlike the launch business, which earns project-based revenue tied to individual missions, Starlink generates recurring subscription income from a growing global customer base. Understanding this distinction is not optional for anyone considering SPCX; the investment thesis hinges far more on satellite broadband adoption curves than on rocket cadence.

Starlink’s two-franchise model separates a direct-to-consumer rural broadband business with high retention and limited terrestrial competition from a wholesale direct-to-cell infrastructure play distributed through mobile carriers, a structural distinction that matters when assessing how durable the recurring revenue base actually is.

SPCX does not sit cleanly in any established sector category. It is not a pure technology stock, a traditional defence contractor, or a simple telecommunications provider. That makes benchmarking genuinely difficult, even for professional analysts. Equity research and market commentary have characterised the IPO price as effectively “pre-paying” several years of expected Starlink-led growth, and the limited public financial track record relative to other companies valued at USD 1.77 trillion at listing makes independent verification harder still.

For ASX-weighted portfolios, this multi-sector profile may offer genuinely distinct exposure. That distinctiveness, however, cuts both ways: there is no ready-made peer group to anchor expectations, and no established playbook for how SPCX should trade relative to existing holdings.

SpaceX is not listed on the ASX. Australian investors access SPCX the same way they would buy any US-listed stock, but each step in the process carries a cost or friction point worth understanding before placing an order.

The W-8BEN completion requirements for Australian investors in US-listed securities invoke the Australia-US Double Taxation Agreement to reduce the default 30% withholding rate, but the form must be correctly submitted and kept current with the broker to ensure the reduced rate actually applies.

nabtrade published a dedicated SpaceX FAQ resource covering key considerations for the listing. Commentary from Gemma Dale, Director of SMSF and Investor Behaviour at nabtrade, and Glen James of the money money money podcast framed the IPO as a moment requiring investor discipline, not just enthusiasm. Checking platform-level guidance before entering a first order in SPCX is strongly recommended.

The first-day premium and the subsequent trading trajectory mean that anyone buying SPCX today is not purchasing at the USD 135 offer price. They are buying into a price that already reflects considerable enthusiasm, with the market capitalisation exceeding USD 2 trillion roughly ten days after listing, up from the USD 1.77 trillion IPO valuation.

Even a company with extraordinary technology and a powerful brand can be a poor investment at the wrong price. Equity research has characterised the listing price as pre-paying for several years of Starlink-led growth, and every dollar above that price compounds the execution burden required to justify the investment.

The SpaceX IPO valuation carries an internal tension that is easy to miss in headline coverage: SpaceX posted a $4.28 billion net loss on $4.69 billion in Q1 2026 revenue, which means the company lost approximately $0.91 for every dollar earned in its most recently reported quarter, a data point that sits uncomfortably alongside a market capitalisation now past $2 trillion.

The months ahead will introduce additional dynamics that can drive sharp price moves unrelated to underlying business performance:

A generally strong global equity environment may also be contributing to early SPCX strength independent of company-specific assessment, a distinction worth bearing in mind when evaluating post-IPO price action.

Three considerations apply specifically to Australian holders. First, AUD/USD currency exposure: SPCX returns in Australian dollars depend on both the share price and the exchange rate. A strengthening Australian dollar can offset USD-denominated gains, while a weaker AUD can magnify them.

Second, US withholding tax treatment: eligible income is typically subject to US withholding tax, moderated by the Australia-US tax treaty and completion of the W-8BEN form. The treaty does not eliminate the obligation; it reduces the rate.

US withholding tax treatment for Australian investors is governed by the Australia-US tax treaty, which reduces the default 30% withholding rate on eligible income, but the treaty reduction requires active steps, including completing and submitting the W-8BEN form, to take effect at the broker level.

Third, unintended portfolio concentration: investors already holding US tech, defence, or satellite-communications exposure through global ETFs or individual holdings may find that adding SPCX increases correlation to those themes more than expected. Mapping existing exposures before sizing a position is a practical step that is easy to skip in the excitement of a landmark listing.

This checklist is not a buying framework. It is a slowing-down mechanism. Answering these questions honestly might lead to a smaller position, a delayed entry, or no position at all, and all three outcomes can be the right one.

For investors attracted to SPCX but uncertain how much of their portfolio it should represent, the core-and-satellite framework offers a structured starting point: a broad index ETF foundation capturing diversified market returns, with a capped satellite allocation reserved for high-conviction single-stock positions like SPCX.

Space infrastructure plays out over years, not quarters. If the time horizon does not match, the thesis does not hold.

Investors who can answer all five questions clearly before buying are in a fundamentally stronger position than those reacting to the listing’s headline dominance alone.

The investment case for SpaceX is legitimate. The company has reshaped the global launch market, driven down the cost of orbital access, and built Starlink into a meaningful, revenue-generating satellite broadband business, not a speculative future project. Access to that business as a public equity is genuinely new, and for Australian portfolios it offers exposure that is difficult to replicate through existing ASX or global ETF holdings.

The price, however, already reflects a great deal of that story. USD 75 billion raised, a market capitalisation past USD 2 trillion within ten days, and a strong global equity environment contributing to early momentum all suggest that a significant portion of the optimism is already embedded. The post-IPO period introduces additional volatility dynamics, from lock-up expiries to potential index inclusion, that can move the price sharply in either direction for reasons unrelated to business fundamentals.

For most retail investors, the practical orientation is straightforward:

Gradual entry, through staggered purchases over time, tends to serve investors better than a single large trade at an arbitrary early post-IPO price. The opportunity is not going away. The urgency is mostly narrative.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and forward-looking statements regarding SpaceX’s business trajectory and market performance are subject to change based on market developments and company execution.

The SpaceX IPO is the public listing of SpaceX on Nasdaq under the ticker SPCX, which began trading on 12 June 2026 at an offer price of USD 135 per share, raising approximately USD 75 billion and making it the largest IPO in history by both proceeds and market value at debut.

Australian investors can buy SPCX through brokers that offer US market access, including nabtrade, Superhero, Stake, Moomoo, Interactive Brokers, and CommSec International; investors must also complete a W-8BEN tax form and account for AUD-to-USD conversion costs before placing an order.

The W-8BEN is a US tax form that Australian investors must submit to their broker when trading US-listed shares; it activates the Australia-US Double Taxation Agreement, which reduces the default 30% US withholding tax rate on eligible income to a lower rate under the treaty.

Key risks include buying into a market capitalisation already past USD 2 trillion reflecting significant optimism, AUD/USD currency exposure that can erode USD-denominated gains, US withholding tax obligations, potential price volatility from lock-up expiries and index inclusion events, and unintended portfolio concentration in US tech or defence themes.

SpaceX reported a net loss of USD 4.28 billion on USD 4.69 billion in Q1 2026 revenue, meaning the company lost approximately USD 0.91 for every dollar earned in its most recently reported quarter, a figure that sits in contrast to its post-IPO market capitalisation of over USD 2 trillion.