ASIC Sues Equity Trustees Over $65M Shield Master Fund Failures

1 hr ago

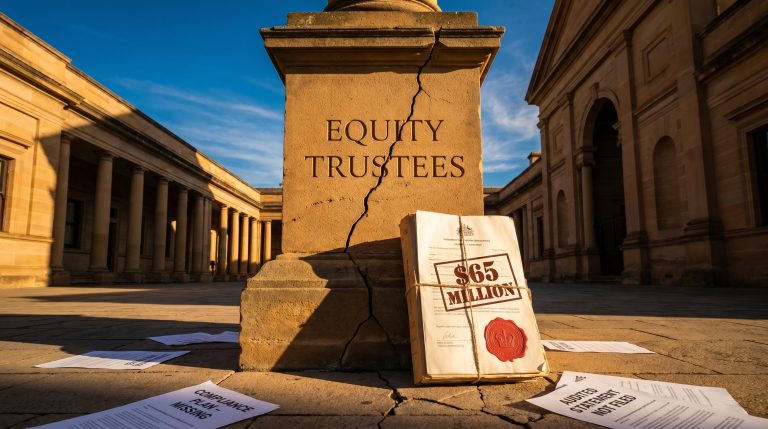

The entire semiconductor complex lit up before the opening bell on Wednesday 20 May 2026, and Nvidia had not yet reported a single number. Nvidia shares climbed 1.7% in premarket trading. Marvell Technology gained 4.7%. Intel surged 4.8%. The iShares Semiconductor ETF rose 2.2%. Tonight’s after-market earnings release, the last major catalyst of the current reporting season, has turned a single company’s quarterly update into a market-wide event. What follows is the consensus bar Nvidia must clear, the specific numbers Wall Street is watching beyond the headline, and what tonight’s results signal for the broader AI infrastructure trade and U.S. equity sentiment.

The premarket move was not confined to one ticker. It swept across the semiconductor complex in a single coordinated wave:

The ETF gain is the number that matters most. Individual names can move on idiosyncratic catalysts; a 2.2% premarket lift across the sector’s broadest benchmark signals collective positioning ahead of a single event.

Equity index futures reflected the same optimism bleeding into the broader market. As of 8:27 a.m. ET, Dow Jones E-mini futures were up 184 points (+0.37%), S&P 500 E-mini futures gained 30.5 points (+0.41%), and Nasdaq 100 E-mini futures climbed 215.5 points (+0.75%).

Chris Beauchamp, chief market analyst at IG Group, characterised Nvidia’s earnings as the most significant remaining event of the current reporting season.

The breadth of the rally raises a question the after-market release will answer: is this anticipatory move pricing in results the market has already modelled, or is capital running ahead of confirmation it does not yet have?

The breadth of the premarket rally aligns with semiconductor positioning data published by Bank of America on 18 May, which showed active long-only overweight in semiconductors at approximately 20%, half the 2017 cycle peak, suggesting the coordinated move reflects genuine fundamental conviction rather than the crowded speculative positioning typically associated with late-cycle sector surges.

The consensus revenue estimate sits at approximately $78-79.2 billion for Q1 FY2027. Nvidia’s own guidance of $78 billion (plus or minus 2%) aligns closely with that figure. Consensus earnings per share range from approximately $1.74 to $1.78. A headline beat on either metric, given the tight alignment between company guidance and Street expectations, is unlikely to move markets on its own.

The real information arrives in three places, ranked by the order in which the market will process them:

Those demand signals are already priced in. The new information tonight sits on the supply and execution side: whether Nvidia can deliver against the backlog it has built.

Nvidia’s data centre segment is the direct beneficiary of hyperscaler GPU spending. When Microsoft, Alphabet, Meta, and Amazon commit capital to AI infrastructure, the bulk of GPU procurement flows through Nvidia. That makes tonight’s data centre revenue figure something larger than a line item on one company’s income statement. It is a real-time audit of whether approximately $725 billion in combined hyperscaler capital expenditure commitments for 2026 is converting into actual orders.

The scale of those commitments, disclosed during late April 2026 earnings calls, represents an approximately 77% year-over-year increase in combined Big Tech capital spending.

The hyperscaler capital expenditure commitments disclosed during late April 2026 earnings calls were not incremental updates; they represented a structural step-change, with Amazon, Microsoft, Alphabet, and Meta collectively deploying $130 billion in Q1 2026 alone and setting a trajectory toward $1 trillion in annual AI infrastructure spending by 2027.

| Company | 2026 Capex Guidance |

|---|---|

| Microsoft | ~$190 billion |

| Alphabet | ~$180-190 billion |

| Meta | ~$125-145 billion |

| Amazon | ~$200 billion (reaffirmed) |

Capital expenditure at this level, the annual spending that companies allocate to building physical and digital infrastructure, does not guarantee sustained GPU demand indefinitely. But it establishes the structural backdrop against which Nvidia’s quarterly results are measured. A strong data centre print tonight validates the thesis that hyperscaler dollars are flowing through to orders. A miss complicates it.

The premarket optimism landed into a bond market that spent the prior session repricing rate expectations. The 10-year U.S. Treasury yield hit a 16-month peak of 4.687% on 19 May, driven by a global bond selloff that directly pressures high-multiple technology valuations. That yield retreated slightly to 4.635% on 20 May, offering modest relief without reversing the trend.

The rate picture extends beyond yields. According to CME FedWatch data:

The shift in 50-basis-point rate-hike probability, from 4.2% to 13.7% in a single week, reflects a market rapidly recalibrating its expectations for Federal Reserve policy through year-end.

The 5-year Treasury yield sat at approximately 4.27% as of 18-19 May, while the fed funds rate remained near 3.63%. Brent crude futures fell approximately 2% to $109.14 per barrel, partially driven by Trump administration comments on Iran, providing one disinflationary offset.

The Federal Reserve minutes release later today adds a second catalyst to a session already defined by Nvidia’s report. A strong beat lands into an environment willing to reward it. A miss lands into a rate and yield backdrop already compressing the multiple investors will pay for AI growth.

The Federal Reserve minutes release later today adds a second major catalyst to an already event-dense session; the April minutes contain four dissenting votes, the most at any single meeting since 1992, and the internal disagreement they document will shape how markets interpret any shift in rate-hike probability signals that accompany Nvidia’s after-market report.

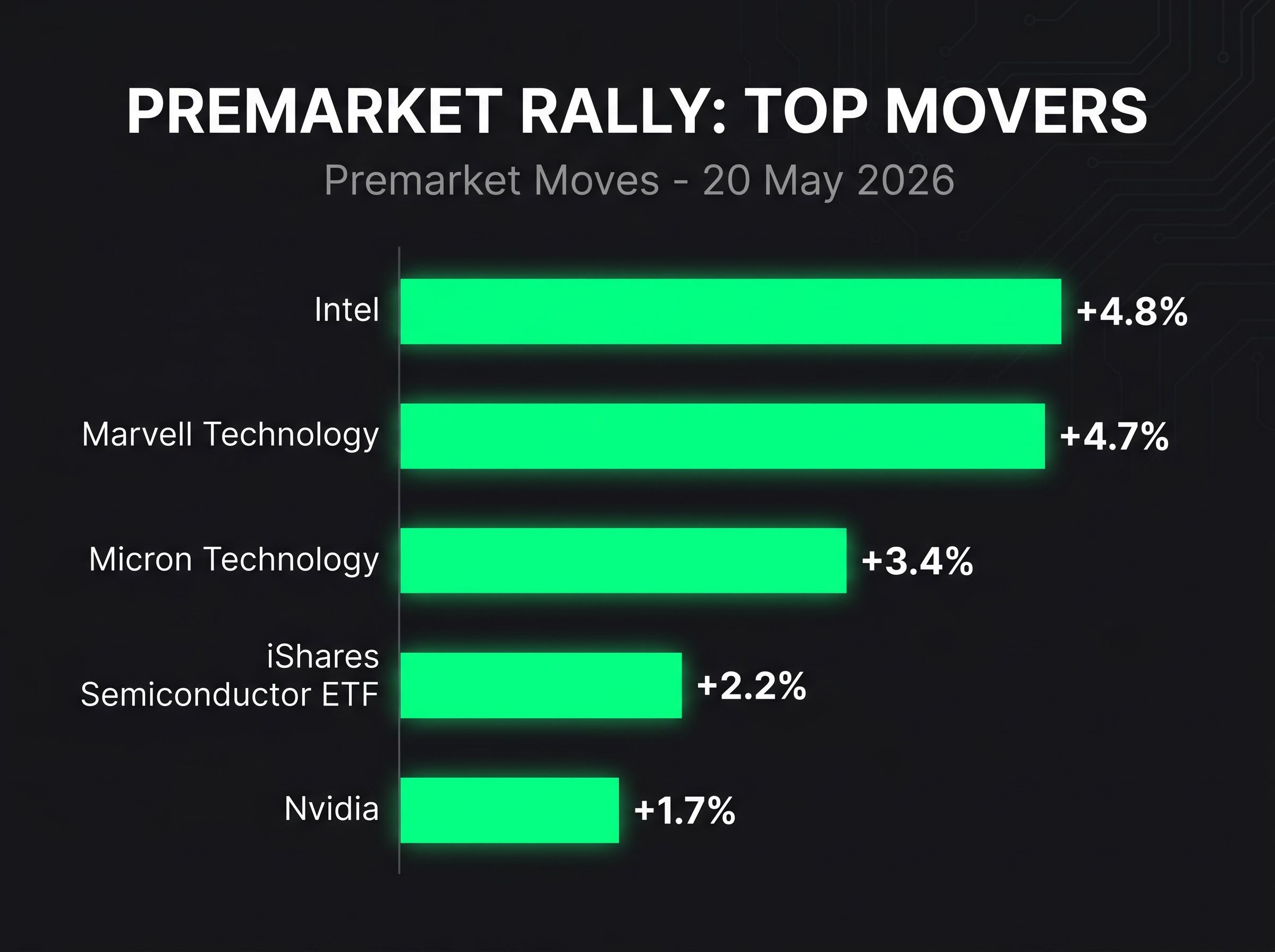

The Street entered today with a Buy consensus rating on Nvidia. HSBC set a price target of $325 in a note dated 19 May 2026. DA Davidson and Morgan Stanley published notes on 18 May 2026. The Wall Street average price target sits at approximately $274-285, with the full analyst range spanning $205 to $360.

That $155 gap between floor and ceiling reflects genuine disagreement about how long the AI infrastructure cycle sustains current GPU demand, and tonight’s results will pull that range tighter in one direction or the other.

The beat scenario rests on three indicators:

The miss scenario involves the inverse:

The pre-result price target range gives readers a framework for evaluating the analyst revisions that will follow within hours of the release. Knowing where the Street stood before results makes the morning-after upgrades and downgrades interpretable rather than arbitrary.

Nvidia’s quarterly report has evolved beyond a company event. It functions as the most concentrated data point on whether the AI infrastructure thesis, now backed by approximately $725 billion in hyperscaler capital commitments for 2026, is delivering at the GPU procurement level.

When results drop after the close, three numbers will determine the market’s reaction: data centre revenue versus the $72-73 billion anchor, Q2 FY2027 guidance relative to current consensus, and any update on Blackwell supply constraints and the Rubin architecture roadmap.

A strong report sustains the case for elevated AI valuations across the semiconductor complex. A miss, into a rising-yield environment where rate-hike probabilities have tripled in a week, creates a more complicated picture for the sector heading into the second half of the year. The after-market release and the post-close analyst call, where management commentary on guidance and supply will carry the most weight, are the moments to watch.

A strong beat tonight would validate the near-term demand thesis, but the capex-to-revenue lag identified by Morningstar as an 18-24 month structural risk means the more consequential question is whether $725 billion in 2026 hyperscaler commitments translates into proportional AI revenue before investor patience with elevated semiconductor valuations runs out.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Wall Street consensus estimates Q1 FY2027 revenue of approximately $78-79.2 billion, in line with Nvidia's own guidance of $78 billion plus or minus 2%, with earnings per share consensus ranging from $1.74 to $1.78. Analysts say a headline beat alone is unlikely to move markets without an upward Q2 guidance raise.

Nvidia's data centre segment is the primary destination for hyperscaler GPU spending from Microsoft, Alphabet, Meta, and Amazon, which have collectively committed approximately $725 billion in capital expenditure for 2026. The quarterly results function as a real-time audit of whether that capital is converting into actual GPU orders.

Analysts will prioritise Q2 FY2027 guidance relative to current consensus, data centre revenue versus the $72-73 billion anchor, and any commentary on Blackwell GPU supply constraints and the Rubin architecture timeline. These three data points carry more weight than the headline earnings per share figure.

The 10-year U.S. Treasury yield hit a 16-month peak of 4.687% on 19 May, directly compressing the high multiples investors pay for AI growth stocks. A miss in this rate environment would create a more complicated picture for the semiconductor sector, while a strong beat could sustain elevated AI valuations despite the yield pressure.

Blackwell is Nvidia's current GPU architecture, including the GB200 and GB300 product lines, which Jensen Huang stated were sold out as of February 2026 with approximately $1 trillion in Blackwell and Rubin orders through 2027. Tonight's commentary on supply cadence and delivery execution will indicate whether Nvidia can fulfil the backlog it has already built.