Why AI Makes Markets Safer Daily but Riskier in a Crisis

32 mins ago

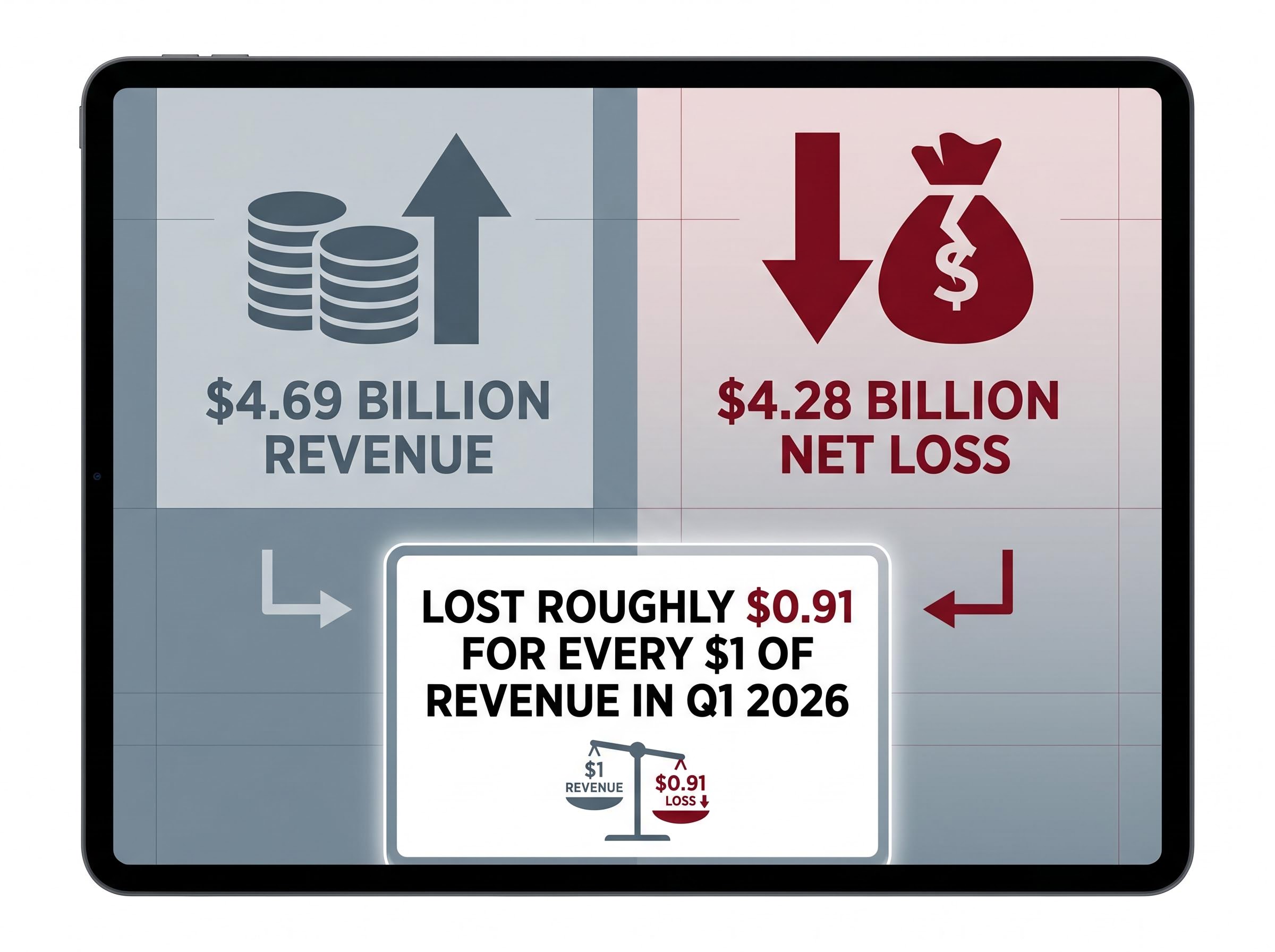

SpaceX disclosed a Q1 net loss of $4.28 billion on $4.69 billion in revenue, and is simultaneously being discussed as a $2 trillion IPO candidate. That gap is not a reporting error. It is the entire investment question for anyone considering participation when the company lists, widely expected as early as June 2026.

The confidential IPO filing has been submitted. The $1.75 trillion to $2 trillion valuation range circulating in analyst commentary and financial media exceeds the peak market capitalisations of Amazon, Berkshire Hathaway, and Nvidia at various points in their histories. Yet the company’s most recent quarterly financials show it lost roughly ninety-one cents on every dollar of revenue it generated.

What follows is a segment-by-segment breakdown of what SpaceX actually earns today, what assumptions the $2 trillion premium requires investors to accept, and where the specific execution and governance risks sit underneath the narrative. The goal is not a verdict. It is a framework for evaluating whether the price makes sense within any individual portfolio.

The Q1 2026 financials are a single data point. They are also the only recent data point available from the confidential filing, as reported in the CNBC segment posted 12 May 2026. And they reframe everything.

SpaceX generated $4.69 billion in quarterly revenue and posted a $4.28 billion net loss in the same period. The implied annualised revenue run-rate sits at approximately $18-19 billion.

SpaceX lost roughly $0.91 for every dollar of revenue it generated in Q1 2026.

The $1.75 trillion valuation figure was first reported on 27 March 2026, with Bloomberg and CNBC as the underlying sources, as summarised by Satellite Today on 1 April 2026. The upper-range figure of “as much as $2 trillion” comes from analyst and commentator framing in the CNBC segment, not from a locked figure in a public S-1 document. No such document has been filed publicly as of late May 2026, meaning the full financials behind the IPO remain unavailable for independent analysis.

Every number that follows in this article is an attempt to answer the question that ratio poses: what, precisely, justifies pricing a loss-making business at $2 trillion?

The SpaceX IPO filing, published on 20 May 2026, added important precision to the revenue picture: full-year revenue of $18.67 billion, a confirmed $1.94 billion operating loss in Q1 2026, and a disclosure that Starlink accounted for approximately 69% of quarterly revenue, with an AI segment contributing $818 million and signalling where management expects the revenue mix to shift.

No officially segmented profit-and-loss statement has been made publicly available through the IPO filing process. The figures below draw on 2025 full-year estimates reported across financial coverage and analyst commentary to illustrate how the business breaks down.

| Segment | 2025 Revenue (Est.) | EBITDA / Operating Income (Est.) | Cash Flow Status |

|---|---|---|---|

| Connectivity (Starlink) | ~$11.4 billion | ~$7B EBITDA / ~$4B operating income | Positive operating cash flow |

| Launch Services | ~$4 billion | ~$600M EBITDA | Positive but modest |

| AI Infrastructure | Not separately disclosed | Not separately disclosed | Cash-flow negative, capital-intensive |

Starlink is the segment carrying the business. With an estimated 10.3 million subscribers across 164 countries and roughly 50% year-on-year revenue growth in 2025, it is the only division generating meaningful positive operating cash flow. Launch services contribute revenue and modest EBITDA, but the margins are narrow relative to the connectivity business. AI infrastructure, following the February 2026 xAI acquisition, remains capital-intensive and cash-flow negative.

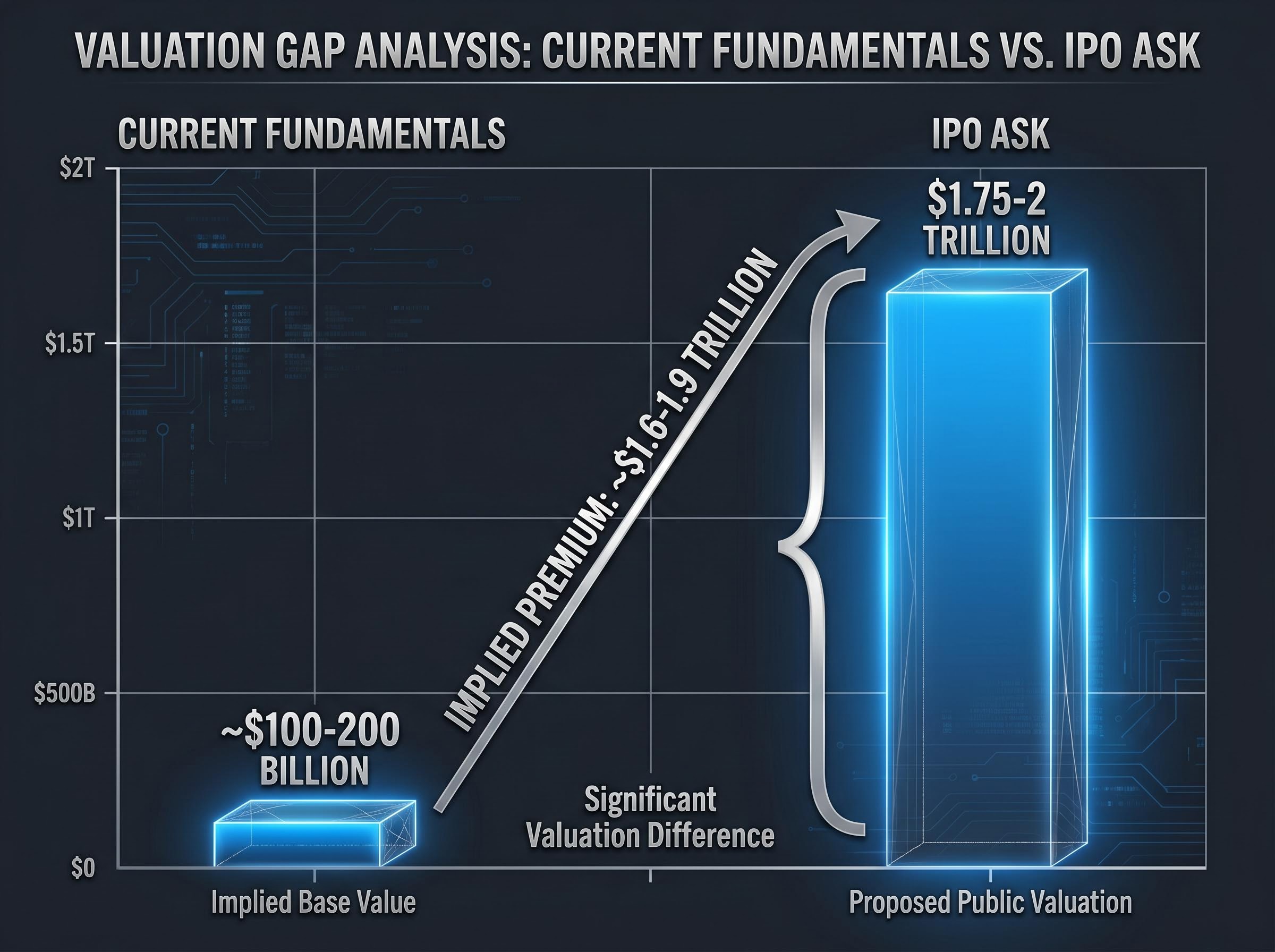

Applying a 40x multiple to an estimated $5 billion in connectivity operating profit produces a segment valuation of approximately $200 billion for Starlink alone. Adding launch services and early-stage AI infrastructure at generous multiples brings the range of analyst-estimated fundamental value to roughly $100-200 billion based on current operations.

That means approximately $1.8 trillion of the anticipated IPO valuation is not a reflection of current earnings. It is a premium on future execution across segments that are either modestly profitable or not yet generating revenue. The rest of this article examines what that premium demands.

The EBITDA multiple at the IPO valuation sits at approximately 250x on reported figures, a level that multiple analyst assessments have flagged as pricing in decades of future growth rather than current operational performance, with roughly 30% overvaluation risk cited in independent commentary.

Starlink operates a subscriber-based broadband service delivered through a constellation of low-Earth orbit (LEO) satellites, meaning satellites positioned close enough to Earth (roughly 550 kilometres altitude) to deliver low-latency internet comparable to ground-based connections. Subscribers pay a recurring monthly fee for access. The economics work like most infrastructure-heavy subscription businesses: upfront capital costs are enormous, but each additional subscriber added to the existing network improves unit margins because the satellites are already in orbit.

The network currently serves subscribers across 164 countries with a mission success rate exceeding 99% across hundreds of Falcon 9 launches. Management estimates the combined addressable market for broadband and mobile connectivity at approximately $1.6 trillion. Long-term analyst projections for the connectivity segment range from $50 billion to $100 billion in revenue potential, with operating profits potentially reaching $50 billion at the upper end of that range.

Independent LEO satellite broadband market projections from Roots Analysis forecast sector growth from $13.53 billion in 2025 to $66.54 billion by 2035 at a 17% compound annual rate, providing an external benchmark against which management’s $1.6 trillion combined addressable market estimate can be assessed.

“A single Starship V3 launch could deliver roughly 20 times the downlink capacity of a current Falcon 9 mission.”

Starship V3 is anticipated to become operational in the second half of 2026, which would enable the mass deployment of Starlink V3 satellites at a pace and per-unit cost that the current Falcon 9 platform cannot match. The capacity improvement is not incremental; it represents a step-change in the economics of constellation build-out.

This remains a development programme, not a confirmed operational cadence. The entire scaling story for Starlink V3, and by extension the upper-range revenue projections that underpin the IPO valuation, depends on a rocket that is still being iteratively tested as of late May 2026. Competitive pressure from Amazon’s Project Kuiper, which plans a constellation of thousands of LEO satellites with substantial capital backing, adds a structural dimension to the broadband market that did not exist when earlier Starlink projections were formed.

The gap between the estimated $100-200 billion fundamental value and the $2 trillion IPO ask is not empty. It is filled with three specific growth bets, each requiring distinct execution milestones that have not yet been reached.

Management estimates approximately $29 trillion in addressable markets across all segments. Current company-wide revenue runs at roughly $18-19 billion annualised.

| Growth Bet | Current Status | Key Execution Dependency |

|---|---|---|

| Orbital Data Centres | xAI acquired Feb 2026; Colossus facilities at ~1 GW combined capacity; long-term target up to 100 GW/year | Operational Starship V3, viable orbital hardware deployment, enterprise customer contracts |

| Enterprise AI Platform | Grok platform processing ~10B image and ~2B video inputs/month; no disclosed enterprise revenue | Commercial platform launch, competitive positioning against established cloud providers |

| Direct-to-Device | Technology in development; no large-scale commercial deployment | Multi-jurisdiction regulatory approval, carrier partnerships |

One data point requires explicit flagging. Source materials reference a $1.2 billion per month Anthropic data centre agreement with SpaceX. This figure has not been independently confirmed in any named outlet, including Bloomberg, Reuters, the Wall Street Journal, the Financial Times, or CNBC, through late May 2026. Investors should treat it as unverified.

For investors wanting to model the hardware dependencies behind the orbital data centre thesis, our deep-dive into SpaceX’s orbital compute roadmap covers the $20 billion Terafab project, Intel’s role as foundry partner, the $7.7 billion AI capex figure from Q1 2026, and Wolfe Research’s assessment of the launch cadence required to reach 100 gigawatts of orbital capacity by 2028.

The upside story requires multiple simultaneous wins. The downside requires only one significant miss, and at a $2 trillion starting price, the compression on any single failure is amplified.

“Super-voting shares mean retail investors buying the SpaceX IPO are buying economic exposure, not a seat at the table.”

The super-voting structure is not unusual for founder-led technology companies, but its practical implication is worth stating plainly: public shareholders will have no ability to influence strategic direction, capital allocation, or executive decisions. Combined with the confidential filing structure, which means no public S-1 risk factors section is available for review before IPO pricing, retail investors face an information and governance asymmetry that is structurally different from most large-cap IPOs.

The arithmetic is straightforward. Current operations support a valuation of approximately $100-200 billion. The IPO ask sits at $1.75-2 trillion. The implied premium for future optionality is approximately $1.6-1.9 trillion.

| Valuation Scenario | What It Assumes | Horizon Required | Risk Profile |

|---|---|---|---|

| Current Fundamentals (~$100-200B) | Starlink grows steadily; launch services stable; no AI revenue materialises | 1-3 years | Moderate |

| Starlink Scales to Upper Projection (~$500B-1T) | Connectivity revenue reaches $50-100B; operating margins expand significantly | 5-10 years | Moderate-to-high |

| AI + Enterprise Fully Execute (~$2T+) | Orbital compute, enterprise AI, and direct-to-device all reach commercial scale | 10-20+ years | High; requires all segments to execute |

Baron Capital holds an estimated $15 billion position in SpaceX, and founder Ron Baron has indicated intent to add approximately $1 billion at the IPO. Baron’s long-term thesis envisions a $10-30 trillion valuation over a multi-decade horizon, a legitimate bull case, but one that requires every major segment to execute at scale over a timeframe that extends well beyond most retail investment horizons.

Before committing capital, three questions merit clear personal answers:

Retail investors who cannot secure IPO-price allocation, which is expected to be dominated by institutional accounts, have access to publicly traded space stocks including Rocket Lab, Intuitive Machines, and AST SpaceMobile through any major brokerage today, with no lockup periods or accreditation requirements and meaningful year-to-date performance on record.

The business SpaceX operates today, a profitable satellite broadband network and a reliable launch services provider, supports a valuation that is a fraction of the IPO price under discussion. The remaining $1.8 trillion is priced-in optionality on orbital compute, an enterprise AI platform, and a rocket that is still being tested.

Optionality premiums can be rational for companies with genuine scale advantages and competitive moats. SpaceX possesses both. But “rational” and “safe” are not interchangeable terms at $2 trillion, and the Q1 loss-to-revenue ratio is a reminder that the current business is still investing heavily against a future that has not yet arrived.

Current operations support approximately $100-200 billion in valuation. The IPO ask is $1.75-2 trillion. The gap is the investment decision.

The public S-1 filing, when it becomes available, will be the first opportunity for retail investors to review full risk factor disclosures and segment-level financials on their own terms. Until that document is published, every valuation figure in the market narrative, including the ones cited in this article, carries the limitation of incomplete information. Historical pre-2025 analyst valuations from the Morgan Stanley era placed SpaceX at $150-300 billion. The distance from there to $2 trillion is measurable; whether it is justified remains an open question each investor must answer individually.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections referenced are subject to market conditions and various risk factors. Forward-looking statements regarding SpaceX’s growth segments, addressable markets, and technology timelines are speculative and subject to change based on market developments and company performance.

—

SpaceX is targeting a valuation of $1.75 trillion to $2 trillion, with the IPO widely expected as early as June 2026 following a confidential filing submitted to regulators.

SpaceX reported a net loss of $4.28 billion on $4.69 billion in revenue in Q1 2026, meaning the company lost roughly $0.91 for every dollar of revenue it generated in that quarter.

Starlink, SpaceX's satellite broadband connectivity business, accounts for approximately 69% of quarterly revenue and is the only segment generating meaningful positive operating cash flow, with an estimated 10.3 million subscribers across 164 countries.

Key risks include a super-voting share structure that gives Elon Musk full strategic control regardless of public shareholder composition, a confidential filing with no public S-1 risk disclosures available, dependence on an unproven Starship V3 rocket, and a valuation that prices in decades of future growth across segments not yet generating revenue.

Analyst estimates place SpaceX's fundamental value based on current operations at approximately $100 billion to $200 billion, meaning roughly $1.8 trillion of the $2 trillion IPO ask represents a premium on future execution across orbital compute, enterprise AI, and direct-to-device connectivity segments.