Goldman Warns CPI Print Could Reprice an Overvalued Market

11 mins ago

Barclays flagged three simultaneous risks for U.S. equity investors in a note published today, 27 May 2026, warning that a record-setting wave of IPO supply, dangerously crowded AI and momentum trades, and specific positioning reversals could converge to punish the consensus bets that have driven returns over the past two years. The warning arrives as U.S. equities remain dominated by a narrow set of technology and AI-adjacent winners, with institutional capital piled into that leadership in ways that create asymmetric downside if the narrative shifts. What follows is a breakdown of exactly what Barclays warned, what a pain trade is and why it matters, which specific market reversals would cause the most damage, and what the IPO supply surge means for stocks today.

The Barclays note, reported via Investing.com on 27 May 2026, is not a vague call for caution. It names three distinct, interconnected risk categories:

Barclays characterised 2026 IPO activity as on pace to produce the heaviest annual issuance since 2021, a year whose supply boom preceded a sharp correction in growth stocks.

The three risks reinforce each other. Heavy IPO supply absorbs capital from existing holdings. That capital drain hits hardest when positioning is already concentrated in a narrow group of winners. And the pain trade scenarios define exactly which reversals would do the most damage to that concentration. Barclays’ Emmanuel Cau appeared on CNBC on 21 May 2026 discussing SpaceX’s IPO and its implications for U.S. market dominance, providing additional context for the bank’s broader positioning view.

The pace of new issuance in 2026 is accelerating, and the data confirms Barclays’ characterisation of trajectory.

| Period | Number of IPOs | Proceeds | Source |

|---|---|---|---|

| Q1 2025 | 15 | $7.9 billion | PwC US Capital Markets Watch |

| Q1 2026 | 22 | $9.4 billion | PwC US Capital Markets Watch |

| Full-year 2025 | 216-347 | $47.4 billion | EY / Stout / Dealogic |

| 2021 (benchmark) | 400+ | Hundreds of billions | Reuters, FT |

Through late May 2026, 63 IPOs have priced, raising $28.8 billion, according to Renaissance Capital. The year-on-year jump from Q1 2025 to Q1 2026 (15 IPOs to 22, $7.9 billion to $9.4 billion) confirms the acceleration.

Renaissance Capital IPO market statistics confirm the acceleration: 63 IPOs have priced through late May 2026, raising $28.8 billion, a pace that tracks materially ahead of the same period in 2025 and consistent with Barclays’ characterisation of 2026 issuance as the heaviest since 2021.

The mechanics are straightforward. New listings require institutional investors to allocate capital, and that capital often comes from trimming existing positions. When the IPO pipeline is heavy, the selling pressure on current holdings is a mechanical drag, not a sentiment story.

The capital absorption dynamic is better understood with a firm grasp of IPO mechanics for retail investors: institutional allocations happen at the offer price, while public buyers typically enter the secondary market after the first-day pop has already cleared, absorbing the premium that insiders captured at the bottom of the pricing chain.

Barclays’ use of 2021 as the benchmark is deliberate. That year produced more than 400 deals and hundreds of billions in proceeds, according to Reuters and the Financial Times. It was also the peak before a sharp drawdown in growth and technology stocks through 2022. The comparison signals pace and risk, not celebration.

A pain trade is a market move that inflicts the most damage on the largest number of investors because it runs directly against the most crowded positioning at the time.

The concept, defined consistently across Bloomberg, the Financial Times, and the Wall Street Journal, rests on a mechanical reality. When positioning becomes heavily skewed in one direction, the move that causes the greatest aggregate loss is the one that reverses that consensus. The more lopsided the positioning, the more severe the reversal.

A recent illustration: unexpected bond market rallies in 2023-2024 wrong-footed investors who had positioned heavily for equities over fixed income. The pain was not that bonds rose; it was that the majority of capital sat on the other side of the trade.

Three structural conditions make a pain trade severe:

In 2026, the unusually concentrated positioning in U.S. technology and AI-adjacent stocks meets all three conditions, which is precisely the setup Barclays is flagging.

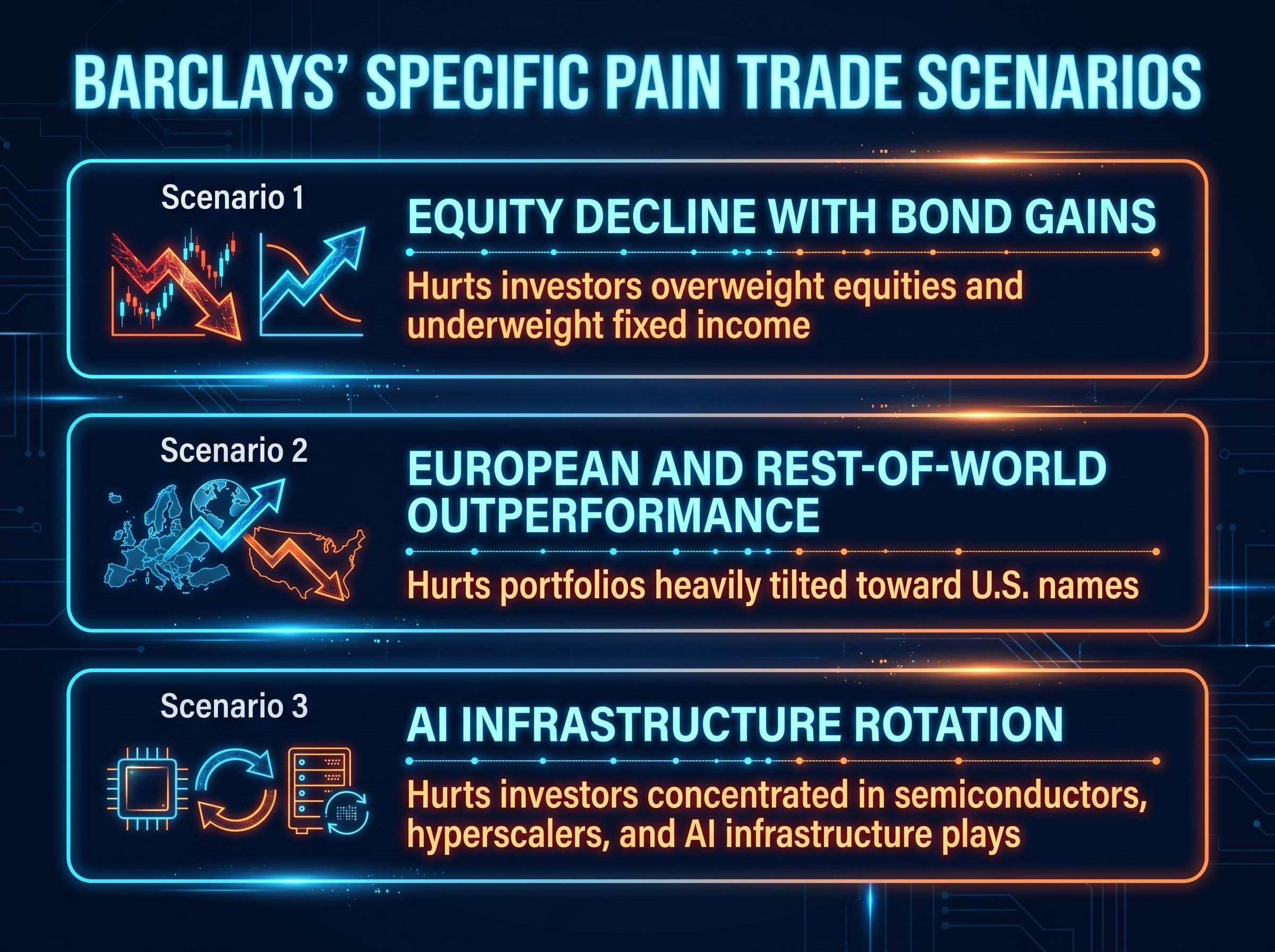

Barclays named three scenarios, each targeting a different dimension of current positioning.

| Scenario | What reverses | Who gets hurt most |

|---|---|---|

| Equity decline with bond gains | Stocks fall while bonds rally | Investors overweight equities and underweight fixed income |

| European and rest-of-world outperformance | Non-U.S. markets outpace U.S. equities | Portfolios heavily tilted toward U.S. names relative to historical norms |

| AI infrastructure rotation | AI/semiconductor weakness; consumer and bond proxy strength | Investors concentrated in semiconductors, hyperscalers, and AI infrastructure plays |

The first two scenarios are positioning reversals in the traditional sense: a shift in asset class leadership (equities to bonds) or geographic leadership (U.S. to rest of world). Neither requires a market crash; a sustained period of relative underperformance would be enough to damage concentrated portfolios.

US equity home bias has transformed from a diversification shortfall into a concentrated directional bet on the AI infrastructure capex cycle, with the average US investor holding 70-76% of their equity portfolio in domestic stocks at a moment when S&P 500 earnings growth forecasts are disproportionately reliant on a small number of AI-exposed firms.

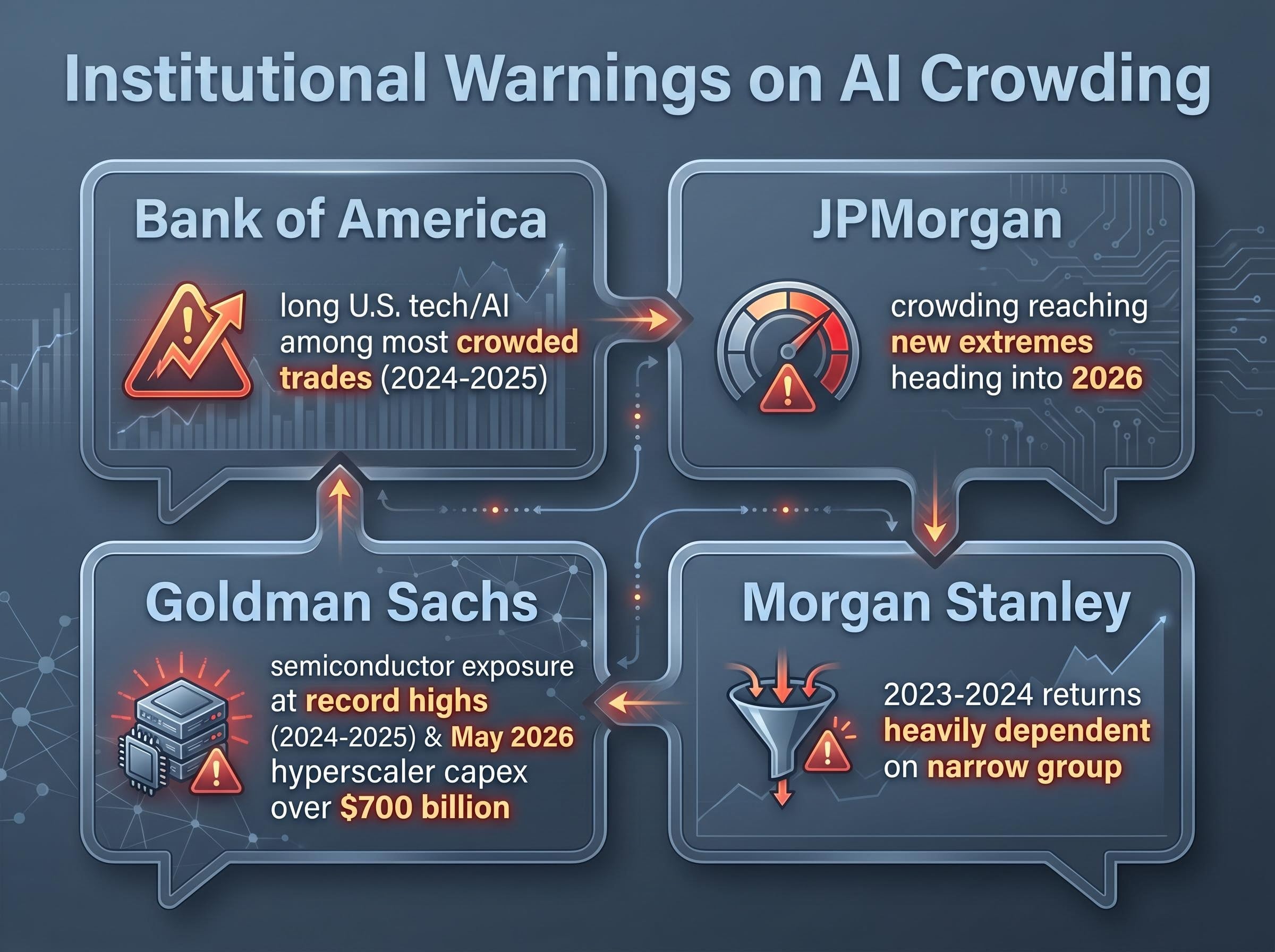

JPMorgan’s 2026 Global Research Market Outlook corroborates the setup, characterising crowding as reaching new extremes and describing a “winner-takes-all” dynamic between AI and non-AI sectors.

The third scenario is the most complex. It does not require a broad market selloff, only a shift in sector leadership. Investors concentrated in semiconductors (through ETFs such as SOXX and SMH), hyperscalers, and AI infrastructure names would experience underperformance even if the overall index held steady.

Morgan Stanley’s expectations for 2026 included potential broadening of market leadership beyond AI mega-caps, implying that the concentrated positioning built during the AI boom could begin to unwind. A rotation toward consumer-oriented stocks and bond proxies (utilities, REITs, dividend payers) would represent exactly the kind of leadership shift that punishes the most popular trades without triggering headline panic.

Barclays’ crowding characterisation is not a subjective call. Multiple institutions have independently flagged the same positioning imbalance:

JPMorgan characterised crowding as reaching “new extremes” heading into 2026, with multidimensional polarisation developing between AI and non-AI sectors.

According to Goldman Sachs’ May 2026 commentary, hyperscaler capital expenditure commitments were running at more than $700 billion on an annualised basis, a figure that captures the scale of investment flowing into AI infrastructure. When three of Wall Street’s largest institutions independently flag the same concentration concern, the signal carries more weight than any single bank’s view.

The expectations gap framework, drawn from Howard Marks and Aswath Damodaran, offers a precise explanation for why consensus trades become dangerous even when the underlying thesis is correct: returns are determined by the difference between what a price already implies and what actually occurs, not by the quality of the outcome alone, which means a correct AI investment thesis can still produce negative returns for investors who entered after expectations were fully embedded.

Institutional risk flags are probability-weighted cautions, not forecasts of imminent collapse. Acting on them means reviewing positioning, not panic-selling.

Late-cycle equity positioning is characterised by exactly the conditions Barclays is flagging: five major asset managers including BlackRock and JPMorgan maintained overweight equity stances into mid-2026 while simultaneously warning that a 10-20% drawdown would not be surprising, a combination of constructive macro views and elevated risk acknowledgement that reflects how crowded the consensus bull case has become.

Based on Barclays’ three pain trade scenarios, investors can ask three direct questions of their own portfolios:

The IPO supply warning adds a fourth consideration: investors who participate in IPOs or hold funds that allocate to new issuance face near-term capital absorption pressure that can drag on existing positions mechanically, regardless of sentiment.

Pain trades by definition arrive at unexpected moments and cannot be timed with precision. The value of Barclays’ warning is in the positioning review it prompts, not in predicting the exact catalyst or date. The 2021 IPO comparison serves as a reminder: record issuance years can coincide with near-term market stress even when underlying fundamentals remain intact.

Barclays’ broader cross-asset framing suggests the risks are interconnected. A single trigger, such as heavy IPO supply absorbing capital, can amplify positioning risk already embedded in crowded AI trades. The note functions best as a self-assessment framework, one that works regardless of portfolio size.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements regarding potential market scenarios are speculative and subject to change based on market developments and positioning shifts.

A pain trade is a market move that inflicts the greatest damage on the largest number of investors because it runs directly against the most crowded positioning at the time. The more lopsided the positioning, the more severe the reversal when it occurs.

Heavy IPO supply forces institutional investors to allocate new capital to incoming listings, which often means trimming existing positions. This creates mechanical selling pressure on current holdings regardless of underlying sentiment or fundamentals.

Barclays named three scenarios: an equity decline paired with a bond market rally, outperformance by European and rest-of-world markets relative to US equities, and a rotation away from AI and semiconductor names toward consumer stocks and bond proxies such as utilities and dividend payers.

Multiple major institutions have independently flagged extreme crowding in AI and technology positions. Bank of America, JPMorgan, Goldman Sachs, and Morgan Stanley have all warned about concentration risk in semiconductors, hyperscalers, and AI infrastructure names, with JPMorgan describing crowding as reaching new extremes heading into 2026.

Investors can audit three areas of their portfolio: their fixed income allocation relative to equities, their US versus non-US market tilt, and their concentration in AI infrastructure, semiconductor, and hyperscaler names through individual stocks or thematic ETFs. Barclays frames the warning as a positioning review checklist, not a signal to panic-sell.