What NDQ Gives Australian Investors That the ASX Cannot

2 hrs ago

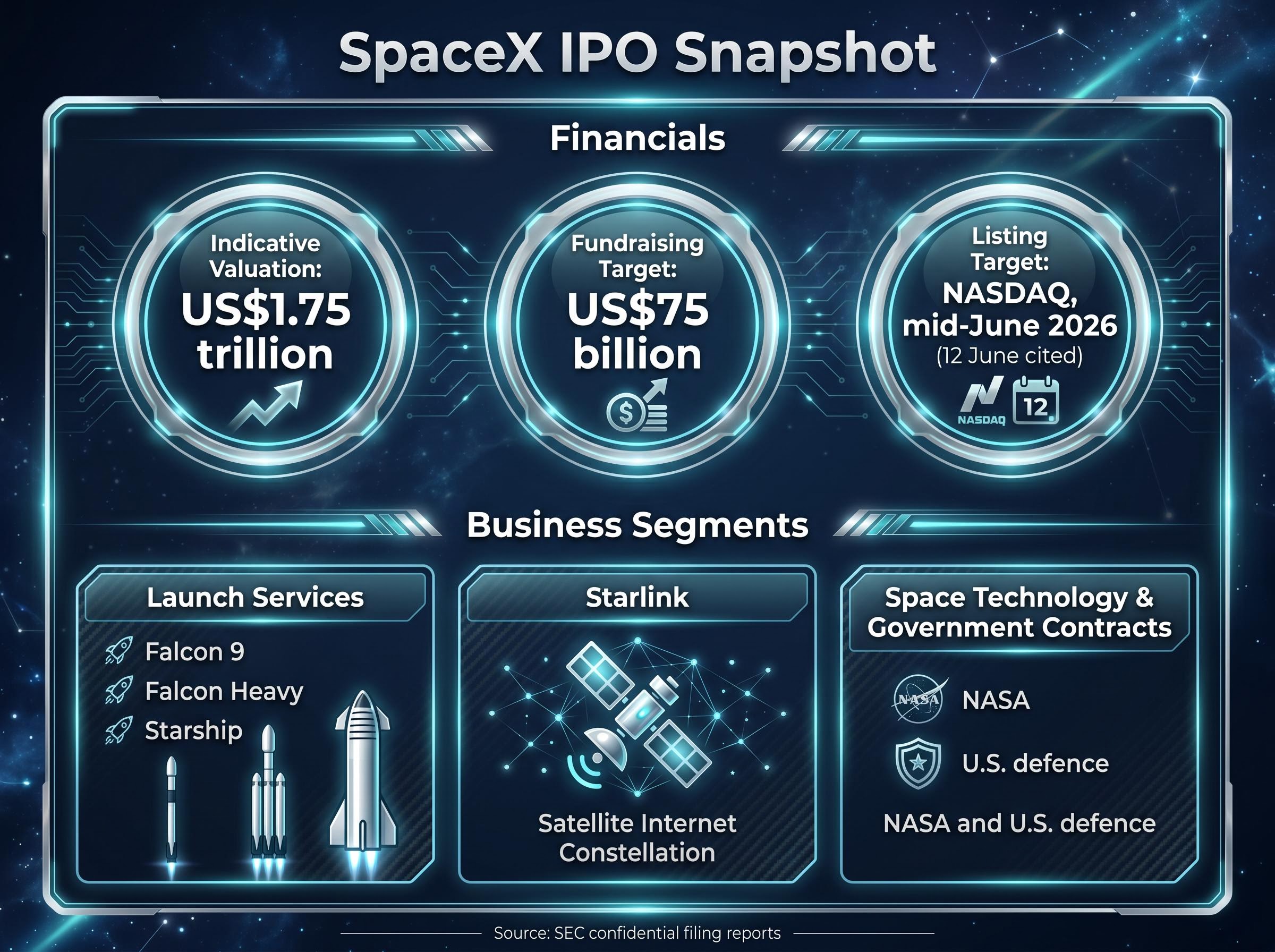

SpaceX has confidentially filed with the SEC for a NASDAQ listing targeting mid-June 2026, at a reported valuation of approximately US$1.75 trillion. For Australian retail investors, the question is not whether to watch this IPO but how to actually access it.

Australian brokers do not offer primary IPO allocations for U.S. listings. Investors who want SpaceX exposure will either need to buy on the secondary market through an international broker, with all the foreign exchange friction and first-day volatility that entails, or consider a newly available domestic route: the BetaShares Space Industry ETF (ASX: RCKT), which launched in the week of 12 May 2026 and tracks the Solactive Space Industry Index.

What follows is a detailed explanation of how RCKT works, what it currently holds, under what conditions SpaceX could be added after its IPO, and how the ETF compares to going direct via a U.S.-market broker. Readers will finish with a clear, practical understanding of which pathway suits their situation.

SpaceX filed confidentially with the SEC in early April 2026, according to reporting from Bloomberg and CNBC. The company is targeting a NASDAQ listing in mid-June, with 12 June 2026 cited in some reports as the working date.

The SEC confidential S-1 submission rules, established under the JOBS Act, allow Emerging Growth Companies to submit draft registration statements for non-public review before a public filing, a provision that gives companies like SpaceX the ability to test investor appetite and finalise pricing terms without triggering immediate public disclosure obligations.

The numbers behind the listing are striking:

US$1.75 trillion. If SpaceX lists at that valuation, it would rank among the most valuable companies on any global exchange.

For Australian retail investors, the scale is only part of the story. The more immediate problem is access. Mainstream domestic brokers, including CommSec, nabtrade, and SelfWealth, do not offer primary allocations for U.S. IPOs. That means no Australian retail investor can subscribe at the IPO offer price through their existing brokerage account. Any participation will happen on the secondary market, at whatever price the stock opens for public trading.

This access gap is what makes the domestic ETF route worth understanding before the listing date arrives.

SpaceX operates across three interdependent business segments, each carrying its own growth thesis and its own execution risk:

The US$1.75 trillion valuation reflects the convergence of these narratives: satellite broadband with a global addressable market, a near-monopoly in commercial launch frequency, and a long-duration bet on Starship as the vehicle for deep-space exploration. Each narrative is credible in isolation. Priced together into a single pre-IPO entity, they produce a valuation that exceeds most listed defence and telecommunications companies combined.

That concentration of ambition in one company is precisely what makes SpaceX compelling and risky at the same time.

Elon Musk holds dominant control over SpaceX’s corporate strategy. The Financial Times and Wall Street Journal have both flagged recurring concerns about this structure: potential for decisions that reflect personal priorities over minority shareholder interests, and conflicts of interest across Musk’s simultaneous leadership of Tesla, xAI, and SpaceX. For investors evaluating post-IPO exposure, this governance concentration is a factor that cannot be diversified away.

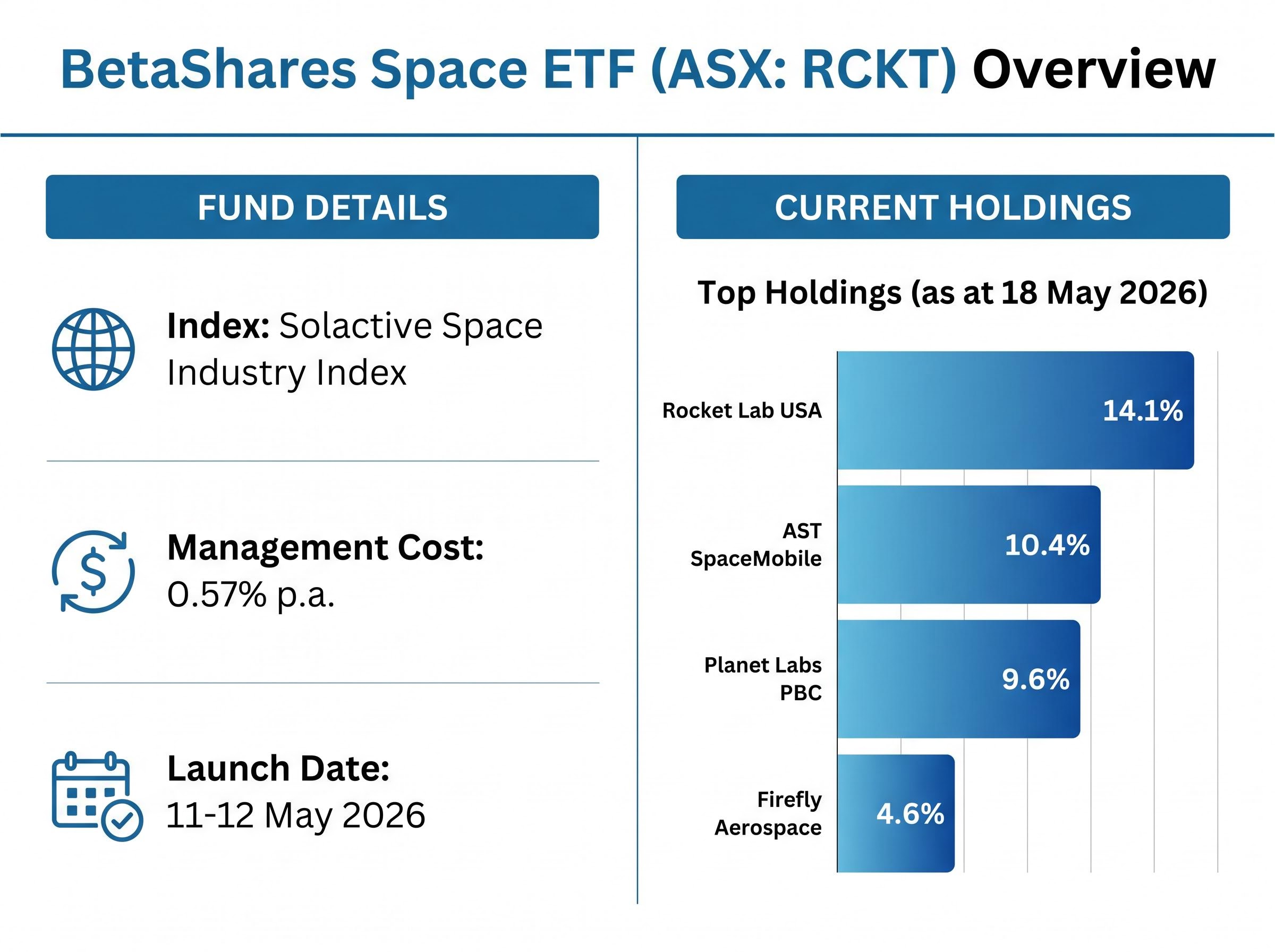

RCKT is not an actively managed fund where a portfolio manager decides which stocks to buy. It is an index-tracking ETF that follows the Solactive Space Industry Index. The portfolio composition is driven by rules built into the index methodology, not by fund manager judgement calls.

The fund’s mandate covers companies deriving material revenue from space-related activities: launch services, satellite manufacturers and operators, space technology, ground equipment, and businesses enabling the commercialisation of space.

| Fund Detail | Value |

|---|---|

| Fund Name | BetaShares Space ETF |

| Ticker | RCKT (ASX) |

| Index Tracked | Solactive Space Industry Index |

| Management Cost | 0.57% p.a. |

| Launch Date | Approximately 11-12 May 2026 |

One feature is directly relevant to SpaceX. RCKT includes a fast-track mechanism for newly listed companies. This means qualifying names can be added outside regular index rebalance cycles, which matters for a high-profile post-IPO addition. The distinction is important: SpaceX inclusion is a rules-based process governed by the Solactive methodology, not a discretionary promise from BetaShares.

Understanding that difference is what separates realistic timing expectations from marketing assumptions.

RCKT’s launch metrics and risk profile reveal details that matter before transacting: the fund opened at $14.00 per unit, carries an estimated annualised volatility of 28%, and UBS Australia has recommended capping the position at less than 5% of a portfolio, a sizing discipline that changes the practical calculus for investors thinking about it as a meaningful SpaceX proxy.

As at 18 May 2026, RCKT’s portfolio is concentrated in established space-sector names. SpaceX does not appear because it is not yet publicly listed.

| Company | Ticker | Approximate Weighting (18 May 2026) |

|---|---|---|

| Rocket Lab USA | NASDAQ: RKLB | ~14.1% |

| AST SpaceMobile | ~10.4% | |

| Planet Labs PBC | NYSE: PL | ~9.6% |

| Firefly Aerospace | ~4.6% |

For SpaceX to be added post-IPO, four conditions need to be met under the Solactive index methodology and RCKT’s fund rules:

SpaceX inclusion in RCKT is subject to the Solactive index methodology and fast-track provisions. BetaShares has made no public commitment to a specific inclusion date or timetable.

Third-party Australian commentators, including Livewire Markets and various ETF research blogs, have speculated that inclusion could occur within weeks to a few months of listing. These are expectations, not guarantees. No firm, dated forecast for an exact RCKT inclusion date is publicly available.

Buying RCKT today provides diversified space-sector exposure. Whether it constitutes meaningful SpaceX pre-positioning depends entirely on how quickly the index methodology and fast-track provisions operate after the IPO settles.

The decision between going direct and using the ETF comes down to what kind of exposure the investor actually wants, and what friction they are willing to accept.

The ownership structure differences between ETFs and direct shares extend beyond cost and diversification: direct shareholders in a listed company hold legal title on the share registry and receive corporate actions directly, while ETF unitholders own a proportional interest in the fund’s trust structure, with corporate actions, voting rights, and income distribution handled by the fund manager on their behalf.

| Factor | Direct U.S. Market (Secondary) | RCKT via ASX |

|---|---|---|

| Access method | International broker (e.g., Stake, Interactive Brokers Australia) | Any ASX broker |

| Currency | USD (AUD/USD conversion required) | AUD |

| FX cost | Varies by broker; check current pricing before transacting | Internalised by fund |

| SpaceX specificity | 100% SpaceX exposure | Diversified basket; SpaceX inclusion not guaranteed on fixed timetable |

| Management cost | Nil (brokerage fees apply) | 0.57% p.a. |

Investors going direct cannot access the IPO offer price. They will buy at whatever the secondary market opens at, which in large U.S. tech IPOs, as historical analogues such as Coinbase and Airbnb illustrate, can be substantially above the institutional allocation price. Lock-up expiry periods, when insiders are permitted to sell, introduce further timing risk in subsequent months.

Australian financial adviser commentary published in May 2026, including analysis from Morningstar Australia and Livewire Markets, has emphasised that thematic ETFs are generally preferred over single-stock IPO positions for risk management and position-sizing purposes, particularly where valuation and governance risks are elevated.

RCKT removes the FX friction and international brokerage complexity. It trades on the ASX in Australian dollars like any domestic security. The trade-off is clear: the exposure is to the broader space sector, not to SpaceX specifically, and the 0.57% annual management cost represents an ongoing drag relative to direct ownership.

Both access pathways carry real risk. The categories are distinct, and worth separating.

SpaceX valuation scepticism has a concrete analytical basis: at a 250x EBITDA multiple, the reported figure prices in decades of future growth across Starlink, launch services, and Starship, and multiple analyst assessments cited in international financial press have flagged approximately 30% overvaluation risk even before accounting for governance or execution variables.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

RCKT is the lower-friction pathway for most Australian retail investors who want space-sector exposure in the near term. It is AUD-denominated, requires no international brokerage account, provides diversified exposure across the space sector, and offers a credible path to SpaceX inclusion post-IPO through its fast-track mechanism, even if the timeline remains uncertain.

Investors who want SpaceX specifically, rather than thematic space exposure, will need to go direct via a U.S.-market broker and accept secondary market pricing, FX costs, and first-day volatility.

Before committing capital under either route, three steps are worth completing:

The public S-1 filing has not been released as of late May 2026. Once available, it will provide the first detailed financial disclosure on SpaceX’s revenue, costs, and contract structure, allowing a more grounded valuation assessment before committing capital.

For investors who want to work through the prospectus systematically once it lands on SEC EDGAR, our dedicated guide to reading the SpaceX S-1 covers the specific sections that matter most, including revenue breakdown by segment, governance disclosures on Musk’s control structure, and how to interpret the Saudi Aramco pricing precedent as a reference point for bookbuilding outcomes.

Neither pathway guarantees access at the IPO offer price. The difference is in friction, specificity, and how much uncertainty the investor is comfortable carrying.

The BetaShares Space Industry ETF (ASX: RCKT) is an index-tracking fund that follows the Solactive Space Industry Index, covering companies with material revenue from space-related activities. It launched in May 2026 and includes a fast-track mechanism that could allow SpaceX to be added to the portfolio after its NASDAQ listing, subject to meeting the index methodology's eligibility criteria.

No. Australian retail brokers including CommSec, nabtrade, and SelfWealth do not offer primary allocations for U.S. IPOs, so Australian investors cannot subscribe at the IPO offer price and would need to buy on the secondary market through an international broker after trading begins.

SpaceX filed confidentially with the SEC in early April 2026 and is targeting a NASDAQ listing in mid-June 2026, with 12 June 2026 cited in some reports as the working date, at an indicative valuation of approximately US$1.75 trillion.

Key risks include SpaceX inclusion not being guaranteed on any fixed timetable, the fund having essentially no performance track record since it launched in May 2026, a 0.57% annual management cost acting as an ongoing drag, and concentration in a single sector where many holdings are pre-profit and trade at high revenue multiples.

Australian investors can buy SpaceX shares on the secondary market through international brokers such as Stake or Interactive Brokers Australia, which provide access to U.S. markets, though this requires AUD to USD currency conversion and exposes buyers to first-day volatility rather than the IPO offer price.