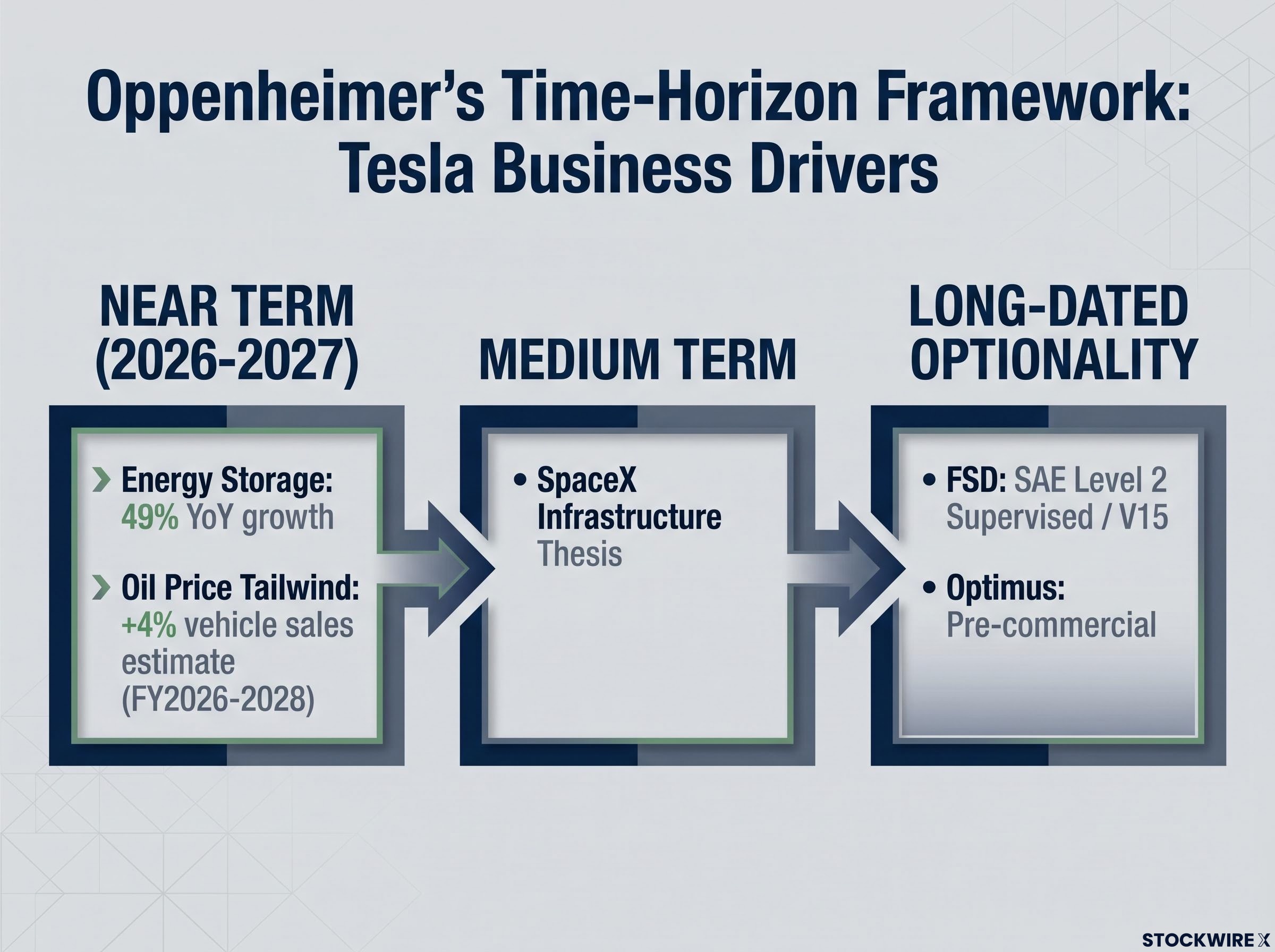

Oppenheimer has quietly shifted its near-term Tesla thesis away from self-driving cars and humanoid robots, redirecting analytical attention to a business line growing 49% year over year that most retail investors barely track. In mid-2026, most Tesla coverage remains dominated by Full Self-Driving (FSD) milestones and Optimus timelines. But Oppenheimer’s recent framework argues the more actionable 2026-2027 upside lives in stationary energy storage, a macro oil price tailwind boosting EV economics, and an emerging supply chain relationship with SpaceX that has not been fully priced by the market. What follows breaks down each component of that thesis, distinguishes what is quantifiable from what remains qualitative, and gives investors a time-horizon framework for evaluating which parts of Tesla’s business are doing the analytical work right now.

Tesla’s fastest-growing business is not what most investors are watching

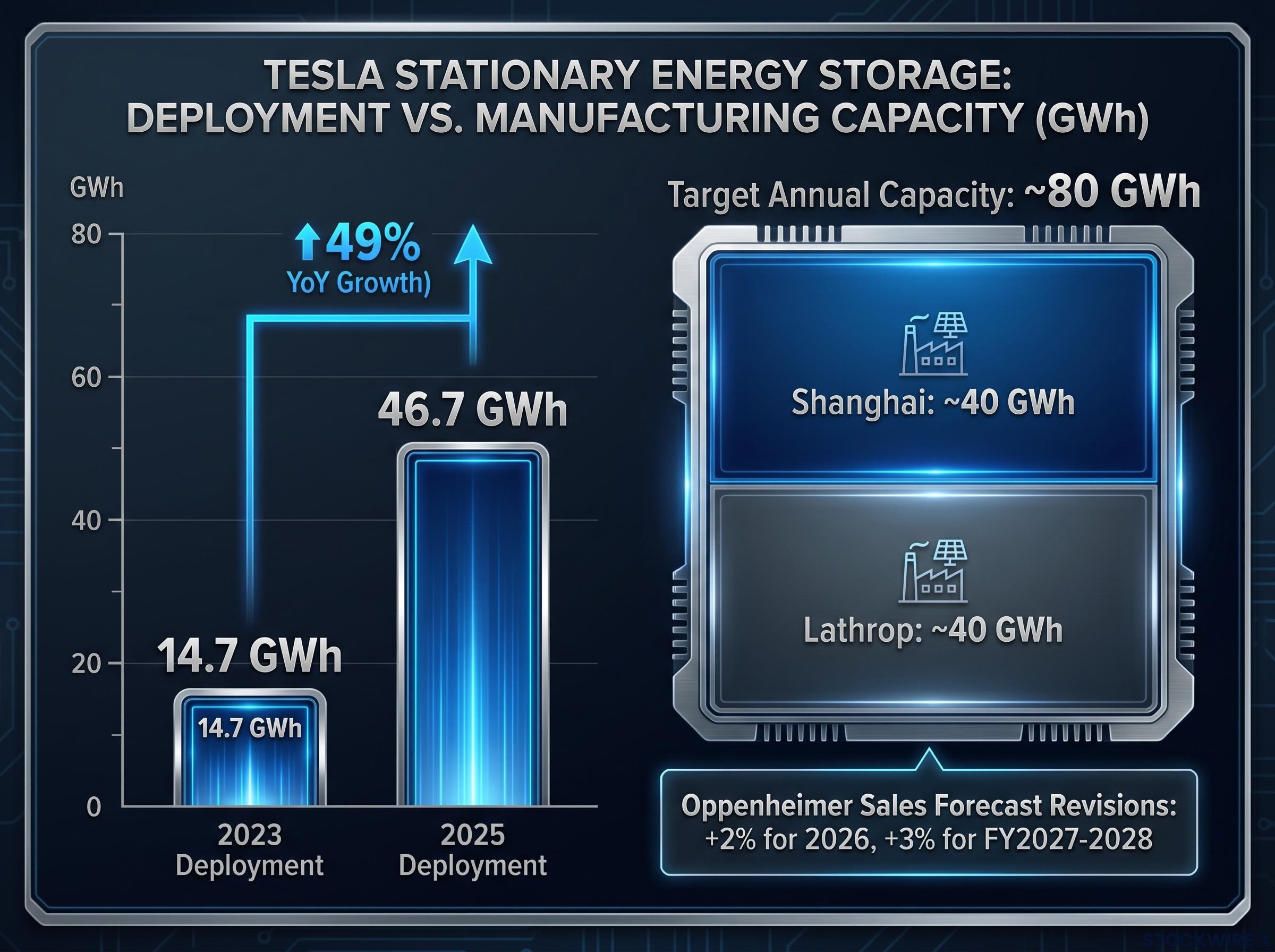

Tesla deployed 46.7 GWh of stationary energy storage in 2025, up 49% year over year. For context, the company deployed 14.7 GWh in 2023. That is a tripling of volume in roughly two years, a growth rate that no other major Tesla business line comes close to matching.

Elon Musk, Chief Executive Officer, has described the stationary storage business as “growing like wildfire,” characterising Megapack demand as “very strong.”

What separates this segment from automotive is its demand profile. Energy storage is driven by grid stability requirements, AI compute load growth, and data centre buildout, none of which depend on consumer vehicle purchasing cycles. Oppenheimer raised its energy storage sales forecasts by 2% for the remainder of 2026 and by 3% for each of FY2027 and FY2028. Modest percentage increases on a base compounding at near-50% annual rates carry meaningful valuation weight.

Key deployment milestones:

- 14.7 GWh deployed in 2023 (baseline)

- 46.7 GWh deployed in 2025 (up 49% year over year)

- Lathrop Megapack factory: approximately 40 GWh annual capacity

- Shanghai Megapack factory: targeting approximately 40 GWh annually (not formally confirmed in public filings)

Manufacturing capacity is catching up to demand

The Lathrop, California factory has ramped to approximately 40 GWh of annual production capacity. The Shanghai Megapack facility targets a similar 40 GWh annual output, though that figure has not been formally confirmed in public filings and investors should monitor upcoming earnings disclosures for clarity on the ramp timeline.

Combined, the two factories would provide roughly 80 GWh of annual capacity, a figure that only recently would have seemed aggressive but now appears necessary given the deployment trajectory.

When big ASX news breaks, our subscribers know first

Why energy storage is structurally tied to AI infrastructure, not just the grid

The connection between AI workload growth and battery demand runs through a specific mechanism that makes this more than a cyclical commodity story.

- AI workloads, particularly large language model training and inference, require immense GPU compute

- GPU clusters produce spiky, irregular power demand that strains grid connections

- Grid instability forces data centres to over-provision backup generation, raising costs

- Large-scale batteries buffer those demand spikes, allowing generators and grid connections to run at higher, more efficient utilisation

- Megapack deployment fills this exact role for commercial and industrial sites

Industry experts have characterised large-scale batteries as a “fundamental new part of infrastructure” for data centres and AI workloads. That framing matters because it positions battery storage not as an optional efficiency upgrade but as a structural requirement for the next generation of compute facilities.

U.S. large-scale battery storage capacity trends tracked by the EIA show installed capacity accelerating sharply through 2024 and 2025, a market-wide backdrop that contextualises why Megapack deployment volumes are growing at the rates Tesla is reporting rather than being a company-specific anomaly.

| Use Case | Problem Solved | Tesla Product | Demand Driver |

|---|---|---|---|

| Data centre | Spiky GPU power demand exceeds grid capacity | Megapack | AI compute buildout |

| Grid stability | Renewable intermittency creates frequency imbalance | Megapack | Renewable energy integration |

| Industrial facility | Peak-shaving and backup power reduce energy costs | Megapack | Commercial electricity cost management |

This structural dynamic is why Oppenheimer’s forward storage revisions may prove conservative by design. If AI infrastructure demand continues accelerating, those estimates could function as a floor rather than a ceiling on the segment’s contribution to Tesla’s valuation.

The SpaceX angle: a thesis with real strategic logic and real limits

The case for Tesla as infrastructure provider to SpaceX rests on straightforward industrial logic. SpaceX operates power-intensive facilities across launch sites, tracking stations, Starlink ground infrastructure, and data-centre-style compute operations. Megapack is purpose-built for exactly this type of high-uptime industrial deployment. Shared ownership and leadership culture between the two companies makes increasing internal procurement structurally plausible.

Oppenheimer specifically identified SpaceX’s data centre leasing activities as a cash flow source connected to this dynamic. A potential SpaceX initial public offering could accelerate both disclosure and investor attention on the relationship.

The Tesla-SpaceX supply relationship sits inside a broader institutional debate about whether the two companies might eventually merge; Wolfe Research confirmed in June 2026 that a Tesla-SpaceX combination has moved from retail speculation to a mainstream allocator thesis, with the SpaceX IPO filing including equity-issuance language analysts read as deliberate legal flexibility for a stock-based transaction.

What would change this from thesis to line item

The distinction between strategic logic and confirmed revenue matters here. Several disclosures would materially upgrade this thesis:

What makes this thesis credible:

- Megapack’s exact product fit for high-uptime, power-intensive facilities

- SpaceX’s growing power and compute infrastructure footprint

- Shared ownership and leadership between the two companies

- Oppenheimer’s identification of SpaceX data centre leasing as a connected cash flow source

What is not yet confirmed:

- No formal contracts between Tesla and SpaceX have been publicly announced

- No specific percentage of Megapack volume has been attributed to SpaceX projects

- The connection remains qualitative, not quantified in earnings disclosures

Investors should watch for three specific triggers: a public contract announcement, volume attribution in Tesla earnings commentary, or detail in a SpaceX IPO prospectus regarding power infrastructure sourcing. Until one of those materialises, this remains an emerging thesis with meaningful upside optionality, not a confirmed line item to model with confidence.

A SpaceX IPO prospectus surfacing detail on power infrastructure sourcing would be the single disclosure that converts this thesis from qualitative signal to modellable line item; SpaceX priced its IPO at $135 per share on 3 June 2026, implying a $1.75 trillion valuation and bypassing the traditional institutional roadshow, which means the prospectus itself remains the primary document investors can interrogate for infrastructure contract detail.

Oil prices are doing quiet work on Tesla’s vehicle demand outlook

Oppenheimer raised Tesla vehicle sales estimates by 4% across FY2026 through FY2028, and the driver was not a new product launch or FSD progress. It was elevated oil prices.

The mechanism operates through total cost of ownership:

- Higher oil prices raise the multi-year operating cost of internal combustion engine (ICE) vehicles

- The raised operating cost makes the upfront EV price premium easier to justify through fuel savings calculations

- The improved payback period increases the probability that cost-sensitive buyers convert to EVs

Persistent high oil prices make current vehicle volume estimates more likely to be conservative than aggressive, according to Oppenheimer’s framework, because the total cost of ownership advantage for EVs widens with every sustained quarter of elevated fuel costs.

The oil supply disruption driving this EV tailwind is not a temporary demand spike; Saudi Arabia’s crude output collapsed to 6.316 million barrels per day in April 2026, its lowest level since 1990, and the IEA projects no scenario in which global supply and demand return to balance before October 2026, making the fuel-cost advantage for EV buyers structurally durable across the 2026-2027 window Oppenheimer is modelling.

Tesla’s share leadership in higher-end EVs means it tends to capture a disproportionate share of incremental EV demand relative to legacy automakers when macro conditions favour battery-electric vehicles. This tailwind operates independently of Tesla’s software execution risk, providing a macro buffer that supports unit volume estimates even if FSD timelines slip or new product launches are delayed.

Why autonomy and Optimus should be watched, not modelled

FSD remains classified as SAE Level 2, Supervised, as of mid-2026. The human driver is responsible for supervision and liability in all major markets. Scaling to wide-area, unsupervised robotaxi services requires not just technical performance improvements but also safety data accumulation, regulatory approval frameworks, insurance structures, and large-scale fleet operations, all of which are time-consuming across jurisdictions.

Oppenheimer flagged FSD V15 as the next significant milestone to monitor. A “proof point” in this context means evidence that the technology is progressing toward unsupervised capability, not evidence that it is ready to generate revenue at scale. The distinction matters for anyone building a near-term earnings model.

| Business Line | Current Status | Time Horizon | What to Monitor |

|---|---|---|---|

| Energy storage (Megapack) | Scaling; 49% YoY growth | Near term (2026-2027) | Quarterly deployment volumes, factory ramp updates |

| FSD / Autonomy | SAE Level 2 Supervised | Long-dated optionality | FSD V15 release, regulatory approvals, safety data |

| Optimus (Humanoid robotics) | Pre-commercial development | Long-dated optionality | Pilot deployment scale, unit economics disclosure |

Optimus on a separate timeline from FSD

Optimus faces a distinct set of commercialisation challenges. Where FSD is primarily a software and regulatory problem, humanoid robotics involves manufacturing at scale, embodied AI reliability in unstructured environments, and deployment economics that remain unproven across the entire industry.

Broader industry progress on humanoid platforms does not change Tesla’s specific execution timeline. Investors should avoid conflating sector headlines with Tesla’s roadmap; economically viable humanoid deployments at scale remain speculative beyond the near term for all participants.

A time-horizon map for building a Tesla position in mid-2026

Oppenheimer’s framework, stripped to its load-bearing components, segments Tesla exposure across three time horizons. The bull case for 2026-2027 does not require autonomy to be true. It requires five things:

- AI, data-centre, and grid-stability demand for storage to be real and durable

- Continued Megapack manufacturing scale-up across both factories

- Oil prices sustaining the EV total cost of ownership advantage

- Competent execution across Tesla’s existing core businesses

- The emerging SpaceX infrastructure relationship to move toward disclosure

| Time Horizon | Key Driver | What Makes It Credible | Key Risk |

|---|---|---|---|

| Near term (2026-2027) | Energy storage growth | 49% YoY deployment growth, dual factory ramp | Manufacturing execution, supply chain constraints |

| Near term (2026-2027) | Oil price tailwind | Elevated fuel costs widening EV TCO advantage | Oil price reversal, policy changes |

| Medium term | SpaceX infrastructure thesis | Structural logic, shared ownership, product fit | No public disclosure or confirmed contracts |

| Long-dated optionality | FSD, robotaxis, Optimus | Technical progress, fleet data accumulation | Regulatory timelines, unproven unit economics |

The single most important item to watch in upcoming quarters: whether Tesla earnings commentary or a SpaceX IPO prospectus provides quantitative detail on the Megapack supply relationship. That disclosure would convert the medium-term thesis from qualitative signal to modellable line item.

The analytical work in Tesla’s 2026 bull case is already being done by Megapack

Oppenheimer’s framework does not require Tesla to solve autonomy to justify near-term upside. The analytical weight sits with energy storage growing at 49% annually, a macro oil price tailwind independently supporting vehicle volumes, and a strategically plausible (if not yet quantified) infrastructure relationship with SpaceX.

FSD and Optimus remain legitimate sources of long-dated optionality. They are not, however, the foundation of the 2026-2027 case. Investors who treat them as the primary driver carry asymmetric downside risk if timelines slip; those who understand that Megapack and macro conditions are doing the near-term work are better positioned regardless of which direction the autonomy narrative moves.

The catalysts to monitor are specific: energy storage deployment figures in upcoming earnings, SpaceX IPO prospectus detail on power infrastructure sourcing, and FSD V15 progress updates. Each one either validates or challenges a distinct component of the thesis.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and company performance.