Brent crude fell below $80 per barrel for the first time since March 2026 on Thursday as U.S. Vice President JD Vance withdrew from scheduled peace talks in Switzerland, leaving markets to price a deal that has not yet been delivered. The U.S. and Iran struck a ceasefire in mid-June, built on a specific promise: a phased reopening of the Strait of Hormuz, the chokepoint carrying roughly one-fifth of global oil and liquefied natural gas (LNG) shipments. The cancellation of follow-up talks in Geneva on 19 June puts that timeline in doubt, introducing a fresh layer of implementation risk into a market that had already begun trading as if the agreement were done.

What follows is an account of what the cancelled talks mean for oil prices, why the ceasefire and the peace deal are not the same thing, and what the asymmetric risk structure looks like for investors positioned across energy and broader financial markets.

Vance pulls out of Geneva, throwing the implementation timeline into question

U.S. officials informed Swiss hosts that the American delegation would not attend the 19 June Geneva session. Switzerland confirmed the planned U.S.–Iran meeting “would not take place on Friday.”

The current status, at a glance:

- Ceasefire: In place since mid-June 2026, following a conflict that began in late February 2026

- Strait of Hormuz: Phased reopening envisioned under the framework agreement but not yet underway

- Follow-up talks: Cancelled; no replacement date announced

Iranian media framed the impasse as an implementation dispute, with Tehran seeking tangible evidence that Washington is fulfilling its obligations under the existing agreement before engaging in another negotiating round. Western outlets reported a broadly similar reading: this is a dispute over execution, not an outright collapse.

The distinction matters more than the headline suggests. A ceasefire stops the shooting. A completed deal reopens the strait, normalises sanctions, and restores the supply flows that global energy markets depend on. The first can hold while the second stalls indefinitely, and that gap is precisely what traders are now being forced to price.

When big ASX news breaks, our subscribers know first

Why the Strait of Hormuz is the only number that matters for oil supply right now

The Strait of Hormuz sits between Iran and the Arabian Peninsula, and every barrel of crude or cargo of LNG that leaves the Persian Gulf must pass through it.

Approximately one-fifth of global oil and LNG shipments transit the Strait of Hormuz, making it the single most important energy chokepoint in the world.

The strait remained largely closed throughout much of the 2026 conflict. When the mid-June ceasefire explicitly envisioned a phased reopening alongside an extension of the truce, oil prices fell sharply as traders priced in imminent supply normalisation. The cancelled Geneva session now introduces doubt about the speed and reliability of that reopening.

LNG exposure extends the risk beyond crude. Qatar and other Gulf producers ship significant volumes of gas through the strait, meaning Asian and European markets reliant on seaborne LNG face direct exposure to any implementation delay. The interim deal had eased fears of a prolonged LNG shock; a stalled reopening would tighten those markets again.

From geography to price: how Hormuz closures transmit into markets

When the strait is closed or threatened, near-term supply tightens faster than longer-dated supply, widening time spreads and steepening backwardation (a market structure in which contracts for immediate delivery trade at a premium to those further out, signalling that buyers expect scarcity to persist). The ceasefire news narrowed those spreads as traders priced in imminent supply relief. Any reversal would widen them again, repricing the entire forward curve.

Oil prices have already banked the deal, creating a two-sided risk structure

Brent and WTI are sitting at levels that reflect a bet on successful implementation, not on a fully resolved diplomatic relationship. That distinction is the source of vulnerability.

| Benchmark | Current Price | Daily Move | Weekly Move |

|---|---|---|---|

| Brent Crude | $79.01/barrel | −1.1% | ≈ −10% |

| WTI Crude | $76.05/barrel | −0.7% | ≈ −10% |

Both benchmarks are on track to lose approximately 10% for the week ending 19 June 2026, their steepest weekly decline in several months.

Brent dropped below the psychologically significant $80 mark for the first time since early March 2026. The speed of the decline reflects how aggressively the market had priced in supply normalisation.

The risk from here is two-sided. Further downside remains possible if diplomacy resumes and the Hormuz reopening proceeds on schedule. But upside spike risk is equally material: any headline suggesting renewed fighting, sabotage in the Gulf, or explicit delays to reopening could trigger a fast reversal as short positions cover and hedging demand surges. Earlier phases of the conflict produced double-digit percentage intraday moves on breaking news of attacks, strikes, or breakthroughs. That sensitivity to incremental headlines has not dissipated; it has simply been compressed into a narrower range.

Investors who read the current price level as a stable new floor are misreading the structure. This is a provisional zone where each diplomatic development carries outsized impact in both directions.

Cross-asset spillover: what stalled talks mean beyond the crude price

The cancelled Geneva session is not just an energy story. The transmission runs through at least three distinct channels:

- Energy equities: The drop in crude has weighed on integrated oil majors and upstream producers. A sudden rebound driven by geopolitical headlines would support upstream names but could squeeze refiners if crude rises faster than product prices, compressing margins.

- Central bank rate paths: The 2026 Hormuz crisis contributed to higher headline inflation, particularly in import-dependent Asia and Europe. Some central banks had begun treating lower crude as a disinflationary tailwind, signalling more comfort about the medium-term energy outlook after the ceasefire. A stalled reopening complicates that narrative, potentially delaying easing cycles or prompting more cautious guidance.

- Equity and credit risk premia: A breakdown in truce confidence could generate higher equity risk premia in Europe and Asia, pressure on airlines and logistics stocks sensitive to jet fuel and bunker costs, and wider credit spreads for lower-rated energy issuers whose cash flows depend on stable export volumes.

The 2026 conflict had already demonstrated that sharp moves in crude rarely stay confined to oil. Cyclicals, transportation, chemicals, emerging markets, and high-yield credit tied to energy producers all absorbed the volatility during earlier escalation phases. That interconnection has not unwound.

What investors should watch as the deal enters contested implementation

Implementation risk is now the dominant variable shaping energy prices and the cross-asset effects that follow from them. Disputes over sanctions relief terms, verification timelines, and security guarantees each transmit directly into Hormuz flows.

The ceasefire and the peace deal remain structurally distinct. The absence of active hostilities does not guarantee timely implementation of the strait’s reopening or sanctions normalisation. Earlier conflict phases produced double-digit percentage intraday price moves on breaking news, and the nonlinear negotiation dynamic means frequent headline risk is likely to persist.

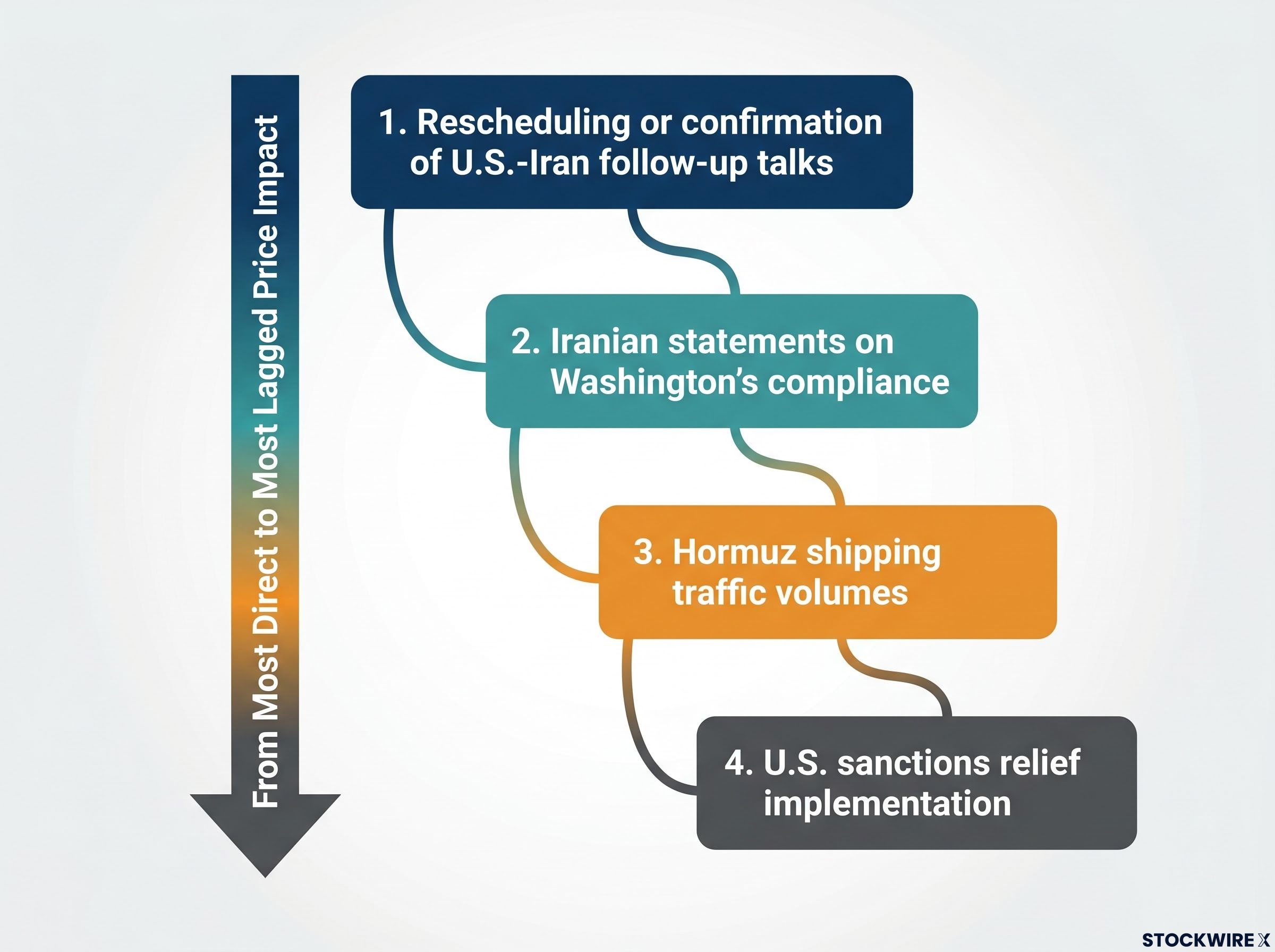

The four signals closest to the oil price

The following signals are ordered by proximity to price impact, from most direct to most lagged:

- Rescheduling or confirmation of U.S.–Iran follow-up talks. Any announcement of a replacement session would signal that the diplomatic track remains active; continued silence would deepen implementation doubt.

- Iranian official statements on Washington’s compliance with existing obligations under the framework agreement, the condition Tehran has set for re-engagement.

- Official or third-party reporting on Hormuz shipping traffic volumes. Physical vessel data is the most direct measure of whether the strait is actually reopening, regardless of what either government says.

- U.S. Treasury or State Department announcements on sanctions relief implementation. These determine whether the economic architecture of the deal is being built or delayed.

In a market this sensitive to incremental news, the difference between a well-positioned portfolio and a reactive one is knowing in advance which signals carry material weight.

A provisional market, not a new equilibrium

The week’s price action tells a specific story: markets priced in the deal before the deal was done, and the cancelled Geneva session has exposed that assumption. Brent and WTI have lost roughly 10% in a week, yet the current level still reflects substantial optimism about a reopening that remains unconfirmed.

Multi-market transmission means the stakes extend well beyond the crude price line. Volatility in oil and LNG feeds directly into inflation expectations, central bank rate paths, and sector performance across global equities and credit. A single headline from Tehran or Washington can move all of them simultaneously.

The ceasefire holding is a necessary condition for supply normalisation. It is not a sufficient one. The diplomatic path from “no shooting” to fully restored Hormuz traffic requires implementation steps that are now visibly contested. Until those steps are completed, the current price environment is best understood as provisional, not as a floor.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding the ceasefire, Hormuz reopening, and oil price movements are speculative and subject to change based on diplomatic developments, market conditions, and geopolitical risk factors.