CURE and CLNE: the ASX ETFs Returning 25% in 2026

6 hrs ago

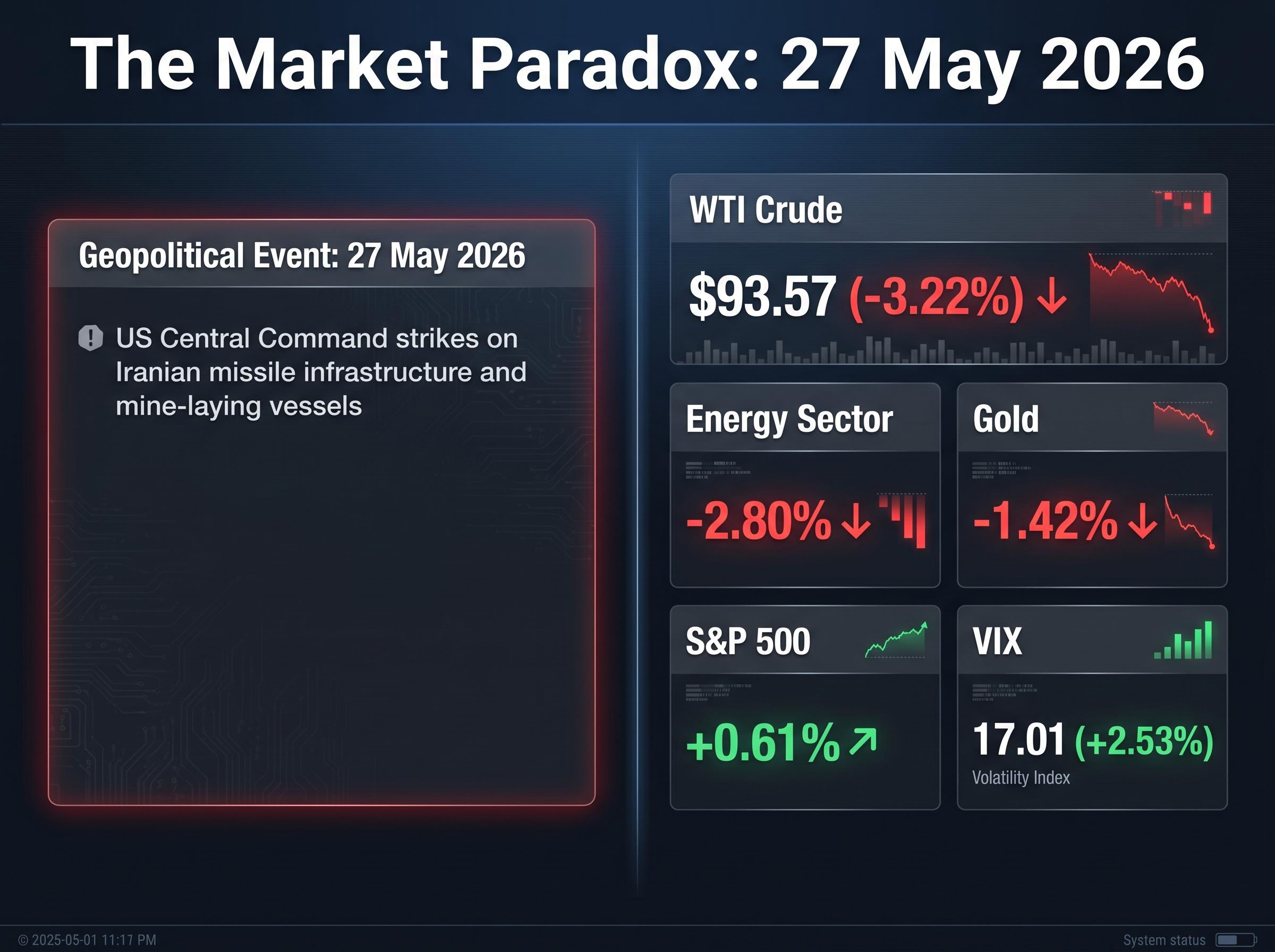

On 27 May 2026, WTI crude fell 3.22% to $93.57 per barrel. On the same day, US Central Command conducted defensive strikes against Iranian missile infrastructure and mine-laying vessels in the southern Gulf. For most readers, that price move is backwards. The conventional mental model holds that military conflict in the Middle East means higher oil prices, and for decades that model held. It is now increasingly unreliable.

Understanding why oil prices declined during an active military exchange matters well beyond the energy trading desk. Crude oil functions as a real-time geopolitical signal for portfolio managers, central bankers, and macro strategists alike. When that signal stops behaving the way it once did, reading it correctly becomes a structural advantage. What follows identifies the specific forces that pushed crude lower on a day of live escalation, explains the structural shift in how markets price geopolitical risk, and sets out the conditions that would actually move prices materially in either direction.

The sequence of events on 26-27 May 2026 was unambiguous in its escalation:

Energy was the worst-performing US sector on the session, down 2.80%. Gold fell 1.42%, suggesting the commodity complex was not experiencing a rush into safe-haven assets but rather a broad repricing away from geopolitical premium. The S&P 500 gained 0.61% on the same day.

“The traditional correlation between Middle East conflict risk and accelerating oil prices is now broken.” — Georgetown Journal of International Affairs, 2024

This was not a one-off anomaly. Iran’s direct April 2024 attack on Israel produced a price spike that, according to GJIA analysis, “quickly flattened.” The pattern has repeated with enough consistency to qualify as structural. Something in how the market processes geopolitical risk has changed.

The oil price paradox visible on 27 May was not its first appearance in this cycle; WTI fell 1.86% to $100.37 on 6 May 2026 under almost identical conditions, with the Strait of Hormuz effectively closed and the US naval escort operation Project Freedom paused, establishing a repeating pattern rather than a single anomaly.

The shift did not happen overnight. Through the conflict cycle that began after October 2023, Brent crude remained in a moderate range despite escalating military activity involving state and non-state actors across the Middle East. The GJIA’s 2024 analysis offers the most detailed available framework for why.

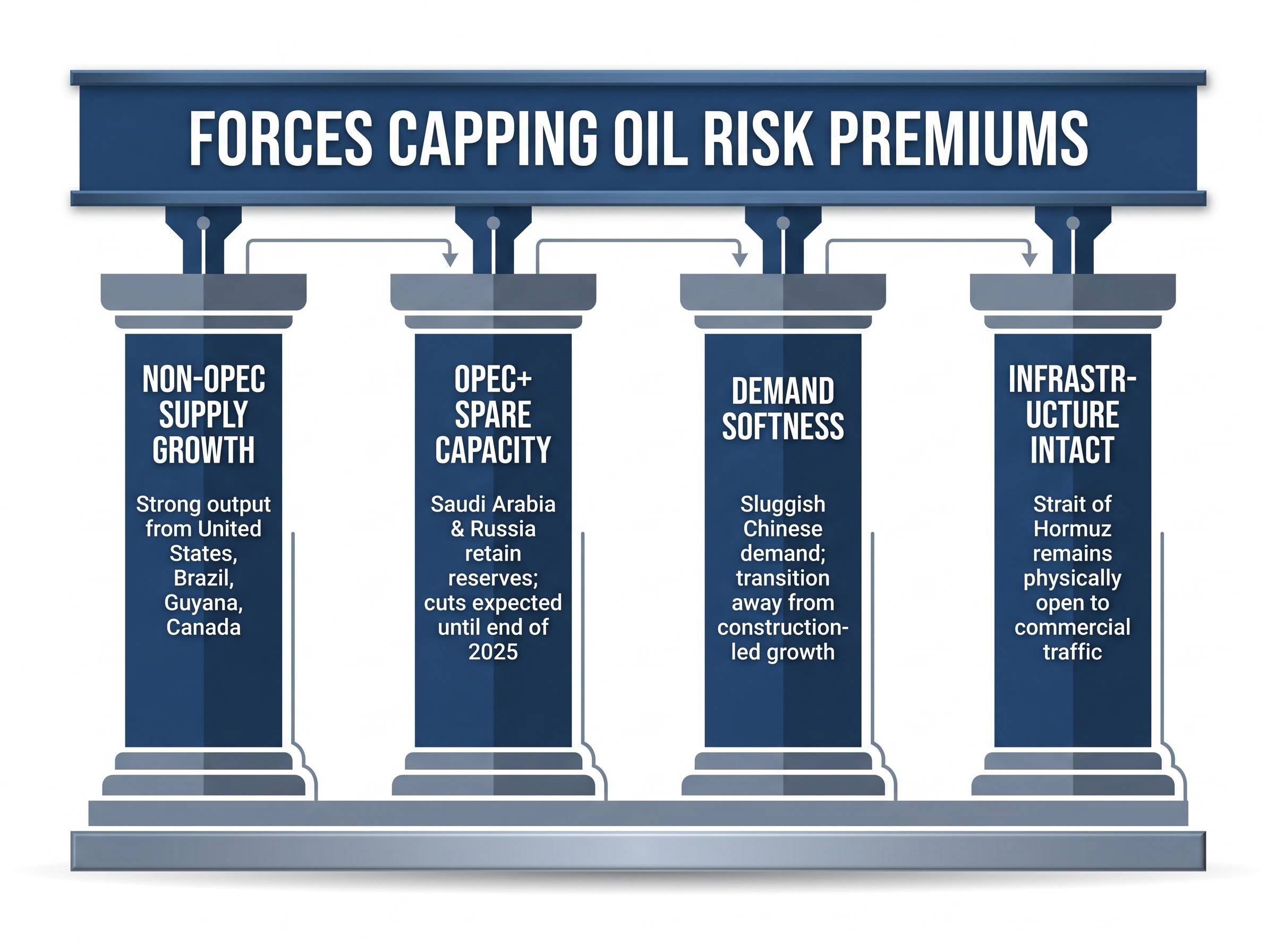

According to that framework, “price sensitivity is now more precisely focused on threats and strikes to specific sites of production and transit” rather than broad regional instability. Markets now differentiate sharply between political tension and physical supply risk. Fighting that does not damage oil fields, pipelines, or the Strait of Hormuz does not threaten the barrels traders need, and so does not command a sustained premium.

The GJIA analysis of oil price sensitivity to Middle East conflict concludes that the traditional correlation between regional instability and sustained price acceleration is now broken, with markets responding materially only when specific production or transit infrastructure faces direct physical threat.

Four structural factors reinforce this dampened transmission mechanism:

The practical implication is that the market now prices “is the Strait of Hormuz actually closed?” rather than “is there a conflict near the Strait?” Even during the April 2026 US-Iran exchanges, commercial traffic through the Strait remained physically open. That single fact, more than any diplomatic statement, determined the ceiling on the risk premium the market required.

This distinction is what makes the rest of the analysis intelligible. Without it, a 3.22% decline on a day of active military strikes looks like a malfunction. With it, the decline looks like a market doing exactly what its current pricing logic dictates.

The structural repricing described above is not merely theoretical. It is grounded in a demonstrably well-supplied market.

IEA Oil Market Reports through 2024-2025 consistently characterised the global supply picture as increasingly comfortable, driven by non-OPEC+ output growth outpacing demand. Strong production from the United States, Brazil, Guyana, and Canada created what the GJIA described as “sanguinity about the availability of supply.”

OPEC+ production cuts, expected to last “until the end of 2025 and beyond” for major producers such as Saudi Arabia and Russia, preserved substantial spare capacity. Traders understand that these barrels can be brought online if disruption materialises, effectively capping the risk premium the market needs to hold oil exposure.

OPEC spare capacity is central to the market’s current confidence, but the cartel’s ability to deploy it as a price stabiliser has been structurally narrowed: the UAE’s formal withdrawal on 1 May 2026 permanently removed approximately 14% of coordinated production capacity, and OPEC’s share of global crude output now sits at roughly 27-28%, down from a historical peak above 50%.

On 27 May 2026, a US Strategic Petroleum Reserve cargo was en route to the Philippines, the first Asian delivery of US emergency reserves since November 2022, signalling supply management confidence even during live military exchanges.

| Factor | Evidence Base | Direction of Effect on Price | Strength of Effect |

|---|---|---|---|

| Non-OPEC+ supply growth | IEA OMR: US, Brazil, Guyana, Canada output outpacing demand | Bearish | Strong |

| OPEC+ spare capacity | GJIA: cuts preserved capacity buffer deployable at short notice | Bearish (caps upside) | Moderate to strong |

| SPR deployment to Asia | First US SPR delivery to Philippines since November 2022 | Bearish (signals supply confidence) | Moderate |

| Infrastructure remains intact | Strait of Hormuz open to commercial traffic through 26-27 May 2026 | Bearish (no physical disruption premium) | Strong |

The SPR deployment and the IEA supply picture together confirm that the decline in crude was not irrational. It reflected a market with genuine supply confidence, even during live military exchanges.

Layered onto the supply fundamentals is a diplomatic dynamic that simultaneously pressured prices from both directions, and on this session, the bearish read won.

The diplomatic framework under negotiation involves a 60-day ceasefire extension, with the US potentially lifting its naval blockade in exchange for Iran reopening the Strait of Hormuz. President Trump signalled on the same day that “a US-Iran agreement had not yet been fully concluded,” leaving the outcome uncertain.

Traders read the diplomatic trajectory asymmetrically. Progress toward a ceasefire and Hormuz reopening is supply-positive: more barrels become available. The unresolved status of the deal meant the risk premium for a closure scenario was being partially discounted before the agreement was even signed, because the direction of travel pointed toward resolution rather than escalation.

At the Quad foreign ministers’ meeting in New Delhi around 26 May 2026, Australia’s Penny Wong publicly rejected Iran’s proposed transit toll on Hormuz traffic. The unified stance of four major naval-aligned powers against a mechanism that could formalise the Strait as a revenue chokepoint for Iran carries weight in how traders model the probability of sustained closure.

If the major powers will not legitimise a toll framework, the probability of a de facto toll-based closure drops. That is itself a bearish input for oil, because it narrows the range of scenarios under which Hormuz traffic could be materially disrupted through negotiation rather than force.

Even if supply-side risks were to materialise more acutely, sluggish demand growth caps how high prices could go, and therefore limits the risk premium the market will pay for disruption scenarios.

The GJIA 2024 analysis identified China’s economic transition away from construction-led growth toward export value-chain upgrading as a persistent source of demand softness. As long as Chinese demand remains sluggish, the analysis noted, prices are likely to stay flat in a moderate range despite Middle East instability. IEA outlook documents through 2024 reinforced this theme, citing moderate demand growth with downside risks from China and broader macroeconomic uncertainty.

The IEA demand forecasts citing China softness as a persistent structural drag on global oil consumption provide direct quantitative backing for why even a significant supply disruption would cause less economic damage in the current environment than it would have in a period of synchronised global growth.

Two sides of the demand picture define the current equilibrium:

The European Central Bank’s Francois Villeroy de Galhau stated around 26 May 2026 that there is currently no evidence that higher energy costs have triggered second-round inflationary effects, suggesting that even at $93.57, the market does not view current crude levels as demand-destructive.

ECB board member Isabel Schnabel separately indicated that a June rate increase remained warranted regardless of whether an Iran ceasefire materialised, a signal that the central bank is not treating the energy price environment as sufficiently severe to alter the policy calculus. Demand softness does not just lower prices directly; it also reduces the premium the market will pay for supply disruption scenarios, because a disruption that hits a sluggish demand environment causes less economic damage than one that hits a booming one.

The analysis above converts into a concrete monitoring framework. According to the GJIA’s infrastructure-focus thesis, risk premiums rise materially only when production facilities, export terminals, or transit chokepoints face “direct, credible physical threat.” The Strait of Hormuz remained physically open to commercial traffic through the events of 26-27 May 2026. The VIX rose 2.53% to 17.01 on the session, elevated but not extreme.

| Scenario | Required Condition | Expected Price Direction |

|---|---|---|

| Physical closure of the Strait of Hormuz | Commercial shipping blocked or diverted at scale | Sharply higher |

| Strike on Saudi or UAE production facilities | Direct, confirmed damage to export terminals or fields | Sharply higher |

| Ceasefire formalisation and Hormuz reopening | Signed agreement with verifiable compliance | Lower |

| China demand revision downward | IEA or OPEC cuts to 2026 demand growth forecasts | Lower |

| OPEC+ deploys spare capacity | Production increases announced and implemented | Lower |

The asymmetry in how traders are currently positioned is telling. Falling prices during active conflict suggest the market’s base case is that physical infrastructure will remain intact and the ceasefire framework will eventually formalise. That base case is falsifiable; the table above identifies what would falsify it.

The Hormuz enforcement regime shifted materially between the events of 27 May and 19 May 2026, when Iran moved from political threat to active maritime enforcement of its claimed authority over the Strait, a development that raises the probability of the physical closure scenario the current article identifies as the key falsifying condition for the bearish base case.

Four structural forces, non-OPEC supply growth, OPEC+ spare capacity, demand softness from China, and an infrastructure-focused risk premium framework, converge to explain why WTI crude fell 3.22% on a day of active US-Iran military contact. The decline was not paradoxical. It was the market telling anyone willing to listen that it does not believe the physical barrels are at risk.

The energy sector fell 2.80% while the S&P 500 gained 0.61% and the equal-weighted S&P 500 finished at an all-time high. This was not a systemic risk-off event. It was a sector-specific repricing of the geopolitical premium that the supply picture no longer supports.

Cross-asset repricing during energy shocks does not follow a uniform pattern: the Hang Seng fell approximately 1.7% and the ASX 200 fell approximately 1.6% on 18 May 2026, while the S&P 500 posted a gain on 27 May, illustrating how the same underlying supply shock can produce divergent equity outcomes depending on regional energy import exposure and central bank positioning.

The conditions that would change this read are specific and monitorable:

The market’s current pricing implies confidence in the ceasefire framework and infrastructure integrity. That confidence is falsifiable. Watch the Strait, not the headlines.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding oil prices, ceasefire negotiations, and supply-demand dynamics are speculative and subject to change based on market developments and geopolitical conditions.

Markets now differentiate between political tension and physical supply disruption, pricing risk premiums only when production facilities, export terminals, or transit chokepoints like the Strait of Hormuz face direct physical threat. Because commercial shipping through the Strait remained open during the May 2026 exchanges, traders saw no credible threat to the physical barrels they need.

The infrastructure-focus thesis holds that oil markets no longer respond materially to broad regional instability; instead, price sensitivity is concentrated on specific threats to production sites, export terminals, and transit chokepoints. This framework, outlined in Georgetown Journal of International Affairs analysis, explains why fighting that does not damage oil infrastructure fails to sustain a price premium.

Four factors converge to suppress risk premiums: strong non-OPEC supply growth from the US, Brazil, Guyana, and Canada; substantial OPEC+ spare capacity deployable at short notice; sluggish Chinese demand due to the country's economic transition; and a market pricing framework that responds only to direct infrastructure threats, not general regional conflict.

According to the infrastructure-focus framework, a sharp price rise would require physical closure of the Strait of Hormuz to commercial shipping, direct confirmed damage to Gulf production or export facilities, or a breakdown in ceasefire diplomacy that credibly raises the probability of either scenario. A demand revival strong enough to tighten the global supply-demand balance would also reignite risk premiums.

China's structural transition away from construction-led growth toward export value-chain upgrading has created persistent demand softness that caps how high oil prices can rise even if supply-side risks materialise. The IEA and GJIA both cite sluggish Chinese demand as a key reason prices remain in a moderate range despite ongoing Middle East instability.