Bank of America just issued a double-upgrade on Intel, jumping directly from Underperform to Buy, a rating move so unusual it signals not an incremental view change but a complete thesis reset. On 11 June 2026, analyst Vivek Arya raised Intel’s price target from $96 to a Street-high $135 while colleague Didier Scemama simultaneously set a Street-high price target of €86 on STMicroelectronics. Both calls rest on the same underlying conviction: the market is materially mispricing the long-term earnings power of semiconductor companies that are not Nvidia, and a broadening AI infrastructure cycle is the mechanism that will close that gap.

What follows unpacks the specific catalysts BofA identified for each company, the valuation frameworks behind the targets, and what this pairing reveals about where the next phase of AI-driven semiconductor returns may be concentrated.

Why Bank of America’s Intel call is structurally unlike a standard upgrade

A double-upgrade, moving directly from Underperform to Buy in a single step, is one of the rarest actions in sell-side practice. Analysts almost always pass through Neutral on the way up, giving their institutional clients time to reposition. Skipping that step is a public signal that the prior bearish thesis has not merely softened; it has broken.

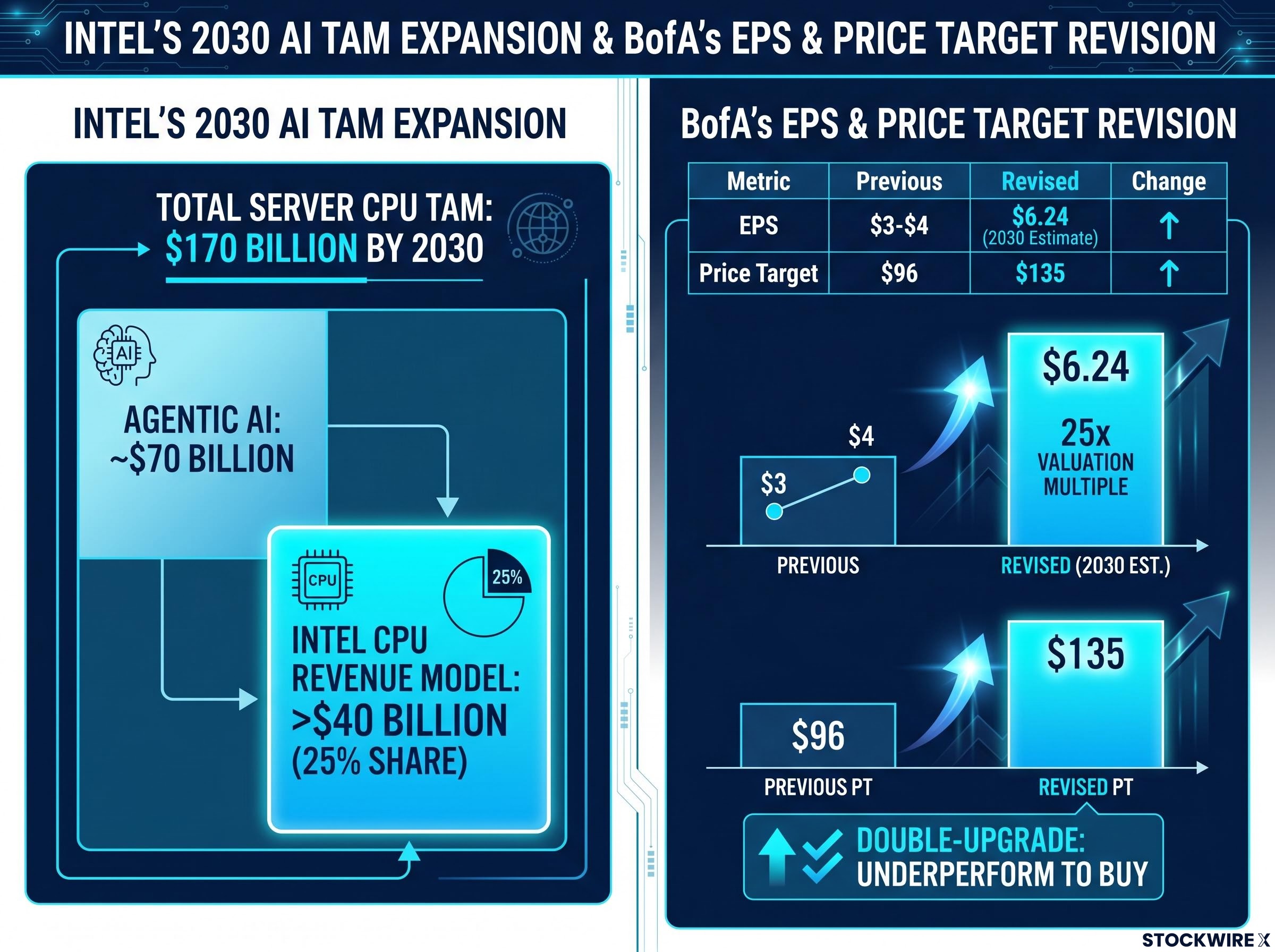

BofA acknowledged as much explicitly. The firm stated that its prior sum-of-parts valuation methodology was inadequate for capturing Intel’s longer-dated CPU and foundry opportunities, meaning the old framework was not generating a wrong number from correct assumptions but was structurally unable to see the opportunity at all. Arya’s new $135 target sits well above Street consensus, which remained in the low $90s at publication, below both the stock price and BofA’s call.

Intel shares rose approximately 6.51% on the day, with more than 151 million shares traded. The stock’s $540 billion market capitalisation makes this one of the largest companies in the S&P 500 to receive a double-upgrade in recent years.

Institutional positioning: Intel is held by only approximately 16% of S&P 500 funds, ranking as the second least-owned stock in its semiconductor peer group despite holding the fifth-largest market cap in the sector. BofA highlights this under-ownership as a potential re-rating amplifier.

When big ASX news breaks, our subscribers know first

The agentic AI thesis reframes what a CPU is worth

The prevailing narrative for most of the AI hardware cycle has been straightforward: GPUs win, CPUs lose relevance. BofA’s note challenges that framing directly, and the mechanism it identifies is specific enough to evaluate on its merits.

Arya positions CPUs not as legacy compute being displaced but as orchestrators of agentic AI workloads, the autonomous reasoning loops, memory state management, and tool-use coordination that run alongside GPU-dense inference. As agentic architectures scale, the CPU does not shrink in importance; its function broadens. BofA projects this structural shift produces a total addressable market (TAM) for server CPUs of $170 billion by 2030, with the agentic AI category alone estimated at approximately $70 billion.

AMD’s Q1 2026 earnings provided independent confirmation of agentic AI hardware demand, with the company raising its server CPU total addressable market growth forecast from 18% to 35% annually and identifying agent orchestration tasks as the driver, corroborating the CPU-as-orchestrator thesis that BofA applies to Intel’s 2030 earnings model.

BofA projects a $170 billion total addressable market for server CPUs by 2030, with Intel’s CPU revenue modelled at more than $40 billion, representing approximately 25% TAM share.

Intel’s modelled share of that TAM is where the earnings revision gets its scale. BofA now estimates Intel can generate $6.24 in earnings per share by 2030, up from its prior range of $3-$4, a roughly 60%+ upward revision. The mechanical translation from thesis to price target is direct: a 25x multiple applied to $6.24, discounted back two years, yields $135.

| Metric | Prior BofA estimate | Revised 2030 estimate | Implied outcome |

|---|---|---|---|

| EPS power | $3-$4 | $6.24 | ~60%+ upward revision |

| Valuation multiple | N/A (prior methodology) | 25x | Applied to 2030 EPS |

| Price target | $96 | $135 | Discounted back two years |

The size of the EPS revision explains why BofA bypassed a neutral step. At $3-$4, the stock was a hold-at-best; at $6.24, the valuation framework produces a target that requires a Buy rating to be intellectually consistent.

Intel Foundry Services is the second engine in BofA’s thesis

The CPU demand story is one leg; the supply-side story is the other. Intel Foundry Services (IFS) has carried the reputation of a capital-intensive liability for much of its existence. BofA’s note reframes it as a capacity asset that external chip designers are finding increasingly difficult to ignore.

The firm sizes the foundry opportunity at more than $45 billion by 2030 and identifies a specific pipeline of potential external customers:

- Apple M-series wafer production

- MediaTek TPU wafer production

- ARM-based server CPU designs from multiple vendors

None of these wins are confirmed orders, and the distinction matters. They represent the addressable pipeline BofA believes is realistic given Intel’s process technology trajectory and the industry’s broader shortage of leading-edge wafer and advanced packaging capacity.

Ecosystem readiness and the Cadence collaboration

The more immediate signal in the note is Intel’s intellectual property collaboration with Cadence Design Systems on the 14A node. For external designers considering Intel’s foundry, the availability of third-party design tools and verified IP blocks is a friction point that has historically kept customers on TSMC. The Cadence collaboration directly addresses that barrier, and BofA cites it as evidence that the ecosystem around Intel’s process nodes is becoming tool-chain ready for third-party adoption.

Intel’s Terafab-related capacity work provides further evidence that the foundry commitment is backed by physical infrastructure, not just strategic aspiration. IFS turns Intel from a single-product thesis into a dual-engine story; the $135 target requires both the CPU TAM expansion and the external wafer revenue to materialise.

The Terafab foundry partnership disclosed in SpaceX’s S-1 filing represents the most high-profile external validation Intel Foundry Services has received, with the $20 billion project targeting roughly 1 terawatt of annual compute hardware output, though Intel had not filed a Terafab-specific 8-K or disclosed associated revenue in its 10-Q as of May 2026.

STMicroelectronics: how BofA sees a cyclical stock hiding a structural business

STM is trading at a roughly 32% discount to diversified semiconductor peers on 2028 estimated EV/EBITDA. BofA’s €86 target (approximately $100) implies a valuation at approximately 13x 2028 EV/EBITDA, which is the upper end of STM’s historical range but still a double-digit percentage discount to diversified peers trading at approximately 14.8x. The question the note answers is whether that discount is earned or mistaken.

Scemama argues it is mistaken, and identifies three structural catalysts that the market’s cyclical framing fails to capture.

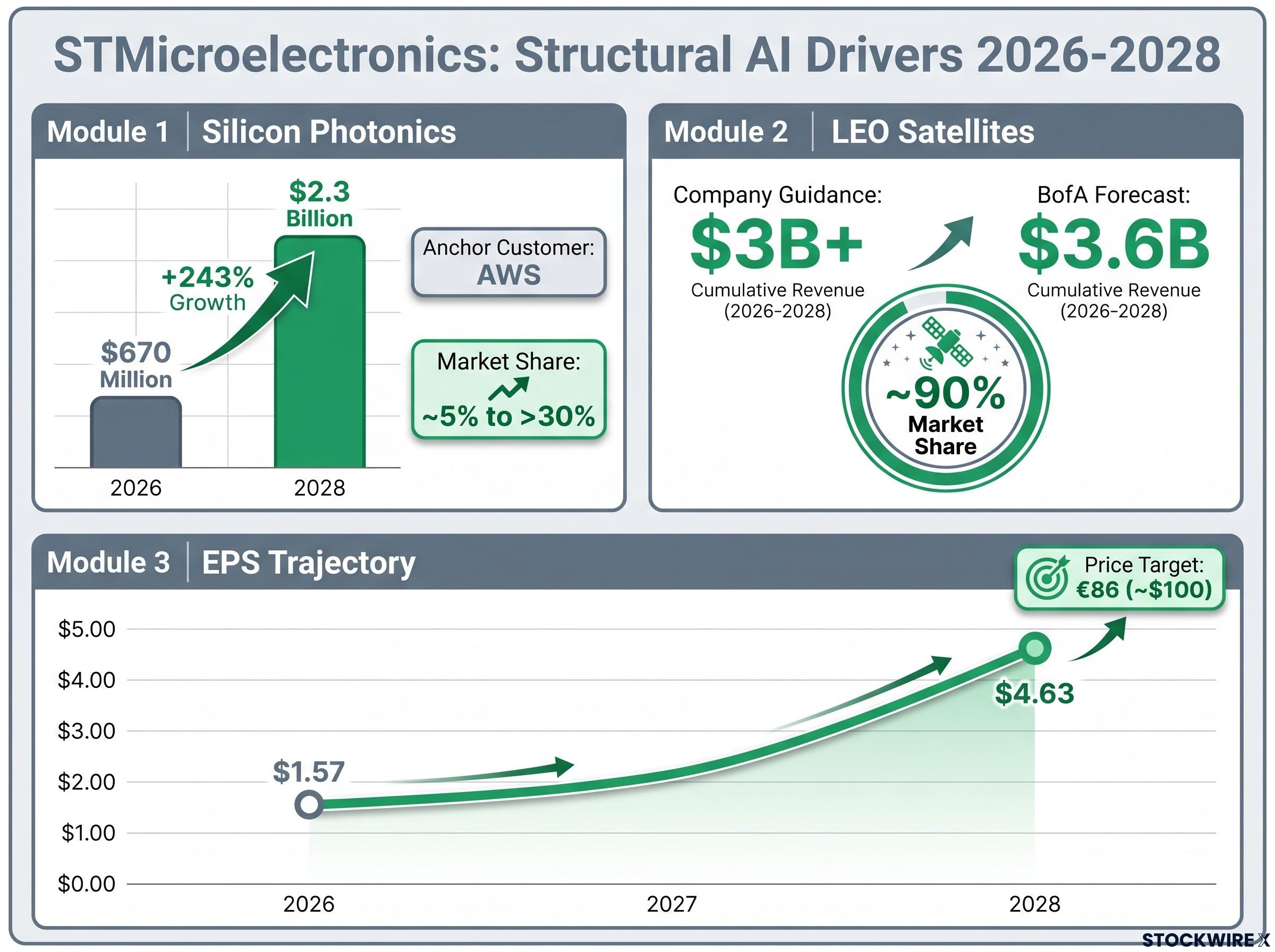

Silicon photonics is the first. STM manufactures silicon photonics components on 300mm wafers with advanced packaging technology, a capital-intensive and relatively scarce capability that supports optical modules for AI data centres. AWS is identified as the anchor customer. BofA models optical interconnect revenues growing from $670 million in 2026 to $2.3 billion by 2028, with STM’s market share expanding from approximately 5% to more than 30%.

STM currently holds approximately 90% market share in components for low-Earth orbit (LEO) satellites, according to BofA’s research.

LEO satellites are the second catalyst. Cumulative revenues are forecast at $3.6 billion between 2026 and 2028, ahead of the company’s own published guidance of $3 billion or more. The multi-year constellation build-out timeline offers earnings visibility that auto and industrial cycles do not.

BofA’s EPS estimates of $1.57 (2026), $3.53 (2027), and $4.63 (2028) run 30-43% above Street consensus. The automotive and industrial recovery provides upside, but the steepness of BofA’s earnings trajectory is driven primarily by operating leverage: spare capacity filling with higher-margin photonics and satellite volumes.

STM shares declined approximately 1.05% on the day of the note’s publication, suggesting the market has not yet accepted the structural reframing.

| Catalyst | Key metric | 2026 baseline | 2028 target |

|---|---|---|---|

| Silicon photonics | Revenue | $670M | $2.3B |

| LEO satellites | Cumulative revenue (2026-2028) | Company guidance: $3B+ | BofA forecast: $3.6B |

| EPS trajectory | Earnings per share | $1.57 (2026) | $4.63 (2028) |

What both calls share: how the AI infrastructure cycle is creating a second tier of semiconductor winners

Read together, the Intel and STM notes are not coincidental publications. They are expressions of a single analytical framework about where AI infrastructure value flows after the GPU-and-hyperscaler phase.

BofA’s thesis, stripped to its mechanics, applies three moves to both companies:

- Extend the valuation horizon to 2028-2030, pushing beyond the two-year forward estimates that dominate consensus modelling and capturing earnings power that shorter-horizon frameworks miss entirely.

- Raise the long-term EPS power estimate above consensus, by modelling specific demand drivers (agentic CPU workloads, silicon photonics, LEO satellites, foundry wins) that the Street has not yet embedded in its numbers.

- Apply a higher multiple justified by infrastructure-like growth characteristics, arguing that companies positioned in AI infrastructure supply chains deserve structural premiums rather than cyclical discounts.

The first wave of the AI trade rewarded GPU vendors and hyperscalers. BofA’s second-wave framing extends the value chain to CPU orchestration, optical interconnects, satellite communications backbones, and foundry capacity, treating these as infrastructure assets rather than commodity inputs.

BofA’s bullish sector posture on Intel and STM fits within a broader house view: semiconductor earnings revision momentum across the sector has exceeded 20% in 2026, driven by hyperscaler AI capex commitments that Savita Subramanian argued in a separate May 2026 note provide genuine fundamental support rather than speculative froth.

The operating leverage logic applies most directly to STM, where spare 300mm and specialty capacity fills with higher-margin silicon photonics and LEO volumes. The fixed-cost base means incremental volume drops through at high margins, which is the mechanical driver of BofA’s 30-43% EPS premium over consensus. For Intel, the leverage is more structural: the CPU’s expanding role in agentic architectures adds TAM without requiring a proportional increase in capital spending.

The degree of consensus divergence quantifies how far this reassessment has to run if BofA is right. Intel’s Street consensus sat in the low $90s at publication; BofA is at $135. STM’s consensus EPS estimates trail BofA’s by 30-43% across the 2026-2028 window. Both gaps are wide enough that meaningful convergence would drive significant share price movement.

The risks BofA is pricing but the Street is still discounting

BofA is not dismissing execution risk. The firm is judging that the upside from getting the thesis right outweighs the downside of execution slippage, given the current starting valuations. The specific dependencies are worth monitoring as checkpoints.

Intel execution dependencies

- 14A node delivery. The foundry thesis requires Intel to produce competitive yields on its 14A process node on schedule. The Cadence IP collaboration is the near-term signal to watch; delays or design-tool gaps would slow external customer adoption.

- External foundry wins. Apple M-series wafers, MediaTek TPU wafers, and ARM-based server designs represent the addressable pipeline. If these wins materialise more slowly than modelled, the IFS revenue contribution to the $6.24 EPS estimate compresses.

- Agentic AI architecture evolution. The CPU-as-orchestrator thesis depends on how agentic workloads develop over a five-year horizon, a timeframe long enough for architectural alternatives to emerge.

STMicroelectronics risk vectors

- Silicon photonics ramp pace. The expansion from approximately 5% to more than 30% market share is a measurable checkpoint for the $2.3 billion 2028 revenue forecast. Slower adoption or increased competition would directly affect the operating leverage thesis.

- Auto and industrial normalisation. If recovery in EV, ADAS, and factory-automation demand extends beyond 2028, the capacity utilisation ramp that drives BofA’s 30-43% EPS premium over consensus would take longer to materialise.

- LEO constellation delays. Satellite programme resizing or build-out postponements would reduce the visibility that distinguishes this revenue stream from cyclical end markets.

Investors wanting to pressure-test BofA’s structural optimism against the broader market debate will find our full explainer on AI bull market risk horizons useful; it examines Paul Tudor Jones’s 1-2 year runway estimate, the hyperscaler capex growth thresholds that matter most for semiconductor valuations, and the specific signals that would indicate the cycle is turning.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections referenced are subject to market conditions and various risk factors, and past performance does not guarantee future results.

Beyond Intel and STM: A New Era for Chip Valuations

Both upgrades are expressions of the same view: traditional semiconductor names are being valued on yesterday’s earnings power rather than a structurally expanded 2030 TAM. The quantitative measure of how far this reassessment has to run is the gap between BofA and consensus, $135 versus a Street in the low $90s for Intel, and EPS estimates 30-43% above consensus for STM across the next three years.

Whether the reassessment proves correct depends on specific, trackable signals. Intel’s 14A node progress and the pace of external foundry customer commitments will determine whether the dual-engine thesis holds. STM’s silicon photonics customer wins beyond AWS, and the cadence of LEO satellite revenue, will test whether the cyclical discount the market applies is a mispricing or an accurate reflection of risk.

BofA’s methodology here is repeatable: extend the horizon, model the second-order AI demand, apply a structural multiple. If the thesis is right, the Intel and STM calls may prove to be early entries in a broader rotation toward semiconductor names the market has not yet recognised as AI infrastructure.

—