The four largest AI hyperscalers are collectively channelling hundreds of billions of dollars into AI infrastructure in 2026, and the first stop for that capital is semiconductors. For Australian retail investors, direct access to the companies building AI at scale remains limited, but ASX-listed AI ETFs now offer targeted exposure to the semiconductor supply chain and the physical infrastructure layer powering it. The Global X Semiconductor ETF (ASX: SEMI) has returned approximately 51% year-to-date as of mid-May 2026, forcing a pointed question: chase the run, wait for a pullback, or look elsewhere in the AI spending chain? What follows profiles three ASX-listed ETFs capturing AI infrastructure spending at different points in the supply chain, with analyst entry point guidance, concentration risk detail, and a framework for matching each fund’s risk profile to an investor’s tolerance.

Why hyperscaler AI spending lands in semiconductors first

Between 70% and 75% of combined hyperscaler capital expenditure is directed specifically toward AI infrastructure rather than general cloud expansion, according to analyst aggregation from James Gerrish at Shaw and Partners via Market Matters. The corporate rationale is straightforward.

The dominant hyperscalers believe that falling behind in AI carries greater competitive risk than the risk of over-investing.

Microsoft CEO Satya Nadella reiterated in May 2025 a commitment to invest “over $50 billion annually” in AI and cloud infrastructure. Meta Platforms raised its 2025 capex guidance to $35-40 billion, with management indicating the “vast majority” is directed at AI and data centres.

Hyperscaler capex commitments reached $130 billion in Q1 2026 alone, with full-year 2026 combined guidance for Amazon, Microsoft, Alphabet, and Meta sitting at approximately $725 billion, a figure that provides the structural demand floor semiconductor ETFs are pricing in.

The capital flows in a specific order:

- Chips and semiconductors: GPUs, custom accelerators, networking silicon, and high-bandwidth memory

- Physical infrastructure: Data centres, power generation, cooling systems, and grid upgrades

- Cloud software and workloads: Applications running on the hardware above

GPUs, custom silicon, and networking chips sit at the front of the capex queue because no data centre, model, or smart device can function without them. That structural front-loading is what makes semiconductor ETFs the most direct vehicle for capturing AI spending as it happens.

When big ASX news breaks, our subscribers know first

What ASX: SEMI actually holds and how it is structured

SEMI tracks the Solactive Semiconductor 30 Index and holds 31 globally listed equities, with more than 60% US-listed exposure. Assets under management sit in the range of approximately $732-903 million based on April-May 2026 data points.

Three holdings anchor the fund’s AI thesis, each capturing a different link in the chip ecosystem.

Investors comparing chip-focused options within the Global X fund family should note that the GXAI vs SEMI distinction matters at the portfolio construction level: SEMI concentrates on the semiconductor supply chain from design through fabrication, while GXAI adds cloud infrastructure, enterprise AI software, and AI-enabled services to the underlying index.

| Holding | Role in AI chain | Key recent metric | Why it matters for SEMI |

|---|---|---|---|

| Nvidia | AI GPU compute | Data-centre revenue of $22.6 billion (quarter ended 27 April 2025), up approximately 400% YoY | Largest single driver of fund returns; sets the tone for AI demand sentiment |

| TSMC | Advanced node foundry | 2025 capex guidance of US$28-32 billion for AI and HPC nodes | Sole manufacturer of leading-edge AI chips; bottleneck with pricing power |

| Broadcom | Networking and custom silicon | AI-related revenue expected to exceed $13 billion in FY25 | Captures the networking and custom accelerator layer beyond GPUs |

Concentration risk and what it means in practice

Heavy weighting to Nvidia and TSMC means a single earnings miss or export control headline can swing the fund’s unit price materially. This is not ordinary equity volatility.

TSMC’s geographic concentration in Taiwan adds a geopolitical risk layer that persists regardless of the company’s financial performance. A disruption to Taiwanese semiconductor output would affect nearly every AI-capable chip in production globally.

TSMC’s control of advanced node production extends to approximately 90% of the world’s most sophisticated chip manufacturing, a concentration level that means any disruption to Taiwanese semiconductor output cascades across every hyperscaler’s AI build-out simultaneously rather than affecting individual supply chains in isolation.

ASX: SEMI performance and analyst entry point guidance

SEMI has delivered a year-to-date return of approximately 51% as of mid-May 2026, with the unit price at $35.47 (down 2.3% on the day at time of reporting). The approximate 2026 return to that point stood at roughly 36%.

That performance creates a genuine dilemma for investors who missed the move.

James Gerrish at Shaw and Partners has indicated a preferred entry point of approximately $31 per unit, with additional buying interest on dips of $3-4 from current levels. This represents analyst opinion and should not be treated as personal financial advice.

Gerrish favours accumulating on pullbacks rather than chasing elevated valuations, given cyclical risk and a compressed margin of safety at current prices. For the latest unit price, the ASX quote page is available at ASX: SEMI.

The key risk factors at current levels include:

- Over-build cycle if hyperscaler spending decelerates faster than expected

- US export controls on advanced chips restricting market access

- Elevated valuation multiples reducing the margin of safety

- Geopolitical risk concentrated in TSMC’s Taiwan operations

ASX: AINF, the physical infrastructure layer of AI spending

After two sections focused on chips, the analytical lens shifts. Global X AI and Innovative Infrastructure ETF (ASX: AINF) targets the layer that makes the chip layer possible: the companies that physically build and power AI data centres.

AINF was the first ASX-listed fund specifically targeting physical AI infrastructure, launched in April 2025.

The fund holds 31 equities with approximately 50% US-listed exposure. Top holdings include Delta Electronics, GE Vernova, and Vertiv Holdings. The composition spans three categories:

- Energy and utilities: Power generation and grid infrastructure serving data centre demand

- Materials and commodities: Copper and uranium producers supplying physical inputs

- Engineering and data centre equipment: Cooling, power distribution, and facility construction

At time of reporting, the unit price was $17.44 (down 2.5% on the day), with a year-to-date return of approximately 17% and a 2026 return of roughly 20%.

Gerrish’s preferred entry sits below $18, with additional buying interest below $17. For investors seeking AI exposure with lower sensitivity to chip-cycle volatility, AINF offers a risk profile tied more to electricity demand, construction timelines, and commodity inputs than to GPU earnings beats.

ASX: IFRA, the broad infrastructure play with an AI tailwind

VanEck FTSE Global Infrastructure (Hedged) ETF (ASX: IFRA) represents the most conservative option in this group. The trade-off is explicit: lower direct AI sensitivity in exchange for yield, diversification, and currency hedging.

The fund holds approximately 150 equities with more than 70% US and Canadian exposure, currency-hedged to AUD. Its AI relevance comes from data centre electricity demand flowing through to utilities and grid operators, not from direct semiconductor exposure.

The largest individual holding is Transurban Group (ASX: TCL), a name familiar to most Australian investors and an indicator of how different this fund’s character is from SEMI.

At time of reporting, the unit price stood at $25.19 (up 1.2% on the day), with a year-to-date return of approximately 8%, a 12-month return exceeding 16%, and a forward dividend yield of nearly 3% over the next 12 months. Gerrish holds the fund in his Core ETF portfolio with a long, bullish position.

| ETF ticker | AI exposure layer | YTD return (approx.) | Holdings count | Key risk |

|---|---|---|---|---|

| SEMI | Semiconductors (chips, GPUs, foundry) | 51% | 31 | Nvidia/TSMC concentration; export controls |

| AINF | Physical infrastructure (power, cooling, materials) | 17% | 31 | Commodity input costs; construction delays |

| IFRA | Broad global infrastructure (utilities, transport, grid) | 8% | ~150 | Indirect AI link; lower return potential |

The next major ASX story will hit our subscribers first

How AI capex translates into semiconductor demand, the mechanism explained

AI model training requires massive parallel computation. Only high-end GPUs and custom ASICs, such as those designed by Nvidia and Broadcom, can provide this at scale. That concentrated demand funnels through a single dominant foundry: TSMC, whose growth in Q1 2025 was attributed to “strong demand for HPC and AI applications” at 3nm and below.

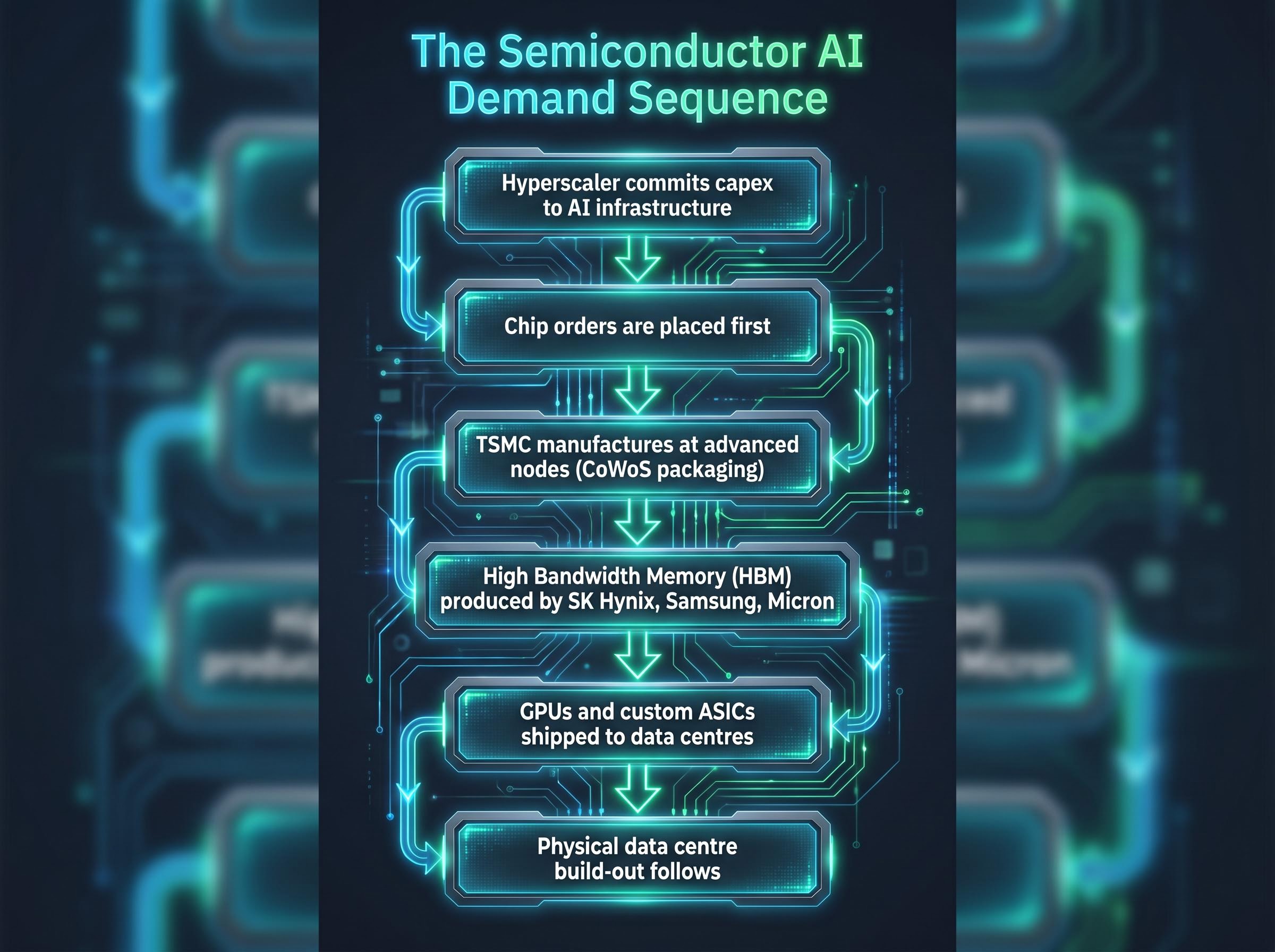

The demand chain follows a specific sequence:

- Hyperscaler commits capex to AI infrastructure

- Chip orders are placed first, before physical construction begins

- TSMC manufactures at advanced nodes, with advanced packaging (CoWoS) acting as a capacity-constrained bottleneck

- High Bandwidth Memory (HBM) is produced alongside to feed the GPUs

- GPUs and custom ASICs are shipped to data centre sites

- Physical data centre build-out follows around the installed compute

Semiconductor demand is front-loaded because nothing else in the chain can proceed without chips.

The HBM angle: why memory demand tracks GPU demand

High Bandwidth Memory is the memory technology specifically designed for AI GPU workloads, distinct from standard DRAM. AI GPUs are only as fast as the memory feeding them, making HBM demand a direct corollary of GPU orders.

Supply is concentrated among SK Hynix, Samsung, and Micron, and capacity constraints here mirror the TSMC CoWoS bottleneck. This means investors tracking GPU demand should also monitor memory supply as a signal of whether the AI build-out is accelerating or plateauing.

The memory chip supercycle now unfolding differs structurally from prior DRAM cycles because AI data centre operators account for an estimated 70% of total memory shipment volumes, meaning HBM demand is no longer a niche GPU-specific input but the primary demand centre for the entire memory industry.

The AI infrastructure spending wave still has years to run, but entry price matters

The structural case remains intact. Hyperscaler capex commitments are multi-year, semiconductor demand is front-loaded in the cycle, and the three ETFs profiled capture different risk-and-return points along the same spending chain.

The central investor dilemma is equally clear. SEMI has already delivered approximately 51% year-to-date, AINF roughly 17%, and IFRA about 8%. The risk-reward profile is now asymmetric compared to entry points earlier in the year.

- SEMI: Highest return potential, highest concentration risk; suited to investors willing to accept chip-cycle volatility for maximum AI exposure

- AINF: Moderate return profile, commodity and construction risk; suited to investors who want AI exposure through the physical infrastructure layer

- IFRA: Lower return potential with income and diversification; suited to investors prioritising yield and reduced volatility with an AI tailwind

The analyst entry point guidance (SEMI at approximately $31, AINF below $18) offers a framework for thinking about margin of safety rather than a directive to act at a specific price. Readers should verify current unit prices, management expense ratios, and updated factsheets at the Global X product pages and VanEck IFRA page before making any decisions.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Analyst commentary referenced in this article represents opinion, not personal financial advice.