HYLD ETF: Monthly ASX Income Above 4% With Real Trade-Offs

3 hrs ago

Wesfarmers dropped to approximately A$71 in May 2026 and recovered to A$85 within weeks. Macquarie Group posted a 30% jump in full-year profit to A$4.847 billion. Both stocks now sit at or near record levels, and the question facing Australian investors is not whether these are quality businesses. It is whether they are quality buys at these prices.

Mid-2026 has delivered a sharp convergence of positive catalysts. Wesfarmers completed a strategy day that reaffirmed its AI integration ambitions and format expansion plans, while Macquarie’s FY26 result confirmed a cyclical acceleration that few predicted in magnitude. The market has repriced both stocks accordingly, and new investors face the full weight of those expectations in the entry price.

What follows is an examination of the earnings drivers, valuation realities, and entry approaches for each company, followed by a comparison of their roles in a portfolio. The aim is to give investors a clearer picture of what they are actually buying at current prices, and how to approach each stock with discipline rather than enthusiasm alone.

The May 2026 selloff took Wesfarmers to approximately A$70-72, with closes around A$71-75 during the week of 18 May. By mid-June, the shares had recovered to approximately A$85, putting them back near record territory.

That kind of move, a 10-15% drawdown followed by a swift recovery, is not unusual for this stock. Wesfarmers has a historical pattern of attracting long-term capital during pullbacks of that magnitude, and the May episode followed the same script. The correction did not reflect a structural break in the business. It reflected a temporary repricing that quality-focused investors treated as a buying opportunity.

Wesfarmers fell to approximately A$70-72 in May 2026 and recovered to approximately A$85 by mid-June, a move that validated the May selloff as a correction rather than a structural break.

What matters for investors at current prices is the nature of the catalyst behind the recovery. The rebound was not simply a broad market squeeze.

Management’s strategy day served as the specific catalyst for renewed investor interest. By reaffirming Wesfarmers’ AI integration plans and format expansion direction, the company communicated a clear medium-term investment thesis that gave the market fresh reason to reprice forward expectations.

For a stock commanding a premium multiple, that kind of management communication is itself a valuation input. It signals that the premium is backed by specific, articulated growth plans rather than backward-looking momentum alone. Investors evaluating Wesfarmers at A$85 need to understand that this price embeds those forward expectations, and the May pullback showed what happens when sentiment briefly disconnects from them.

The ASX continuous disclosure obligations under Listing Rule 3.1 require companies to immediately notify the exchange of any information that a reasonable person would expect to have a material effect on price, which is why strategy day announcements and earnings results from companies like Wesfarmers and Macquarie carry formal disclosure weight beyond their investor relations function.

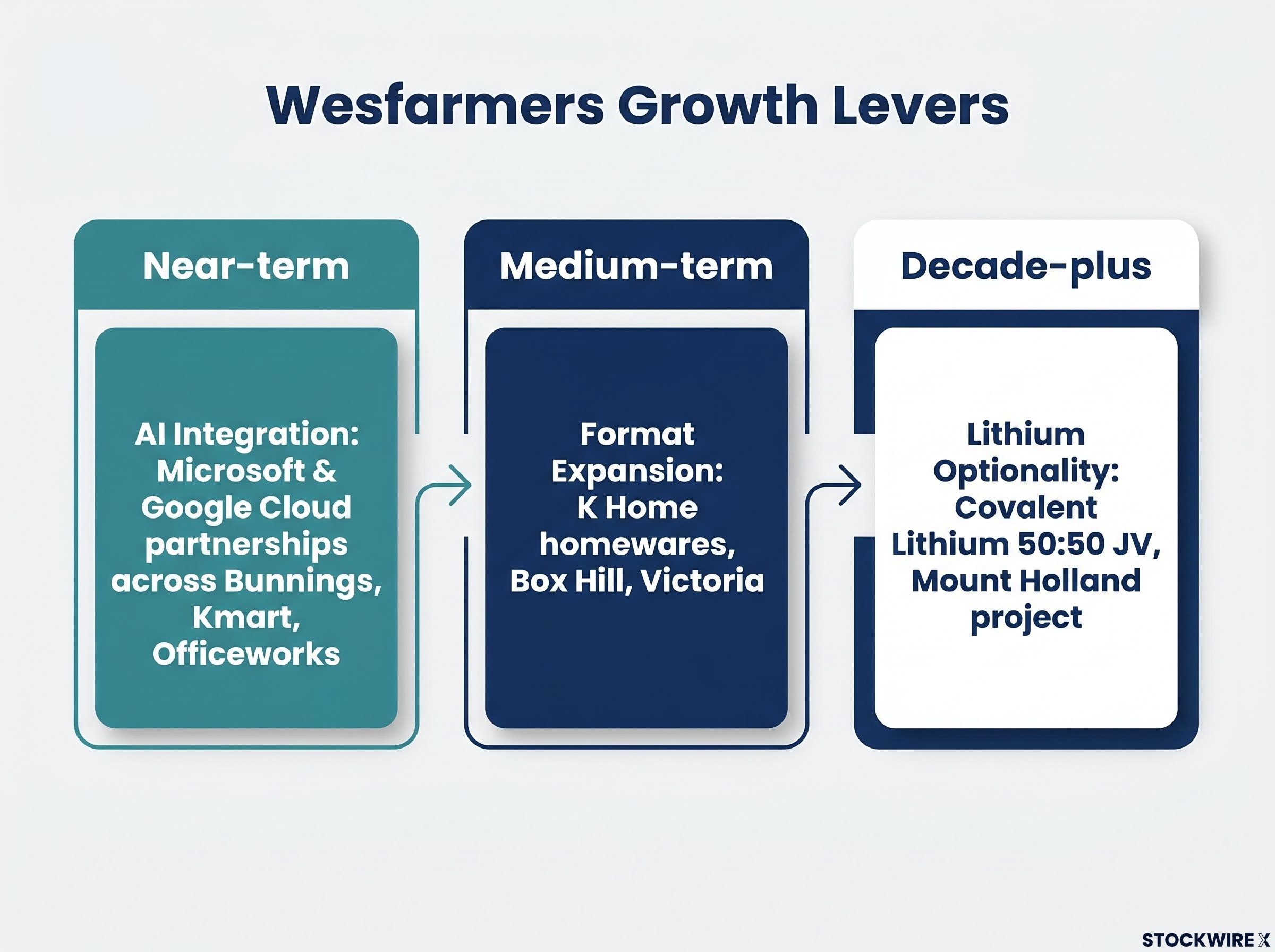

Three growth levers sit inside Wesfarmers, and they operate on fundamentally different time horizons. Conflating them produces a distorted valuation picture. Separating them is the prerequisite for calibrating return expectations at current prices.

In February 2026, Wesfarmers announced multi-year strategic partnerships with both Microsoft and Google Cloud to deploy agentic AI across its retail businesses. The initiatives span:

This is credible execution rather than aspirational positioning. Wesfarmers has both the scale of data and the balance sheet to industrialise AI across inventory, pricing, supply chain, and customer engagement. Even low-single-digit margin improvement leveraged across three major retail brands could translate into material earnings upside. The timing and magnitude remain uncertain, but the partnerships are named, funded, and underway.

The lithium exposure via Covalent Lithium (a 50:50 joint venture operating the Mount Holland project) is a different proposition entirely. This is a decade-plus call option on battery materials and EV adoption, not a near-term earnings driver. Historical scepticism has surrounded each of Wesfarmers’ major strategic bets, from the Coles acquisition through to the subsequent divestment, yet each was subsequently viewed more favourably.

The Wesfarmers business model has historically delivered value through three discrete stages: acquiring businesses with durable demand, building earnings through operational improvement, and divesting when incremental value creation is exhausted, a cycle that explains both the Coles demerger and the rationale for long-cycle bets like lithium and health.

K Home, a standalone homewares format launching in Box Hill, Victoria, extends Kmart’s private-label strength into a new category. It fits Wesfarmers’ long-running test-and-scale discipline: trial new formats carefully, and scale only what earns its keep.

| Growth Lever | Initiative | Time Horizon | Key Uncertainty |

|---|---|---|---|

| AI Integration | Microsoft and Google Cloud partnerships across Bunnings, Kmart, Officeworks | Near-term | Execution pace and margin uplift magnitude |

| Lithium Optionality | Covalent Lithium (50:50 JV), Mount Holland project | Decade-plus | Commodity cycle timing and lithium price trajectory |

| Format Expansion | K Home homewares, Box Hill, Victoria | Medium-term | Scalability beyond initial location |

Macquarie Group is not a domestic bank. It is a globally operating platform spanning four business segments: asset management, commodities and global markets, banking, and advisory and capital markets. In FY26, 68% of its income was generated internationally.

That composition matters because it determines how investors should read the earnings. Two engines inside Macquarie are highly sensitive to macro conditions and market volatility; the other parts of the business are more structural.

The cyclical drivers and structural growth drivers sit alongside each other, and the distinction between them is the single most important analytical frame for evaluating Macquarie at current prices.

Cyclical income drivers:

Structural growth drivers:

Commodities trading and risk management, capital markets deal fees, and performance fees in asset management are the most volatility-sensitive income lines. When energy prices are elevated and deal flow is strong, these segments deliver outsized results. When conditions normalise, they compress.

This is not a flaw in the business model. Macquarie has spent years building scale advantages in global commodities and capital markets, and those advantages are real. But investors who mistake cyclically elevated earnings for a new structural baseline will overpay. The FY26 result was exceptional. The question is how much of it persists.

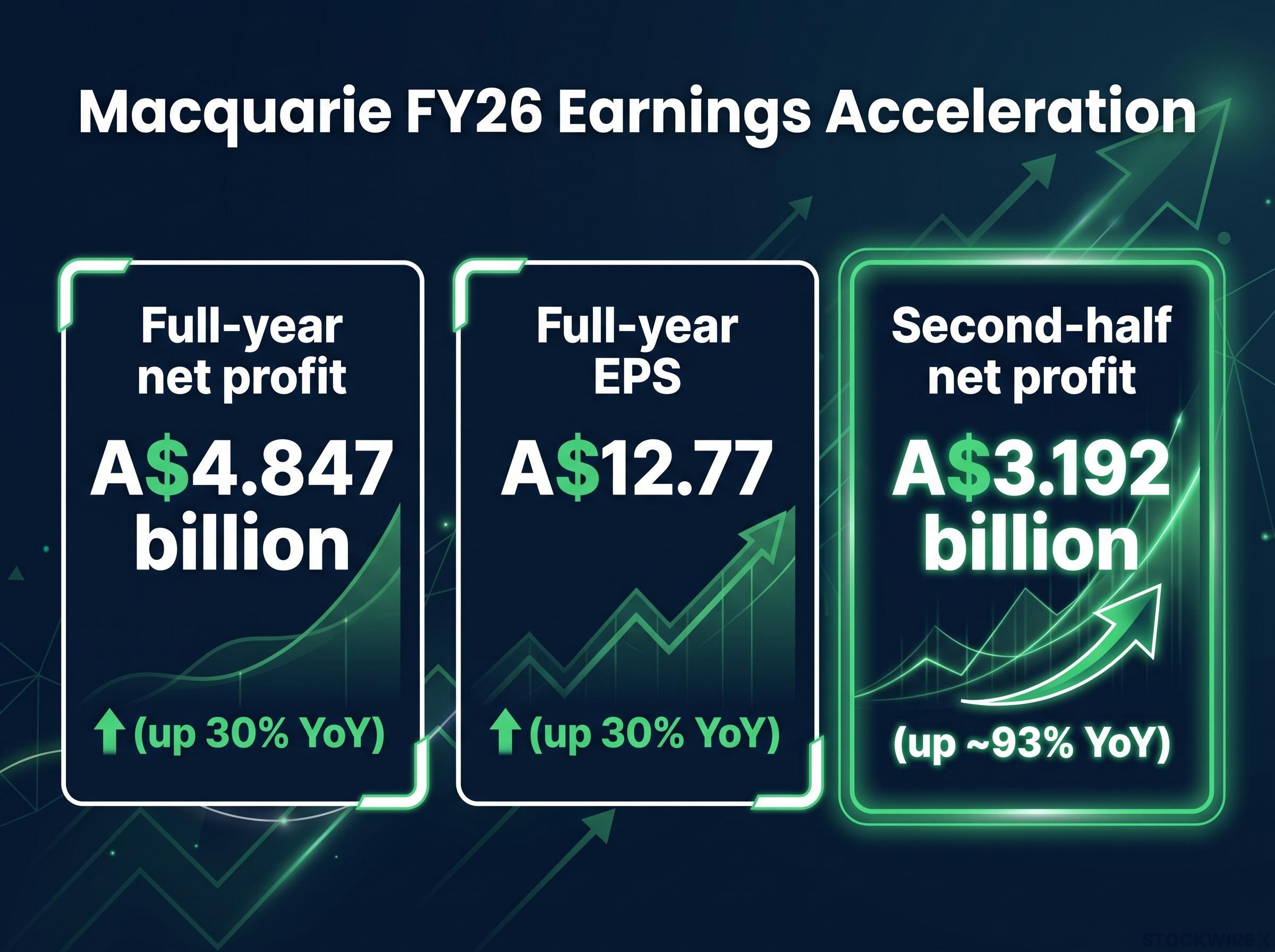

Macquarie’s full-year net profit came in at A$4.847 billion, up 30% year-on-year. Full-year earnings per share reached A$12.77, also up 30%. Those are strong numbers by any measure.

The acceleration from the first half to the second half tells the more specific story. Second-half net profit hit A$3.192 billion, a record, representing approximately 93% growth year-on-year. The combination of elevated commodities income and a cyclical rebound in deal and capital markets activity explains the shape of that acceleration.

Commodities and Global Markets was the single largest contributor to the FY26 earnings acceleration, rising 49% to A$4,221 million, while Macquarie Capital added 43% growth, together explaining why the second half alone delivered A$3,192 million and why the result sits so heavily on conditions that are inherently difficult to repeat.

Macquarie’s second-half net profit of A$3.192 billion was a record and represented approximately 93% growth year-on-year, illustrating how sharply cyclical conditions can move this business’s earnings.

The full-year dividend was A$7.00 per share, with a final dividend of A$4.20 per share at 35% franked. At a share price in the mid-A$200s (approximately A$250), these figures imply a trailing price-earnings ratio of just under 20x and a dividend yield of roughly 3% before franking.

| Metric | Result |

|---|---|

| Full-year net profit | A$4.847 billion (up 30% YoY) |

| Full-year EPS | A$12.77 (up 30% YoY) |

| Second-half net profit | A$3.192 billion (record, up ~93% YoY) |

| Full-year dividend | A$7.00 per share |

| Final dividend | A$4.20 per share, 35% franked |

| Trailing PE (at mid-A$200s) | Just under 20x |

| Dividend yield (pre-franking) | Approximately 3% |

A trailing PE of just under 20x is defensible for a franchise of this quality and global scale. But it is not cheap for a business whose earnings have just benefited from a pronounced cyclical tailwind. The share price has moved from approximately A$100 not many years ago to the mid-A$200s, and the FY26 result is embedded in that repricing. The entry price relative to the cycle matters more here than in a steady compounder.

Both Wesfarmers and Macquarie qualify as high-quality businesses. The choice between them is not about quality. It is about what kind of earnings exposure and volatility profile the investor is seeking.

Wesfarmers generates steady, diversified cash flows across retail and industrial operations. The valuation risk is that a premium multiple delivers middling returns if earnings growth merely matches, rather than exceeds, embedded expectations. The downside is muted; the upside requires patience.

A premium multiple for Wesfarmers carries a specific set of conditions: healthcare earnings growth sustained above 30%, Covalent lithium volumes arriving on schedule at elevated commodity pricing, and retail divisions holding mid-single-digit earnings growth simultaneously, a combination of requirements that explains why analysts have revised consensus targets down even as the share price has recovered.

Macquarie generates highly variable income from commodities, capital markets, and fee-based businesses. The valuation risk is that cyclically elevated earnings are already priced in. The upside, if the cycle extends, could be significant; the downside, if it turns, will arrive faster than many investors expect.

| Dimension | Wesfarmers | Macquarie |

|---|---|---|

| Character | Defensive compounder | Cyclical outperformer |

| Cash Flow Profile | Steady, diversified retail and industrial | Highly variable; commodities, capital markets, fees |

| Growth Drivers | AI integration, lithium optionality, format expansion | Green infrastructure, commodities, capital markets recovery |

| Valuation Risk | Premium multiple; modest upside if expectations merely met | Cyclically elevated earnings embedded in current price |

| Suits Investor Who | Prefers stability and visibility at a premium valuation | Accepts volatility and cyclical swings for potentially higher upside |

Investors who treat both as interchangeable “quality ASX buys” are likely to be caught off guard by Macquarie’s earnings volatility if the cycle turns. Those who dismiss Wesfarmers’ premium without understanding its compounding track record may exit too early.

At elevated prices, the question is not whether to own these stocks. It is how to enter without embedding unnecessary timing risk into the position.

Investors who want a structured framework for implementing the staged entry approach described here will find our comprehensive walkthrough of DCA versus lump sum for ASX investors useful, covering the historical outperformance data for each method, the CGT parcel advantages of staged purchases in the Australian tax context, and a hybrid deployment model suited to investors whose risk tolerance sits between the two pure strategies.

This is not an argument against owning either stock. It is an argument for respecting the cycle and the starting price, particularly for investors who did not benefit from the multi-year run that brought both stocks to where they are today.

Wesfarmers at approximately A$85 is a defensive compounder where the risk is paying a premium multiple for returns that merely match expectations. Macquarie after 30% profit growth is a cyclical outperformer where the risk is mistaking a cyclical earnings spike for a structural earnings floor.

Both remain ownable quality at mid-2026 prices for investors with appropriate time horizons and risk tolerance. Neither qualifies as a set-and-forget purchase without attention to entry discipline.

Conviction in a business and patience with the price are not opposites. For quality compounders and cyclical outperformers alike, they are the same discipline.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

Wesfarmers recovered from approximately A$70-72 in May 2026 to around A$85 by mid-June following a strategy day in which management reaffirmed AI integration partnerships with Microsoft and Google Cloud and outlined format expansion plans, giving the market fresh reason to reprice forward earnings expectations.

Macquarie Group is a globally diversified financial platform spanning asset management, commodities and global markets, banking, and advisory services, with 68% of FY26 income generated internationally; key income lines including commodities trading and capital markets fees are highly sensitive to market conditions, meaning earnings can compress quickly when cyclical tailwinds fade.

The article recommends staged entry rather than all-in purchases: for Wesfarmers, using pullbacks of 10-15% from highs as accumulation points; for Macquarie, initiating a first tranche for structural exposure and reserving subsequent purchases for pullbacks of 8-12% or confirmation that FY26 earnings represent a sustainable base rather than a cyclical spike.

Wesfarmers has three distinct growth levers: near-term AI integration via Microsoft and Google Cloud partnerships across Bunnings, Kmart, and Officeworks; medium-term format expansion through the K Home homewares concept launching in Box Hill, Victoria; and a decade-plus lithium optionality position through the Covalent Lithium joint venture at the Mount Holland project.

Macquarie posted a full-year net profit of A$4.847 billion, up 30% year-on-year, with second-half profit of A$3.192 billion representing a record and approximately 93% year-on-year growth, driven primarily by a 49% rise in Commodities and Global Markets income and a 43% increase in Macquarie Capital.