Is NAB’s Dividend Worth Buying at a 6.5% Grossed-Up Yield?

37 mins ago

On 21 May 2026, Jensen Huang told investors that Nvidia sees “over $200 billion” in CPU market opportunity ahead. The figure spans a decade. It includes China. Both details drew immediate scrutiny from Wall Street, where analysts split sharply on whether the number reflects a credible long-term platform thesis or a marketing figure dressed in financial language. Nvidia built its dominance on GPUs, yet the announcement of its Vera processor platform signals a deliberate push into a segment controlled by Intel, AMD, and increasingly by custom Arm silicon from Amazon, Google, and Microsoft. The timing is tied to a structural shift: agentic AI is changing what data centres actually need, and Nvidia is positioning Vera as the answer. What follows unpacks what the $200 billion figure actually represents, why agentic AI underpins the demand thesis, who stands in Nvidia’s way, and what the inclusion of China signals about the company’s risk tolerance.

The number is large enough to command attention, and vague enough to warrant interrogation. Jensen Huang’s 21 May 2026 earnings call framed Nvidia’s CPU opportunity as “over $200 billion” across the next decade, encompassing server-class CPU sockets tied to AI inference, retrieval, and data processing workloads. No pricing detail for the Vera platform was disclosed. No benchmarks against x86 incumbents were shared. No concrete OEM design wins were announced.

Nvidia’s Q1 FY2027 earnings delivered record data centre revenue of $75.2 billion, growing 21% quarter-over-quarter, and it was on the call accompanying those results that Jensen Huang introduced the Vera CPU platform and the $200 billion TAM framing that has since dominated analyst commentary.

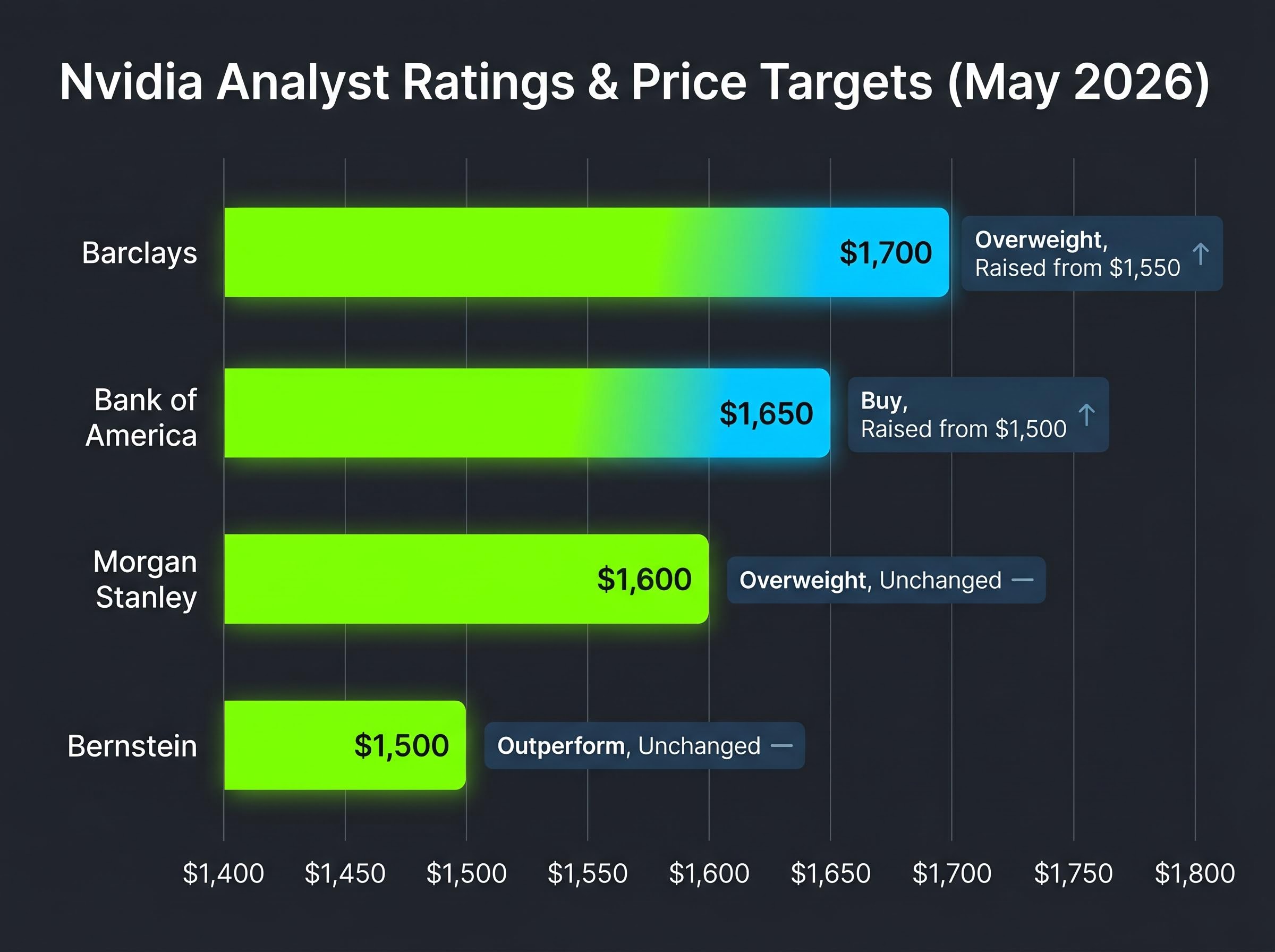

Wall Street’s response split along a familiar line: directionally credible versus insufficiently modelled. Barclays analyst Blayne Curtis, who raised his price target to $1,700 from $1,550, described the figure as “a long-term CPU+accelerator platform TAM rather than a pure CPU revenue forecast,” explicitly flagging potential double-counting with existing GPU system spend.

Bernstein’s Stacy Rasgon called the $200 billion figure “more aspirational than modeled,” noting Nvidia provided no timing, pricing, or market-share assumptions at the time of announcement.

Rasgon held his price target at $1,500. The gap between the two readings, Curtis’s structural optimism and Rasgon’s methodological scepticism, captures the analytical tension investors face. A total addressable market projection is not a revenue forecast, and the distinction matters enormously for how the Vera strategy should be valued.

Server CPU market forecasts from multiple analyst houses converge on a similar directional claim despite different methodologies: Citi projects growth from $29.3 billion in 2025 to $131.5 billion by 2030, with a newly defined agentic CPU segment growing at a 185% CAGR representing roughly 45% of that total by decade end, a figure that contextualises why Nvidia frames its own Vera opportunity at $200 billion when the broader market it is entering is itself on a steep growth trajectory.

| Firm | Rating | Price Target | Direction |

|---|---|---|---|

| Barclays | Overweight | $1,700 | Raised from $1,550 |

| Bank of America | Buy | $1,650 | Raised from $1,500 |

| Morgan Stanley | Overweight | $1,600 | Unchanged |

| Bernstein | Outperform | $1,500 | Unchanged |

The demand thesis behind Vera does not rest on Nvidia wanting to sell CPUs for their own sake. It rests on a structural change in what AI workloads actually require.

Training large language models is a GPU-intensive, bursty process: massive compute for weeks or months, then relative quiet. Agentic AI operates differently. Agents are stateful, interactive, and persistent. They run inference continuously, orchestrate multi-step workflows, and retrieve data from vector databases in real time. The compute profile shifts from a single tier of top-end GPUs to a multi-tier architecture spanning GPUs, CPUs, high-bandwidth memory, and networking.

As the Wall Street Journal reported, industry analysts have observed that “compute shifts from bursty GPU training to continuous inference and orchestration” as agents become stateful and interactive. Ars Technica, reporting on 17 May 2026, noted that agent workloads require “large fleets of moderately powerful cores” alongside accelerators, driving renewed interest in high-core-count CPUs and efficient Arm servers.

Huang described Vera as a server-class CPU platform built to run “agentic AI inference, retrieval, and data processing” alongside Nvidia GPUs. Morgan Stanley’s Joseph Moore framed the strategy directly: Nvidia is “trying to repeat the CUDA playbook on the CPU side,” using Vera to bind more of the AI stack to its software ecosystem.

The logic is coherent. GPU dominance alone may not capture the full AI infrastructure spend cycle if agentic workloads redirect a meaningful share of data centre budgets toward CPUs and orchestration layers. Vera is Nvidia’s answer to that redirection. Whether the market opportunity is $200 billion or substantially less, the structural shift creating it is independently verifiable across multiple sources.

Structural demand is one thing. Winning share against entrenched incumbents is another. The CPU market Nvidia is entering is defended by companies with deep customer relationships, long qualification histories, and, in the case of hyperscalers, the ability to build their own chips.

AMD presented its strongest counterargument at its Financial Analyst Day on 16 May 2026. Turin (Zen 5-based EPYC) already occupies substantial data centre share, and the Zen 6 EPYC roadmap is being positioned as AI-ready, pairing with AMD’s Instinct accelerators. Analysts note AMD holds an “incumbent advantage” in CPU sockets that Vera must overcome through qualification cycles that historically run 12-18 months or longer.

Intel is playing defence with depth. Its earnings call commentary on 2 May 2026 positioned Sapphire Rapids and successors (Granite Rapids, Sierra Forest) as the default CPU supplier for AI back-end servers, with increased core counts and memory bandwidth explicitly targeting inference and cloud workloads. Intel’s pitch is that its CPUs pair with both Nvidia and Intel accelerators, making it vendor-agnostic in a way Vera is not.

The five competitive vectors Nvidia faces:

The hyperscaler programmes deserve separate weight. Amazon’s next-generation Graviton, detailed by The Register on 8 May 2026, includes enhanced matrix capabilities for AI inference. Google’s Axion and Microsoft’s custom Arm CPU efforts, both reported in May 2026, are framed as reducing reliance on third-party CPU suppliers. These are not speculative roadmaps; they are production silicon programmes from companies that represent a disproportionate share of the addressable data centre CPU market.

When the three largest cloud buyers are building their own CPUs, the addressable opportunity for any third-party supplier, including Nvidia, contracts meaningfully. This is why Morgan Stanley’s Moore flagged that full TAM capture is unlikely, and why the undisclosed market-share assumptions behind the $200 billion figure matter more than the headline number itself.

The paradox at the core of Nvidia’s competitive position is that hyperscaler custom silicon programmes are funded by the same AI capital expenditure wave that drives Nvidia’s order book: the $700 billion-plus in combined U.S. tech firm AI capex projected for 2026 finances both Nvidia’s record revenues and the Google Axion, Amazon Graviton, and Microsoft Arm programmes that directly constrain Vera’s addressable opportunity.

Including China in a $200 billion TAM was not a passive assumption. It was a named decision by management, and it drew immediate, polarised analyst responses.

Bank of America’s Vivek Arya, who raised his price target to $1,650, interpreted the inclusion as a signal of management confidence that “export-compliant configurations will find demand.” He simultaneously cautioned that “regulatory risk remains elevated.” Rasgon at Bernstein was blunter.

Bernstein’s Stacy Rasgon described China’s inclusion in the TAM as “highly uncertain under current export regimes.”

The H200 situation offers the clearest real-world stress test. According to Reuters on 21 May 2026, approximately 10 Chinese companies hold U.S. clearance to purchase H200 AI chips. Yet no deliveries had occurred as of late May 2026, because Chinese regulatory approval had not been secured. Huang participated in Beijing U.S.-China leadership talks in May 2026; no resolution on H200 shipments resulted.

The regulatory hurdles are layered and sequential:

Bloomberg reported on 14 May 2026 that the U.S. administration is considering broader restrictions potentially affecting next-generation AI products. Nikkei Asia reported on 12 May 2026 that Chinese authorities may be slow-walking approvals as leverage in broader trade negotiations.

For investors evaluating a $1 trillion cumulative revenue projection, the China variable is not a footnote. It is a material upside assumption inside the TAM figure, contingent on policy outcomes outside Nvidia’s control.

For investors who want to model the China variable with greater precision, our deep-dive into Nvidia’s China market positioning traces the revenue collapse from approximately $6 billion in FY2024 to near zero by FY2026 Q1, examines how institutional investors at BlackRock, Goldman Sachs, and Vanguard are treating China upside in their valuation frameworks, and quantifies why the analyst consensus price target is built on U.S. and allied market demand with China treated as a binary optionality position.

The evidence supports a calibrated reading: Nvidia’s CPU strategy is structurally coherent, but the gap between addressable market and captured revenue will be determined by variables that remain unresolved.

Barclays’ Curtis expects meaningful Vera revenue only from FY2028 onward, given long data centre qualification cycles. Bernstein’s Rasgon estimated “tens of billions” of CPU revenue are plausible by the early 2030s, but only if Nvidia wins significant hyperscaler share. Bank of America’s Arya suggested CPU sockets for agentic AI could “rival the existing GPU accelerator market” over the next decade.

Conditions under which Vera gains significant CPU market share:

Conditions under which incumbents and custom silicon absorb the growth:

The most durable competitive advantage Nvidia could bring to the CPU market is software lock-in, not hardware specifications alone. Morgan Stanley’s Moore described the strategy as “repeating the CUDA playbook on the CPU side.” CUDA’s success came from deep integration with developer workflows over more than a decade. Whether Vera can achieve similar embeddedness in agentic AI development pipelines is the long-term question that hardware benchmarks alone cannot answer.

The CPU move is best understood not as a near-term revenue driver but as a platform extension. If successful, it reduces the risk that agentic AI infrastructure spend flows to AMD, Intel, or custom silicon rather than staying inside Nvidia’s ecosystem.

The structural demand shift driven by agentic AI is credible. Multiple independent sources confirm that inference-heavy, persistent workloads are changing the compute mix data centres require. That shift creates a genuine opening for CPU suppliers, and Nvidia’s Vera platform targets it directly.

The $200 billion TAM figure, however, remains a ceiling claim. It is built on optimistic assumptions about market share, China access, and qualification timelines that have not been disclosed or stress-tested publicly. The gap between addressable market and captured revenue will become clearer only from FY2028 onward, as qualification cycles conclude and the competitive responses from AMD, Intel, and hyperscaler custom silicon programmes are measured against actual workload adoption.

Jensen Huang’s scheduled GTC Taipei keynote in June 2026 is the next event where Vera platform specifics, OEM design wins, and pricing details may begin to fill in the assumptions currently absent from the headline figure.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding Nvidia’s CPU market opportunity and revenue projections are subject to market conditions, regulatory developments, and competitive dynamics.

Vera is Nvidia's server-class CPU platform designed to run agentic AI inference, retrieval, and data processing workloads alongside Nvidia GPUs, targeting the multi-tier compute architecture that persistent AI agents require.

Analyst reactions split sharply: Barclays raised its price target to $1,700 and described the figure as a long-term CPU and accelerator platform TAM, while Bernstein held at $1,500 and called the number more aspirational than modeled due to absent pricing, timing, and market-share assumptions.

Unlike bursty GPU-intensive model training, agentic AI workloads are stateful and persistent, requiring continuous inference, multi-step orchestration, and real-time data retrieval, which shifts data centre compute budgets toward high-core-count CPUs alongside accelerators.

Bernstein's Stacy Rasgon described China's inclusion as highly uncertain under current export regimes; as of late May 2026, no H200 deliveries had occurred in China despite partial U.S. clearance, and broader restrictions on next-generation AI products were under consideration.

Barclays analyst Blayne Curtis expects meaningful Vera revenue only from FY2028 onward, given that data centre CPU qualification cycles historically run 12-18 months or longer for a new entrant.