Pro Medicus Down 41%: Great Business, but Is It Cheap?

9 mins ago

One ETF gives Australian investors simultaneous exposure to nearly 2,100 Asian companies, yet a single Taiwanese chipmaker accounts for more than 13.6% of the entire portfolio. That tension sits at the centre of the Vanguard FTSE Asia ex Japan Shares Index ETF (ASX: VAE) investment case.

With Australian investors increasingly looking beyond domestic equities for growth, Asia ex-Japan ETFs have attracted growing attention through 2025 and into 2026. VAE sits at the centre of this conversation as one of the two lowest-cost broad-Asia options on ASX, assessed favourably by Morningstar analyst Cerise Bootsma for its cost structure and benchmark tracking quality. This analysis unpacks what VAE actually owns, how its FTSE-based index construction differs from MSCI-based competitors, where the fee advantage sits relative to the field, and what the three dominant country exposures mean for investors willing to hold for the long term.

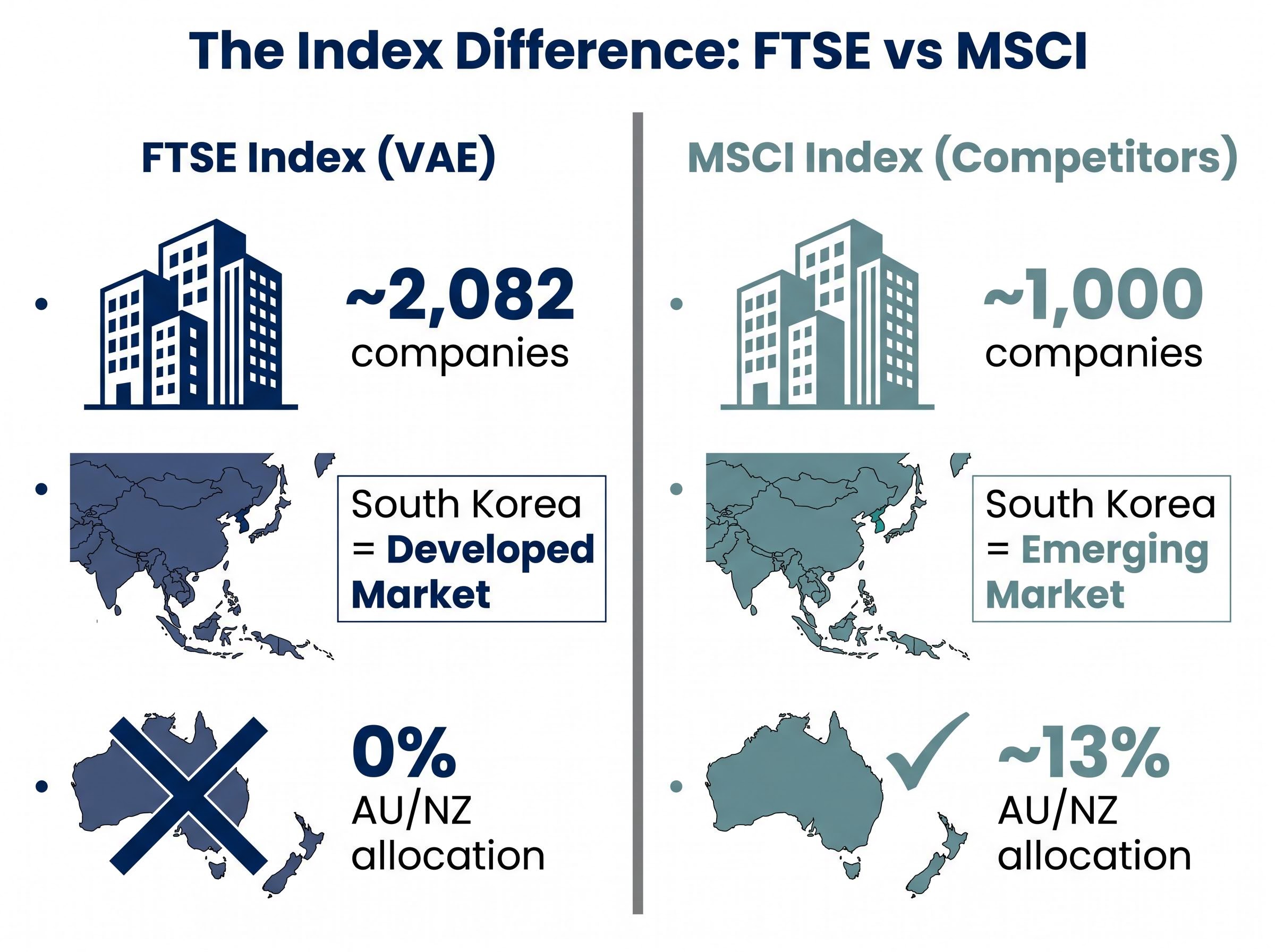

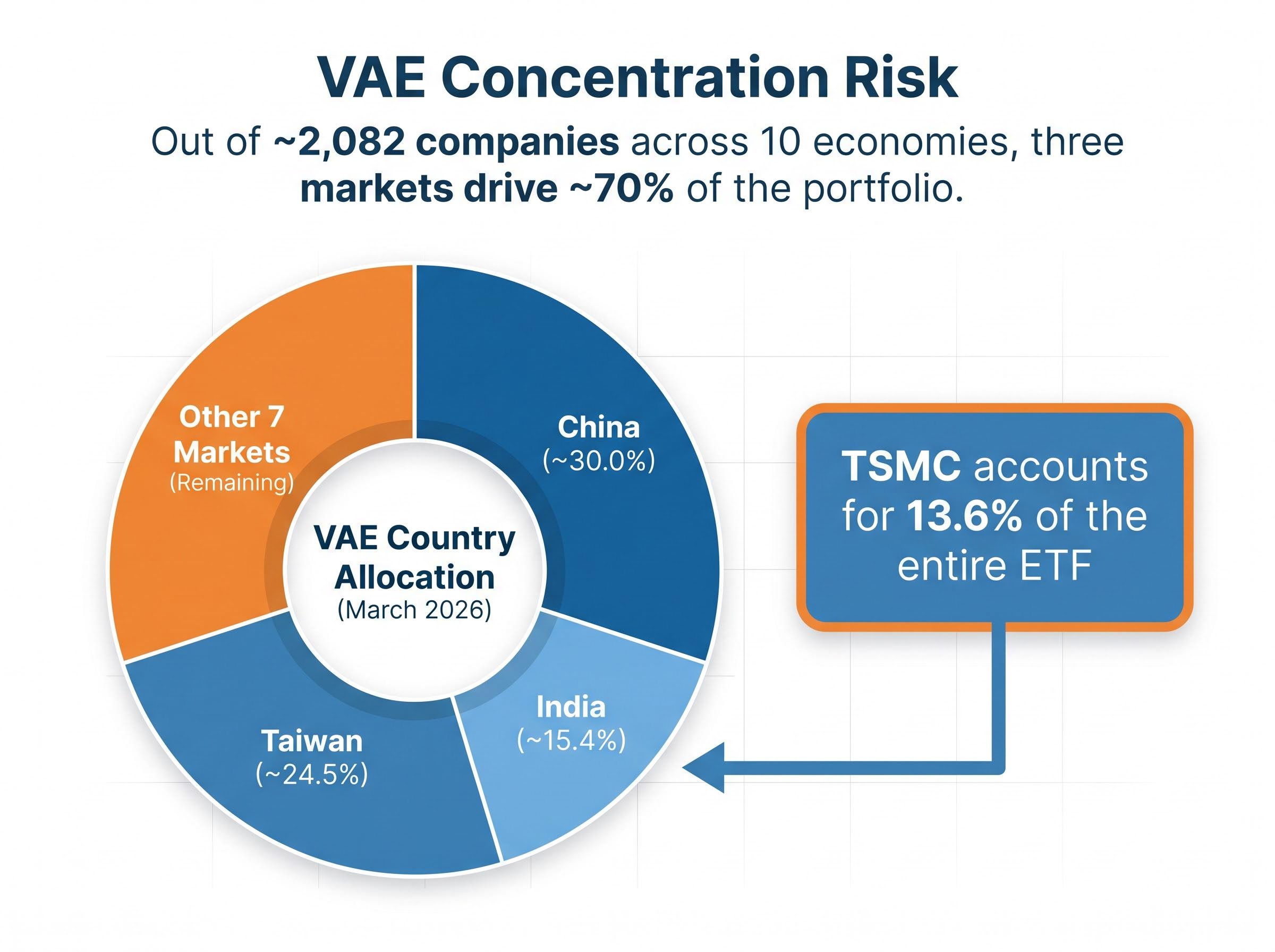

VAE tracks the FTSE Asia Pacific ex Japan, Australia and New Zealand Index, a free-float-adjusted, market-cap-weighted benchmark covering large- and mid-cap equities across 10 Asian economies. As at March 2026, the index held approximately 2,082 constituent companies, rebalanced on a semi-annual schedule.

The markets covered:

That breadth matters. The MSCI All Country Asia ex Japan Index, used by several competing products, holds roughly 1,000 companies. VAE’s index casts a materially wider net.

The single most important structural difference between VAE and MSCI-based Asia ex-Japan products is the treatment of South Korea.

FTSE Russell’s country classification matrix formally lists South Korea under developed market status, the primary structural reason why VAE’s portfolio composition diverges from MSCI-based Asia ex-Japan products that treat the same market as emerging.

FTSE treats South Korea as a developed market; MSCI treats it as emerging. The same regional label, a different portfolio.

This classification decision changes the country weightings an investor is actually buying. The iShares MSCI AC Asia ex Japan ETF (IAAE), which matches VAE’s 0.40% MER, tracks the MSCI index and consequently holds a different Korea, China, and India mix despite the identical fee.

Morningstar’s own category benchmark is the MSCI All Country Asia ex Japan Index, meaning VAE’s “active share” relative to its peer group is structurally baked in from the index choice alone. The average fund in the Asia ex-Japan Morningstar Category allocates roughly 13% to Australia and New Zealand. VAE holds none, a meaningful structural differentiator for Australian investors who already carry domestic equity exposure.

Three country allocations collectively drive most of VAE’s return and risk profile. The concentration builds quickly.

| Country | Approximate Weight (March 2026) | Key Observation |

|---|---|---|

| China | ~30.0% | Largest single-country allocation; regulatory and property sector risk |

| Taiwan | ~24.5% | Dominated by TSMC; geopolitical tail risk |

| India | ~15.4% | Growth engine with elevated valuations across key sectors |

Together, those three markets account for roughly 70% of the portfolio. India, South Korea, and Taiwan collectively represent approximately 56% according to Morningstar’s grouped allocation data. Both technology and financials each exceeded 20% of total portfolio weighting, reinforcing the concentration theme at the sector level.

TSMC alone accounts for 13.6% of the fund, the sharpest expression of the index’s cap-weighting logic. This is not an active decision by Vanguard; it is the mechanical outcome of Taiwan Semiconductor’s dominant market capitalisation flowing through a cap-weighted benchmark.

The top 10 holdings collectively represent 29.4% of the portfolio. Investors entering VAE are making an implicit bet on three distinct country-level risk stories. Knowing the weights makes that bet legible rather than hidden inside a diversification narrative.

VAE charges a management expense ratio of 0.40% per annum, placing it at the lowest tier of Asia ex-Japan ETFs available on ASX. The fee advantage is real, but the competitive picture requires context beyond cost alone.

| ASX Code | Issuer | MER | Index / Mandate | Key Differentiator |

|---|---|---|---|---|

| VAE | Vanguard | 0.40% | FTSE Asia Pacific ex Japan, AU, NZ | Broadest coverage (~2,082 holdings); FTSE methodology |

| IAAE | iShares | 0.40% | MSCI AC Asia ex Japan | MSCI methodology; South Korea as emerging market |

| IAA | iShares | 0.50% | MSCI-linked large-cap Asia ex-Japan | Concentrated 50-stock portfolio; mega-cap focus |

| ASIA | BetaShares | 0.67% | Tech-tilted Asia mandate | Satellite positioning; not broad-market beta |

At the same 0.40% price point as IAAE, VAE’s advantage is not over cost but over mandate design. The choice between them is a question of index philosophy, not savings.

The return dispersion across ASX Asia ETFs over a single year has exceeded 46 percentage points, a gap that reflects fundamentally different index construction and sector tilts rather than simple geographic positioning, and that spread matters considerably when choosing between VAE’s broad-market approach and more concentrated alternatives.

VAE’s securities lending programme provides an additional cost offset:

Passive investing is often treated as a neutral default, a low-cost way to capture market returns without active intervention. In Asian markets, the trade-off is sharper than that framing suggests.

Morningstar’s assessment of the Asia ex-Japan category acknowledges that skilled active managers have historically generated strong results in these markets, particularly in Taiwan and India, where wide return dispersion and structural inefficiencies create opportunities for stock selection to add value. Choosing VAE’s passive approach means accepting cost certainty and low tracking error as compensation for foregoing the possibility of outperformance from active selection.

Vanguard manages tracking quality through three operational levers:

Even small basis-point gaps between fund and benchmark returns compound meaningfully over a 10-20 year holding period. At a 0.40% MER, every basis point of unnecessary tracking error erodes the fee advantage VAE holds over higher-cost alternatives.

Morningstar’s assessment specifically highlights the experienced management team’s proficiency in keeping tracking error low. For a fund where the entire value proposition rests on reliable benchmark delivery at low cost, that operational discipline is not a secondary feature. It is the product.

VAE holds approximately 2,082 companies across 10 markets. The diversification is real at the security level. At the country level, the risk story is concentrated in three engines that interact in ways worth understanding before committing capital.

China (~30%):

Taiwan (~24-25%):

India (~15%):

These three markets collectively account for roughly 70% of the portfolio. Investors who understand these drivers can hold more deliberately through volatility rather than reacting to headline noise.

Vietnam’s scheduled addition to the FTSE index from September 2026 will mark the fund’s first exposure to a frontier-market-reclassified economy.

FTSE Russell is reclassifying Vietnam from frontier to secondary emerging market status, triggering inclusion in the benchmark VAE tracks. The projected weight is approximately 0.2% in 2027, making the initial portfolio impact modest. Symbolically, the addition signals the benchmark’s ongoing evolution and widens the fund’s exposure set beyond its current 10 markets.

Morningstar’s favourable assessment of VAE, attributed to Senior Associate Manager Research Analyst Cerise Bootsma of Morningstar Australasia Pty Ltd, rests on three specific pillars rather than a single summary judgement:

Morningstar positions VAE’s below-average fee structure as a “durable, long-term advantage” for investors, one that compounds over time rather than delivering its value in any single year.

Morningstar’s assessment also acknowledges the active manager opportunity in Asia ex-Japan markets. VAE’s passive approach is framed as a deliberate trade-off: cost certainty and benchmark reliability at the expense of potential alpha from stock selection.

For Australian investors specifically, one structural feature stands out. The average Asia ex-Japan fund in the Morningstar category allocates roughly 13% to Australia and New Zealand. VAE holds 0%, making it a clean regional complement for portfolios already carrying domestic equity exposure through ASX-focused holdings.

The investment case for VAE is structurally sound rather than narratively exciting. Low cost, broad coverage across approximately 2,082 companies, and tight benchmark tracking are strengths best realised over multi-year holding periods. The fund’s approximately A$3.02 billion in assets under management (as at 30 April 2026) reflects steady accumulation by investors who have reached the same conclusion.

The legitimate considerations remain visible: TSMC’s 13.6% single-stock concentration, country-level risk centred on China and Taiwan, and the existence of a price-matched alternative (IAAE) that tracks a different index and may suit different investor preferences depending on views about South Korea’s classification and the FTSE/MSCI methodology split. Vietnam’s scheduled September 2026 index inclusion signals the benchmark’s ongoing evolution, though the near-term portfolio impact will be minimal.

Investors weighing VAE against adjacent emerging market ETFs such as IEM, EMKT, and BEMG will find that many of the same country-level risk engines, particularly Taiwan, China, and India, appear across both the Asia ex-Japan and broad EM categories, making the overlap in underlying exposures worth mapping before adding a second fund.

Investors considering VAE should verify current performance data, MER, and funds under management directly from the Vanguard product page before making any investment decision, and consider how the fund’s country exposures interact with existing Australian or global equity holdings.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

VAE is an ASX-listed ETF managed by Vanguard that tracks the FTSE Asia Pacific ex Japan, Australia and New Zealand Index, providing exposure to approximately 2,082 large- and mid-cap companies across 10 Asian economies at a management expense ratio of 0.40% per annum.

The key structural difference is the treatment of South Korea: FTSE classifies South Korea as a developed market and includes it in VAE's benchmark, while MSCI treats it as an emerging market, resulting in materially different country weightings across the two funds despite both charging 0.40% MER.

Taiwan Semiconductor Manufacturing Company (TSMC) accounts for approximately 13.6% of VAE's portfolio, making it the single largest holding and meaning any Taiwan-specific geopolitical or operational shock would have an outsized impact on the fund's returns.

As at March 2026, China (approximately 30%), Taiwan (approximately 24.5%), and India (approximately 15.4%) are the three dominant country allocations in VAE, collectively accounting for roughly 70% of the total portfolio.

FTSE Russell is reclassifying Vietnam from frontier to secondary emerging market status, which will trigger its inclusion in the benchmark VAE tracks from September 2026, though its projected weight of approximately 0.2% means the near-term portfolio impact will be minimal.