A pension fund that never once ranked in the top quarter of its peer group in any single year somehow finished in the top 4% of all funds over a 14-year period. That result is not a paradox. It is a demonstration of what happens when a defensive investing strategy is maintained with discipline across full market cycles.

Most investors are taught to think about performance as the pursuit of exceptional outcomes: the right stock at the right time, the manager who sees what others miss. The defensive case inverts that framing entirely. The real edge in investing, this argument holds, is not in finding winners but in reliably not producing losers. The idea is associated closely with Howard Marks and Oaktree Capital, but its intellectual roots run through amateur tennis, bond mathematics, and the structural role of randomness in financial markets. What follows unpacks why avoiding bad investments compounds into superior long-term results more reliably than chasing exceptional ones, drawing on the loser’s game framework, the logic of fixed income, the mathematics of loss avoidance, and over a decade of institutional data.

The game most investors think they are playing (and why they are wrong)

The appeal of the “winner” model is intuitive. Find the best opportunities, act decisively, and outperform. It is the model that sells newsletters, fills conference halls, and populates the covers of financial magazines. It also misrepresents the game most participants are actually playing.

The distinction comes from Charlie Ellis’s article “The Loser’s Game,” which draws on an unlikely source: competitive tennis. In professional tennis, points are won. The player who hits the more brilliant shot, who executes with greater precision under pressure, earns the point through superior shot-making. In amateur tennis, the dynamic reverses. Points are lost. The player who makes fewer unforced errors wins, not because of brilliance but because the opponent defeats themselves.

Marks applies this distinction directly to investing. He partially agrees with Ellis’s conclusion but reaches it through a different lens. Where Ellis attributes the dynamic to market efficiency, Marks emphasises that the skill required to consistently exploit market inefficiencies is exceptionally rare. Most participants simply do not possess it, regardless of how sophisticated they believe their approach to be.

| Dimension | Professional Tennis / Active Stock-Picking | Amateur Tennis / Defensive Approach |

|---|---|---|

| How points are won | Superior shot-making / identifying mispriced assets | Opponent’s errors / avoiding self-inflicted losses |

| Primary skill required | Exceptional execution under pressure | Discipline and error minimisation |

| Analogous investment behaviour | Concentrated bets on high-conviction ideas | Consistent avoidance of catastrophic holdings |

From tennis court to trading floor

Translated into portfolio terms, investors lose to the benchmark not because other participants are brilliant but because they generate their own errors: overtrading, poor risk assessment, emotional decision-making during drawdowns. Marks’s specific framing is that exceptional skill capable of exploiting inefficiencies is rare, not universal. The primary question for most investors is not “how do I find the next great investment?” but “how do I stop making mistakes?”

When big ASX news breaks, our subscribers know first

What bond investing reveals about the logic of loss avoidance

If the tennis analogy opens the door, bond investing walks straight through it. Fixed income strips away the noise of equity speculation and reveals the loss-avoidance logic in its purest form.

Benjamin Graham and David Dodd described bond investing as a “negative art” in the 1940 edition of Security Analysis. The phrase captures something fundamental about how fixed income outperformance actually works. In a bond portfolio, every performing bond yields the same contractual return. There is no mechanism to “win more” on successful holdings. A bond that pays as promised delivers exactly the coupon and principal specified at issuance. The only variable is on the downside: which bonds default and how severely.

This structural reality makes loss avoidance not merely a preference but the only available source of edge. Three conditions create this dynamic:

- Uniform upside among performing bonds (all pay the same contractual return)

- Variable downside from defaults (losses range from partial to total)

- No amplification mechanism on winners (a bond cannot outperform its own coupon)

Oaktree Capital’s guiding principle distils this logic into a single sentence:

“If we can avoid the losers, the winners will take care of themselves.”

Understanding this mechanism in fixed income helps clarify why the same logic, applied to equities, is not a counsel of timidity. It is a structurally grounded strategy that recognises where the real edge lives for most market participants.

Why randomness breaks the link between good decisions and good outcomes

The defensive case does not rest on modesty alone. It rests on a structural feature of financial markets that most performance narratives ignore: luck.

For any investment situation, a distribution of possible outcomes exists. The most probable single outcome is still far from guaranteed to materialise. C. Jackson Grayson, in work referenced by Marks from his Wharton coursework beginning in 1963, captured this with a formulation that serves as a working definition of risk:

“More things can happen than will happen.”

Even correct probabilistic reasoning does not guarantee the expected result in any single instance. Events that are theoretically expected to occur often fail to happen, and when they do occur, they frequently do not happen within the anticipated timeframe. This is not an edge case. It is the baseline condition of investing.

The implication for strategy is direct. Approaches that depend on repeatedly hitting outlier outcomes face compounding probability headwinds. Each cycle requires the investor to be right again, and the distribution offers no guarantee of repetition. Strategies that avoid catastrophic outcomes, by contrast, are structurally more resilient to the randomness that markets deliver as a matter of course.

The survivor problem in active management

Nassim Nicholas Taleb’s Fooled by Randomness addresses the consequence of this dynamic at industry scale. Survivorship bias populates the top of performance league tables with managers whose results reflect fortunate conditions rather than repeatable skill. Good outcomes are mistakenly attributed to sound logic, generating false confidence in strategies that may not be replicable.

Dimensional Fund Advisors research on survivorship bias quantifies a specific distortion in how active fund performance is typically reported: the liquidation and merger of underperforming funds inflates the apparent median alpha of the surviving peer group by roughly 50%, meaning the active management track record that investors observe is structurally more flattering than the full population of decisions would produce.

The SPIVA U.S. Scorecard for Year-End 2024, published by S&P Dow Jones Indices in March 2025, provides the aggregate confirmation: 65% of large-cap active U.S. equity funds underperformed the S&P 500 over the measured period. That figure is consistent with a multi-decade pattern, illustrating how rare genuine repeatable outperformance is once luck is properly accounted for.

The mathematics of not losing: how consistency compounds into top-decile results

The pension fund case study that opens this article is worth examining in full, because the arithmetic proves itself.

An Oaktree Capital client pension fund ranked between the 27th and 47th percentile annually over 14 years. Not once did it break into the top quarter. In any single year, the result looked unremarkable. Over the full period, the fund achieved a composite ranking of approximately the 4th percentile, outperforming nearly all peers.

The mechanism is not mysterious. By never falling to the bottom of the annual distribution, the fund avoided the deep losses that permanently impair a portfolio’s starting base for the following year. The asymmetry of loss is the engine:

A 50% drawdown requires a 100% subsequent gain just to return to breakeven. Loss avoidance is arithmetically worth more than an equivalent gain.

The downside protection mathematics behind this asymmetry are well documented in institutional investment research: a portfolio that avoids a 50% drawdown does not merely preserve capital, it eliminates the need for the subsequent 100% gain that recovery would otherwise demand, compounding forward from a higher base throughout.

Funds that posted occasional top-5% years but suffered catastrophic reversals faced a different compounding path. Their exceptional gains were erased by the drawdowns that followed, and the recovery mathematics worked against them from a diminished base.

| Year | Consistent Fund (Percentile) | Volatile Fund (Percentile) |

|---|---|---|

| 1-3 | 35th, 40th, 30th | 5th, 85th, 3rd |

| 4-7 | 27th, 45th, 33rd, 47th | 10th, 92nd, 8th, 88th |

| 8-11 | 38th, 29th, 42nd, 35th | 4th, 90th, 15th, 80th |

| 12-14 | 31st, 44th, 36th | 6th, 87th, 12th |

| 14-Year Composite | ~4th percentile | ~40th-50th percentile |

The principle at work is not the presence of extraordinary gains. It is the absence of extraordinary losses. That absence, repeated consistently, is what produces the exceptional long-run composite result.

What defensive investing actually requires in practice

Defensive investing is not passive investing. It is not low-engagement investing. It requires active discipline in saying no, maintaining consistent principles under pressure, and resisting the temptation to chase recent outperformers.

Classifying market selloffs before committing capital is where the loser’s game framework connects to specific decision-making: distinguishing an irrational overreaction (where underlying moats remain intact) from a structural disruption (where the industry’s future earnings may not exist) is precisely the kind of disciplined assessment that separates loss avoidance from simply holding cash through every decline.

Oaktree Capital was founded on 10 April 1995. Its six foundational principles were written at inception and have not been modified since. They centre on risk control, consistency, scepticism of macro forecasting, and a preference for long-term holdings in underpriced assets over market timing. The fact that these principles survived unchanged through multiple market cycles is itself an expression of the philosophy: conviction in a framework must outlast the environments that test it.

In March 2025, AQR Capital Management’s Cliff Asness discussed simpler approaches to achieving lower-risk equity exposure through diversification into uncorrelated assets or defensive and quality tilts, reinforcing that risk reduction through disciplined allocation remains a practitioner-level priority rather than a theoretical exercise.

The psychological difficulty is real. In a rising market, defensive positioning feels like underperformance. Peers who concentrated into momentum names post stronger short-term numbers. The social and professional pressure to match those leaders is one of the primary ways defensive discipline breaks down.

The psychological asymmetry that makes losses feel roughly twice as painful as equivalent gains is a core driver of every failure mode on this list; loss aversion in investor behaviour, formally documented by Kahneman and Tversky in 1979, is not a personality quirk but a structural bias that costs investors an estimated 1-2 percentage points in annual returns through poorly timed exits and delayed re-entries.

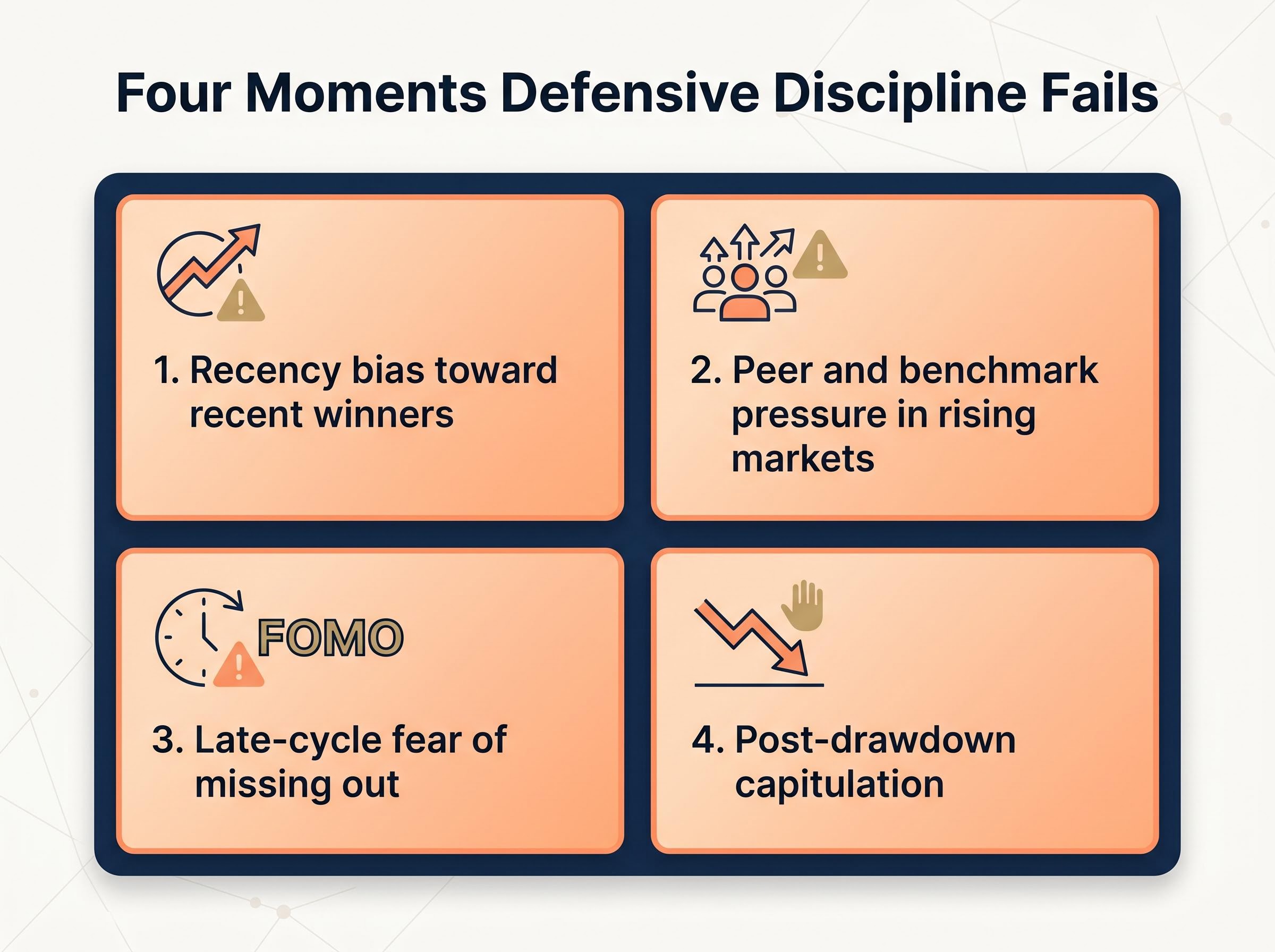

The four moments when defensive discipline is most likely to fail

- Recency bias toward recent winners: investors overweight whatever performed well in the most recent period, abandoning diversified positioning to chase returns that may not repeat

- Peer and benchmark pressure in rising markets: when concentrated strategies outperform in the short term, consistent positioning feels costly and career-threatening for professional managers

- Late-cycle fear of missing out: as asset prices extend and euphoria builds, the pressure to participate overrides the discipline to stay cautious

- Post-drawdown capitulation: after suffering losses, investors sell at the worst moment, locking in damage precisely when the defensive posture’s value is about to materialise

Each failure mode involves abandoning the strategy precisely when it is most important to maintain it. The irony of defensive investing is that its benefits are invisible during the periods when discipline is hardest to sustain.

The next major ASX story will hit our subscribers first

The evidence gap that most active managers cannot close

The loser’s game is not merely a philosophy. It is an empirically documented outcome at industry scale.

The SPIVA U.S. Scorecard for Year-End 2024 (S&P Dow Jones Indices, March 2025) found that 65% of large-cap active U.S. equity funds underperformed the S&P 500 over the reported period.

That finding is not a single-year anomaly. S&P Dow Jones Indices has published annual SPIVA Scorecards continuously, and the pattern of active fund underperformance relative to passive benchmarks over long horizons is persistent and multi-decade. The evidence extends beyond U.S. borders:

The structural causes of active fund underperformance go beyond individual manager skill gaps; regulatory position limits under the Investment Company Act of 1940 cap individual fund holdings at 5% of assets, making it mathematically impossible for most active funds to match benchmark weights when single S&P 500 constituents exceed 6-7% of index weight, a constraint that compounds the randomness problem Marks and Taleb each describe.

Active versus passive performance evidence is not confined to U.S. markets: in Australia, 74% of active equity managers failed to beat the S&P/ASX 200 in 2025, and over a 15-year horizon that figure extends to 87%, confirming that the structural dynamic Marks describes is a global condition rather than a feature of any single market’s efficiency or size.

- U.S.: 65% of large-cap active funds underperformed the S&P 500 (Year-End 2024)

- Europe: A majority of active managers underperformed their benchmarks over 5- and 10-year periods (SPIVA Europe, 2025)

- Global: Consistent underperformance patterns documented across most regions and time horizons (SPIVA Global, 2025)

If the majority of active managers trail their benchmarks over measured periods, they are not playing a winner’s game. They are playing a loser’s game, and losing it. The SPIVA data transforms the defensive investing argument from a theoretical position into a statistical reality that holds across decades and geographies.

Consistency is the strategy, not the consolation prize

The loser’s game thesis is not a counsel of mediocrity. It is a precise claim about where the real edge in investing lives for most participants. The mathematics of loss avoidance, the structural logic of fixed income, the role of randomness, and the aggregate evidence from active management all converge on the same conclusion: reliably avoiding bad outcomes compounds into results that sporadic brilliance cannot match.

The pension fund that ranked between the 27th and 47th percentile every year for 14 years and finished in the 4th percentile did not achieve that result by accident. It achieved it by never being catastrophically wrong. No single year was exceptional. The composite was.

“If we can avoid the losers, the winners will take care of themselves.”

The most important investment question may not be “what am I trying to win?” It may be “what am I working hardest not to lose?”

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.