European equity indices have spent three months trading below their late-February highs while the S&P 500 has climbed roughly 9% above the same reference point. That divergence, largely background noise through April and early May, is now drawing pointed attention from equity strategists. A potential US-Iran agreement, and its downstream effects on oil prices and interest rate expectations, has moved from speculative scenario to a front-of-mind catalyst. Barclays, in a strategy note dated 29 May 2026, framed the deal as the single event most capable of breaking European markets out of their extended consolidation range. What follows is an analysis of what drove the divergence, which European sectors carry the most asymmetric exposure, and how short-squeeze mechanics could amplify any breakout if a catalyst materialises.

Why European equities have stalled while US markets moved on

The gap between European and US equity performance is not new, but the scale has become difficult to dismiss. Both the STOXX Europe 600 and the Euro STOXX 50 remain below their 27 February 2026 peak levels, a consolidation that has now persisted for approximately three months. Over the same window, the S&P 500 has pushed materially higher.

The S&P 500 stood approximately 9% above its 27 February 2026 reference level as of 29 May 2026, according to Barclays equity strategy data, while both major European indices remained trapped below that same benchmark.

The temptation is to attribute the gap to structural European weakness: slower growth, a more cautious European Central Bank (ECB), or persistent productivity differentials. Barclays’ reading points in a different direction. The consolidation, on this analysis, is geopolitically driven, with the US-Iran conflict overlaying a specific set of pressures on European sector compositions that US markets, with their heavier technology and growth weighting, have been better positioned to absorb.

European capital flow dynamics in 2026 add structural context to the divergence: US semiconductor ETFs have captured record inflows driven partly by a self-reinforcing dollar feedback loop, while European segments face the combined headwinds of sluggish eurozone growth, elevated energy costs, and an ECB holding rates at 2.00% with no near-term stimulus catalyst, conditions that make the current US-Europe gap something more than a geopolitical pricing anomaly.

If the stall is geopolitical rather than structural, the conditions for a breakout become identifiable. Barclays frames three as necessary:

- A confirmed US-Iran agreement that reopens the Strait of Hormuz

- A resulting decline in oil prices

- A consequent shift lower in interest rate expectations

Each condition feeds the next. Whether all three materialise remains genuinely uncertain.

When big ASX news breaks, our subscribers know first

The geopolitical fault lines running through European sector performance

The performance split across European sectors tells the story before the explanation arrives. Since the onset of the conflict, a clear divide has opened between sectors that absorbed the shock and those that were compressed by it.

| Sector | Conflict-period performance direction |

|---|---|

| Energy | Outperformer: direct commodity price exposure |

| Telecoms | Outperformer: defensive yield characteristics |

| Utilities | Outperformer: defensive yield and regulated pricing |

| Insurance | Outperformer: conflict-related demand and pricing power |

| Consumer discretionary | Underperformer: demand suppression and rate sensitivity |

| Mining | Underperformer: global demand uncertainty |

| Banking | Underperformer: rate-path uncertainty and credit risk repricing |

The pattern did not emerge from a single shock. It has been building since the conflict’s onset, according to Barclays, with the four outperformers sharing either direct commodity exposure, defensive yield appeal, or conflict-amplified demand. The three laggards share a common vulnerability: sensitivity to the rate and demand environment that elevated energy prices have sustained.

European equity valuations have compressed from approximately 18x forward earnings in January 2026 to around 14.4x by May, with Goldman Sachs estimating that each 1% rise in oil prices removes roughly 20 basis points through multiple compression rather than earnings deterioration, a dynamic that partly explains why the STOXX indices have stalled without collapsing outright.

This matters because any de-escalation would not produce a uniform market rally. The reversal, if it comes, would be concentrated in the names that have been most compressed, making the sector split a map of where rotation pressure is most likely to build.

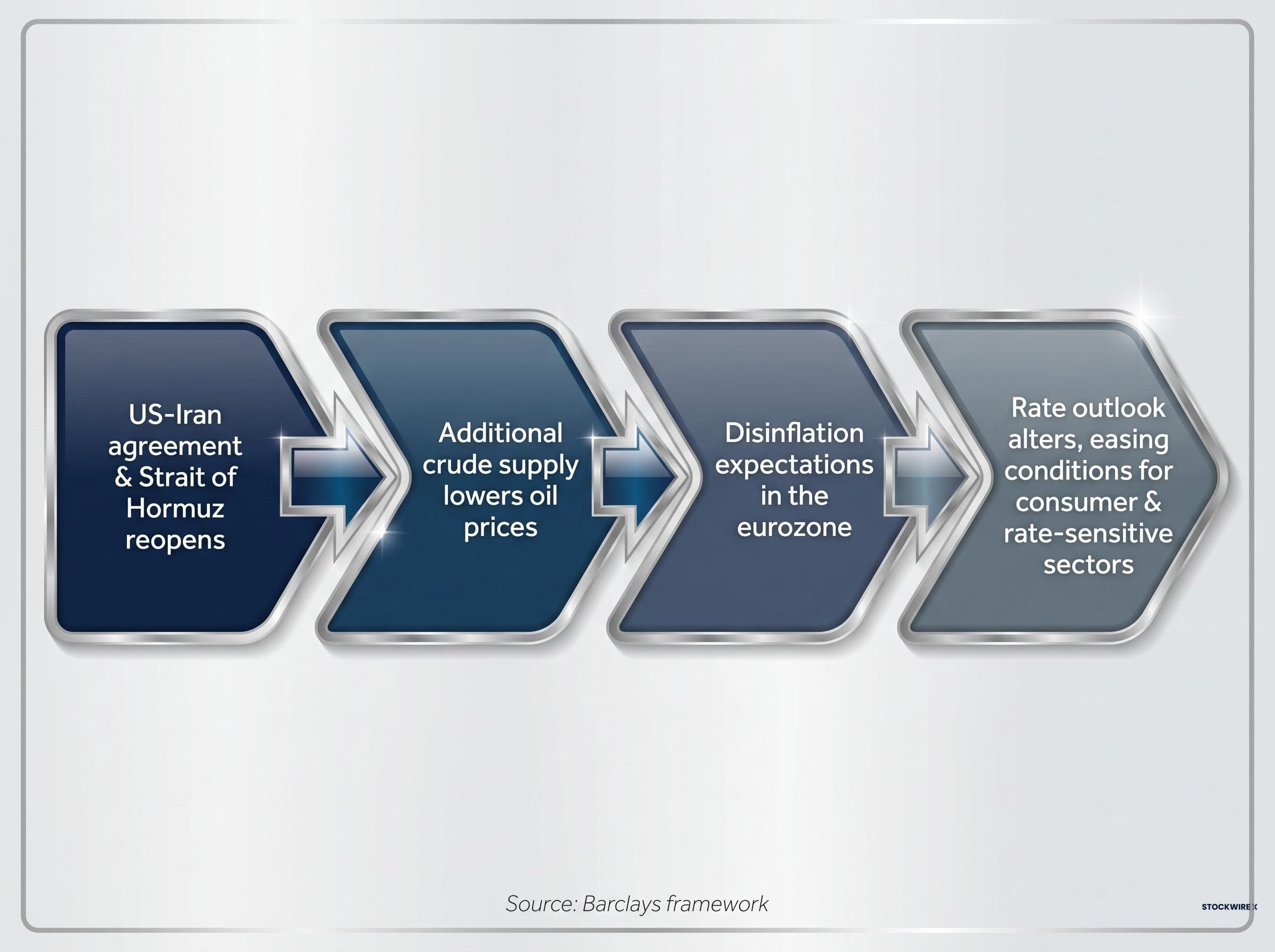

What a US-Iran deal would actually change for oil, rates, and European markets

The phrase “deal equals rally” compresses a multi-step transmission mechanism into a conclusion. The actual pathway from diplomatic agreement to European equity repricing runs through several distinct stages, each carrying its own uncertainty.

- A US-Iran agreement that includes specific provisions for reopening the Strait of Hormuz

- The reopening introduces additional crude supply to global markets, creating downward pressure on oil prices

- Lower oil prices feed into disinflation expectations across the eurozone, where elevated energy costs have been a persistent driver of inflationary pressure

- Shifting inflation expectations alter the rate outlook, easing conditions for the consumer and rate-sensitive sectors that have been most compressed

Barclays frames this chain as the combined catalyst capable of breaking European indices out of their consolidation range. The scenario is conditional and forward-looking; no independently verified May 2026 diplomatic progress was located in public reporting, and the sequence should be understood as a contingent framework rather than an imminent event.

Bloomberg’s May 2026 coverage of US-Iran negotiations, published the day before the Barclays strategy note, described peace talks as fragile while also noting President Trump’s public comments on the Strait of Hormuz, illustrating how quickly the diplomatic picture can shift between a headline catalyst and a durable geopolitical resolution.

Barclays cautioned that any rally in underperforming European names following a potential deal could prove temporary. The bank’s macro team anticipated elevated oil prices persisting, which would limit the durability of rate-sensitive sector gains.

That internal tension within Barclays’ own analysis is informative. The equity strategy team identifies the catalyst; the macro team questions its staying power. Historical precedent offers some support for the equity view: Barclays noted that energy-related market disruptions in recent decades have tended not to sustain lasting crude price impacts, with values typically declining as excess supply grew post-shock. Equity positioning, the bank observed, did not appear to reflect this historical pattern.

Short squeezes and the mechanics of a sector rotation under pressure

Before applying the short-squeeze framework to European sectors, the underlying mechanics warrant explanation. A short squeeze is not simply a sharp rally. It is a specific market dynamic where the mechanics of bearish positioning amplify upward price movement beyond what the underlying catalyst alone would produce.

Short selling involves borrowing shares and selling them with the intention of buying them back later at a lower price. When a stock or sector that has attracted substantial short positions experiences a positive catalyst, the resulting price increase forces short sellers into a difficult position: their losses mount as prices rise, and they must eventually buy shares to close their positions. That forced buying adds further upward pressure, which in turn forces more short covering, creating a self-reinforcing cycle.

Barclays identified elevated short positioning in consumer and rate-sensitive European segments as a potential source of amplified returns in a de-escalation scenario. The specific sub-sectors flagged as short-squeeze candidates include:

- Luxury goods

- Travel and leisure

- Automobiles

- Retail

No quantitative short interest data for these sub-sectors was independently verified, but the directional logic is clear: these are the segments that have accumulated bearish bets during the conflict period, precisely because they are most sensitive to the conditions the conflict has sustained.

How short positioning amplifies sector moves in a de-escalation scenario

The forced-buying dynamic is what distinguishes a short squeeze from an ordinary rally. In a standard recovery, buyers enter at prices they consider attractive. In a squeeze, buying occurs regardless of valuation, driven by risk management rather than conviction. Short sellers covering their positions are not expressing a positive view; they are limiting losses.

For the named sub-sectors, the combination of a geopolitical catalyst and accumulated short positioning creates compounding upside risk. A confirmed deal would shift the fundamental outlook; the short covering would then mechanically amplify the price response. This is why sector rotations out of geopolitical discounts can move faster and further than the underlying change in conditions would seem to justify.

Calibrating expectations: what the historical pattern says about staying power

The rotation scenario is compelling as a short-term trade thesis. Whether it supports a durable rerating of European consumer and rate-sensitive sectors is a separate question, and the evidence is less encouraging.

Barclays’ own macro team expects elevated oil prices to persist, which would limit the duration and depth of any rate-sensitive rally even if a deal materialises. If oil does not fall as sharply or as durably as the equity catalyst scenario requires, the third and fourth links in the transmission chain (disinflation expectations and rate path shifts) weaken accordingly.

The 2027 dimension adds a further complication: Goldman Sachs revised its STOXX 600 2026 EPS growth forecast to 10%, but the upgrade rests almost entirely on commodity-sector earnings from energy and mining, with non-commodity margins tracking flat against a consensus expectation of 100 basis points of improvement, and 2027 forecasts already reflecting a partial reversal of that commodity tailwind.

MPRA research on oil prices and European equity performance, covering European markets from 1991 to 2023, found that rising energy costs consistently exerted downward pressure on petroleum-reliant industries by increasing production costs, with the magnitude of the effect varying materially across sectors, a pattern consistent with the compression observed in consumer discretionary and industrial names during the current conflict period.

The historical pattern Barclays cites cuts both ways. Past energy disruptions have seen crude prices decline sharply once excess supply emerged, but the timeline for that supply response has varied. Equity positioning has historically not reflected the eventual supply correction, suggesting markets may be slow to price in the medium-term normalisation, even as the near-term catalyst drives sharp moves.

Investors attempting to distinguish between a short-squeeze bounce and a structural rerating should monitor several signals:

- Oil price trajectory in the weeks following any confirmed deal

- ECB commentary or rate path adjustments in response to shifting inflation data

- Depth and specificity of diplomatic confirmation beyond initial headlines

- Duration of short-covering activity relative to fresh long positioning in the affected sub-sectors

The absence of independent ECB commentary linking the rate path to European sector performance, as of late May 2026, means the rate leg of the thesis remains scenario-dependent rather than policy-confirmed.

European equities are priced for a conflict that may already be repricing

The analytical picture, taken whole, is one of conditional opportunity with honest uncertainty at its centre. European equity markets have spent three months consolidating below their February highs while the S&P 500 has moved 9% higher. The gap is not random; it tracks a specific set of geopolitical pressures that have rewarded energy, telecoms, utilities, and insurance while compressing consumer discretionary, mining, and banking names.

A US-Iran agreement remains the identified catalyst capable of reversing that split. The transmission runs from diplomacy through oil through rates through sector repricing, and each link carries its own probability. Barclays frames the scenario with institutional specificity, but the bank’s own macro team tempers the equity thesis, and no corroborating institutional voice was identified in available public research.

The value of this framework is not a directional call. It is a structured lens for interpreting the news flow as diplomatic developments unfold. If a deal materialises, the sector map above identifies where rotation pressure should concentrate. If it does not, the consolidation range likely persists, and the divergence with US markets widens further. Either path is readable within the framework; neither is guaranteed.

Investors wanting to translate this sector rotation framework into concrete portfolio positioning will find our dedicated guide to geopolitical investing strategy covers gold allocation targets, defence sector exposure mechanics, and a five-component resilience checklist designed to function before, during, and after the kind of geopolitical catalyst cycle this article analyses.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and diplomatic progress.