Australian businesses are being disqualified from contracts and denied insurance claims based on their cybersecurity posture, not their product quality. The shift is structural, driven by procurement gatekeeping, insurance market restructuring following heavy losses in the early 2020s, and fresh exposure from ungoverned AI adoption across organisations of every size. Hubify (ASX: HFY), a listed Australian technology company, has positioned itself at this intersection, building a managed services model around the premise that cyber security maturity is now inseparable from commercial competitiveness. What follows is an analysis of how security posture creates a compounding commercial moat, why that matters when evaluating cybersecurity-exposed stocks on the ASX, and what the Hubify model reveals about the broader structural opportunity.

Security posture is a system, not a product

Consider how a business secures its physical premises. No organisation relies on a single deadlock. It layers defences: locks, alarms, access cards, security cameras, visitor protocols, and trained staff. The protection comes from the combination. Remove any layer and the system weakens, regardless of how strong the remaining components are.

Cybersecurity operates the same way. A business may have endpoint protection but no multi-factor authentication (MFA), a protocol requiring users to verify their identity through more than one method before gaining access. It may enforce strong access controls but neglect patching discipline. Each gap is a point of exposure. When clients, insurers, or regulators assess a business’s security posture, they evaluate the whole system, not a single product licence.

Hubify’s own framing draws explicitly on this layered model, positioning cybersecurity as an integrated system rather than a standalone function. The components fall into three broad categories:

- Technical controls: endpoint protection, MFA, patching, backup systems, access management

- Organisational behaviours: staff training, incident response procedures, data handling practices

- Governance structures: policy frameworks, compliance documentation, ongoing monitoring and accountability

This systemic view is the foundation for every commercial argument that follows. Without it, the moat logic has no structural grounding.

When big ASX news breaks, our subscribers know first

How procurement gatekeeping turned security into a revenue lever

The shift began gradually. Large organisations and government agencies started embedding cybersecurity criteria into supplier onboarding processes. Early iterations were soft requirements: policy statements, self-assessments, general commitments.

Those soft requirements hardened. Contracts with enterprise and government buyers in Australia now regularly demand evidence of structured security controls, often referencing recognised frameworks and requiring documentation well beyond policy statements. In many cases, the requirements function as hard gates: if a supplier cannot meet the security threshold, the bid does not proceed. Product quality and pricing become irrelevant.

This gatekeeping is active across professional services, technology, health, and infrastructure sectors, and it carries three direct commercial implications:

- Security maturity is inseparable from business development. Organisations that treat cybersecurity as an IT cost centre are functionally excluding themselves from high-value revenue opportunities.

- Weak posture disqualifies regardless of product quality. A superior product at a competitive price cannot compensate for a supplier that fails the security gate.

- Strong posture acts as a competitive moat. Documented, evidenced security maturity creates a differentiator that under-invested competitors cannot replicate quickly.

Security maturity has ceased to be a pure cost. When it directly improves win rates in competitive tenders, it becomes a revenue-enabling investment.

Hubify has reported that clients achieving security uplift through its managed services have experienced improved tender win rates and stronger supply chain positioning. The commercial logic is straightforward: lift posture to a level that satisfies procurement requirements, document it rigorously, and use that posture to unlock or retain contracts.

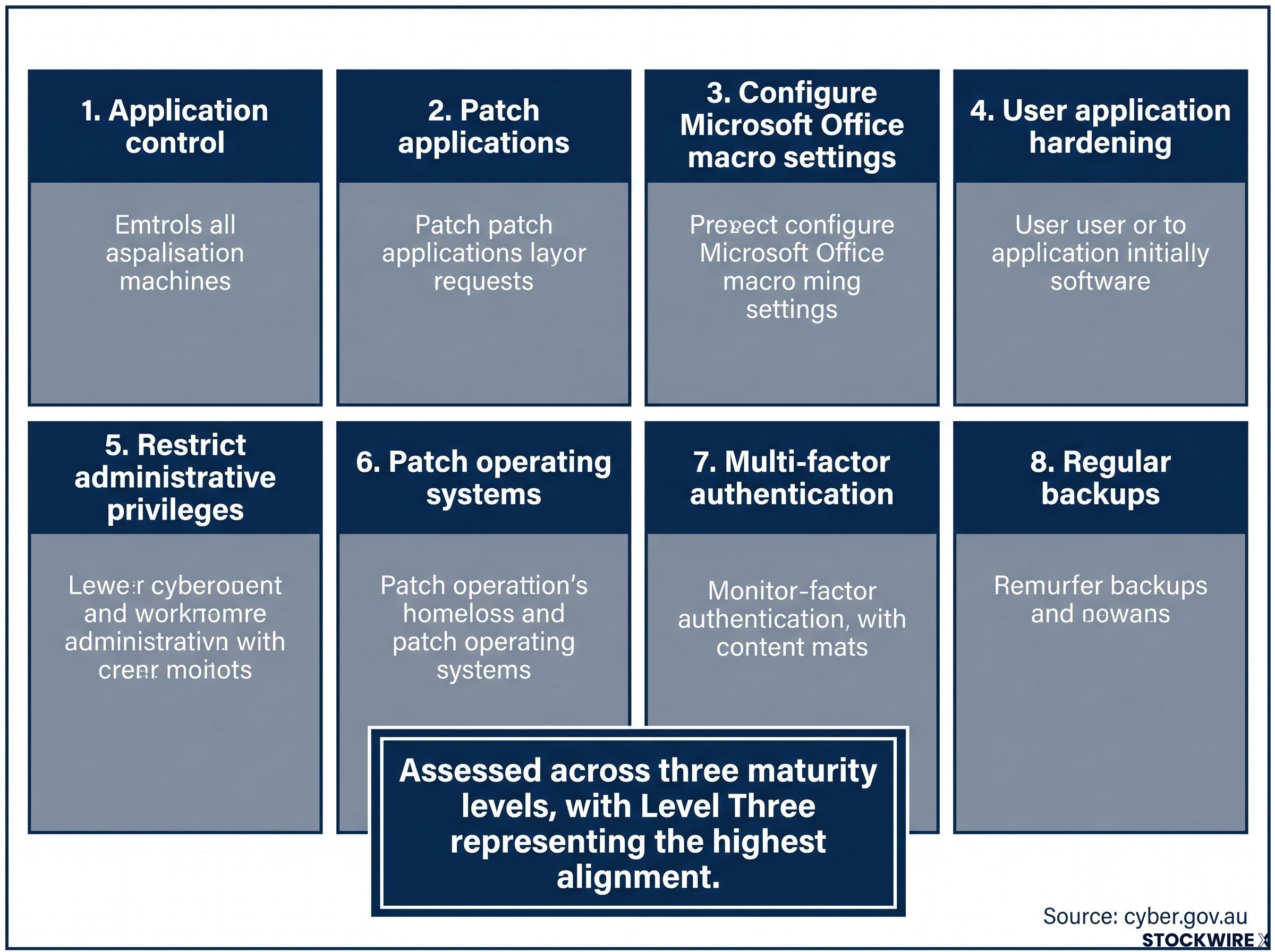

What the Essential Eight framework actually does for Australian businesses

The Essential Eight is a cybersecurity framework developed by the Australian Signals Directorate (ASD), available via cyber.gov.au, designed to mitigate the most common cyber threats targeting Australian networks. It consists of eight core strategies:

- Application control

- Patch applications

- Configure Microsoft Office macro settings

- User application hardening

- Restrict administrative privileges

- Patch operating systems

- Multi-factor authentication

- Regular backups

The framework is tailored to the Australian threat environment and is increasingly referenced across public sector and critical infrastructure procurement. When implemented at maturity, the Essential Eight is reported to materially reduce an organisation’s exposure to common cyber threat categories.

The Essential Eight maturity model, published and regularly updated by the Australian Cyber Security Centre, defines specific benchmarks for each of the eight controls across three ascending levels, with the assessments used by procurement teams and insurers as externally verifiable evidence of an organisation’s security posture.

Its commercial utility extends beyond risk reduction. The framework creates a structured, externally verifiable narrative that can be presented to clients, auditors, regulators, and insurance underwriters. It transforms an abstract security claim into a documentable credential.

Essential Eight accreditation as an acquisition rationale has already surfaced in the listed technology sector: Infotrust (ASX: ITS) acquired Canberra-based Catalyst Cyber in March 2026 specifically to secure IRAP and Essential Eight credentials, which unlock access to high-barrier federal government cyber contracts that remain closed to suppliers without those accreditations.

Maturity levels and what they mean in practice

Each of the eight controls is assessed across three maturity levels, with Level Three representing the highest alignment. These maturity designations are what procurement teams and insurers reference when evaluating suppliers, making the level itself a commercially meaningful credential rather than an internal benchmark.

Reaching a target maturity level, however, is only the beginning. Threats evolve, systems change, and staff turn over. Without continuous monitoring, maintenance, and governance, maturity degrades, and the procurement and insurance benefits it secured degrade with it. Hubify positions ongoing monitoring and support as the mechanism for maintaining and improving maturity over time, converting a one-off compliance project into a recurring engagement.

Cyber insurance has restructured around posture, and the stakes are now higher

Cyber insurers spent much of the early 2020s absorbing heavy losses from ransomware, business interruption, and data breach claims. Their response has been to restructure underwriting standards and tie coverage far more aggressively to demonstrated security controls, a tightening that has continued into 2026.

Three dimensions now define the relationship between security posture and insurance outcomes, and each carries escalating consequences.

| Insurance dimension | What determines the outcome | Implication for businesses without strong posture |

|---|---|---|

| Eligibility | Baseline controls including MFA, patching, and data backup practices | May be unable to obtain meaningful cyber cover at all |

| Pricing | Documented controls, regular patch cycles, privileged access management, tested backup and restoration | Higher premiums and less favourable policy limits |

| Claims validity | Whether required controls were in place at the time of the breach | Claim may be denied even where premiums have been paid |

The eligibility and pricing dimensions are well understood. The claims validity dimension is where the highest-stakes risk sits.

A business can believe it is insured, suffer a major incident, and then discover its posture did not meet the conditions of cover. The claim is denied. The premiums were paid. The protection was illusory.

The controls that insurers treat as thresholds map closely to those emphasised in the Essential Eight: MFA, patching, privileged access management, and tested backup and restoration. For managed security providers like Hubify, this creates a tangible return-on-investment narrative for clients: improved posture, lower premiums, and reduced claims risk. Insurance economics, not just risk sentiment, are driving demand for these services, and that represents a more durable demand driver for investors to evaluate.

The AI governance gap is compounding the risk for unprepared organisations

Australian organisations are accelerating their adoption of generative AI across productivity, customer service, and internal operations. Much of this adoption is occurring at the team or individual level, frequently ahead of formal policies, data governance frameworks, or risk assessments. The gap between adoption speed and governance maturity is widening.

The risk is structural, not speculative. When employees paste client data, proprietary information, or sensitive communications into cloud-based AI platforms, they may unintentionally expose that data to third parties, retain it in external systems beyond the organisation’s control, or contribute it to model training and jurisdictional transfer.

AI-amplified attack surfaces are compounding this exposure: CrowdStrike’s 2026 Global Threat Report recorded an 89% surge in AI-enabled attacks and adversary breakout times falling to 29 minutes, a threat escalation pattern that APRA’s April 2026 review found was running ahead of governance responses at Australian financial institutions.

This creates three categories of exposure:

- Data governance failures and regulatory breaches where sensitive information leaves the organisation’s governance perimeter

- Contractual exposure with clients who assume tighter data controls than are actually in place

- Insurance complications where AI-related exposures fall outside existing policy wordings

Why existing governance infrastructure is the differentiator

The same disciplines used for Essential Eight compliance, including access control, data classification, logging, and policy enforcement, provide the foundation for extending governance to AI tools and workflows. Organisations already operating at higher maturity levels face a lower incremental cost to build AI governance policies than those starting from scratch.

Hubify’s positioning explicitly addresses this parallel requirement, framing AI governance as a natural extension of its cyber maturity programmes. For managed security providers broadly, this expands the addressable market beyond traditional controls and deepens the per-client engagement, making the managed security relationship more embedded in client operations over time.

What the Hubify model signals for investors evaluating cybersecurity exposure on the ASX

Hubify (ASX: HFY) describes itself as a listed Australian provider of AI-powered ICT managed services, encompassing telecommunications, IT, connectivity, cloud, and cybersecurity solutions. The company targets businesses with approximately 10 to 1,000 employees and markets itself as a single-source provider of “cyber secure, intelligent, reliable” services, with a growing emphasis on managed security at the network and endpoint layers.

The investor thesis rests on the structural nature of the demand drivers described throughout this analysis. Regulatory pressure, procurement gatekeeping, and insurance economics are driving demand for managed cybersecurity services in Australia, rather than discretionary IT sentiment. That distinction matters: it implies more durable, less cyclical demand.

The ASX cybersecurity investment case extends beyond individual managed service providers: the Betashares HACK ETF, which holds approximately A$1.386 billion in funds under management, provides diversified exposure to the same structural demand drivers, including regulatory pressure, non-discretionary enterprise spending, and the expansion of attack surfaces driven by AI adoption.

Five structural positioning elements define the commercial model:

| Structural positioning element | Commercial outcome enabled |

|---|---|

| Recurring revenue alignment | Continuous monitoring, patching, and policy management generate predictable, recurring revenue streams |

| Embedded supply chain relationships | Security uplift increases client eligibility for sensitive projects, deepening relationship stickiness |

| Tender and procurement leverage | Essential Eight alignment directly influences client ability to win enterprise and government contracts |

| Quantifiable ROI via insurance | Posture-linked premium reductions and improved coverage terms create a measurable financial justification |

| Intersection of two structural tailwinds | Cybersecurity maturity and AI governance combine into a single integrated service model with compounding demand |

For businesses operating with weak security posture, the compounding risk profile now includes lost contracts through procurement disqualification, higher insurance premiums, potential claims denial following incidents, and growing AI governance exposure. Managed security providers that can address this full spectrum are positioned to capture value across multiple, mutually reinforcing demand drivers.

Security maturity as a moat is not a trend but a structural reset for Australian technology businesses

Cybersecurity maturity has crossed a commercial threshold. It is now assessed simultaneously by procurement teams deciding who can bid, by underwriters setting coverage terms and premiums, and by regulators reviewing compliance postures. Each evaluation reinforces the others, creating a compounding moat for well-positioned providers.

Three demand drivers underpin this structural reset: procurement gatekeeping, insurance market restructuring, and AI governance requirements. None is cyclical. All are regulatory or structural in origin, and all are intensifying.

Listed technology companies capable of delivering integrated offerings across connectivity, cybersecurity maturity, and AI governance are positioned to benefit from these tailwinds simultaneously. The commercial moat they build, through documented controls, maintained maturity levels, and deep familiarity with client environments, is difficult and costly for competitors to displace.

For investors wanting to understand why the threat environment facing managed security clients is accelerating rather than stabilising, our deep-dive into the AI offence-defence asymmetry examines how Palo Alto Networks compressed five to seven years of vulnerability discovery into six weeks using AI scanning, and what that compression means for enterprise security spending trajectories and platform vendor moats.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.