Are Rate Hikes Actually Bad for Stocks? What the Data Shows

10 mins ago

Holding cash on the sidelines is either the most disciplined move in your portfolio or the quietest wealth-destroying habit you have. The difference has nothing to do with the strategy itself. It has everything to do with where you sit in your investing journey.

That distinction is the reason standard financial guidance feels contradictory. One source tells you “time in the market beats timing the market.” The next tells you to “keep dry powder for opportunities.” Both are correct. They are just talking to different people, and neither tells you how to figure out which one applies to you.

Here is a stage-by-stage framework for making that call honestly, including how to identify which camp you currently fall into, what the appropriate default looks like for your situation, and the specific behavioural trap that catches investors on both sides.

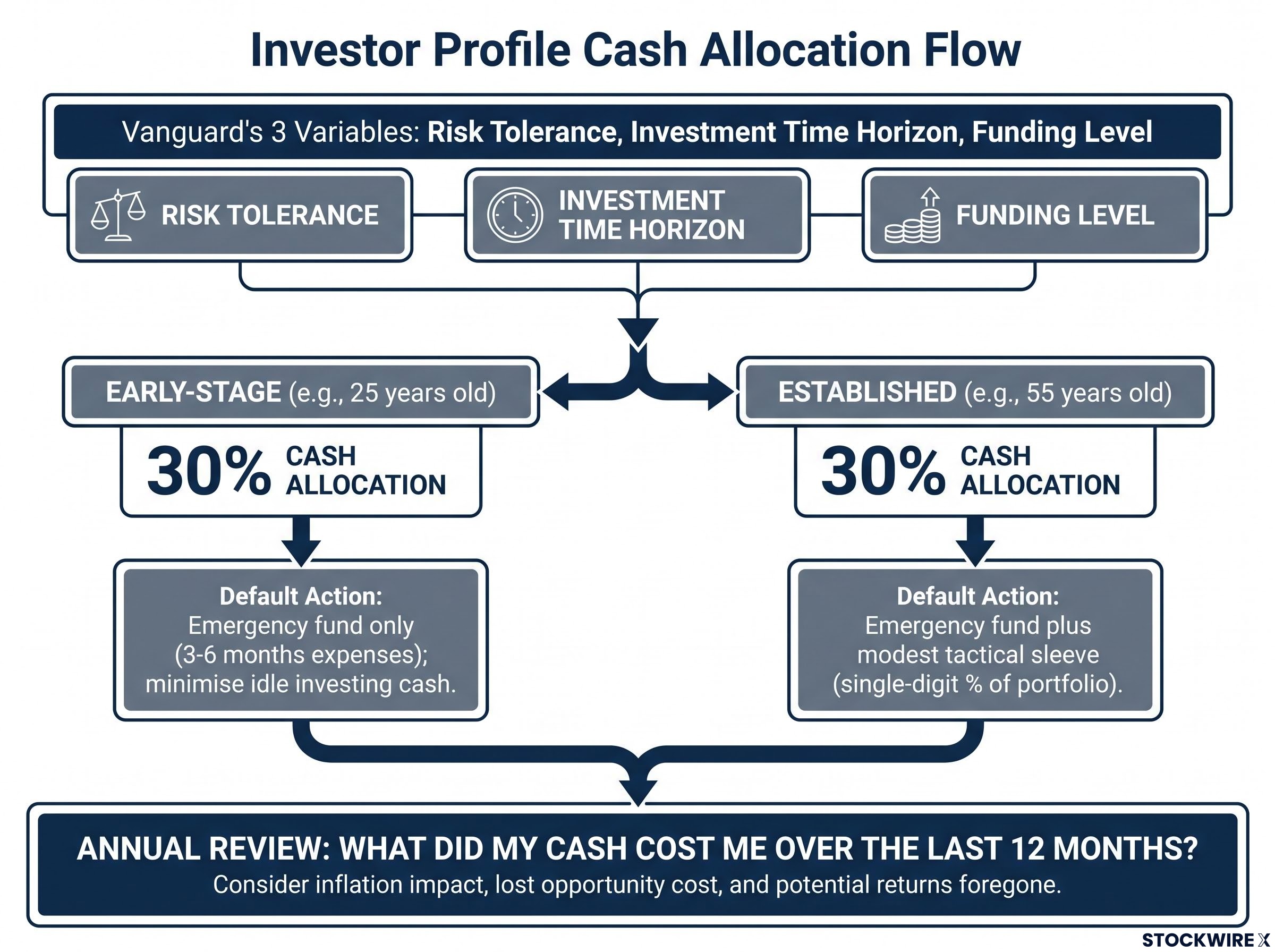

Picture two investors, both holding 30% of their savings in cash. The first is 25, a decade from their next major financial milestone, building wealth through regular contributions. The second is 55, with a portfolio generating enough income to cover most living expenses, a few years from retirement.

The 25-year-old is paying a compounding penalty every year that cash sits idle. The 55-year-old is preserving flexibility and controlling downside risk at exactly the stage where that trade-off makes sense. Same cash allocation. Opposite financial outcomes.

This is why no single “how much cash should I hold” rule works for everyone. The answer depends on three variables, formalised by Vanguard as a professional framework for determining appropriate cash allocations:

Before you ask “how much cash should I hold,” you need to answer a prior question: what phase of the journey are you actually in? Get the prior question wrong, and the cash figure is meaningless regardless of whose rule you follow.

If you are in the accumulation phase, your wealth grows through two engines: new contributions and compounding on invested assets. Cash contributes to neither. Every year your capital sits in a savings account instead of a diversified portfolio, the compounding clock does not pause; it runs against you.

The numbers make the cost concrete.

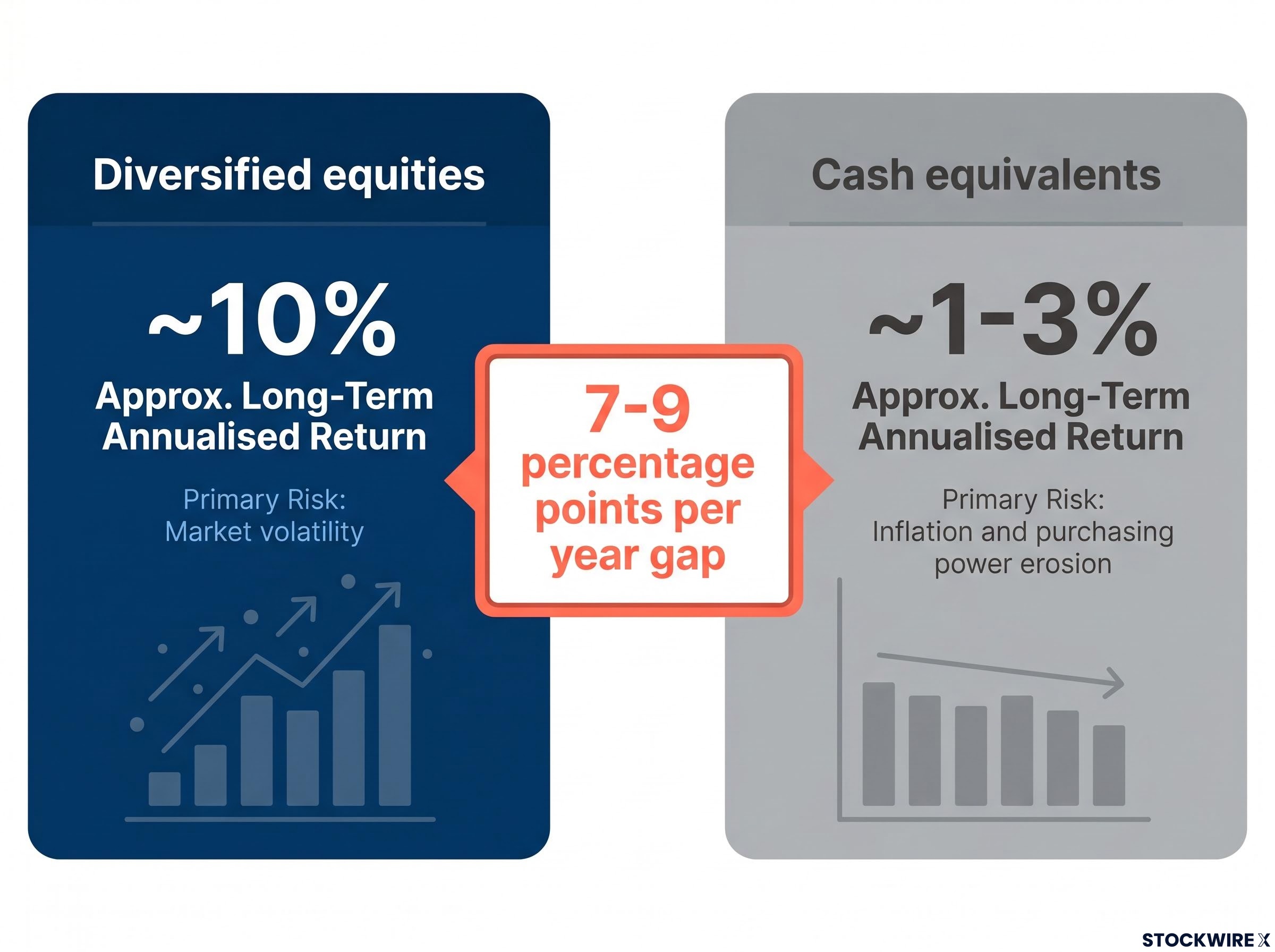

Stocks have delivered long-term annualised nominal returns of approximately 10%. Cash equivalents, such as Treasury bills and similar instruments, have typically returned approximately 1-3% annualised.

That gap, roughly 7-9 percentage points per year over long horizons, is not an abstraction. It is the quantifiable price of waiting for the “right moment” to invest. This pattern is well documented: investors who spend years accumulating savings without putting that capital to work forgo the compounding gains that cannot be recovered later. For early-stage investors, patience waiting on the sidelines carries a cost that compounds against you every year you wait.

The compounding cost of delayed contributions is more concrete than most investors expect: a five-year delay on $100 monthly at 7% annual returns costs approximately $20,400 in final portfolio value, a gap that cannot be closed by contributing more later because the compounding years themselves are irretrievable.

| Asset Type | Approx. Long-Term Annualised Return | Primary Risk | Best Suited To |

|---|---|---|---|

| Diversified equities | ~10% | Market volatility | Long-horizon investors |

| Cash equivalents | ~1-3% | Inflation and purchasing power erosion | Short-term reserves and emergencies |

This does not mean you should keep zero cash. It means the cash you hold should have a specific job. Standard guidance points to an emergency fund of 3-6 months of your essential expenses, held in a high-yield savings account or equivalent, kept separate from your investment portfolio. That is safety-net cash. It is not the same as “investing cash” sitting idle because you are waiting for a pullback.

For early-stage investors, “playing it safe” by holding excess cash is not conservative. It is a structural disadvantage wearing the clothes of caution.

If lump-sum investing beats dollar-cost averaging (DCA) more often than not in mathematical backtests, why do professionals still recommend it? Because DCA’s value was never about producing better returns on average. Its value is behavioural.

Dollar-cost averaging means investing a fixed amount on a regular schedule, regardless of what the market is doing that week. The maths of this approach is straightforward: you buy more units when prices are low and fewer when prices are high, smoothing your average entry price over time. But the real mechanism protecting you is not the price averaging. It is the removal of the decision point that would otherwise give anxiety a chance to talk you into cash.

Here is what DCA actually does in practice:

Asset-allocation specialists consistently caution against moving in and out of the market or parking large sums in cash “waiting for volatility to pass.” DCA keeps you from second-guessing yourself and freezing when headlines get noisy. That is how professionals actually use it.

Starting with small, regular contributions builds more than a balance. It builds the discipline and market literacy that compound alongside your capital. If you are using DCA and feel the urge to pause contributions and “wait,” that is the exact moment the tool is doing its most important work.

For investors wanting to examine the evidence in depth before committing to a schedule, our full explainer on lump sum versus DCA covers the Vanguard 68% finding, how the result shifts for regret-prone investors, and the hybrid deployment approach that resolves the tension for most situations.

Everything above applies to investors whose portfolios are still in the growth phase. The calculus genuinely changes once your portfolio crosses a threshold: when it is generating meaningful income on its own and is close to fully funding your major financial goals.

At that point, your priority shifts. You are no longer maximising growth at all costs. You are preserving flexibility, controlling risk, and maintaining the ability to act when opportunity appears without selling long-term holdings at a bad moment.

A modest portfolio cash sleeve, generally discussed in single-digit percentage terms among professional planners, serves this purpose. The conditions that make it appropriate are specific:

“Tactical” means something precise here. It means cash earmarked for observable conditions: defined drawdown levels, known valuation thresholds, or upcoming spending needs. Periods of negative market sentiment and short-term corrections are a recurring feature of equity markets, and positioning a cash reserve to respond to them requires knowing in advance what conditions would trigger deployment.

Cash is “a tool to limit permanent losses while waiting for better opportunities” but “a terrible long-term investment” if overused, according to Novel Investor’s framework.

For you as an established investor, a small cash sleeve functions as optionality insurance. It lets you avoid forced selling and act when conditions align. But only if the deployment trigger is defined in advance, not constructed after the fact to justify inaction.

For established investors wanting to translate the tactical cash sleeve concept into a fully structured withdrawal framework, our dedicated guide to the retirement bucket strategy explains how to size each bucket against your income gap, which instruments belong in Bucket 1 versus Bucket 2, and when to begin the transition before the first withdrawal.

Here is the most consequential distinction in this entire framework: tactical cash and emotional cash look identical on your brokerage statement. The balance is the same. The asset class is the same. The difference is entirely internal, and the test for which one you are holding is not the amount but the presence or absence of a defined trigger.

Many investors allow anxiety about markets to masquerade as a disciplined cash strategy. They sit on large cash balances without a clearly defined deployment plan, telling themselves they are “waiting for the right opportunity.” Professional literature identifies this pattern, emotional cash holding, as one of the most common failure modes across both stage groups. It is not just an early-stage problem.

Behavioural return drag, the performance gap created by reactive decisions such as pausing contributions during volatile periods or reallocating to cash after a drawdown, costs investors an estimated 1.5 percentage points per year on average, a figure that compounds into a material wealth shortfall across a multi-decade horizon.

| Attribute | Strategic Cash | Emotional Cash |

|---|---|---|

| Motivation | Defined opportunity or known spending need | Fear of volatility or general uncertainty |

| Deployment Trigger | Observable, pre-defined condition | Vague sense that “things feel safer” |

| Review Cadence | Annual opportunity-cost audit | Rarely reviewed; rationalisations updated instead |

| Risk | Modest drag if no opportunity appears | Sustained compounding penalty, often unquantified |

The diagnostic that keeps any cash thesis honest is the opportunity-cost audit: a single question you review annually.

“What did my cash cost me over the last 12 months?”

This question is rarely made this concrete in popular finance writing, yet advisors repeatedly stress it is the central risk of excess cash positions. Convert the abstract risk of sidelining cash into a concrete, reviewable number, and the distinction between optionality and avoidance becomes much harder to ignore.

If you cannot state in a single sentence what specific, observable market condition would cause you to deploy your cash reserve, you are probably not holding strategic cash. You are holding emotional cash with a strategic label on it.

The framework above gives you the logic. Here is how it converts into a practical starting position for each stage.

If you are an early-stage, growth-focused investor:

If you are an established, income-generating investor:

| Investor Stage | Cash Default | Annual Review Question |

|---|---|---|

| Early-Stage (Growth Phase) | Emergency fund only (3-6 months expenses); minimise idle investing cash; deploy on a set schedule | “What did my idle cash cost me versus my target return over the last 12 months?” |

| Established (Income-Generating Phase) | Emergency fund plus modest tactical sleeve (single-digit % of portfolio); tied to pre-defined conditions | “What did my cash cost me versus my target return over the last 12 months, and did any deployment triggers activate?” |

The universal principle across both stages: cash is best suited for short-term goals, emergencies, upcoming known expenses, and targeted optionality. It is not a primary long-term wealth-building asset.

The answer to whether you should hold cash or invest is not a single verdict. It is a moving target that should be recalibrated as your portfolio’s funding level, income generation, and time horizon shift. What stays constant is the discipline: the annual opportunity-cost review and the one-sentence deployment trigger test are the two tools that keep the decision honest regardless of stage.

The most useful thing you can do now is identify honestly which stage you are in, apply the appropriate default, and commit to reviewing the cost of your cash position at least once a year. If you can state in one sentence the observable condition that would cause you to deploy your cash, you have a strategy. If you cannot, you have a habit. The distinction matters more than the number.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The answer depends on your portfolio stage. Early-stage investors building wealth pay a compounding penalty on idle cash, since equities have historically returned around 10% annually versus 1-3% for cash equivalents, so deploying contributions on a set schedule and holding only a 3-6 month emergency fund is the appropriate default. Established investors with income-generating portfolios can justify a modest tactical cash sleeve, provided it is tied to a specific, pre-defined deployment condition.

Dollar-cost averaging (DCA) means investing a fixed amount on a regular schedule regardless of market conditions, buying more units when prices are low and fewer when prices are high. Lump sum investing outperforms DCA in mathematical backtests more often than not, but DCA's real value is behavioural: it eliminates the timing decision that allows anxiety to keep investors on the sidelines.

For early-stage investors, the answer is an emergency fund of 3-6 months of essential expenses held separately from your portfolio, with minimal idle investing cash beyond that. Established investors with substantially funded goals can add a modest tactical cash sleeve in the single-digit percentage range, but only if the conditions for deploying it are defined in advance.

The long-term return gap between equities (approximately 10% annualised) and cash equivalents (approximately 1-3% annualised) represents a 7-9 percentage point annual drag on idle capital. A concrete example from the article: a five-year delay on $100 monthly contributions at 7% annual returns costs approximately $20,400 in final portfolio value, a gap that cannot be recovered because the compounding years themselves are gone.

Strategic cash is tied to a specific, observable deployment condition such as a defined drawdown level, a valuation threshold, or a known upcoming expense. Emotional cash sits idle because of vague market anxiety, with no pre-defined trigger for when it would be invested. The practical test: if you cannot state in one sentence the observable condition that would cause you to deploy your cash, you are holding emotional cash with a strategic label on it.