Nvidia is expected to report fiscal Q1 FY27 results after market close today, 19 May 2026, with shares trading near $225 and an implied market capitalisation above $5.5 trillion. Wall Street already expects a beat. The question driving real money is what comes after the headline.

Bank of America analyst Vivek Arya has framed tonight’s report around five investor debates that will matter more than the top-line result itself. These include whether Nvidia can hold gross margins near 75%, when the Vera Rubin architecture actually ships at scale, and whether management updates its $1 trillion multi-year revenue forecast. What follows is a structured framework for interpreting tonight’s results in real time, covering what to watch, why each debate moves the stock, and what BofA’s bull case depends on.

The baseline everyone agrees on, and why it is not the story tonight

BofA’s Arya projects Nvidia will beat sell-side revenue estimates by 2% to 4%, equivalent to roughly $2 billion to $4 billion above consensus. That sounds like a strong result. It is not the story.

BofA’s Vivek Arya projects Nvidia will exceed sell-side revenue estimates by 2% to 4%, approximately $2 billion to $4 billion above consensus.

The beat is so widely anticipated that it is already embedded in the share price. For context, Nvidia delivered Q1 FY26 revenue of $44.06 billion, up 69% year-over-year, beating consensus of approximately $43.09 billion. That kind of outperformance has become the baseline, not the exception.

BofA maintains a Buy rating with a $320 price target, implying roughly 42% upside from today’s price. That gap between where the stock sits and where the bull case points means the reaction tonight hinges entirely on guidance quality and the five debates below.

Whisper number dynamics are adding another layer of complexity to tonight’s setup: following pre-earnings upgrades from Goldman Sachs, Citi, and Wells Fargo, the effective hurdle rate for a positive stock reaction has drifted materially above the published consensus of $1.75-$1.77 EPS, while options markets are pricing a plus or minus 5.8% swing in shares on the session after results.

When big ASX news breaks, our subscribers know first

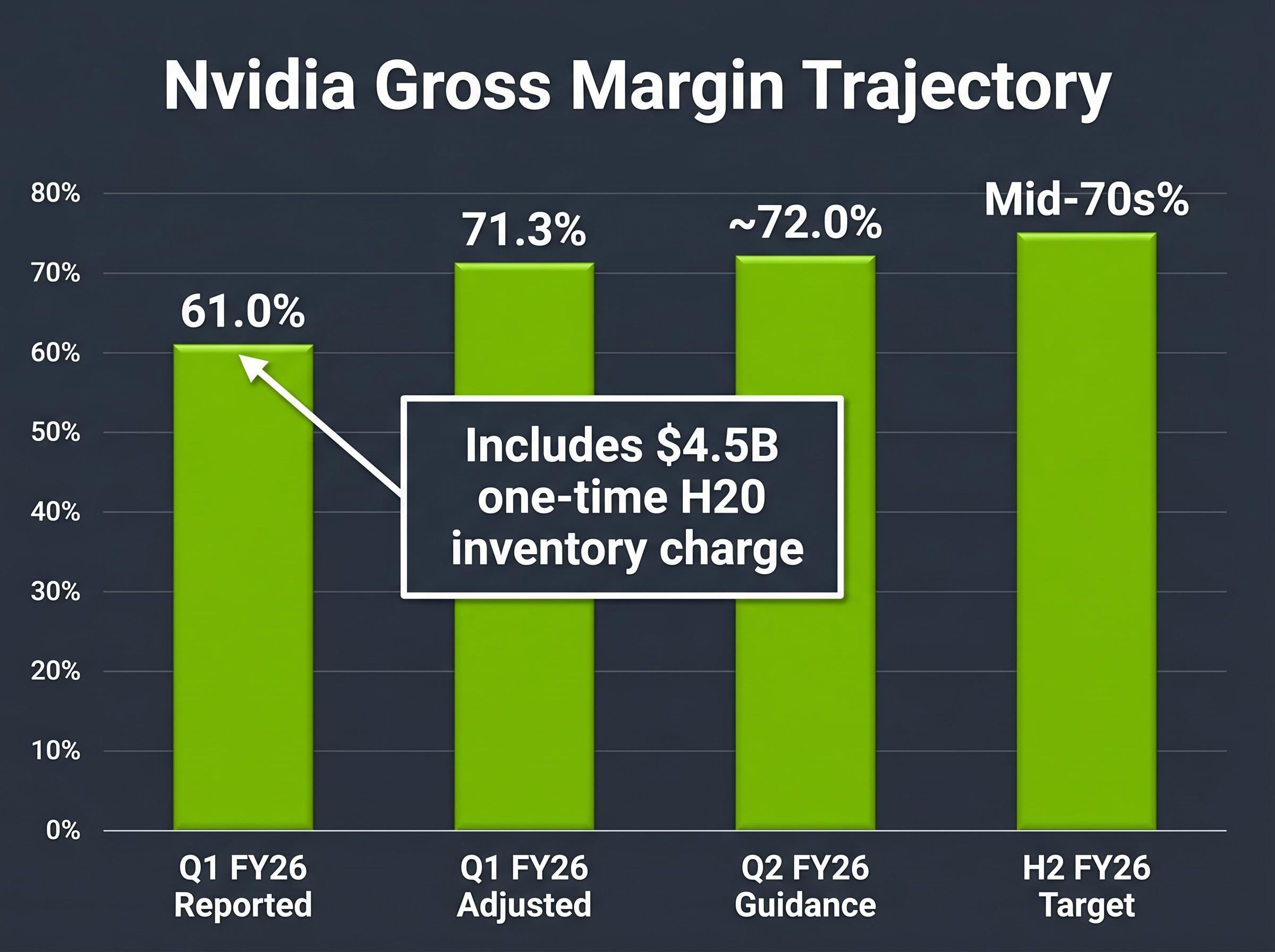

Why gross margin near 75% is harder to hold than it looks

BofA has flagged sustainability of gross margins near 75% as one of the central investor debates. The number itself looks strong. What sits underneath it is more complicated.

The Q1 FY26 non-GAAP gross margin came in at 61.0% as reported, but that figure included a one-time $4.5 billion inventory charge related to H20 chips restricted under export controls. Excluding that charge, the adjusted margin was 71.3%. Management guided Q2 FY26 non-GAAP gross margin to approximately 72% and stated a target of the mid-70% range for the back half of FY26.

The Commerce Department H20 export licensing reversal, which reinstated shipment approvals after an earlier ban, arrived in time to reduce the actual Q1 inventory charge below Nvidia’s initial $8 billion warning, with material reuse accounting for the shortfall, making the adjusted margin figure of 71.3% a cleaner baseline than the reported 61.0% suggests.

| Period | Non-GAAP Gross Margin | Notes |

|---|---|---|

| Q1 FY26 (reported) | 61.0% | Includes $4.5B H20 inventory charge |

| Q1 FY26 (adjusted) | 71.3% | Excluding one-time H20 charge |

| Q2 FY26 (guidance) | ~72.0% | Plus or minus 50 basis points |

| H2 FY26 (target) | Mid-70s% | Management’s stated trajectory |

The primary headwind is high-bandwidth memory (HBM), the specialised memory chips that sit alongside GPUs in data centre accelerators. Supply remains tight, and pricing power rests with vendors including SK Hynix, Samsung, and Micron. A margin print at or above 75% tonight would validate Nvidia’s pricing power and platform lock-in. A compression miss would raise structural questions that headline revenue beats cannot offset.

HBM pricing power is being tested by conditions that go beyond Nvidia’s negotiating position: SK Hynix and Micron have both sold out HBM capacity through 2026-2027, a supply condition driven by manufacturing complexity rather than capital investment alone, and a Samsung labour strike scheduled for 21 May 2026 could reduce DRAM supply by a further 3-4% at exactly the moment Nvidia is reporting.

What the Vera Rubin timeline actually tells investors about execution

Vera Rubin, Nvidia’s next-generation data centre GPU architecture, is targeted for an H2 2026 ramp. BofA has flagged the deployment timeline as one of its five investor debates, and for good reason: analyst models that rely on Vera Rubin revenue contribution in the second half of the year carry meaningful uncertainty without concrete operational signals.

The current flagship Blackwell architecture is the reference point against which Rubin’s incremental contribution is being modelled. What investors need from tonight’s call is specificity, not reassurance.

Three signals would constitute a credible Vera Rubin update:

- Named customer or hyperscaler design-win validation

- Volume or shipment timeline language beyond prior guidance

- Margin profile expectations for the new architecture relative to Blackwell

Without at least one of these, the Vera Rubin ramp remains a roadmap item rather than an execution milestone. A vague update would be interpreted as a yellow flag for revenue continuity beyond current Blackwell demand, and would weigh on FY27 back-half and FY28 modelling across the buy side.

The $1 trillion forecast and what an update means for long-term models

Nvidia has previously communicated a $1 trillion revenue forecast covering calendar years 2025 through 2027. Tonight, investors will be listening for any reaffirmation, revision, or silence on this figure.

Hyperscaler capex commitments from Amazon, Meta, Microsoft, and Alphabet, totalling a combined $600-$725 billion in board-approved 2026 guidance, are the structural demand signal underpinning Nvidia’s order visibility and the reason analysts model data centre revenue at roughly 93% of total company revenue for the current quarter.

Nvidia’s stated revenue target: $1 trillion in cumulative revenue across calendar years 2025 to 2027.

This three-year forecast functions as a commitment mechanism for every institutional model on the stock. Three scenarios carry distinctly different implications:

- Forecast reaffirmed: Signals stable demand visibility and maintains existing buy-side models as calibrated.

- Forecast raised: Signals accelerating hyperscaler capital expenditure and would likely trigger upward earnings revisions across the sell side.

- Forecast hedged or softened: Would trigger model resets, as any qualification of the number introduces uncertainty into three years of earnings projections simultaneously.

BofA projects the long-term AI total addressable market at more than $1.7 trillion by 2030, with Nvidia capturing approximately 70% of that revenue. The $1 trillion forecast implicitly assumes Nvidia defends dominant AI infrastructure share against hyperscaler custom silicon from Google, Amazon, and Microsoft. For long-duration investors, this may be the single most consequential disclosure of the evening.

Nvidia’s competitive moat, and where hyperscaler custom silicon actually threatens it

BofA’s bull case rests on a specific argument about competitive positioning: Nvidia has built a highly standardised infrastructure spanning software (CUDA), developer tools, and multi-cloud accessibility that is structurally difficult for custom silicon to displace in training workloads. The ecosystem, not just the chip, is the moat.

The competitive threat is real, but it is concentrated. Google’s TPU line, Amazon’s Trainium and Inferentia chips, and Microsoft’s Maia accelerators are primarily competitive in inference and steady-state workloads, where cost optimisation matters more than peak training performance.

Broadcom’s custom ASIC contracting model, which locks in multi-year supply agreements with Google and Meta extending through at least 2029, represents the structural alternative to Nvidia’s GPU flywheel that investors must understand when evaluating competitive durability: the two architectures frequently coexist within the same hyperscaler data centre rather than substituting for each other, which matters for how investors should read any hyperscaler capex diversification signal tonight.

| Company | Chip Name | Primary Workload Strength | Threat to Nvidia Training Revenue |

|---|---|---|---|

| TPU | Internal AI workloads, select Cloud inference | Low to moderate | |

| Amazon | Trainium / Inferentia | Cost-efficient training and inference | Low to moderate |

| Microsoft | Maia | Internal inference, negotiating leverage | Low |

BofA has also addressed Nvidia’s partnerships with companies such as OpenAI and Anthropic, arguing these have been incorrectly framed as circular financing arrangements. BofA characterises them instead as strategic ecosystem bets.

BofA argues Nvidia’s investments in AI ecosystem companies have been “incorrectly framed as circular financing” and are instead legitimate strategic positioning within the AI infrastructure stack.

Understanding precisely where competition applies, and where it does not, prevents investors from either dismissing the threat entirely or over-weighting headlines about custom chip announcements that do not actually threaten Nvidia’s core training revenue.

The next major ASX story will hit our subscribers first

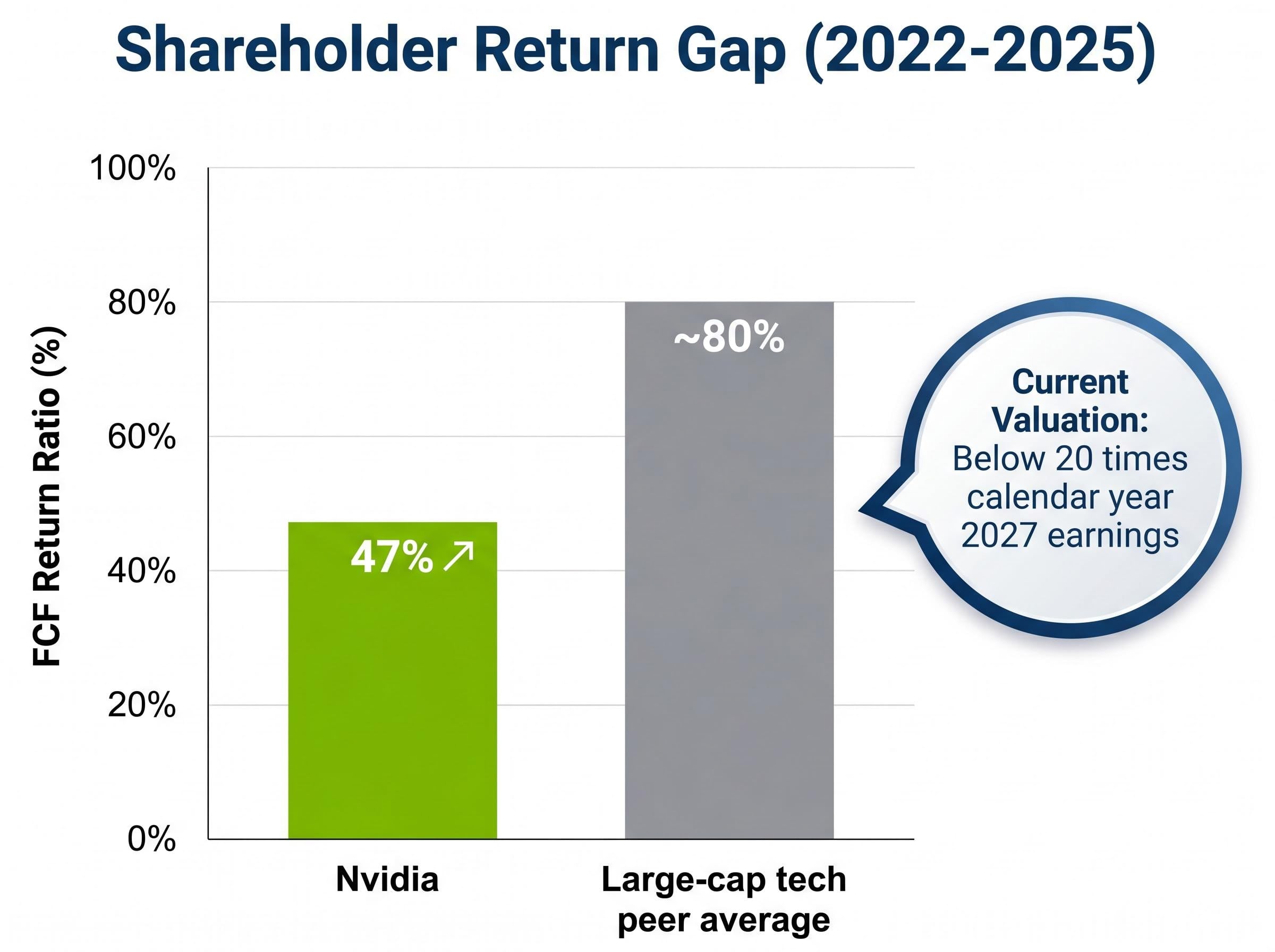

The shareholder return gap that BofA says is a valuation opportunity in disguise

Between 2022 and 2025, Nvidia returned only 47% of free cash flow to shareholders via dividends and buybacks. That figure looks modest on its own. It looks even more striking against comparable large-cap technology peers, which returned approximately 80% over the same period.

- Nvidia FCF return ratio (2022-2025): 47%

- Large-cap tech peer average: approximately 80%

- The gap implies Nvidia has been reinvesting aggressively at the expense of shareholder distributions, a deliberate strategic choice rather than a capital allocation failure.

BofA argues this gap, combined with a current valuation below 20 times calendar year 2027 earnings, represents a misidentified discount. Increasing distributions could broaden the investor base and compress the valuation gap without any change in operating fundamentals.

What tonight’s call could signal on capital returns

For income-oriented and valuation-sensitive investors, any language on buyback authorisation size, dividend policy, or capital return cadence would signal a shift toward the peer group norm. This debate sits entirely outside the AI growth narrative, and that is precisely what makes it a potential re-rating lever.

Five debates, one report, and what to listen for after market close

The beat-and-raise headline is the floor tonight, not the ceiling. The stock reaction will be determined by guidance quality across five dimensions, ranked by near-term market impact: gross margin print first, Vera Rubin deployment language second, $1 trillion forecast commentary third, competitive moat signals fourth, and capital return language fifth.

BofA’s bull case anchors to a $320 price target, approximately 70% AI accelerator revenue share in a market exceeding $1.7 trillion by 2030, and a multi-year compounding thesis that tonight’s commentary either validates or complicates. The numbers after market close will be known within minutes. The language that accompanies them will take longer to parse, and will matter more.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including BofA’s price target and revenue projections, are subject to change based on market developments and company performance.