On the worst day of the April 2025 market sell-off, thousands of Australians logged into their superannuation accounts and moved their balances to cash. It felt like the only rational response. The following month, a major high-growth super option returned approximately 5.8%, and those members were not in it. Market timing in superannuation triggers a predictable pattern: volatility arrives, the instinct to protect kicks in, and the exit happens just before the recovery does.

This article explains why that pattern repeats. It covers the behavioural reflex that drives switching, the data on what happens when investors miss the market’s best days, the structural barriers that make super timing harder than timing a share portfolio, and what Australia’s regulators and largest funds consistently say about the practice. It also sets out a practical framework, core-and-satellite, that gives members a way to act on their instincts without abandoning the long-term discipline the evidence supports.

The reflex that costs Australian super members money

Watching a super balance fall 4% in a month produces a feeling that is difficult to override. The instinct is immediate: stop the loss. Move to cash. Protect what remains. Behavioural finance calls this loss aversion, the well-documented tendency for people to feel losses roughly twice as intensely as equivalent gains. It is not irrational. It is human wiring.

It is also common. During the early 2025 volatility triggered by US tariff announcements, AustralianSuper, Australian Retirement Trust, and Hostplus all published member reassurance messaging. Aware Super updated its investment risk guidance. Funds do not issue these communications unless switching behaviour spikes. The messaging exists because the behaviour exists.

Loss aversion, the tendency to feel losses roughly twice as intensely as equivalent gains, was formally documented by Kahneman and Tversky in 1979 and remains one of the most consistently measured biases in investor behaviour; Morningstar’s ‘Mind the Gap’ research estimates it produces a behavioural return shortfall of approximately 1-2 percentage points per year by pushing investors to sell near lows and re-enter only after prices have already recovered.

The problem is not the exit itself. Moving to cash during a downturn crystallises whatever loss has already occurred, but the real cost comes in what happens next. Markets do not recover on a schedule that gives investors time to switch back. The members who moved to conservative options around April 2025 were positioned to miss a single-month gain of approximately 5.8% in a major high-growth option the following month.

“Switching to lower-risk options after markets fall can mean missing the recovery.” — ASIC MoneySmart, 2024-25 guidance

That single sentence captures the entire mechanism. The exit feels protective. The cost is in the re-entry.

When big ASX news breaks, our subscribers know first

How market volatility clusters and concentrates returns

The strongest argument against timing the market is not theoretical. It is statistical, and it comes from the relationship between the market’s best days and its worst.

Large daily gains and large daily losses do not distribute evenly across the calendar. They cluster. The days of sharpest recovery tend to occur within days, sometimes hours, of the days of steepest decline. An investor who exits the market to avoid a bad week is almost certainly out of the market when it snaps back.

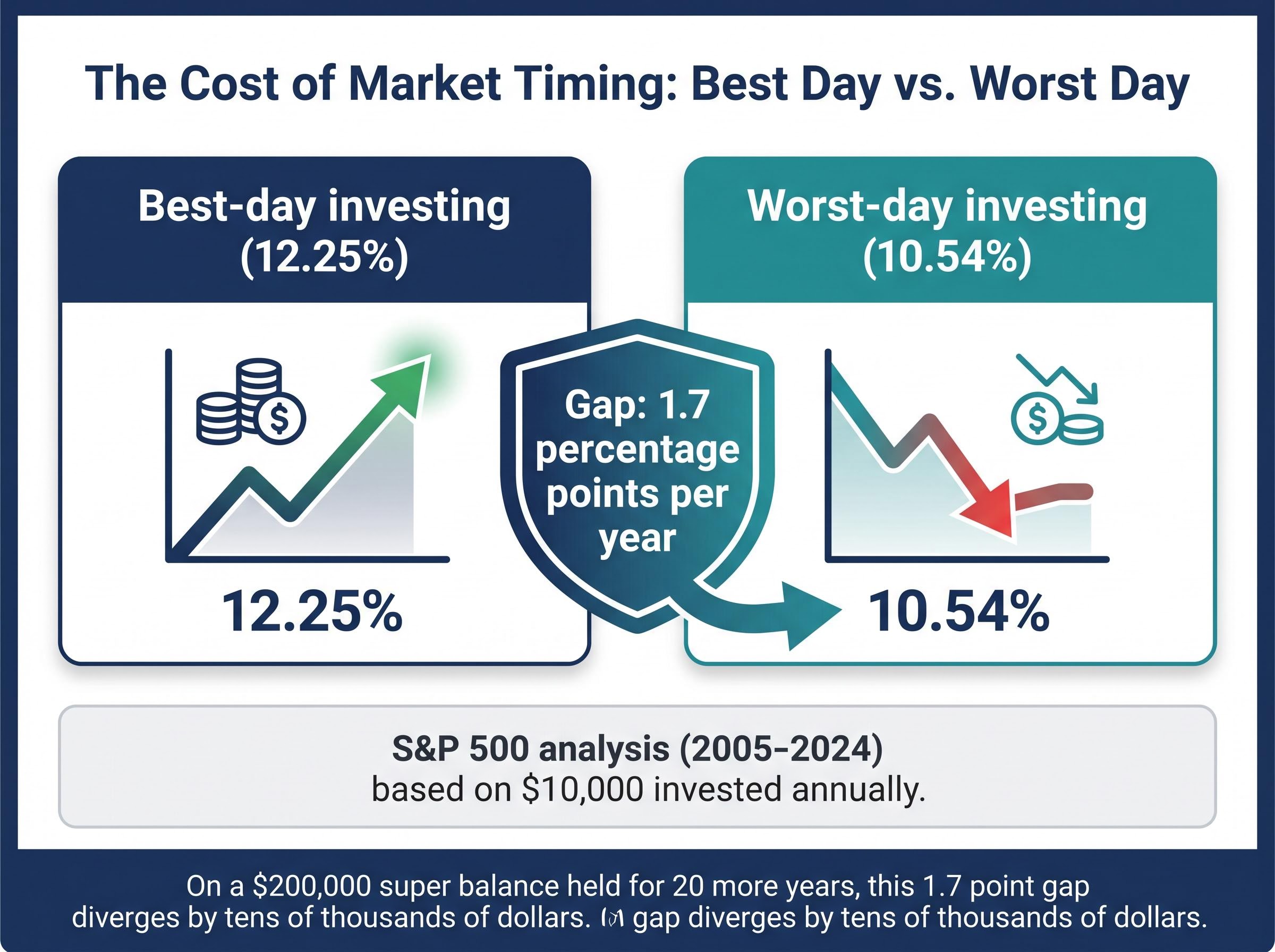

A hypothetical analysis of $10,000 invested annually into the S&P 500 from 2005 to 2024 illustrates the cost. An investor who happened to invest on the best market day of each year achieved average annual returns of 12.25%. An investor who invested on the worst day of each year still achieved 10.54%. The gap: approximately 1.7 percentage points per year.

| Strategy | Average Annual Return | Implication |

|---|---|---|

| Best-day investing | 12.25% | Optimal timing each year (unrealistic in practice) |

| Worst-day investing | 10.54% | Worst possible timing each year, still positive |

| Difference | 1.7 percentage points | Compounding gap grows substantially over 30-40 years |

Source: 20-year S&P 500 analysis, 2005-2024.

1.7 percentage points per year may sound modest in isolation. Compounded across a 30-40 year super accumulation phase, the difference in final balance is substantial. On a $200,000 super balance held for 20 more years, the divergence runs into tens of thousands of dollars.

Superannuation balance benchmarks by age reveal a consistent pattern: the compounding gap between Australians who stay invested through volatility and those who repeatedly exit to cash widens most dramatically in the final decade before retirement, when the balances involved are largest and the cost of a single poorly timed exit is highest.

The practical implication is stark. An investor does not merely need to predict when the market will fall. They need to predict the exact day it recovers, and no evidence suggests any category of investor, professional or retail, does this reliably. ASIC MoneySmart confirms the point: higher-growth options may fall more in downturns but recover over time, and shifting to cash after a fall can crystallise losses and cause members to miss the rebound.

The operational constraints that make super timing uniquely difficult

Even setting aside the behavioural challenge, superannuation imposes structural barriers that a direct share portfolio does not. A self-directed investor holding BHP shares can sell at 10:01am and buy back at 10:03am. Super does not work that way.

Three structural constraints make market timing in super mechanically harder:

- Fund-level execution timing. Australian industry super fund members cannot control the exact moment contributions are deployed into the market. Investment execution is managed at the fund level, meaning there is a lag between a member’s decision and the market action. A switching request lodged on Monday may not be processed until Tuesday or Wednesday, by which time the market may have already moved.

- Contribution cap constraints. Even a member who correctly identifies a market bottom cannot pour unlimited capital into their super to capture the recovery. Annual caps impose a hard ceiling on additional deployment.

- The re-entry timing problem. Switching into a conservative option crystallises a position, but it does not solve the second, equally difficult decision: when to switch back. Members who moved to cash in April 2025 then faced weeks of uncertainty about the right moment to re-enter growth options.

Contribution caps limit opportunistic deployment

The concessional contribution cap stands at $30,000 per year for both 2024-25 and 2025-26, rising to $32,500 from 1 July 2026. The non-concessional cap is $120,000 per year, with a bring-forward rule allowing up to $360,000 over three years for eligible members. These caps exist for tax and retirement policy reasons, not for market timing. The bring-forward provision is a planning tool, not a mechanism for reactive deployment during a downturn.

For members who want to understand how the new cap limits interact with carry-forward rules and unused entitlements expiring on 30 June 2026, our full explainer on superannuation cap changes in 2026 covers the concessional and non-concessional mechanics, the Total Super Balance eligibility threshold, and the specific member profiles for whom the carry-forward opportunity is most material.

What Australia’s regulators and major funds consistently say

One institution warning against market timing could be dismissed as a single perspective. When the consumer regulator, the prudential regulator, and the country’s largest super funds all arrive at the same conclusion independently, the convergence itself becomes data.

- ASIC MoneySmart (current 2024-25 guidance): Super is a long-term investment and should be managed accordingly. Reacting to short-term market moves can lock in losses. Switching to lower-risk options after markets fall can mean missing the recovery.

- APRA CPG 530 (Investment governance for RSE licensees): Requires trustees to manage members’ investment risk with a focus on long-term objectives rather than short-term market moves. Mandates that funds avoid overly reactive investment strategies, providing the structural reason why fund architectures resist reactive repositioning.

APRA’s investment governance guidance under SPG 530 requires superannuation trustees to manage members’ portfolios with an explicit focus on long-term objectives, providing the structural reason why Australian fund architectures are deliberately designed to resist reactive repositioning during short-term market moves.

- AustralianSuper (member education, updated post-July 2024): Moving to cash during downturns can lock in losses. Missing recovery days can significantly reduce long-term super outcomes.

- Aware Super (investment risk guidance, updated for 2024-25 caps): Frames super as a long-term asset, warns against reactive decision-making during market volatility.

These four voices operate at different levels, from retail consumer guidance to prudential governance, but they converge on the same conclusion. The regulatory and institutional consensus in Australia is not ambiguous. It is uniform.

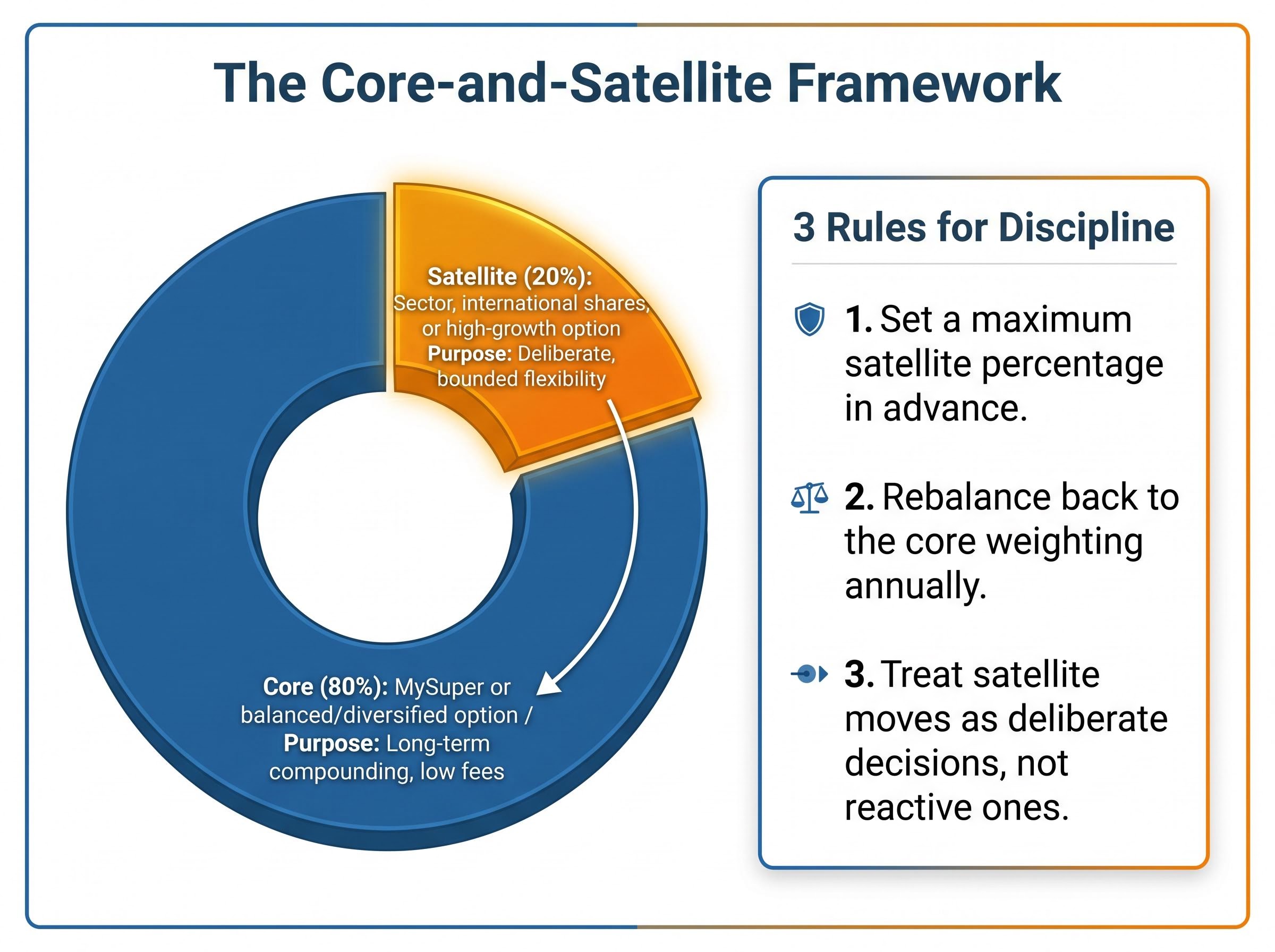

The core-and-satellite approach: structure for investors who want some flexibility

The evidence against market timing in super is strong. The impulse to act during volatility is also strong. For members who cannot sit still through a drawdown, the core-and-satellite framework offers a way to hold both realities at once.

The concept is straightforward. The majority of a super balance sits in a core allocation: a MySuper, balanced, or diversified index option providing broad market exposure and long-term compounding at low fees. A smaller portion, the satellite allocation, sits in more targeted options where a member can make deliberate adjustments.

| Portfolio Component | What It Looks Like in Super | Purpose |

|---|---|---|

| Core (80%) | MySuper or balanced/diversified option | Long-term compounding, low fees |

| Satellite (20%) | Sector, international shares, or high-growth option | Deliberate, bounded flexibility |

An 80/20 split provides a reference point rather than a prescription. The core remains stable through market cycles. The satellite is where a member might shift allocations in response to conditions, but within defined boundaries.

Three practical rules help keep the satellite allocation disciplined rather than reactive:

- Set a maximum satellite percentage in advance. Decide the upper bound before volatility arrives, not during it.

- Rebalance back to the core weighting annually. This prevents satellite drift from gradually increasing portfolio risk.

- Treat satellite moves as deliberate decisions, not reactive ones. If a switch happens the same day as a market fall, it is reactive. If it follows a considered view formed over days or weeks, it is deliberate.

It is worth noting that the April 2025 episode illustrates the risk even within satellite allocations. A major high-growth option lost approximately 4% in one month, recovered approximately 5.8% the next, and delivered a net three-month return of approximately -1.7%. Short-term switching within a satellite allocation still carries timing risk.

ASIC MoneySmart and major fund education materials do not describe core-and-satellite explicitly for superannuation. This is an applied framework drawn from general investment advice literature and mapped to the super context. It does not promise better returns than a fully passive strategy. It gives members who cannot resist acting a structured way to limit the cost of that impulse.

The question is not whether to stay invested, it is how to hold your nerve

The evidence against market timing in superannuation is structural, quantitative, and backed by every major institutional voice in the Australian system. The 1.7 percentage point annual return gap between best-day and worst-day investing over the 2005-2024 period captures the cost in concrete terms. Contribution caps of $30,000 concessional for 2025-26 mean that additional capital deployment during downturns has a hard ceiling regardless of conviction.

None of this makes the feeling of watching a balance fall any easier. The emotional pull to act during volatility is normal. It does not reflect poor financial literacy. The difficulty is behavioural, not informational. Knowing the data and acting on it are different skills.

If the urge to act is strong, the core-and-satellite framework provides a bounded way to engage. Keep the core stable. Use the satellite portion if the impulse to act is overwhelming. Understand that the market’s best days are almost always attached to its worst ones.

Super contribution strategies like salary sacrifice, carry-forward top-ups, and deliberate investment option selection address a different dimension of the same long-term outcome: while avoiding poorly timed exits preserves the compounding already in motion, proactive contribution decisions actively accelerate it.

“Super is a long-term investment and should be managed accordingly.” — ASIC MoneySmart

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.