Why Goldman Sees AI Infrastructure Leading a 21x Market

48 mins ago

Three companies that most investors stopped watching years ago, Micron Technology, Lumentum Holdings, and Intel, posted combined revenue growth between 70% and 90% year over year in early 2026. The AI hardware stocks story has centred on Nvidia, AMD, and the hyperscalers building GPU clusters. But the physical infrastructure underneath those clusters, specifically the memory, optical interconnects, and inference-stage processors that make them function, depends on companies the market had largely written off. Their recent earnings suggest the AI buildout has created a second wave of hardware winners, and the investment case for each is structurally distinct. What follows is an analysis of the specific technical role each company plays, what their financial results reveal about demand durability, and how to evaluate the three as a portfolio rather than a single trade.

The conversation around AI investment has concentrated at two points: the chip designers building accelerators and the cloud providers buying them. That framing accounts for the compute layer. It does not account for the physical infrastructure that makes compute possible at scale.

AI training and inference workloads require three things beyond the accelerator chip itself. They need high-bandwidth memory to feed data to those accelerators fast enough that the silicon does not sit idle. They need optical interconnects to link hundreds or thousands of GPUs across racks and buildings at speeds electrical copper cannot sustain. And they need CPU capacity to handle the growing tier of inference workloads where GPU economics are unfavourable.

McKinsey projects the global semiconductor market will reach $1.6 trillion by 2030, with value accruing not only to logic chips but also to memory and advanced interconnect technologies feeding data-hungry AI accelerators.

Micron, Lumentum, and Intel occupy exactly these three roles. Their core competencies predated the AI cycle, but their products are now structurally embedded in every major AI deployment. The Deloitte 2026 semiconductor outlook frames memory and connectivity vendors as second-order beneficiaries of AI data-centre investment, a category the market has been slow to price.

The scale of capital flowing into AI infrastructure provides the demand foundation for all three companies discussed here: US IT spending reached a record 4.9% of GDP in Q1 2026, and the AI investment boom driving that figure has concentrated its rewards most heavily in the infrastructure and energy layer, including semiconductors and advanced interconnects, rather than in application-layer stocks where monetisation remains contested.

The simplest way to understand Micron’s re-emergence is to start with a constraint. An AI accelerator chip, no matter how powerful, can only process data as fast as that data arrives. If memory cannot feed the chip at sufficient bandwidth, the chip stalls. This is not a theoretical limit; it is the binding constraint on training throughput for large language models and the reason high-bandwidth memory has become architecturally non-negotiable.

HBM solves the bandwidth problem by stacking memory dies vertically and connecting them with through-silicon vias, achieving data throughput that conventional DRAM, arranged in flat packages, cannot approach. Nvidia’s H100 and H200 accelerators cannot operate at full capacity without HBM modules attached. This makes HBM supply a gating factor on AI training infrastructure, and it gives suppliers like Micron pricing power the company has not historically held in standard DRAM markets, where pricing has been cyclically brutal for decades.

HBM supply constraints have already demonstrated their market-repricing power: Micron, Sandisk, and SK Hynix posted combined gains exceeding 250% over 30 days ending 12 May 2026, with HBM capacity at SK Hynix and Micron sold out through 2026-2027, a condition driven by manufacturing complexity around through-silicon via packaging that cannot be resolved quickly even with capital investment.

Constrained HBM supply paired with structurally elevated demand has changed Micron’s earnings architecture. The Deloitte 2026 outlook confirms that server DRAM and HBM are experiencing structurally higher demand due to AI training and inference workloads, not a single product-cycle bump.

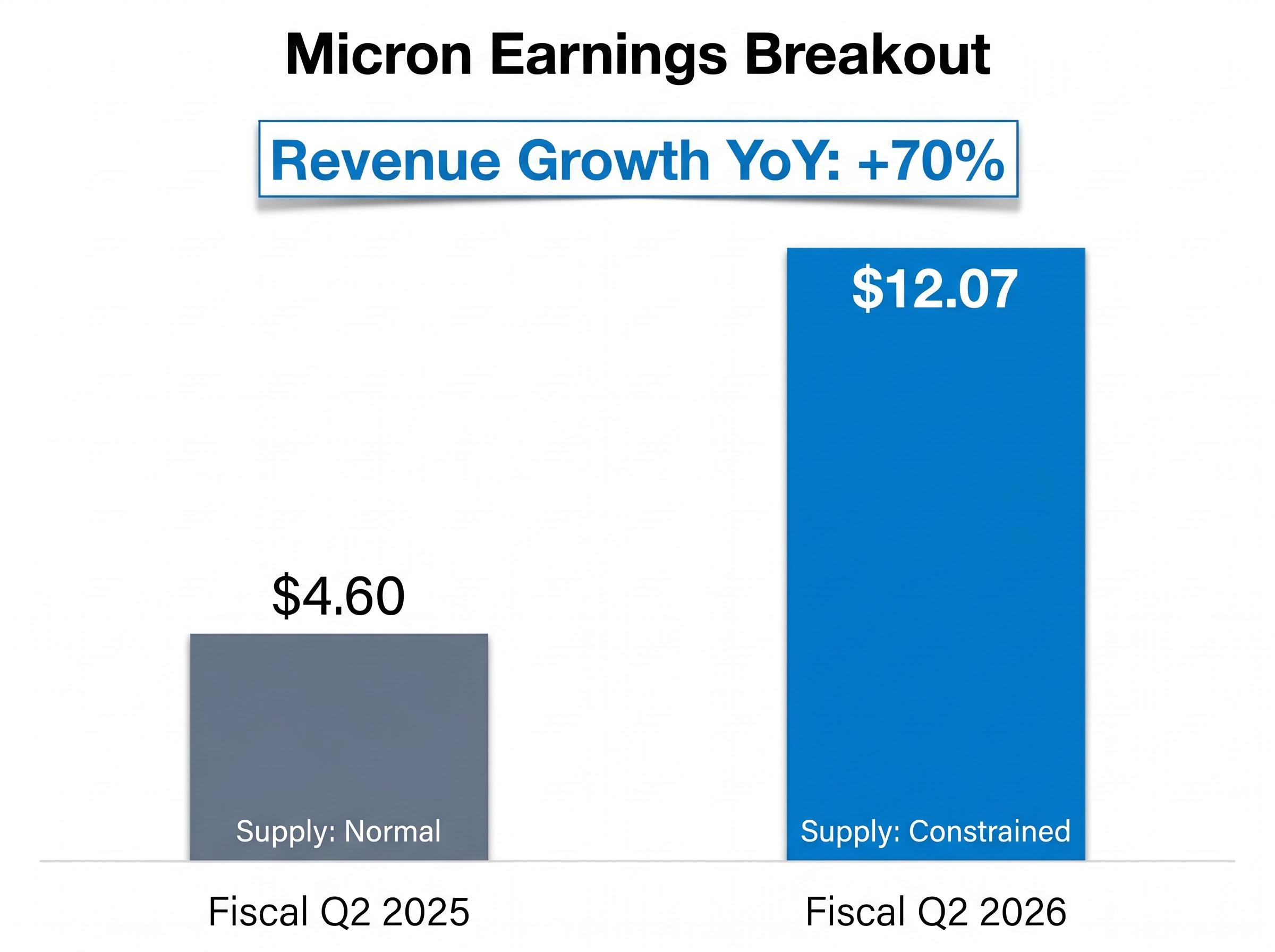

The financial results confirm the thesis rather than constitute it. In fiscal Q2 2026 (quarter ended 27 February 2026), Micron reported revenue growth of 70% year over year. Earnings per share climbed to $12.07, up from $4.60 in the prior-year period, a near-tripling that reflects what happens when a commodity memory supplier finds itself inside a supply-constrained, technically differentiated product category. Management commentary affirmed that favourable supply-demand dynamics are expected to persist in the near term.

| Period | Revenue Growth YoY | EPS | Supply Dynamic |

|---|---|---|---|

| Fiscal Q2 2025 (prior year) | Baseline | $4.60 | Normal |

| Fiscal Q2 2026 | +70% | $12.07 | Constrained |

When an AI cluster scales from dozens of GPUs to thousands, the physical connections between those processors hit a wall. Electrical copper links lose signal integrity and generate heat at the bandwidth densities AI workloads demand. Optical fibre interconnects solve both problems, transmitting data at the speed of light with negligible heat penalty, and they are the established solution at every hyperscale data centre operating today.

Lumentum Holdings manufactures the optical components that make these connections work. The company’s fiscal Q3 2026 results (quarter ended 28 March 2026) showed revenue growth of 90% year over year, and the company returned to GAAP operating profitability after running operating losses in the prior-year period. That operating turnaround, achieved alongside a near-doubling of revenue, indicates the AI demand inflection has passed the threshold where Lumentum’s cost base becomes leverageable.

Two forward catalysts sharpen the outlook:

CEO Michael Hurlston identified co-packaged optics and optical circuit switches as forward earnings drivers, framing both as capacity expansions that could materially enhance the company’s revenue trajectory.

According to STMicroelectronics’ 2025 semiconductor trend report, photonic integrated circuits “increase the speed and capacity of data transfer,” directly enabling AI neural network and neuromorphic computing applications. Lumentum’s 52-week trading range of $71.04 to $1,085.68 illustrates the magnitude of the re-rating since AI demand reached the company’s product lines.

The investment cases for Micron and Lumentum appear to describe different products in different markets. One makes memory chips; the other makes optical components. The connection between them becomes visible when the AI data centre is understood as a system rather than a collection of individual parts.

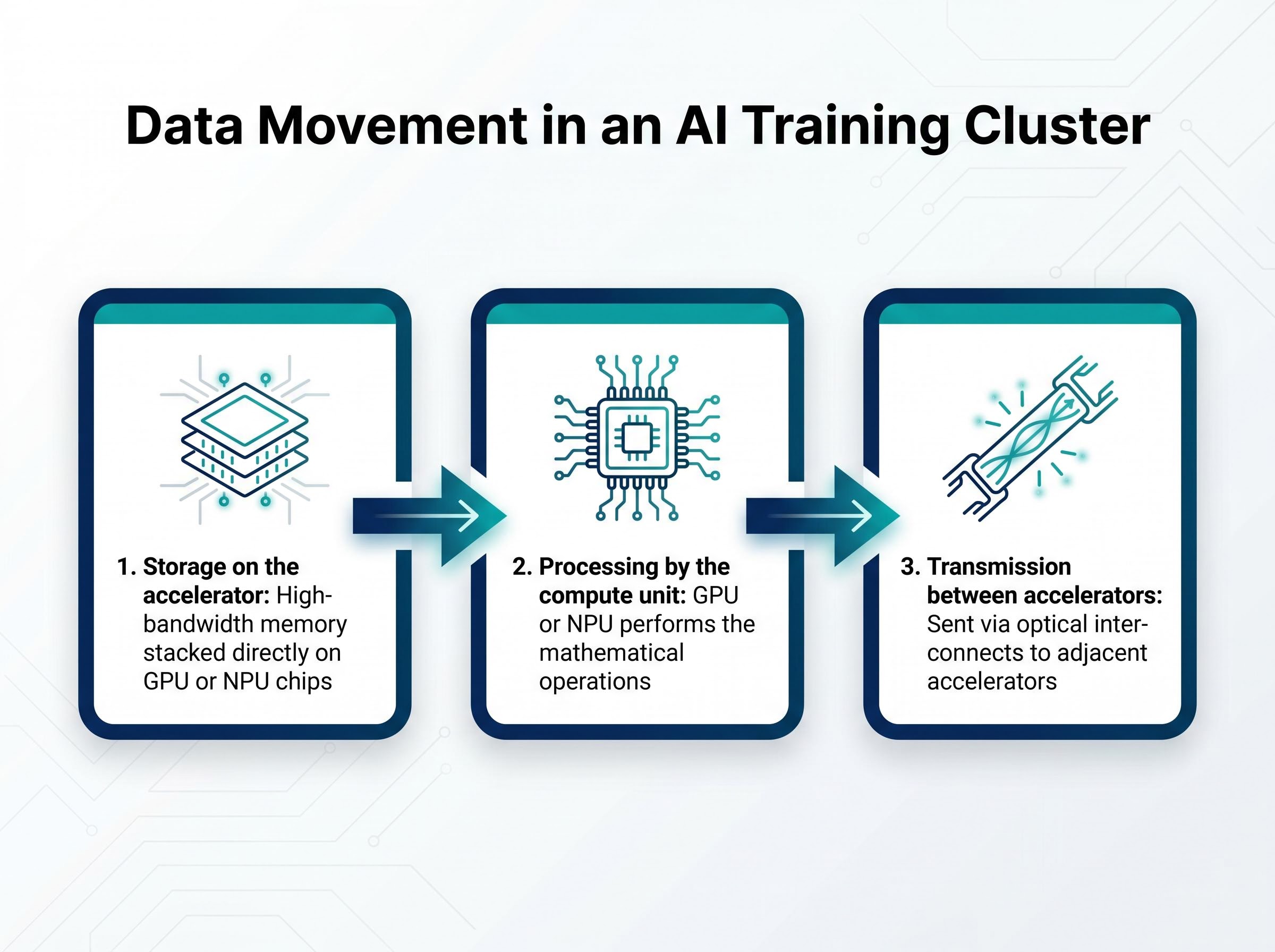

An AI training cluster moves data through three stages:

HBM and optical interconnects solve the same underlying problem from different positions in the architecture: moving data fast enough that compute does not stall. Memory handles the vertical movement of data into and out of the processor. Optics handle the horizontal movement of data across the cluster.

This shared logic explains why both categories are experiencing structurally elevated demand as AI workloads scale. According to the Deloitte 2026 outlook, advanced packaging and high-speed interconnects are identified as components needed to overcome memory bandwidth bottlenecks in AI systems. McKinsey’s semiconductor research reaches the same conclusion: value will accrue to memory and advanced interconnect technologies, not only to the logic chips that sit between them. The demand is structural, not dependent on a single customer or model generation.

Hyperscaler capital expenditure of approximately $725 billion in 2026, with a projected trajectory toward $1 trillion annually by 2027, flows directly into the hardware categories that Micron, Lumentum, and Intel supply, and the $130 billion spent by the four largest US cloud operators in Q1 2026 alone confirms that demand is not a forecast but a procurement reality already translating into order books.

Intel’s position in this analysis is structurally different from Micron or Lumentum, and that difference is the point.

As AI workloads mature, a growing share of compute shifts from training to inference: running trained models to generate predictions, recommendations, and responses. Inference runs at the edge, in enterprise environments, and in cost-sensitive deployments where GPU economics are unfavourable. A retailer running product recommendations, a hospital processing diagnostic imaging, a bank scoring credit applications in real time; these workloads can run on x86 CPUs at a fraction of GPU cost. That creates renewed structural demand for the processor category Intel has dominated for decades.

Intel has secured partnerships with major AI-focused companies, supporting a return to revenue growth. Management commentary, as of May 2026, frames the turnaround as developing over coming months and years. The company’s multi-decade technology leadership provides a foundation, but the recovery timeline is longer and the execution risk higher than for companies already delivering results.

The contrast with Micron and Lumentum is direct. Both of those companies are reporting triple-digit EPS growth or operating turnarounds driven by AI demand that has already arrived. Intel’s gross margin of approximately 35.90% reflects a business still rebuilding its financial architecture. The 52-week trading range of $18.96 to $132.75 illustrates the volatility, and the approximately $621 billion market capitalisation (as reported by the Motley Fool on 17 May 2026) reflects investor expectations that are priced for recovery rather than confirmed by it.

| Company | Recent Revenue Growth | Profitability Status | Recovery Stage | Primary AI Role |

|---|---|---|---|---|

| Micron | +70% YoY | EPS $12.07 (near-tripled) | Delivering | HBM and server DRAM |

| Lumentum | +90% YoY | Returned to GAAP profitability | Delivering | Optical interconnects |

| Intel | Recovery stage | Gross margin ~35.90% | Early | Inference-stage CPUs |

Micron, Lumentum, and Intel all benefit from the same underlying AI infrastructure buildout. They do not represent the same investment.

Micron and Lumentum are already delivering AI-driven earnings growth. Micron’s EPS of $12.07 in fiscal Q2 2026, up from $4.60 a year earlier, and Lumentum’s 90% revenue growth alongside a return to GAAP operating profitability, indicate that the demand inflection has translated into financial results, not just revenue estimates. The structural demand case from Deloitte and McKinsey, pointing toward multi-year elevated demand for memory and optical interconnects, reduces the probability that these results are a one-cycle anomaly.

Intel represents a different question: not whether the AI demand tailwind is real, but whether the company can rebuild execution capacity to capture it ahead of ARM-based and custom silicon alternatives. The timeline is longer. The execution risk is higher.

Investors evaluating all three should ask different questions of each:

The U.S. government’s commitment of CHIPS Act incentives for domestic HBM production, including a preliminary agreement directing $450 million toward SK Hynix’s advanced packaging fabrication facility on U.S. soil, underscores that supply-chain security for high-bandwidth memory has become a matter of national industrial policy, not merely a commercial procurement question.

Treating these three companies as a single trade on AI hardware will misprice the risk in at least one of them. The more rigorous framework is three distinct theses within the same demand cycle, sized according to where each company sits on the risk-return spectrum.

For investors wanting to apply a rigorous valuation framework to Micron and Intel specifically, our dedicated guide to semiconductor stock valuations examines the distinct tools appropriate for each stock type: PEG ratio for hypergrowth names, EV/EBITDA for cyclical recovery names, and cycle-adjusted forward estimates for memory stocks whose trailing earnings understate their medium-term trajectory, with worked multiples for Micron at under 9x forward earnings and Intel at 101x.

The AI investment story extends well beyond GPU designers. Every large-scale AI deployment requires memory fast enough to feed accelerators, optical connections capable of linking them, and CPU capacity to handle inference workloads where GPU economics do not hold. Micron, Lumentum, and Intel occupy those roles, and their recent financial results indicate the demand is structural rather than speculative.

What this analysis does not resolve is where consensus price targets will settle. Verifiable analyst targets for all three companies remain uncertain at the time of publication, and readers should conduct current due diligence before making position decisions.

The forward view is framed by industry data. McKinsey projects a $1.6 trillion global semiconductor market by 2030. The demand categories at the centre of this analysis, HBM, optical interconnects, and inference compute, are positioned inside that growth, not adjacent to it. The companies serving those categories have already demonstrated they can convert AI demand into earnings. The question for investors is whether that conversion is priced in, or still developing.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

AI hardware stocks extend beyond GPU designers like Nvidia and AMD to include companies supplying the physical infrastructure underneath AI clusters, such as Micron Technology for high-bandwidth memory, Lumentum Holdings for optical interconnects, and Intel for inference-stage CPUs.

High-bandwidth memory (HBM) stacks memory dies vertically using through-silicon vias to achieve data throughput that conventional DRAM cannot match, feeding AI accelerators like Nvidia's H100 and H200 at full capacity and making HBM supply a gating factor on AI training infrastructure.

Micron reported 70% year-over-year revenue growth in fiscal Q2 2026 (quarter ended 27 February 2026), with earnings per share climbing to $12.07 from $4.60 in the prior-year period, driven by constrained HBM supply and structurally elevated AI demand.

When AI clusters scale to thousands of GPUs, electrical copper links lose signal integrity and generate excessive heat at the required bandwidth densities; optical fibre interconnects transmit data at the speed of light with negligible heat penalty, making them the established solution in every hyperscale data centre.

Unlike Micron and Lumentum, which are already delivering AI-driven earnings growth, Intel is in an earlier recovery stage targeting the inference market, where trained AI models run in cost-sensitive environments where GPU economics are unfavourable, though execution risk and timeline remain higher.