How to Screen Dividend Stocks Using a 4-Pillar Framework

2 hrs ago

Most investors searching for guidance on how to prepare for a financial crisis are looking for the same thing: a signal to act on before the next crash arrives. The instinct is understandable. Financial crisis histories are widely documented, and the lesson they appear to teach is simple: get out before the fall. Yet that instinct, applied as a timing strategy, is precisely what destroys long-run returns. With AI-driven markets attracting concentrated capital flows, systemic debt levels elevated globally, and narrative momentum building across multiple sectors in 2026, the tension between pattern recognition and disciplined preparation has rarely been more relevant. This guide offers a different approach: a four-question diagnostic framework and a periodic self-assessment checklist designed to convert crisis awareness into a concrete preparation discipline, not a prediction-and-exit strategy.

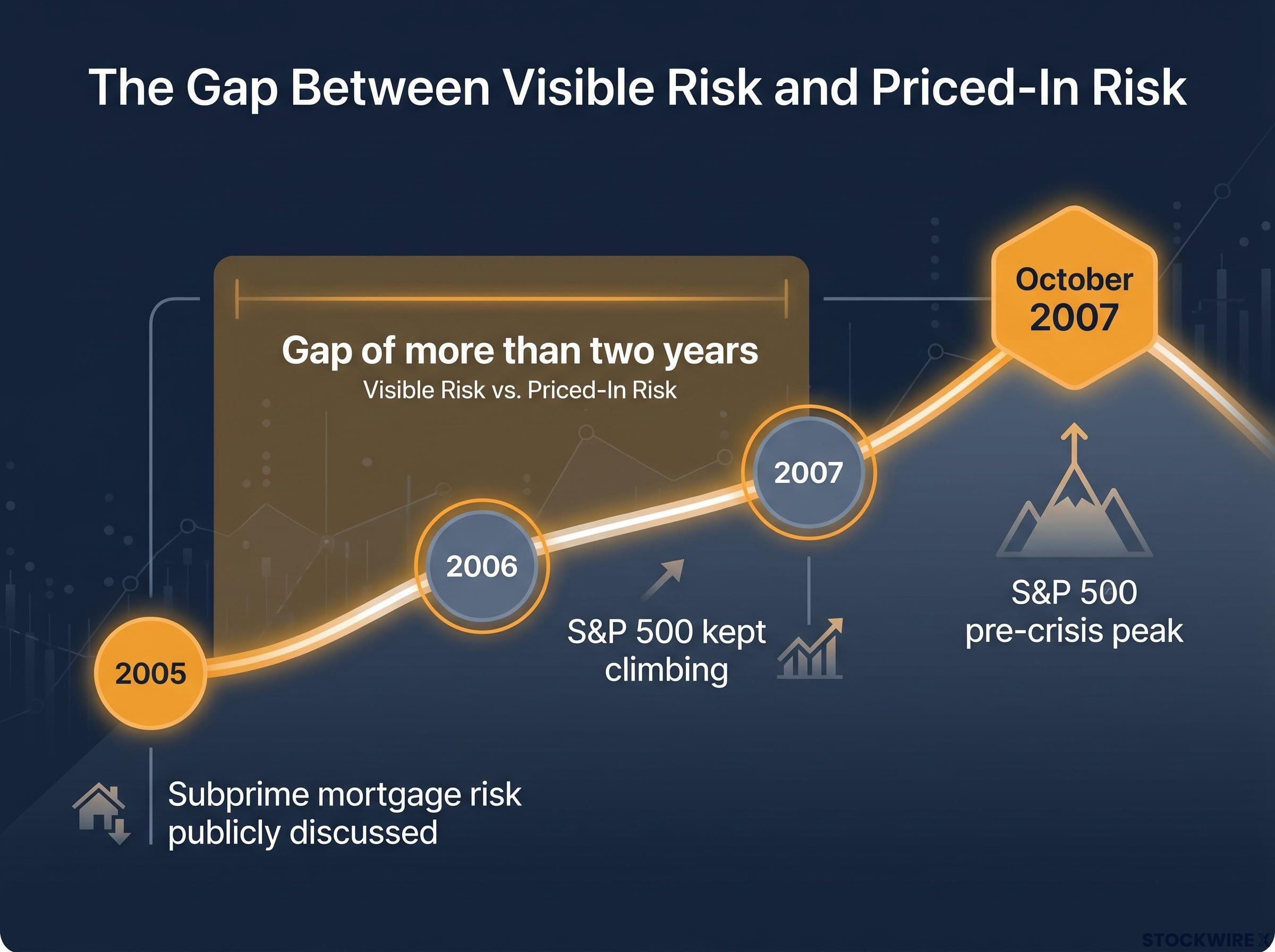

Subprime mortgage risk was publicly discussed as early as 2005. Analysts flagged deteriorating lending standards, rising default probabilities, and structural fragility in securitised debt markets. The S&P 500 kept climbing through 2006 and 2007, reaching its pre-crisis peak in October 2007. The gap between “visible risk” and “priced-in risk” spanned more than two years.

This is not an anomaly. It is the norm. Structural warning signs and rising markets coexist for extended periods across nearly every major crisis episode on record.

Visible structural risks and rising markets frequently coexist for years. Recognising the risk tells investors little about when it will be fully priced in.

Even if an investor correctly identifies a building risk, successful market timing requires executing every step in a fragile sequence:

Missing any single step in that chain typically leaves investors worse off than a simple, fully invested strategy over a full market cycle. Research from major financial education institutions, including Schwab and others, consistently documents that staying invested outperforms ad-hoc timing attempts over complete cycles.

The cost of crash protection strategies is measurable and persistent: the traditional 60/40 portfolio lagged the S&P 500 by approximately 14 percentage points in 2024, illustrating that defensive positioning carries a real annual drag that compounds across the same multi-year periods investors are trying to protect against.

Vanguard research on staying invested over a 37-year period from 1988 to 2024 documents the compounding cost of missing even a small number of the market’s best days, with investors who attempted to time exits consistently underperforming those who held through full cycles.

None of this is a counsel of ignorance. Pattern recognition is genuinely useful. It simply serves a different purpose than most investors assume: it informs preparation, not timing.

If crisis literacy does not reliably improve timing, what does it improve? The answer is the quality of the plan investors bring to volatility before it arrives.

Crisis history is most valuable when it informs a written Investment Policy Statement (IPS), a document that captures the investor’s target allocation, risk boundaries, rebalancing rules, and liquidity plan before markets become stressful. The diagnostic questions introduced later in this guide are designed as prompts to review that IPS, not as overrides for it.

A written IPS typically covers:

The historical pattern reinforces why this matters. Every major innovation cycle, railways, electrification, the internet, financial engineering, crypto, and now AI, has attracted capital, narrative momentum, and periodic dangerous overconfidence. The investors who fared best across those episodes were not the ones who predicted the turning point. They were the ones who entered the downturn with a plan that prevented them from becoming forced sellers at the worst possible moment.

The goal is to be a prepared investor who can hold through volatility and benefit from recovery, not one who crystallises losses at the bottom.

The four questions below are not a one-time audit. Each functions as a lens that sharpens with repeated use across different market environments. A “yes” to any question should trigger a review of the IPS and preparation posture, not a trade.

For non-specialists, these signals fall into two categories. Plumbing stress refers to strain in funding and repo markets, where institutions borrow short-term to finance longer-term positions. Risk premium spikes refer to widening credit spreads, particularly in the sector driving the prevailing narrative.

Crises become systemic when banks, insurers, and shadow banks load up on the same asset class, often funded with short-term borrowing. The image is concrete: dozens of institutions holding the same kind of mortgage bond, all funded overnight.

Institutional herding signals are currently unusually concentrated: the May 2026 BofA Fund Manager Survey recorded the largest single-month equity allocation surge ever measured, a 37-percentage-point jump to a net 50% overweight, with long global semiconductors identified as the most crowded trade at 73% conviction, exactly the configuration that diagnostic question two is designed to detect.

Rising systemic debt shrinks the financial system’s margin of safety. When that margin narrows, the appropriate response is to widen personal margins: less leverage, more liquidity.

The BIS analysis of debt and the financial cycle provides empirical grounding for the relationship between rising leverage and crisis severity, showing that the build-up of financial vulnerabilities across public and private sectors reliably compresses the system’s capacity to absorb subsequent shocks.

Not every major innovation constitutes a speculative bubble. The more relevant question is whether the risks associated with an innovation are being systematically underestimated.

| Question | What it detects | Historical example | Portfolio implication |

|---|---|---|---|

| Funding or credit stress | Early institutional confidence erosion | Repo and commercial paper strain preceding the 2008 acute phase | Confirm near-term cash needs are funded |

| Institutional overexposure | Systemic spillover from leveraged herding | Banks holding subprime mortgage bonds funded with overnight borrowing | Assume contamination of “safe” assets during stress |

| Rising systemic debt | Shrinking system-wide margin of safety | Pre-2008 leverage expansion across public and private sectors | Reduce personal leverage, increase liquidity |

| Untested innovation dominance | Concentration risk from underestimated innovation risk | Internet stocks (late 1990s), financial engineering (mid-2000s) | Audit single-theme concentration |

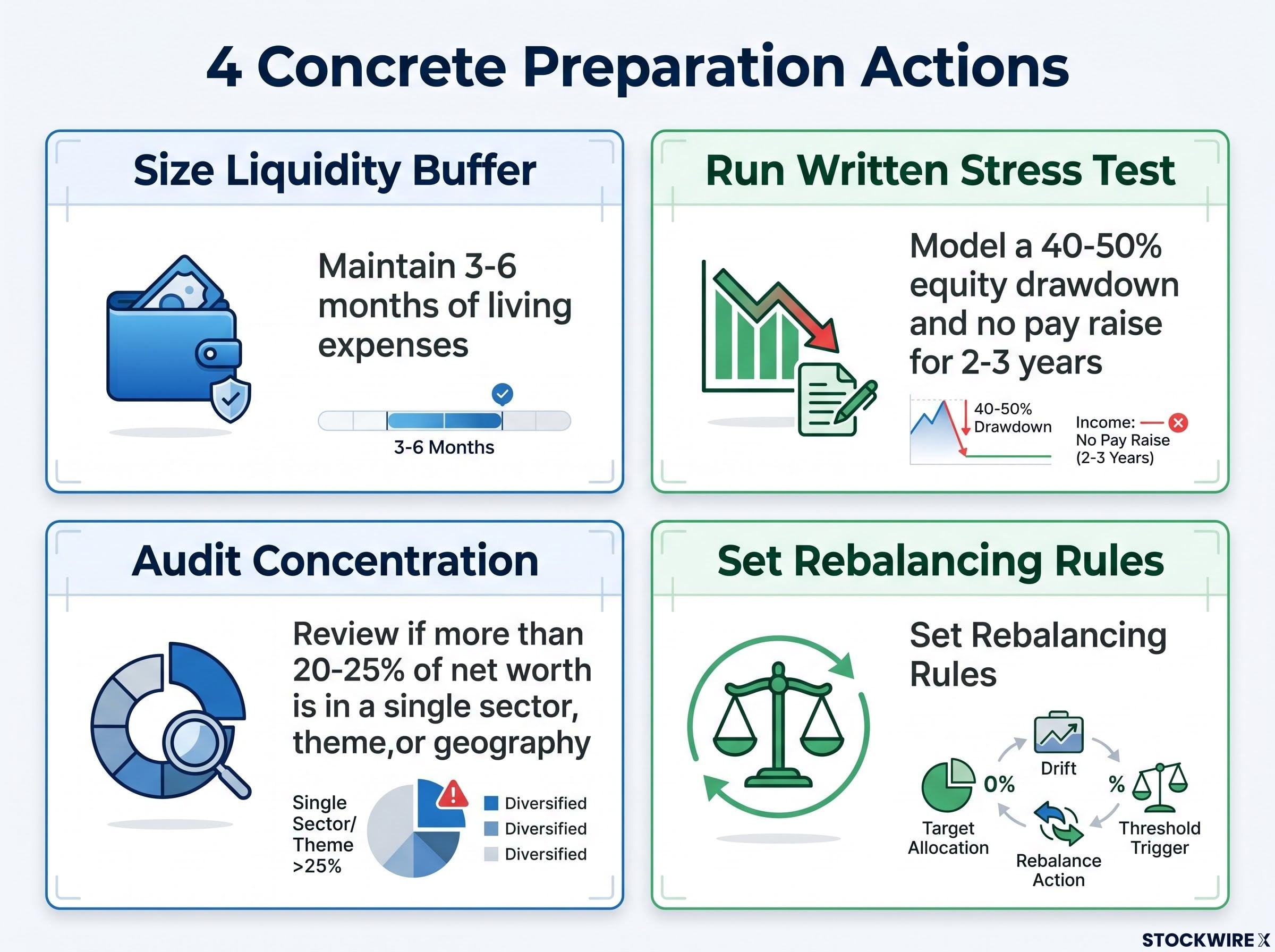

If one or more of the diagnostic questions flags elevated risk, the following four actions represent the practical levers available. Each can be completed this week. Each materially improves resilience regardless of whether a downturn arrives.

Model this scenario: a 40-50% equity drawdown, no pay raise for 2-3 years, and a temporary job loss if relevant. Write down how the portfolio and household cash flow respond. The written results are the preparation; the act of writing them reduces panic-driven decisions during actual downturns.

Rules-based rebalancing after large market moves functions as a systematic sell-high-buy-low mechanism that requires no forecast: Vanguard recommends a quarterly review combined with a 5% drift threshold as the rebalancing trigger, and a portfolio that has drifted from a 60% to a 70% equity weighting during a multi-year rally clearly meets that threshold before a correction arrives.

Writing these down matters. A plan that exists only as a vague intention provides little resilience when volatility arrives. A written protocol, reviewed annually, functions as a commitment device against the very instincts that destroy returns during downturns.

The 2008 financial crisis produced a severe market drawdown that tested every investor’s process. It also produced one of the strongest subsequent recovery periods in stock market history. The gap between those two outcomes, the drawdown and the recovery, is where preparation made the difference.

Investors who navigated 2008 well did not, as a group, predict the crash. They were simply prepared before it arrived. Three elements characterised their positioning:

These three elements map directly to the diagnostic framework and preparation checklist presented above. The framework is not theoretical. It describes, in portable form, the exact preparation posture that distinguished investors who held through the downturn and captured the recovery from those who sold near the bottom and re-entered too late.

Staying invested through the 2008 downturn positioned investors for one of the strongest recovery periods on record. The preparation framework does not promise to avoid losses. It aims to ensure that temporary losses remain temporary, rather than being crystallised into permanent ones by forced or panic-driven selling.

The four diagnostic questions and four preparation actions combine into an eight-question checklist designed for annual or semi-annual review. The checklist applies to any market environment, not only periods that visually resemble past crises.

| Checklist question | What a “yes” means for preparation |

|---|---|

| Untested innovation dominating returns? | Review concentration; ensure exposure is intentional, not performance-chasing |

| Institutions heavily exposed with leverage? | Assume safe assets may correlate with risk assets during stress; diversify accordingly |

| Systemic debt rising? | Widen personal margin of safety: reduce leverage, increase liquidity |

| Funding or credit stress emerging? | Confirm near-term cash needs are funded; verify willingness to hold riskier positions through a full cycle |

| Liquidity buffer adequate? | If not, top it up before markets give a reason to |

| Can a 40-50% drawdown be absorbed? | If not, allocation exceeds true risk tolerance; adjust target weights |

| Concentrated in prevailing themes? | Audit whether concentration reflects conviction or drift |

| Aligned with written IPS? | If no IPS exists, write one. If it exists, confirm it still reflects current circumstances |

Running this checklist once or twice a year takes less than an hour. The discipline it builds compounds across market cycles, ensuring that preparation stays current without requiring ongoing monitoring or specialist expertise.

Crisis literacy, applied as a preparation discipline rather than a prediction tool, positions investors to hold through volatility and benefit from recovery. The data across multiple market cycles supports a consistent finding: investors who entered downturns with a liquidity buffer, a diversified allocation, and a written commitment to their process emerged in stronger positions than those who attempted to time the exit and re-entry.

The most concrete starting point is the Investment Policy Statement. Investors who do not have one can begin by writing their target allocation, risk limits, rebalancing triggers, and liquidity plan on a single page. Those who already have one can run the stress-test scenario: model the 40-50% drawdown, write down the results, and confirm that the plan holds.

From there, the annual checklist sustains the habit. The goal is not to predict what comes next. It is to ensure that whatever comes next does not force a bad decision.

For readers wanting to examine whether their diversification assumptions still hold in the current rate and inflation environment, our full explainer on building portfolio resilience beyond the 60/40 framework covers how the stock-bond correlation turned persistently positive during the inflation shocks of 2022, 2025, and May 2026, and what a three-tier adaptive portfolio structure looks like in practice.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

An Investment Policy Statement (IPS) is a written document that captures your target allocation, risk limits, rebalancing rules, and liquidity plan before markets become stressful. It functions as a commitment device that prevents panic-driven decisions during downturns, which is why financial preparation guides consistently recommend writing one before volatility arrives.

Financial preparation frameworks recommend maintaining 3-6 months of living expenses in cash-like instruments, with a higher buffer recommended if your income is variable or your equity exposure is particularly high. This buffer ensures that no market condition forces you to sell investments at a depressed price.

Successful market timing requires executing every step in a fragile sequence: exiting early enough, holding cash through continued market gains, and re-entering near the bottom without a clear signal the bottom has arrived. Missing any single step typically leaves investors worse off than a simple, fully invested strategy held across a complete market cycle.

If more than 20-25% of net worth is tied to a single sector, theme, or geography, the article recommends auditing whether that exposure is intentional and aligned with your Investment Policy Statement or simply the result of recent performance chasing.

The article recommends running the eight-question crisis readiness checklist once or twice a year, noting that the annual or semi-annual review takes less than an hour and builds a preparation discipline that compounds across multiple market cycles.