The SpaceX IPO Was a Stress Test for Space Stocks, Not a Catalyst

43 mins ago

SpaceX raised $75 billion on 12 June 2026 at a $1.75 trillion valuation, making it the largest initial public offering in history. Morningstar analysts, however, have estimated the company’s intrinsic value at roughly half that figure, approximately $780 billion. The company was losing money at the operating level when it went public. For retail investors deciding today whether to buy SPCX on its first trading day, the question is not whether SpaceX is an extraordinary company. It is whether an extraordinary company at this price, with this governance structure, and this much of its value resting on technology that does not yet exist, represents a rational use of their capital. What follows is a section-by-section breakdown of the offering mechanics, the valuation gap, the governance risks, and a practical framework for determining whether and how much exposure makes sense in a diversified portfolio.

The headline figures are striking:

That last number is the one that matters most. The $75 billion bought the public a sliver. Elon Musk retained roughly 42% of company equity prior to dilution, and the vast majority of remaining ownership stayed with pre-IPO private investors. On its debut, SpaceX surpassed Tesla to become the eighth-largest U.S. company by market capitalisation.

“SpaceX’s market cap on debut surpassed Tesla’s, yet by revenue, SpaceX does not rank among the top 200 U.S. companies.”

A 4.2% float on a $1.75 trillion company means the daily price is being set by a fraction of total shares. Fewer shares absorbing buy and sell pressure amplifies moves in both directions. The stock is structurally more volatile than a typical mega-cap with broad ownership, and it will remain so until insider lockups begin expiring and supply widens.

SpaceX reserved up to approximately 30% of IPO shares for retail investors. The industry norm for U.S. listings sits between 5% and 10%. That is not a rounding difference; it is a deliberate structural decision.

The company launched a dedicated retail portal, SpaceXipo.com, offering prospectus materials and roadshow access typically reserved for institutions. Major brokers offering IPO allocation include:

Fidelity lowered its minimum investment threshold from $500,000 to $2,000 specifically for this offering, the single most aggressive barrier reduction in the deal.

| Metric | SpaceX IPO | Industry Norm |

|---|---|---|

| Retail allocation | ~30% | 5-10% |

| Fidelity minimum threshold | $2,000 | $500,000 |

The accessibility is real. So is the trade-off. SpaceX’s own prospectus acknowledged the risk directly:

Higher retail investor concentration increases the stock’s susceptibility to price volatility.

That disclosure is worth reading twice. The company distributing a historically large retail allocation simultaneously warned, in its own filing, that the resulting ownership structure could make the stock more volatile. Lower barriers may serve retail investors. They also serve a company that needs broad distribution to support a $1.75 trillion valuation on a 4.2% float.

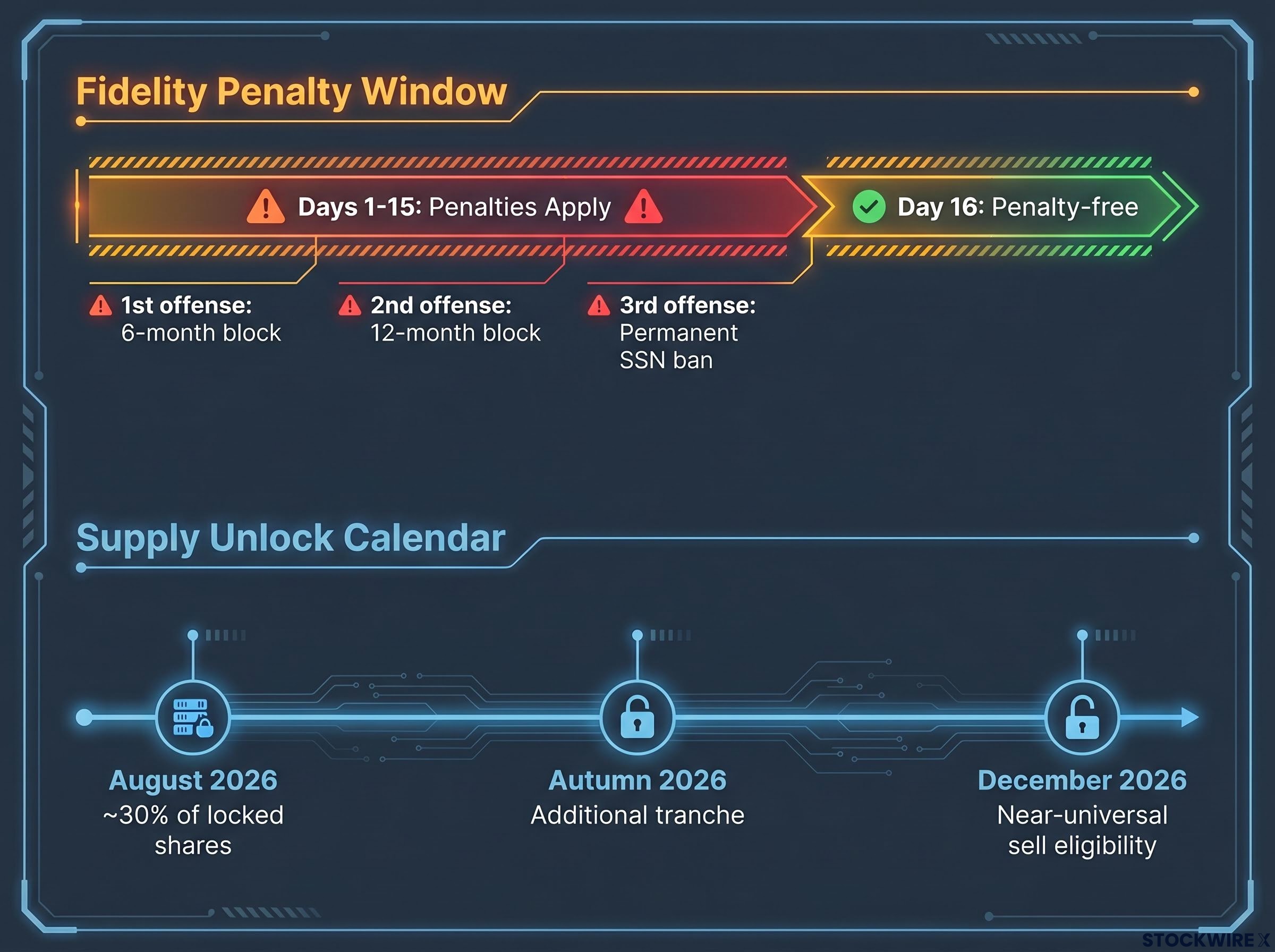

Less than 5% of SpaceX’s total float is freely tradable today. That number shapes everything about the first six months of SPCX’s life as a public stock.

A lockup is a contractual restriction preventing insiders, employees, and early investors from selling their shares for a set period after an IPO. It exists to prevent a flood of supply from crashing the price on day one, but it also means the current price is being set in an artificially constrained market.

| Approximate Date | Unlock Event | Estimated Share Release |

|---|---|---|

| August 2026 | First earnings report | Up to ~30% of locked shares |

| Autumn 2026 | Second earnings / additional tranche | Further significant release |

| December 2026 | Near-universal sell eligibility | “Almost everyone except Elon” can sell |

Nearly $1 billion in insider shares are projected to become available for sale within months. Each unlock event creates a potential wave of new supply meeting existing demand.

Retail investors who received IPO shares through Fidelity face a specific constraint. Selling within 15 calendar days of the IPO triggers escalating penalties:

Day 16 after the IPO is the first penalty-free sell day at Fidelity. This creates a predictable behavioural pattern: retail selling pressure is likely suppressed for the first two weeks, then may increase as that window closes. Sophisticated participants will anticipate this dynamic.

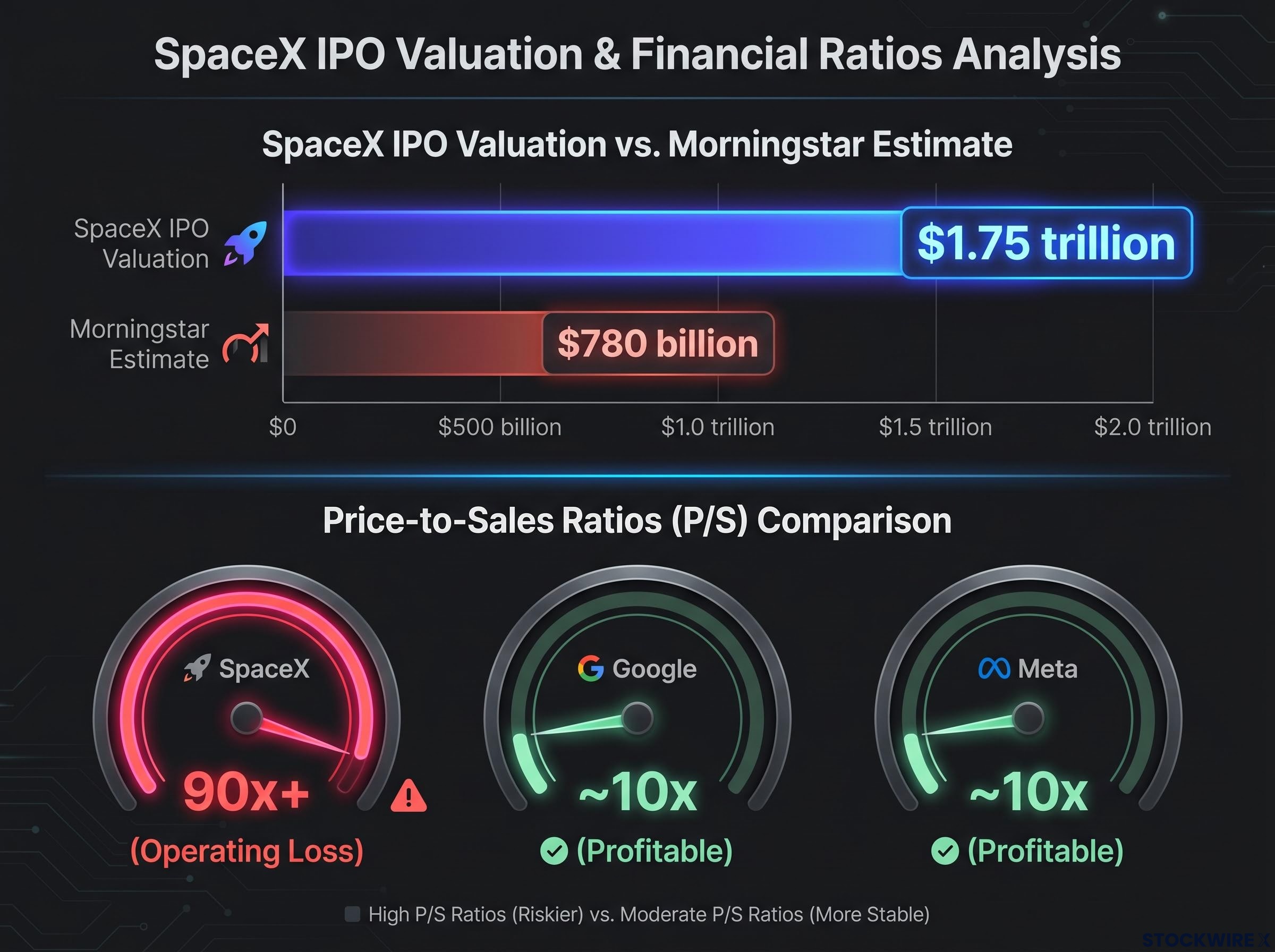

Morningstar analysts estimated SpaceX’s intrinsic value at approximately $780 billion, based on current business performance. The IPO priced the company at $1.75 trillion. The gap between the two figures is not a rounding error; it is more than $900 billion.

Morningstar’s fair-value estimate sits at roughly $780 billion, implying the IPO price carries a premium exceeding 100% over estimated intrinsic value.

Put another way, buyers at $135 per share need to believe in a future that roughly doubles the value that current operations support.

| Company | Price-to-Sales Ratio | Profitable at IPO? | Revenue Growth (YoY) |

|---|---|---|---|

| SpaceX | 90x+ | No (operating loss) | 15.4% |

| ~10x | Yes | N/A (established) | |

| Meta | ~10x | Yes | N/A (established) |

The thesis bridging that gap rests heavily on artificial intelligence. SpaceX’s prospectus attributed 93% of its stated total addressable market to AI opportunities, including enterprise applications. Yet the AI segment recorded revenue growth of just 12.5% year-over-year, which was not even the company’s fastest-growing internal division. The company leases compute capacity to Anthropic at $1.25 billion monthly and to Google at $920 million monthly, a detail that complicates claims of AI dominance: if its own AI were competitive at scale, leasing capacity to rival firms would be an unusual strategy.

The prospectus itself disclosed that speculative future business lines included:

Several of these involve technology the prospectus acknowledged does not yet exist. At 90x price-to-sales with operating losses, the investor’s entire return rests on execution against those future lines. If sentiment shifts toward fundamentals, Morningstar’s estimate implies a potential drawdown of 50% or more from today’s price.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Elon Musk holds 85% of voting rights over SpaceX through a special share class carrying 10 times the voting power of standard Class A shares. Public shareholders cannot meaningfully challenge company decisions regardless of how many shares they collectively own.

“85% voting rights means public shareholders have minimal ability to influence company decisions regardless of how many shares they collectively own.”

The New York Times examined 602 goals Musk has set over several decades:

This track record is directly relevant to investors whose thesis depends on long-term vision being executed. Musk previously projected a fleet of one million robotaxis operating by 2020 and predicted SpaceX would reach Mars by 2025 at the latest.

Index providers Nasdaq and FTSE Russell reportedly eased their criteria for index inclusion at Musk’s request. According to unconfirmed reports, the Russell 1000 could add SPCX within its first 5 trading days, and the Nasdaq-100 within 15 days. If confirmed, this would represent an unprecedented timeline.

The implication is direct: index funds and target-date retirement funds tracking those benchmarks would be required to purchase SPCX shares, putting the stock into millions of portfolios automatically. Investors who never explicitly chose SpaceX may end up owning it through their passive allocations.

Rather than a verdict, what follows is a framework for stress-testing whether this position fits a specific portfolio.

“If your thesis relies primarily on SpaceX’s long-term vision, treat this as high-risk capital from the start.”

Consider starting small and scaling over time rather than committing a lump sum at IPO-adjacent prices. Revisit the thesis against actual earnings, cash flow, and business developments as they arrive.

SpaceX is a genuinely extraordinary company that has made itself historically accessible to retail investors. It is also priced at a $1.75 trillion valuation against a Morningstar estimate of roughly $780 billion, governed by a structure that gives public shareholders no meaningful influence, and trading today on less than 5% of total float with supply unlocks running through December.

A small satellite position could be rational for investors with:

Investors who should pause include:

Passive investors may already be gaining SPCX exposure through index funds if inclusion proceeds on the reported timeline. That indirect allocation is a legitimate substitute for a direct position, and it avoids the governance and concentration risks of a standalone holding.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

SpaceX priced its IPO at $135 per share on 12 June 2026, implying a market capitalisation of approximately $1.75 trillion and raising $75 billion in total proceeds, the largest IPO in history.

Approximately 30% of IPO shares were reserved for retail investors, far above the industry norm of 5-10%, and the public float represents roughly 4.2% of total company equity.

SpaceX insider lockups are set to expire in stages through December 2026, with the first significant unlock projected around August 2026, potentially releasing nearly $1 billion in insider shares into the market.

Morningstar estimates SpaceX's intrinsic value at approximately $780 billion based on current business performance, less than half the $1.75 trillion IPO valuation, because the higher price requires executing on speculative future business lines that do not yet exist.

Retail investors who received SpaceX IPO shares through Fidelity and sell within 15 calendar days face escalating penalties, starting with a 6-month ban from equity IPO participation, rising to a permanent ban after a third offence.