Why Seeing Machines Trades Below 5p Despite EU Mandate Wins

31 mins ago

Australia’s two most popular ETF categories, global growth and domestic quality, are often positioned as competitors. In practice, BetaShares has built NDQ and AQLT to perform fundamentally different jobs within a single portfolio. Australian retail investors constructing long-term ETF portfolios face a structural problem: the ASX 200 is heavily concentrated in banks and resources, yet pure offshore exposure through Nasdaq-tracking funds introduces its own risks around valuation and currency. NDQ and AQLT represent two rules-based solutions to different parts of that problem. This analysis explains how each fund works at the methodology level, identifies the trade-offs each introduces, places them side by side in a structured comparison, and helps readers determine whether holding both makes portfolio construction sense.

The headline number is hard to ignore: total return since inception on 26 May 2015 has exceeded 655% before fees as of mid-2026. But the composition driving that return is more concentrated than the “100 holdings” label suggests. NDQ tracks the NASDAQ-100 Index, selecting the 100 largest non-financial companies listed on the Nasdaq, weighted by market capitalisation. A small group of mega-caps generates most of the performance.

The dominant holdings include:

These names sit across Information Technology, Consumer Discretionary and Communication Services, the three sectors that define NDQ’s return profile. Financial sector holdings are absent entirely; the NASDAQ-100 excludes financials by design. For Australian investors, NDQ is the most accessible single-trade route into the US technology ecosystem, spanning semiconductors, cloud computing, AI infrastructure and digital platforms.

All underlying assets in NDQ are priced in US dollars, and returns convert to AUD at the time of distribution or redemption. This means AUD weakness amplifies NDQ gains for Australian holders, while AUD strength compresses them. The fund is deliberately unhedged; this is a structural feature, not a hedging oversight. Investors who hold NDQ are making a simultaneous bet on US technology earnings and on the AUD/USD exchange rate, whether they recognise it or not.

Unhedged USD exposure is not a neutral position: HNDQ returned 40.2% versus NDQ’s 27.2% over the year to 29 May 2026, a 13-percentage-point gap produced entirely by AUD/USD appreciation rather than any difference in underlying holdings, which illustrates how significantly the currency decision can dominate the investment thesis for Australian holders of Nasdaq-tracking funds.

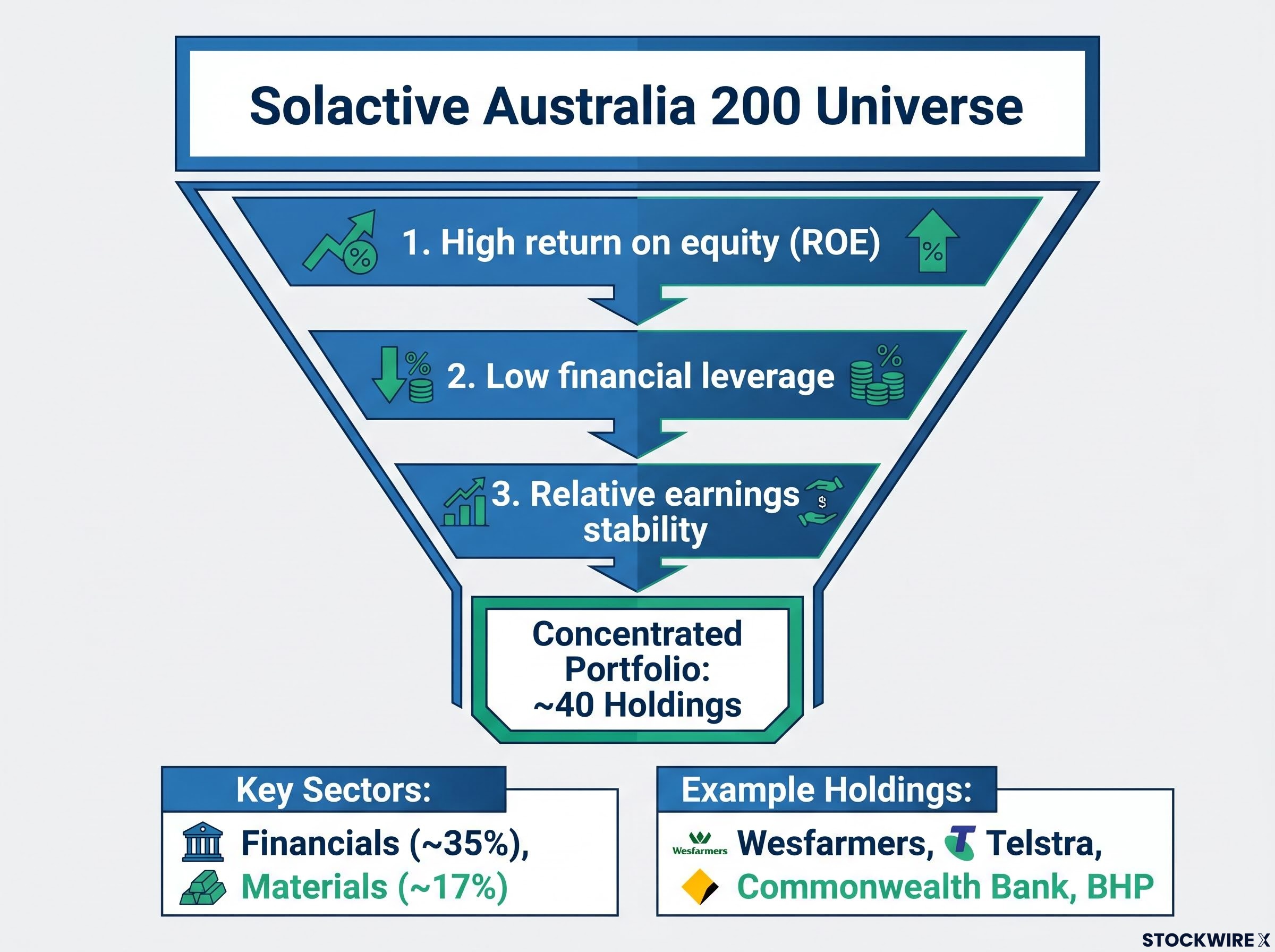

Start with the Solactive Australia 200 universe, the broad pool of Australian large- and mid-cap equities. Now apply three filters simultaneously, and watch the portfolio narrow.

The three quality selection criteria are:

The result is approximately 40 holdings, a concentrated portfolio that looks materially different from a standard ASX 200 index fund.

The sector composition tells the story of what the quality screen does in practice. Financials weighting sits at approximately 35%, and Materials at approximately 17% as of recent available data. Both sectors are present, but concentrated in higher-quality names. Top holdings typically include Wesfarmers, Telstra, Commonwealth Bank and BHP, though only where they pass the quality criteria.

Highly leveraged property names and speculative resources companies are likely screened out. This exclusion improves resilience in downturns but can cause AQLT to lag during cyclical rebounds, when lower-quality, higher-leverage names tend to rally hardest. That is the core quality-factor trade-off: consistency in exchange for underperformance during certain market phases.

AQLT is almost entirely AUD-denominated. There is no natural foreign-currency diversification benefit, which separates it sharply from NDQ’s USD exposure.

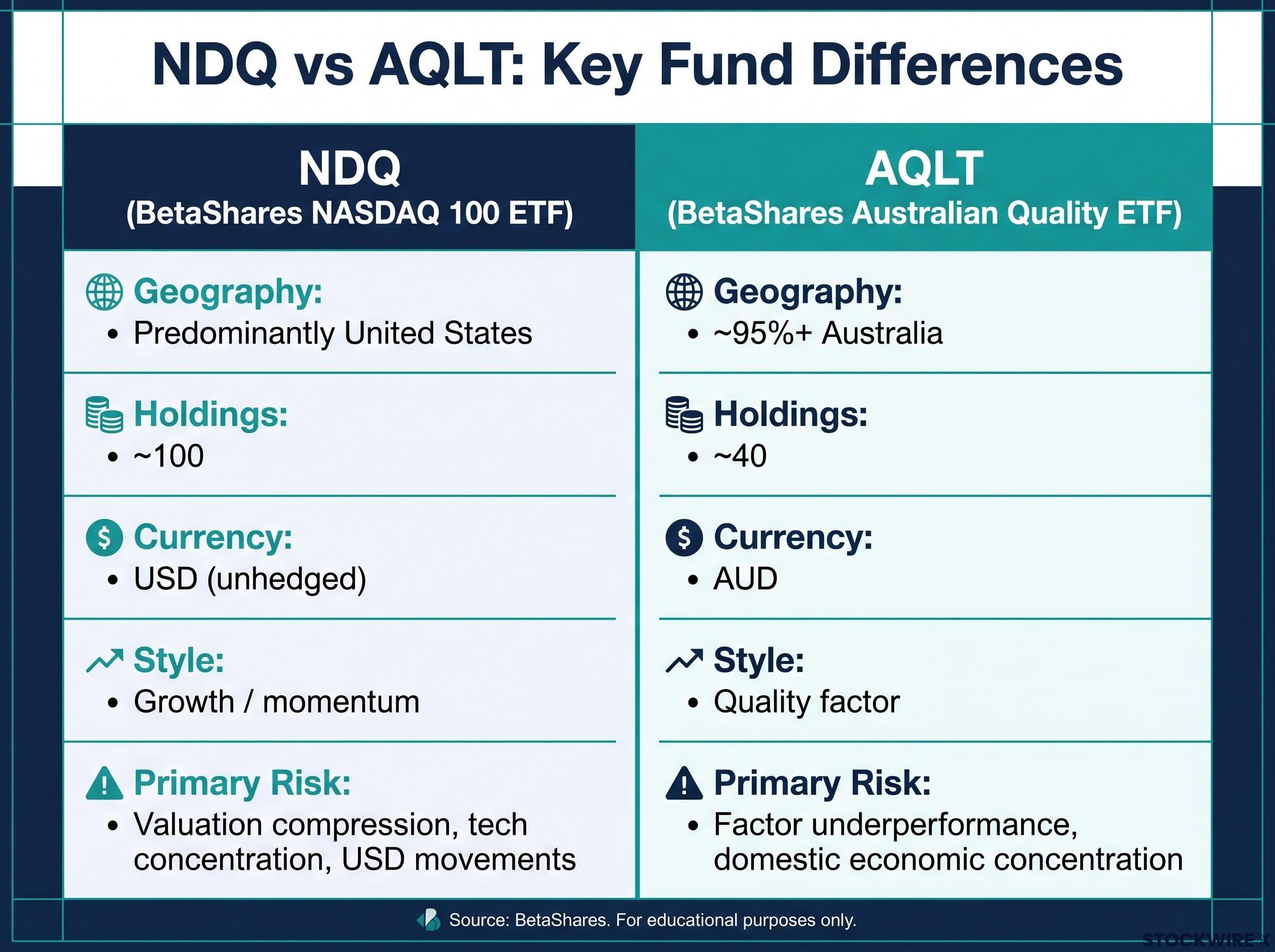

The two funds share an issuer and an ASX listing. Beyond that, the overlap is close to zero. The following comparison isolates the key dimensions where NDQ and AQLT diverge.

| Feature | NDQ | AQLT |

|---|---|---|

| Geography | Predominantly United States | ~95%+ Australia |

| Holdings count | ~100 | ~40 |

| Currency | USD (unhedged) | AUD |

| Style tilt | Growth / momentum | Quality factor (ROE, leverage, earnings stability) |

| Primary risk | Valuation compression, tech concentration, USD movements | Factor underperformance, domestic economic concentration |

NDQ’s return drivers, including US technology earnings, global innovation cycles and AUD/USD movements, share almost no common factor with AQLT’s return drivers, which centre on Australian corporate profitability, domestic demand and quality-factor behaviour. This near-zero overlap is what makes the two funds complementary rather than competing.

The comparison reframes the question. It is not “which one?” but “in what proportion?”

A standard Australian equity portfolio carries structural concentration. Banks and resources dominate the ASX 200, tying returns to credit conditions and commodity prices. Adding pure Nasdaq exposure solves the geographic gap but creates a new concentration problem: US technology valuations and currency volatility.

ASX 200 concentration risk is more pronounced than its 200-stock label implies, with financials and materials together accounting for more than 50% of the index by market-cap weight, a structural feature that persists across market cycles and shapes the return profile of any Australian investor who holds a standard domestic index fund.

NDQ fills the gap that AQLT cannot. It delivers offshore, USD-denominated, innovation-driven growth that is absent from domestic equity exposure. AQLT fills the gap that NDQ cannot. It provides a quality-tilted domestic allocation with reduced cyclicality and AUD-denominated resilience.

A common implementation follows three layers:

NDQ and AQLT operate under different risk regimes. NDQ is sensitive to US interest rate expectations and tech sector sentiment. AQLT is sensitive to Australian economic conditions and quality-factor cycles.

Periods when one underperforms are not necessarily correlated with periods when the other does. NDQ’s USD exposure can act as a natural portfolio hedge in risk-off scenarios, when the AUD typically weakens at the same time Australian equities fall. This partial independence is the mechanism behind the diversification benefit; it distributes risk across regions, currencies and factors rather than concentrating it.

The quality factor is a systematic preference for companies with three characteristics: high profitability, conservative balance sheets and stable earnings. It is not a subjective label. It is a rules-based filter applied to a universe of stocks, and the companies that pass look meaningfully different from those that do not.

AQLT’s index applies three specific quality metrics:

The quality screen favours companies less exposed to commodity cycles, credit stress and earnings volatility. The result is a portfolio that behaves differently from the broad ASX 200, particularly during periods of market stress.

Historically, quality strategies have added value over full market cycles. AQLT reported outperformance versus the ASX 200 in FY25, providing a recent concrete example. The catch is timing. During strong cyclical rebounds and speculative rallies, lower-quality, higher-leverage names tend to outperform as capital chases risk. Quality strategies can lag meaningfully in these phases.

This is not a flaw in the strategy. It is the nature of factor investing. Investors who do not understand this cycle risk selling a quality-tilted fund precisely when it is most likely to recover, a common and costly behavioural mistake.

For investors new to factor-based ETF construction, our dedicated guide to quality investing strategy covers how ROE, leverage, and earnings stability screens are applied in practice, how current valuation conditions as of April 2026 have made quality-factor entry points more attractive, and how AQLT compares with the other ASX-listed quality ETFs available to Australian investors.

Fund selection is ultimately about matching characteristics to personal circumstances. Performance over the past year is the least reliable input for that decision.

NDQ may suit investors who:

AQLT may suit investors who:

Holding both may suit investors who:

Both funds are rules-based and carry risk of capital loss. Investors should review each fund’s Product Disclosure Statement (PDS) and consider consulting a licensed financial adviser before making allocation decisions.

ASIC Regulatory Guide 282 governs exchange-traded product issuers in Australia, setting out portfolio disclosure requirements and Product Disclosure Statement obligations that apply to funds like NDQ and AQLT, giving retail investors a standardised basis for comparing fund characteristics before committing capital.

NDQ and AQLT are not alternatives to each other. They address different portfolio deficits simultaneously: NDQ provides the offshore, growth-driven, USD-denominated exposure that Australian portfolios structurally lack, while AQLT upgrades the quality profile of the domestic allocation that most Australian investors already hold.

The trade-offs do not disappear in combination. Holding both does not eliminate valuation risk, currency risk or factor-cycle risk. It distributes those risks across different sources, which is a meaningfully different proposition from concentrating them in a single instrument.

The practical next steps are straightforward: review each fund’s PDS on the BetaShares website, map each fund’s characteristics against existing portfolio exposures, and consider speaking with a licensed financial adviser before making allocation decisions.

For investors ready to implement the three-layer framework, our comprehensive walkthrough of ETF portfolio construction covers how to determine the right allocation split between core and satellite positions, why keeping the total fund count to 2-6 minimises fee drag and tax administration complexity, and how to map existing superannuation holdings against a new ASX-listed ETF allocation before adding NDQ or AQLT.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

NDQ tracks the NASDAQ-100 Index and provides unhedged USD exposure to approximately 100 large US technology and innovation companies, while AQLT applies a quality screen to Australian equities, selecting around 40 AUD-denominated companies with high ROE, low leverage and stable earnings.

AQLT selects stocks from the Solactive Australia 200 universe using three criteria: high return on equity, low financial leverage, and relative earnings stability, which together tend to exclude speculative, highly leveraged and cyclically volatile companies.

Because NDQ is unhedged, returns convert from USD to AUD at redemption or distribution, meaning a strengthening AUD compresses NDQ gains for Australian holders and a weakening AUD amplifies them; over the year to 29 May 2026, this currency effect alone created a 13-percentage-point return gap between NDQ and its hedged equivalent HNDQ.

Yes, and the article argues they are complementary rather than competing: NDQ fills the offshore, growth-driven, USD-denominated gap that domestic Australian ETFs cannot address, while AQLT upgrades the quality profile of the domestic allocation, with the two funds sharing near-zero factor overlap.

Quality strategies like AQLT tend to lag during strong cyclical rebounds and speculative rallies, when lower-quality, higher-leverage names attract capital chasing risk; this is a known feature of factor investing rather than a flaw, and AQLT reported outperformance versus the ASX 200 in FY25 over a full cycle.