Are Rate Hikes Actually Bad for Stocks? What the Data Shows

8 mins ago

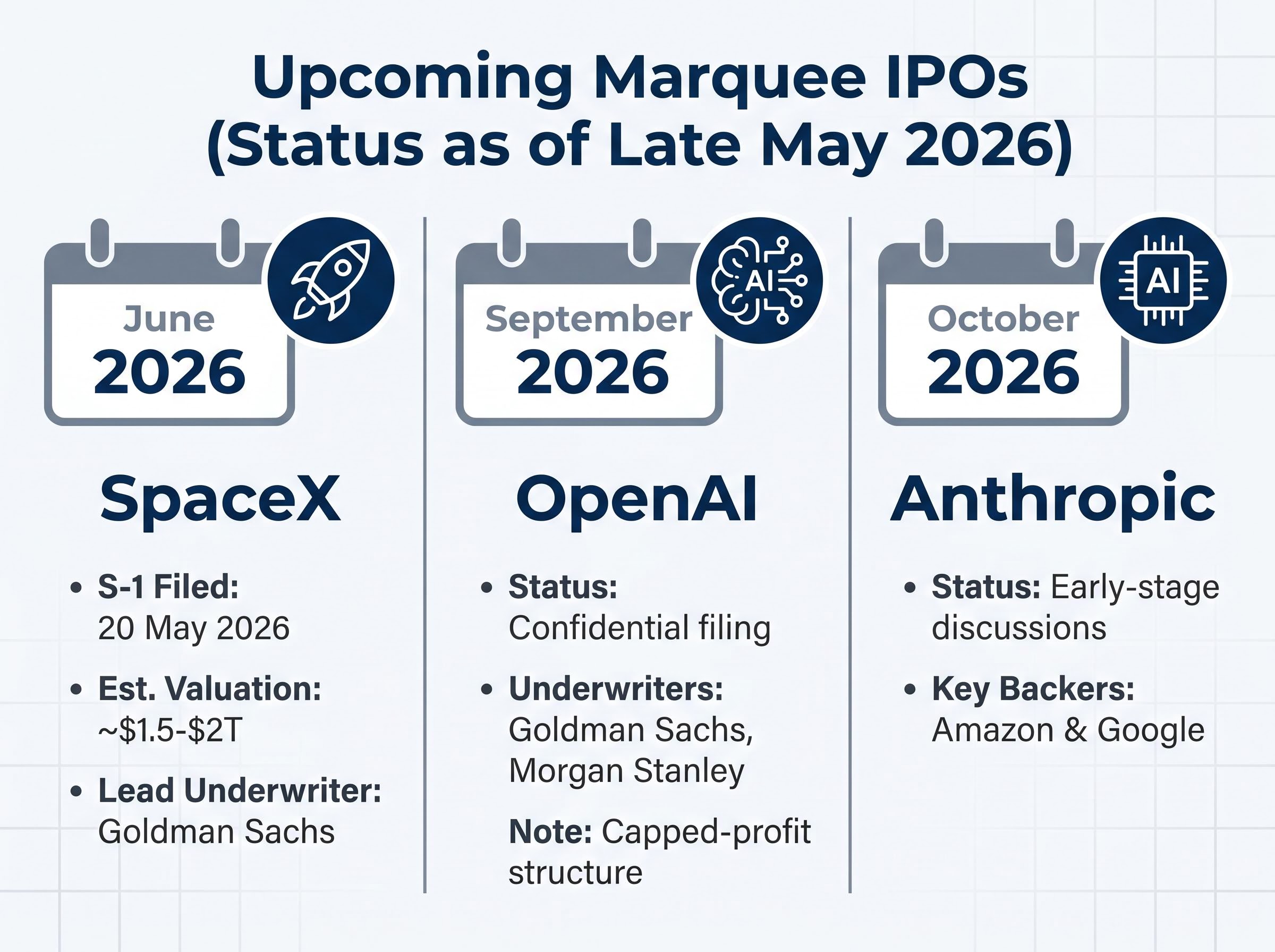

More than 70% of Polymarket bettors wagered that SpaceX will debut above a $2 trillion valuation, even as Wall Street analysts placed the figure closer to $1.5 trillion. That gap between crowd expectation and professional estimate captures something important about how retail investors typically approach marquee IPOs. SpaceX filed its S-1 with the SEC on 20 May 2026, targeting a Nasdaq listing under ticker SPCX as early as June. OpenAI is preparing a confidential filing aimed at a September 2026 debut. Anthropic is in early discussions for a possible October 2026 listing. All three are arriving in a market already feverish about AI-linked equities, which makes this a precise moment to ask: what does participation in high-profile IPOs actually look like for retail investors who buy at or near the offering price, and what happens over the following three to five years? This article explains the structural mechanics of the IPO process, the documented long-run performance pattern, and a practical framework for evaluating whether the hype around any specific listing justifies the risk.

Three category-defining private companies approaching public markets within the same calendar window is unusual by any historical standard. SpaceX has the most advanced timeline: its S-1 is public on EDGAR, Goldman Sachs is the lead underwriter, and roadshow activity is expected to begin around 8 June 2026. OpenAI is further back, working with Goldman Sachs and Morgan Stanley on a confidential filing preparation targeting September 2026. Anthropic, backed by strategic investors including Amazon and Google, is in early-stage discussions for a possible October 2026 listing.

Marquee IPO filing clusters, such as SpaceX and Oura Health both submitting S-1 documents on the same day alongside concurrent preparations by OpenAI and Anthropic, have historically signalled that insiders believe valuations are near peak; the timing tends to favour sellers over buyers regardless of how credible the underlying businesses are.

The following table summarises each company’s publicly reported status as of late May 2026.

| Company | Filing status | Lead underwriter(s) | Valuation reference | Tentative timing |

|---|---|---|---|---|

| SpaceX | Public S-1 on EDGAR | Goldman Sachs | ~$1.5-$2T+ range (analyst vs. Polymarket estimates) | June 2026 |

| OpenAI | Confidential filing in preparation | Goldman Sachs, Morgan Stanley | Not publicly set | September 2026 |

| Anthropic | Early-stage discussions | Not confirmed | Not publicly set | Possibly October 2026 |

The hype is already propagating beyond the IPOs themselves. Companies holding SpaceX stakes rallied on news of the S-1 filing, a sign that secondary-market enthusiasm is spilling into adjacent equities. Retail investors who understand this full landscape of concurrent listings are better positioned to assess whether they are responding to one company’s fundamentals or to a broader sentiment wave. The distinction matters for any allocation decision.

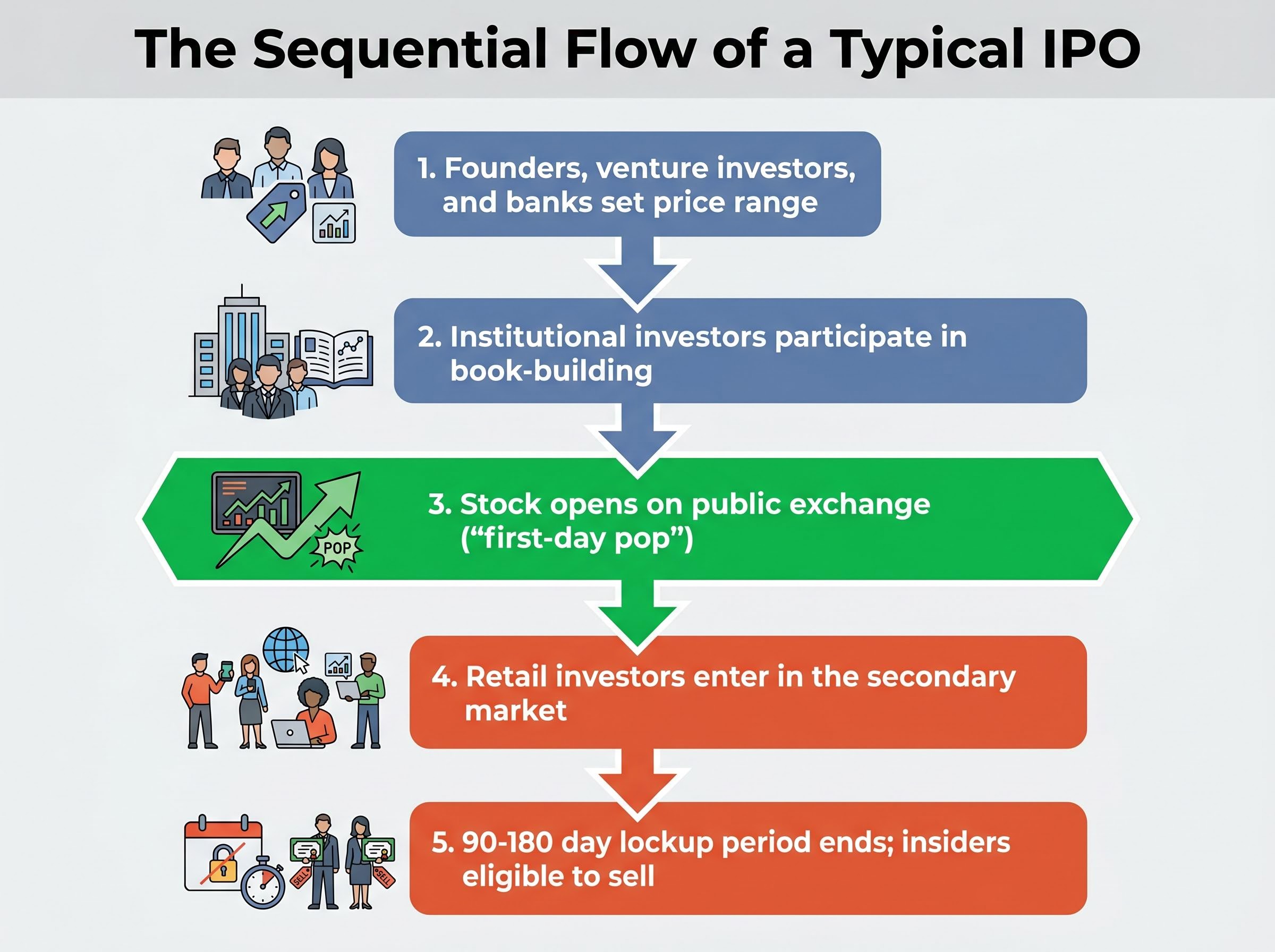

The word “offering” implies a gift. The mechanics suggest otherwise. An IPO is a liquidity event, a structured process that allows founders, early employees, and venture capital investors to convert private equity into public-market cash. Understanding who the process is designed to serve changes how a prospective buyer should evaluate the opportunity.

The sequential flow of a typical IPO works as follows:

The first-day pop is not an accident. Underwriters have a direct financial incentive to price shares at a level that generates a reliable opening-day gain. Allocating below-market shares to institutional clients sustains deal flow; those clients return for the next offering. Academic consensus holds that this underpricing is partly engineered rather than a market miscalculation.

“The IPO is primarily a liquidity event for people who got in before you.”

Most retail buyers are not “getting in early.” They are entering after founders priced their exit, after institutions received their allocations, and before the lockup expiry introduces a fresh supply of insider shares into the market.

The most comprehensive longitudinal record of U.S. IPO performance sits on the University of Florida website, maintained by Professor Jay Ritter. The dataset spans decades, is updated periodically (now incorporating 2021-2023 cohorts), and measures how IPOs perform relative to matched non-IPO firms and broad indices over multi-year horizons.

Professor Jay Ritter’s IPO long-run returns dataset, maintained at the University of Florida and updated through 2024, documents multi-year performance across thousands of listings and consistently shows IPO cohorts underperforming matched non-IPO firms and broad indices over three-to-five year horizons.

The established finding is consistent: IPOs as a cohort tend to underperform over three-to-five year periods following their listing. This is not an outlier result from a single study. It emerges across thousands of IPOs and has held through multiple market cycles.

The IPO underperformance data spanning 1980 to 2024 quantifies this drag precisely: newly listed companies trailed comparably sized established peers by an average of 3.3% per year over their first five years, a compounding gap that turns a $10,000 position into roughly $2,100 less than an equivalent allocation to a seasoned public company.

IPOs, as a class, have historically underperformed broader market benchmarks over three-to-five year horizons following their debut.

The 2020-2021 IPO wave provided the most recent and most vivid illustration of this pattern. Several high-profile listings that debuted to enormous enthusiasm subsequently declined sharply from their early trading levels:

The 2000 dot-com era remains the historical extreme case, where a surge in IPO activity from unprofitable companies preceded a severe market correction. The pattern is not anecdotal. It emerges consistently across academic datasets covering thousands of listings over decades, which means individual company failure does not explain it. The structural dynamics of the process itself appear to be the driver.

The general IPO caution is real. But is the AI wave genuinely different? The answer requires understanding a concept that is more important than any individual company’s revenue growth: the expectations gap.

Market returns are driven by the difference between actual outcomes and prior expectations, not by actual outcomes alone. A company can report strong revenue growth and see its stock decline if that growth was already fully priced into the shares. Conversely, a mediocre result can lift a stock if the market had priced in something worse. When enthusiasm is widespread and expectations are already elevated, the bar for positive surprise rises accordingly.

The current AI-sector environment is one where extraordinary enthusiasm is already reflected in prices. Nvidia’s market capitalisation reached approximately $5 trillion as of late May 2026, a figure that embeds enormous forward expectations across the entire AI supply chain. SpaceX, OpenAI, and Anthropic are not arriving into a market that is unaware of their potential. They are arriving into one that has been pricing AI-linked growth for years.

The SpaceX valuation mechanics underlying the $2 trillion figure involve a 250x EBITDA multiple, a ratio that prices in decades of forward growth and leaves analyst assessments flagging approximately 30% overvaluation risk even before accounting for the structural IPO entry disadvantages that retail buyers face.

“When everyone already expects greatness, even a great result can disappoint.”

Fisher Investments, in a 22 May 2026 editorial, did not assert that an AI bubble exists. It did assert that elevated expectations reduce the probability of positive surprise, a dynamic that applies directly to IPOs entering at peak-cycle sentiment. A parallel from South Korea’s chipmaker sector illustrates the point: as Bloomberg’s Shuli Ren reported on 21 May 2026, domestic retail investors were buying into chipmakers at the same time that international institutional investors were reducing their concentration exposure, a sentiment divergence that often precedes mean reversion.

Retail investors entering AI-linked IPOs in mid-2026 are not buying into an undiscovered opportunity. They are buying into one of the most widely discussed and enthusiastically anticipated IPO waves in recent memory, which is precisely the environment where the expectations gap works against them.

None of the above means every IPO is a poor investment. Some listings do generate strong long-run returns for public-market investors. The question is how to distinguish those from the ones that don’t, before the excitement of the roadshow makes the distinction feel irrelevant.

The following four diagnostic questions apply to SpaceX, OpenAI, Anthropic, or any future listing:

Two additional considerations apply to the current wave specifically. OpenAI’s capped-profit corporate structure creates complexity around shareholder rights that requires due diligence beyond standard IPO analysis. Anthropic’s heavy strategic ownership by Amazon and Google raises potential alignment questions for public minority shareholders whose interests may diverge from those of the dominant backers.

The relevant question is never “is this a great company?” It is “is this a great investment at this price for this investor at this entry point?”

Investors wanting to apply the diagnostic framework above to the actual SpaceX filing will find our comprehensive walkthrough of the SpaceX S-1 prospectus covers the specific sections that reveal revenue structure, governance arrangements, and the valuation step-up from the last verified $800 billion secondary transaction, with guidance on what to look for before the June roadshow closes.

SpaceX, OpenAI, and Anthropic may well be enduringly important companies. Their long-term business trajectories are not in serious question. But business quality and public-market entry price are different questions, and conflating them is how retail investors have historically overpaid for IPO shares across every cycle.

The structural features described in this article, insider liquidity prioritisation, lockup dynamics, institutional allocation advantages, are not unique to these three companies. They are features of every IPO. They were present in 2000, in 2012, in 2021, and they will be present in 2027 and beyond.

Fisher Investments’ editorial conclusion captures the broader point: a constructive market outlook does not translate into an IPO-specific recommendation. Some institutional investors are already positioning toward leadership rotation away from U.S. technology and into international and non-tech equities, a thesis that implies AI-sector multiple compression is plausible even if underlying businesses perform well.

“The question is never whether a company is great. The question is whether the offering price already assumes it.”

The best time to evaluate an IPO is before the roadshow begins, not after the third CNBC segment has aired. Retail investors who build the habit of separating admiration for a company from the price of its public offering will make better decisions across every IPO cycle they encounter.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections and forward-looking statements are subject to market conditions and various risk factors.

IPO investing refers to buying shares in a company at or around the time it lists on a public stock exchange. Retail investors typically cannot access shares at the offering price and instead purchase in the secondary market after institutional allocations have been filled, meaning their effective entry price is often higher than the headline figure.

Academic research, including Professor Jay Ritter's dataset at the University of Florida covering thousands of listings, consistently shows IPO cohorts underperforming matched non-IPO firms and broad indices over three-to-five year horizons, largely because insiders price their exit, institutions receive advantaged allocations, and lockup expiries create fresh selling pressure after retail buyers have entered.

A lockup period is a contractual restriction, typically lasting 90-180 days after listing, that prevents insiders such as founders and early employees from selling their shares. When it expires, a wave of new supply enters the market, which often creates downward price pressure at the precise moment many retail investors are still holding their positions.

Investors should assess whether the company is profitable or has a funded path to cash generation, understand the lockup structure and when insiders can first sell, determine whether the offering price already embeds peak-cycle valuation multiples, and confirm whether they are realistically entering at the offering price or at a secondary-market markup after the first-day pop.

The expectations gap refers to the difference between actual company performance and what the market had already priced in. Because enthusiasm for AI-linked equities is already widely reflected in valuations, companies like SpaceX arriving at a market where Nvidia's capitalisation has reached roughly $5 trillion face a high bar for positive surprise, meaning strong business results can still disappoint shareholders if those results were already assumed.