How Wesfarmers Buys, Builds, and Exits to Create Value

16 mins ago

Global markets are trading at or near record highs, yet a growing number of investment professionals in Australia are urging caution. The disconnect is striking: headline index performance suggests strength, but beneath the surface, supply disruptions, concentration risk, and the accelerating pace of market regime changes are creating structural vulnerabilities that many portfolios were never designed to absorb. Anthony Doyle of Pinnacle Investments, speaking on the nabtrade Your Wealth podcast hosted by Gemma Dale, has framed the current environment as one where conventional portfolio assumptions deserve serious scrutiny. The Reserve Bank of Australia’s characterisation of post-COVID volatility as “elevated” compared to pre-pandemic norms adds institutional weight to that view. This guide explains why the unease is rational, where conventional portfolio construction falls short, and what steps Australian investors can take to build a portfolio capable of weathering a wider range of outcomes.

The ASX 200, the S&P 500, and the MSCI World Index have each traded at or near record levels through early June 2026. By most conventional measures, portfolios have performed well. Yet investor confidence has not kept pace.

Three structural sources of unease explain the gap:

Doyle’s framing on the nabtrade Your Wealth podcast captures the tension directly: markets can be at record highs and structurally fragile at the same time. The strength of headline numbers does not automatically translate into portfolio resilience.

For Australian investors feeling uneasy despite solid returns, that instinct is not irrational. It reflects an accurate reading of conditions that the numbers alone do not convey.

Passive investing earned its dominance for legitimate reasons. Low fees, broad market exposure, tax efficiency, and a track record of outperforming most active managers over long time horizons made index funds the default strategy for millions of Australian retail investors over the past two decades.

Those strengths remain real. Nothing in the current environment erases them.

The structural challenge is specific: market-cap-weighted indices funnel capital disproportionately into the largest stocks. In global index funds, that means Australian investors holding a passive international equity allocation may carry a far heavier weight in a narrow group of US technology names than they realise.

Doyle argues that the current environment is particularly challenging for investors relying solely on passive strategies. The mechanism is concentration, not volatility in the abstract. When the handful of mega-cap names driving index performance reverses, there is no built-in mechanism within a passive strategy to reduce exposure or rotate capital.

The distinction matters:

Tail risk refers to the probability of extreme market outcomes, the kind that sit at the far edges of a statistical distribution and are expected to occur rarely. In practical terms, these are the sharp drawdowns, liquidity seizures, or cross-asset dislocations that conventional portfolio construction assigns very low probability weights.

Because those weights are low, portfolios are typically built with limited defences against such events. The implicit assumption is that extreme moves are infrequent enough that the cost of protecting against them outweighs the benefit.

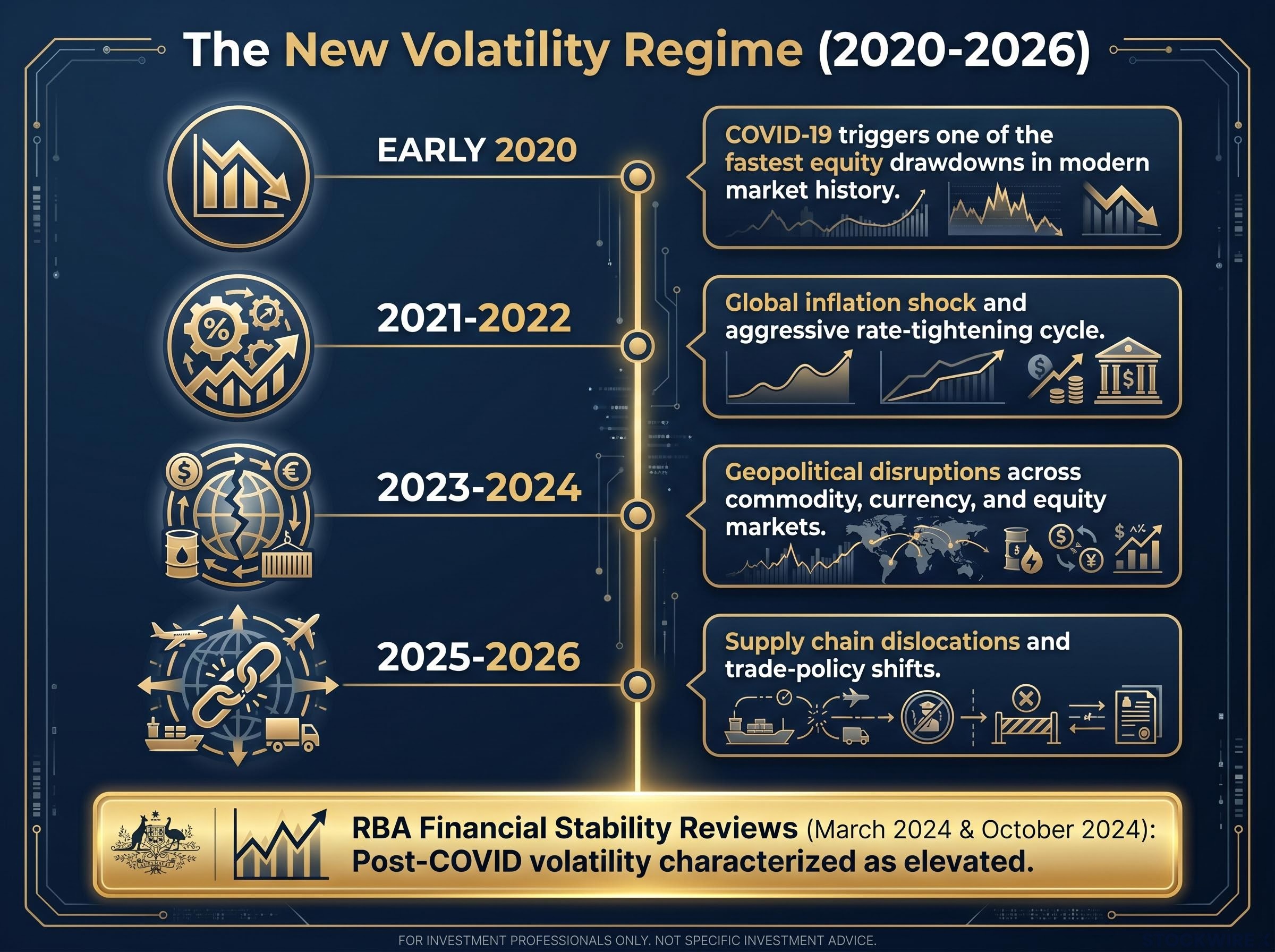

Doyle’s core claim is direct: events historically categorised as once-in-a-century occurrences are now materialising on an annual basis. The sequence since 2020 illustrates the pattern:

The RBA’s Financial Stability Reviews from March 2024 and October 2024 support this reading. Both characterise post-COVID equity and bond market volatility as “elevated” compared to pre-pandemic norms. The characterisation is qualitative, not a precise numeric count, but it carries institutional weight: Australia’s central bank is telling investors that the volatility regime has shifted.

If the statistical assumptions underpinning conventional portfolio construction are wrong, the safety margins investors believe they hold may not exist. That is the discomforting implication, and it is the foundation for everything that follows.

Most portfolios carry assumptions their owners never explicitly chose. These assumptions were baked into the strategy at construction and have gone untested because, until recently, market conditions did not challenge them.

Doyle’s commentary highlights that many portfolios rest on foundational premises that may be overly optimistic or difficult to sustain under current conditions. Three of the most common deserve scrutiny.

| Common Assumption | Why It Formed | Current Challenge | Risk If Wrong |

|---|---|---|---|

| Bonds always offset equity drawdowns | Negative equity-bond correlation held for most of 2000-2020 | Equity and bond markets fell simultaneously during the 2022 rate shock | Portfolios lose their primary shock absorber in the scenario they need it most |

| Volatility is mean-reverting on short time horizons | Pre-COVID volatility clusters tended to resolve within quarters | RBA characterises post-COVID volatility as structurally “elevated,” not episodic | Investors waiting for normalisation may be waiting for a regime that no longer applies |

| A global index fund provides genuine diversification | Global indices historically spread risk across geographies and sectors | Cap-weighted global indices now carry concentrated exposure to a narrow group of US technology names | A “diversified” global holding may behave like a concentrated sector bet |

Safe haven assets including government bonds, gold, and the Japanese yen all fell simultaneously during the 2026 Iran supply shock, with Australian CPI reaching 4.6% and the RBA raising rates into an environment where equities were also under pressure, providing a live-market illustration of exactly the simultaneous equity-bond drawdown scenario the assumptions table above identifies as a key portfolio risk.

The concentration point is worth isolating. Australian investors holding passive global equity index funds may not realise that a meaningful share of their international allocation is concentrated in a small number of US technology-adjacent companies, often referred to as the “Magnificent 7.” Industry commentary from sources including Vanguard Australia and Morningstar Australia has flagged that this concentration flows directly through to the portfolios of Australian investors via their global passive exposures.

Cap-weighted index construction assigns the largest companies the largest portfolio weights and then allows those weights to grow unchecked as prices rise, which is precisely why the top 10 companies in the ASX 200 accounted for nearly half the index as of May 2026, and why major global ETFs marketed to Australian investors can carry US weightings above 70%.

The assumption that a global index fund provides broad diversification may no longer hold in the way it did a decade ago.

Morningstar’s analysis of Magnificent Seven concentration quantifies how the dominance of a small cluster of US technology names reduces the effective diversification of cap-weighted global indices, with narrow market leadership creating portfolio vulnerability that passive exposure alone cannot offset.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

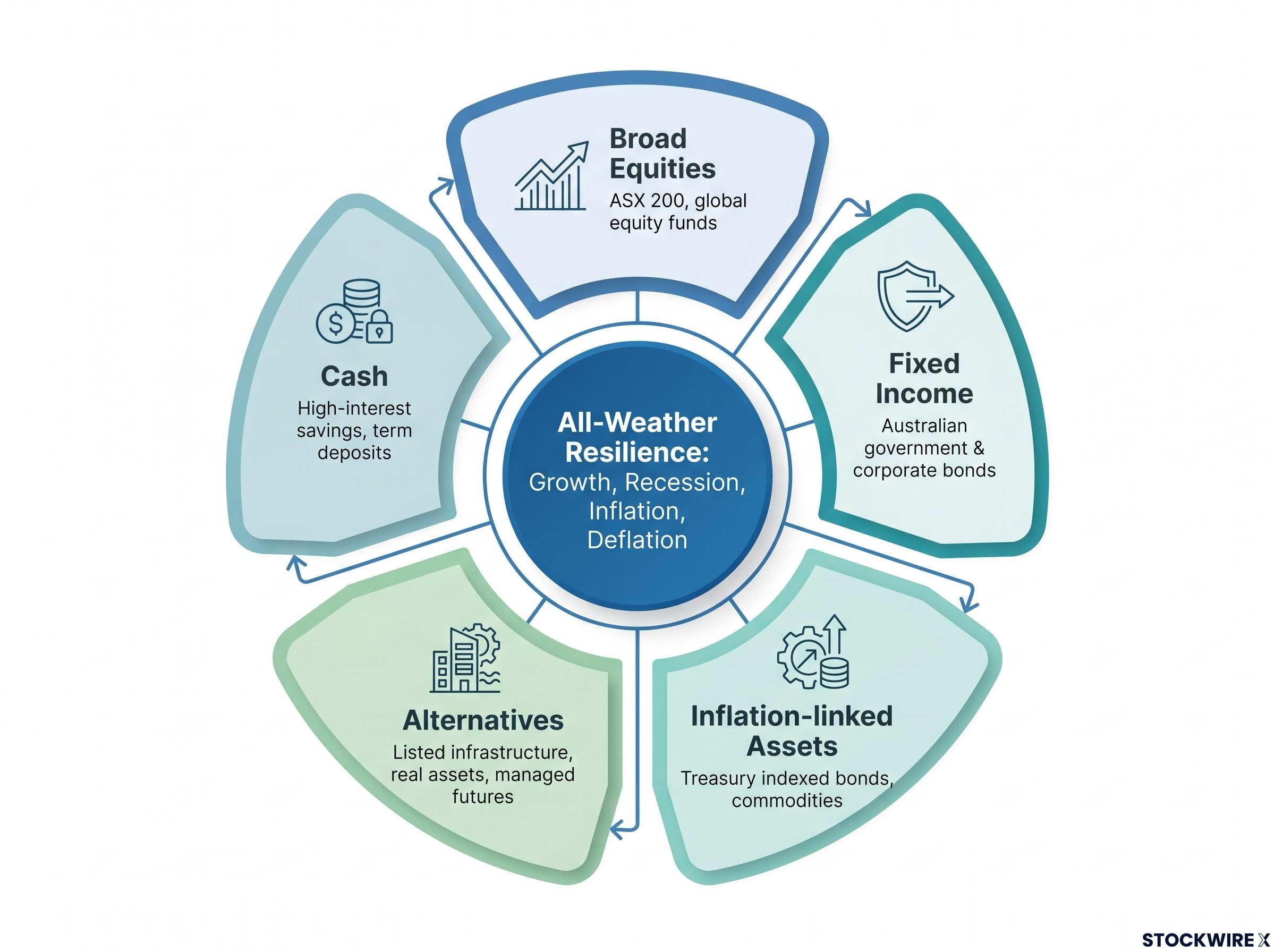

An all-weather portfolio is a multi-asset framework designed to perform adequately across different economic environments, whether growth, recession, inflation, or deflation. Rather than maximising returns in a single scenario, the goal is to build a structure that remains resilient across the range of conditions that cannot be predicted in advance.

Four-quadrant risk balancing, the framework that allocates portfolio weight across rising growth, falling growth, rising inflation, and falling inflation environments, is the conceptual foundation behind the all-weather approach, and it is why the asset class table above looks the way it does: each row is designed to perform in a different macro quadrant rather than a single expected outcome.

Doyle’s recommendation centres on constructing a diversified portfolio designed to withstand downside risk while retaining the capacity to capture upside opportunities. The structural components that deliver this span five core building blocks.

| Asset Class | Role in Portfolio | Australian Examples | Scenario Where It Performs Well |

|---|---|---|---|

| Broad equities (domestic and international) | Growth engine; long-term capital appreciation | ASX 200 index funds, diversified global equity funds with active or equal-weight tilts | Economic expansion, strong corporate earnings |

| Fixed income | Income generation and capital preservation with duration management | Australian government bonds, investment-grade corporate bonds | Recession, falling interest rates, risk-off environments |

| Inflation-linked assets | Purchasing power protection | Treasury indexed bonds, commodity-linked exposures | Rising inflation, supply-driven price shocks |

| Alternatives | Diversification beyond traditional equity-bond correlation | Listed infrastructure (e.g., toll roads, utilities), real assets, managed futures | Stagflation, late-cycle environments, equity-bond correlation breakdown |

| Cash | Tactical buffer and optionality | High-interest savings accounts, term deposits | Market dislocations, providing dry powder for rebalancing |

The construction principles that tie these components together are straightforward:

The ASIC MoneySmart guidance on diversification sets out how spreading exposure across asset classes and within them lowers portfolio risk and produces more stable returns over time, providing the regulatory baseline against which Australian retail investors can benchmark their own allocation decisions.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The RBA’s characterisation of post-COVID volatility as structurally elevated reinforces why a multi-scenario framework is not overcautious. It is portfolio construction calibrated to the environment that actually exists.

The risks outlined in this guide are structural, but the response does not need to be an overhaul driven by headlines. A more effective starting point is a diagnostic self-assessment, a set of questions that stress-test a portfolio against a wider range of scenarios than may have been considered at construction.

Drawing on the principles discussed throughout this guide, five questions provide a practical framework:

These statements are speculative and subject to change based on market developments and company performance.

The goal is not to predict what markets will do next. It is to ensure that the portfolio is prepared for more than one answer.

Record-high markets do not mean a crash is imminent. The argument for an all-weather portfolio is not a forecast; it is a structural position. Volatility is elevated compared to pre-pandemic norms, concentration risk in passive indices has intensified, and the frequency of extreme market events has increased beyond what conventional models assumed.

Investors who stress-test their portfolios now are not betting against the market. They are applying the same rigour to downside scenarios that most already apply to upside planning.

The five diagnostic questions from the previous section offer a practical starting point. Reviewing concentration exposure in any passive global index holdings is a concrete first step. For investors considering changes, consulting a licensed financial adviser before acting remains the prudent course.

For investors who want a standing framework rather than a reactive one, our comprehensive walkthrough of geopolitical investing strategy covers gold allocation thresholds, bond duration management, defence sector exposure, and rebalancing discipline with specific institutional benchmarks from BlackRock and Goldman Sachs, giving readers a rules-based approach to portfolio positioning that functions before, during, and after geopolitical shocks.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

An all-weather portfolio is a multi-asset framework designed to perform adequately across different economic environments, including growth, recession, inflation, and deflation, rather than maximising returns in a single scenario.

Cap-weighted global indices funnel disproportionate weight into the largest stocks, meaning Australian investors holding passive global equity funds may carry heavy concentration in a narrow group of US technology companies, reducing the diversification benefit they expect.

Investors should calculate the combined weight of the largest US technology names across all passive global equity funds in their portfolio, as the figure is often higher than expected due to cap-weighted index construction.

The Reserve Bank of Australia's Financial Stability Reviews from March 2024 and October 2024 characterise post-COVID equity and bond market volatility as elevated compared to pre-pandemic norms, signalling a structural shift in the volatility regime rather than a temporary episode.

A well-constructed all-weather portfolio typically spans broad equities, fixed income with duration management, inflation-linked assets, alternatives such as listed infrastructure and managed futures, and a cash buffer for tactical rebalancing during market dislocations.