US Inflation at 4.2%: a War, Not an Overheating Economy

Jun 10, 2026

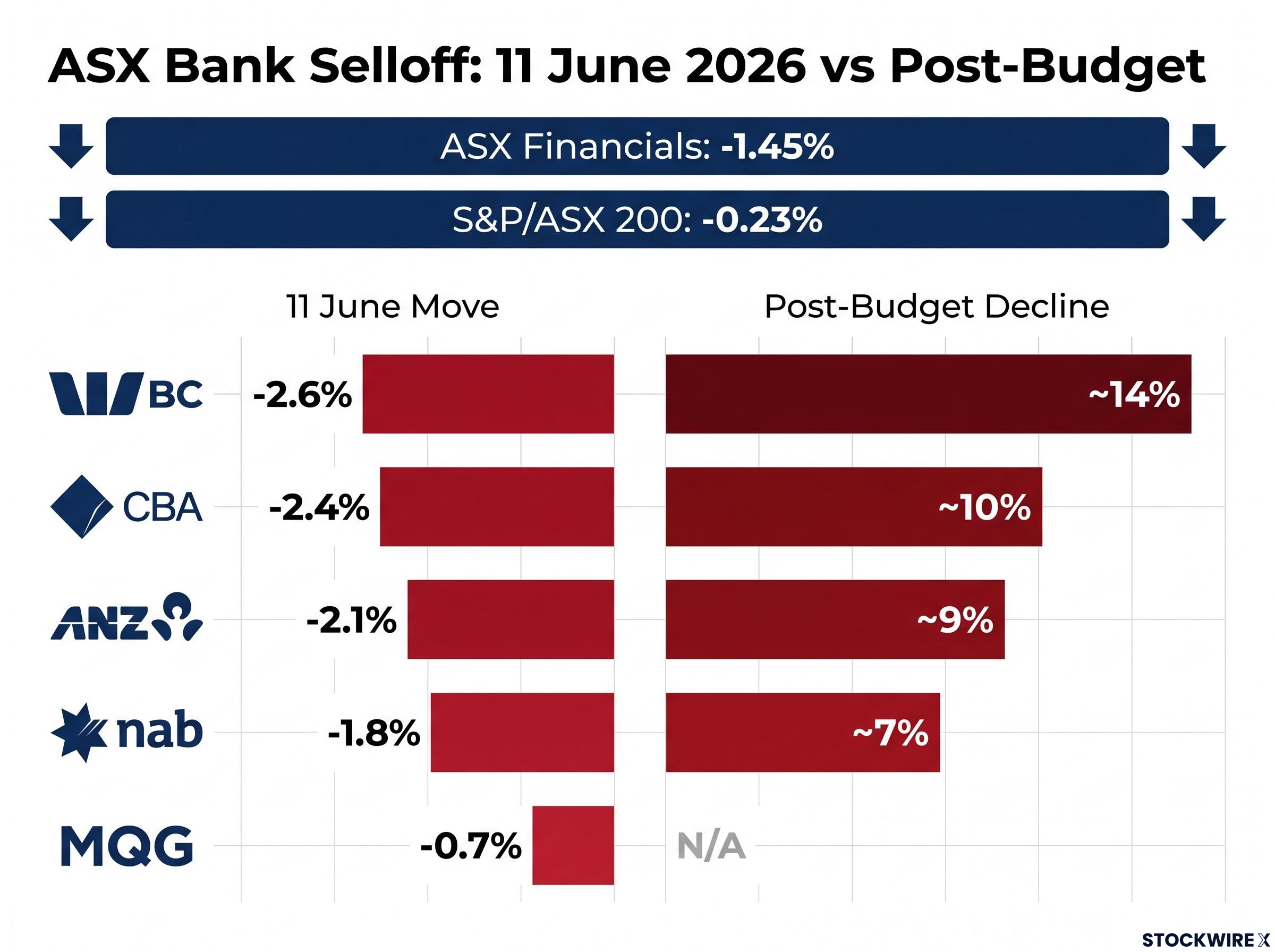

The ASX Financials sector fell 1.45% on 11 June 2026 while the broader S&P/ASX 200 slipped just 0.23%, a gap wide enough to confirm that a single bad session for ASX bank stocks is part of something more persistent. The big four have been losing ground since the May 2026 Federal Budget introduced property-tax reform proposals that strike directly at the mortgage-lending engine underpinning their earnings. Renewed short-selling activity reported on 10 June added fresh downward pressure heading into the session, and the result was the sharpest single-day divergence between financials and the headline index in weeks.

What follows breaks down exactly how far Commonwealth Bank of Australia (CBA), Westpac (WBC), ANZ, and National Australia Bank (NAB) fell on 11 June, why the Budget’s property measures are compressing bank valuations, how elevated short positioning is amplifying the moves, and what investors holding or watching these names should monitor from here.

Westpac led the decline, falling 2.6% on the session. CBA dropped 2.4%, ANZ shed 2.1%, and NAB lost 1.8%. Macquarie Group (MQG), less exposed to residential lending, declined a comparatively modest 0.7%.

The S&P/ASX 200 closed at 8,633.2, finishing 0.9% above its intraday low and just 0.4% below its session peak. Mining stocks staged a partial recovery during the afternoon, pulling the headline number back from worse levels. Financials did not participate in that bounce.

That distinction matters. Investors who track only the ASX 200 may see a 0.23% decline and assume a quiet session. The XFJ’s 1.45% drop tells a different story, and the cumulative damage since the 12 May 2026 Budget is sharper still.

| Bank | 11 June 2026 Move | Approx. Decline Since May Budget |

|---|---|---|

| Westpac (WBC) | -2.6% | ~14% |

| CBA | -2.4% | ~10% |

| ANZ | -2.1% | ~9% |

| NAB | -1.8% | ~7% |

| MQG | -0.7% | N/A |

Bank-heavy portfolios have absorbed considerably more pain than the headline index suggests. The divergence is the starting point for understanding what is actually happening beneath the surface.

Media coverage on 10 June 2026 flagged increased short-selling positions being built against the major banks, contributing to the selling pressure that intensified on 11 June. The XFJ’s 1.45% decline against the ASX 200’s 0.23% move is consistent with bearish institutional positioning layered on top of the fundamental headwinds already weighing on the sector.

Short-selling amplifies downside in weak sessions. It does not, however, create a one-directional trade. The same elevated positioning that pushes prices lower also creates the conditions for sharp recoveries if the catalyst changes. A policy revision, stronger-than-expected mortgage data, or a legislative delay could trigger short covering that produces an outsized rally.

Short-selling mechanics mean elevated bearish positioning functions as a two-sided lever: the same concentration of borrowed-share positions that accelerates selling pressure in weak sessions creates the latent fuel for sharp recoveries when covering demand arrives suddenly.

Two signals are worth monitoring:

Investors watching ASX bank stocks need to understand this dynamic because it changes the interpretation of both down days and up days. The positioning itself is informative about where institutional money is currently placed.

Short interest as an early warning system carries a four-business-day publication lag under ASIC reporting rules, meaning institutional positioning in the major banks is already established by the time retail investors can read the disclosed figures, reinforcing why the monitoring signals in this article matter more than waiting for the next published short position update.

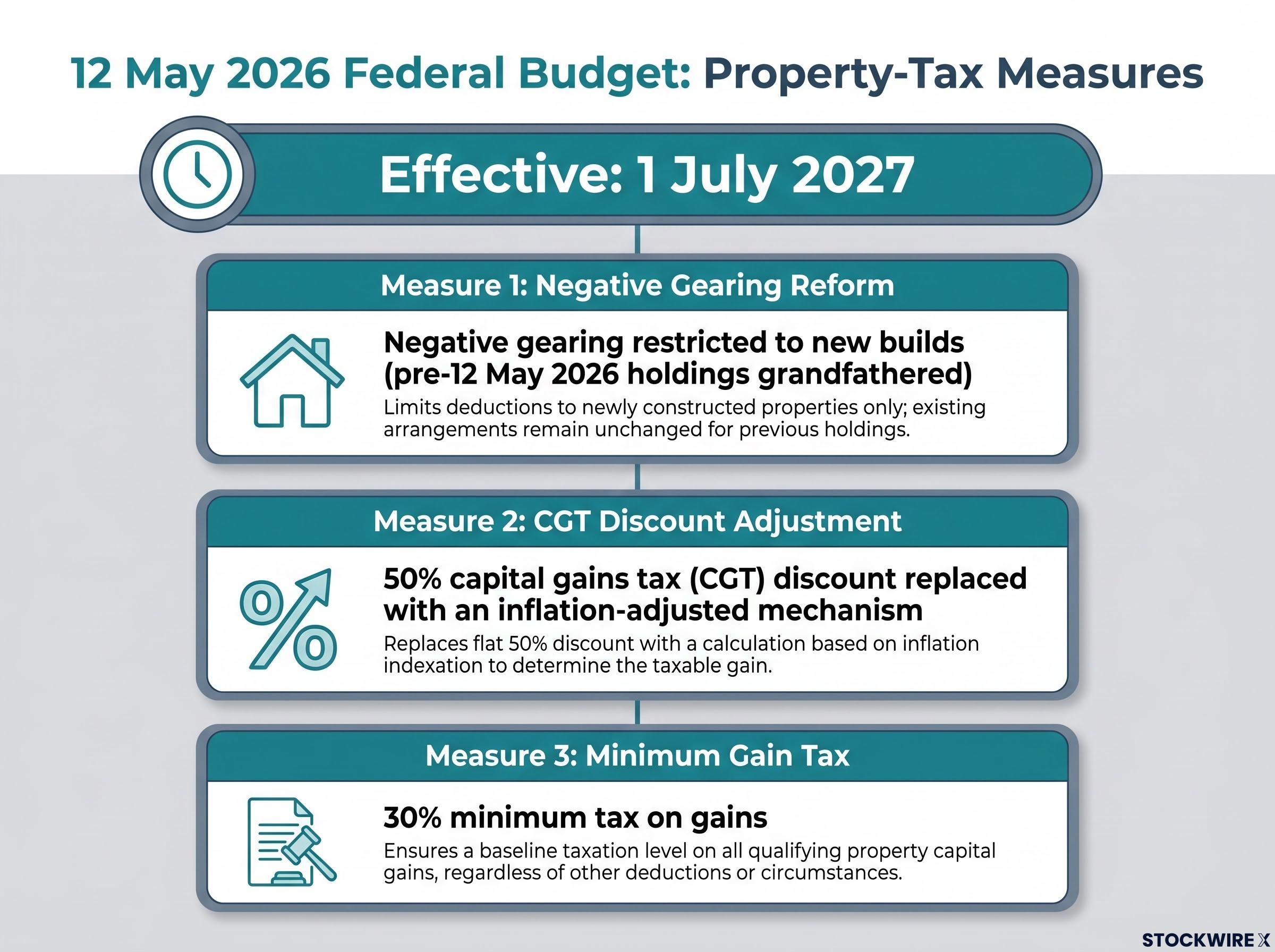

The 12 May 2026 Federal Budget contained three property-tax measures that collectively raised the effective cost of owning and transacting in investment property. Markets began repricing bank earnings expectations from announcement day, well before any legislative implementation.

The Budget packaged three investor tax reforms with a combined $77 billion revenue impact over the decade, covering capital gains treatment, negative gearing eligibility, and discretionary trust distributions, each with distinct grandfathering cut-offs that determine which existing positions remain protected.

The Australian Federal Budget 2026 property tax factsheet confirms the 1 July 2027 implementation date for all three measures, specifying that negative gearing deductibility will be restricted to new builds, the 50% CGT discount will be replaced with a cost-base indexation mechanism, and a 30% minimum tax rate on capital gains will apply to investment property held beyond that date.

The three measures:

The negative gearing restriction is the measure carrying the most weight in bank-sector repricing. By limiting tax deductibility on existing property investment, the proposal reduces the after-tax return on leveraged residential holdings, which directly softens demand for the mortgage products that drive big four revenue.

The mechanism linking these changes to bank earnings is straightforward. Policies that raise the cost of investment property ownership reduce transaction volumes, soften new mortgage demand, and put marginal pressure on residential valuations as investor-seller supply increases. None of these changes have been enacted yet, but markets price risk in advance. Understanding the specific policy mechanics helps investors separate structural headwinds from sentiment-driven overreaction.

Australia’s big four are among the most mortgage-concentrated large banks globally. Residential lending forms the core of each major’s loan book, meaning their earnings are directly tied to property market conditions in a way that more diversified financial institutions are not.

When policy changes raise the effective cost of investment property ownership, three things tend to follow: transaction volumes fall, new mortgage demand softens, and property values face pressure as investor-sellers add supply. Each of those outcomes compresses the revenue and growth outlook for lenders whose primary business is writing home loans.

Investor return modelling under the new framework requires running both a reform-proceeds and a reform-fails scenario, given that neither the negative gearing restriction nor the CGT discount replacement had been tabled as legislation as of late May 2026, meaning the probability-weighted impact on residential transaction volumes remains genuinely uncertain.

This is not a theoretical risk. Westpac has disclosed a measurable decline in home-loan application volumes.

Westpac’s mortgage applications fell from approximately 33,000 to 30,000 per month in fiscal Q3. A broader measure shows volumes down approximately 18% since late 2025, with investor loan applications declining roughly 20% in the weeks following the Budget announcement.

That data provides a concrete anchor for the abstract mechanism. If the bank with the earliest disclosed application data is already seeing double-digit percentage declines in investor mortgage demand, the read-across to CBA, ANZ, and NAB is direct. The framework matters beyond today’s price moves: any future news about property volumes or mortgage growth feeds into the same structural link between housing market health and bank earnings.

The forward picture depends on three observable categories. Rather than predicting outcomes, the following framework allows investors to make their own informed assessments as events unfold.

The 1 July 2027 implementation date for negative gearing and CGT changes remains the anchor. Parliamentary negotiations, any Treasury clarifications on scope and timing, and any indication that proposals may be revised, delayed, or blocked would materially shift the risk premium currently embedded in bank valuations.

Upcoming trading updates will carry outsized importance. The specific numbers to track:

The relative performance of financials versus resources serves as a real-time sector-sentiment proxy. Some equity strategists are already recommending a tilt toward resources and away from banks, reflecting the comparative absence of property-tax and regulatory headwinds in the mining sector.

Offshore sentiment at the Australian close on 11 June was more constructive, with S&P 500 futures at 7,318.5 (+0.55%) and Dow Jones futures at 50,205.0 (+0.43%). That backdrop may temper further downside in subsequent sessions, though domestic headwinds remain the primary driver of bank-specific weakness.

The structural case for Australian major banks has not collapsed. Oligopolistic market structure, strong capital positions, and historically reliable dividends remain in place. These are attributes that have supported the sector through multiple prior cycles and continue to underpin income-oriented allocations.

What has changed is the policy sensitivity the sector now carries. The current environment introduces more regulatory and tax uncertainty than the big four have faced in recent prior periods. Moderate growth and periodic valuation shocks are more likely than a return to the strong-run conditions that characterised the sector before the Budget.

The 7-14% post-Budget decline range indicates the market has already done significant repricing. Whether that repricing is sufficient depends on the single most important variable still in play.

The final legislative form of the property-tax changes has not yet been determined. The full risk is not yet crystallised, and clarity on the enacted legislation remains the most significant catalyst that could shift the sector’s risk premium in either direction.

Because the big four represent a substantial share of ASX 200 market capitalisation, their sustained underperformance materially caps index-level gains. For long-term and income-oriented investors, the task is a clear-eyed assessment of what has changed and what has not, without being pushed toward a conclusion the evidence does not yet support.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Forward-looking statements regarding legislative outcomes and bank earnings are speculative and subject to change based on market developments and policy decisions.

The ASX Financials sector dropped 1.45% while the S&P/ASX 200 fell just 0.23%, a gap driven by property-tax reform proposals in the May 2026 Federal Budget targeting the mortgage-lending businesses that underpin big four bank earnings, compounded by a surge in short-selling activity reported on 10 June.

The May 2026 Budget introduced three measures effective 1 July 2027: restricting negative gearing deductions to new builds, replacing the 50% CGT discount with a cost-base indexation mechanism, and imposing a 30% minimum tax on investment property gains. These reforms raise the effective cost of investment property ownership, which reduces mortgage demand and transaction volumes, directly compressing revenue growth for Australia's big four banks.

Since the 12 May 2026 Budget announcement, Westpac has declined approximately 14%, CBA around 10%, ANZ roughly 9%, and NAB about 7%, reflecting sustained market repricing of bank earnings expectations ahead of any legislative implementation.

Short-selling involves borrowing shares and selling them with the aim of buying them back at a lower price, profiting from the decline. Elevated short positioning in ASX bank stocks amplifies downward moves in weak sessions but also creates the conditions for sharp recoveries if positive news triggers covering demand, making it a two-sided factor for investors to monitor.

Investors should monitor net interest margin trends, mortgage application and approval volumes (Westpac has already disclosed an approximately 18% decline since late 2025), arrears and impairment data in residential portfolios, and any parliamentary developments regarding the 1 July 2027 legislative implementation timeline.