Pro Medicus Down 41%: Great Business, but Is It Cheap?

6 mins ago

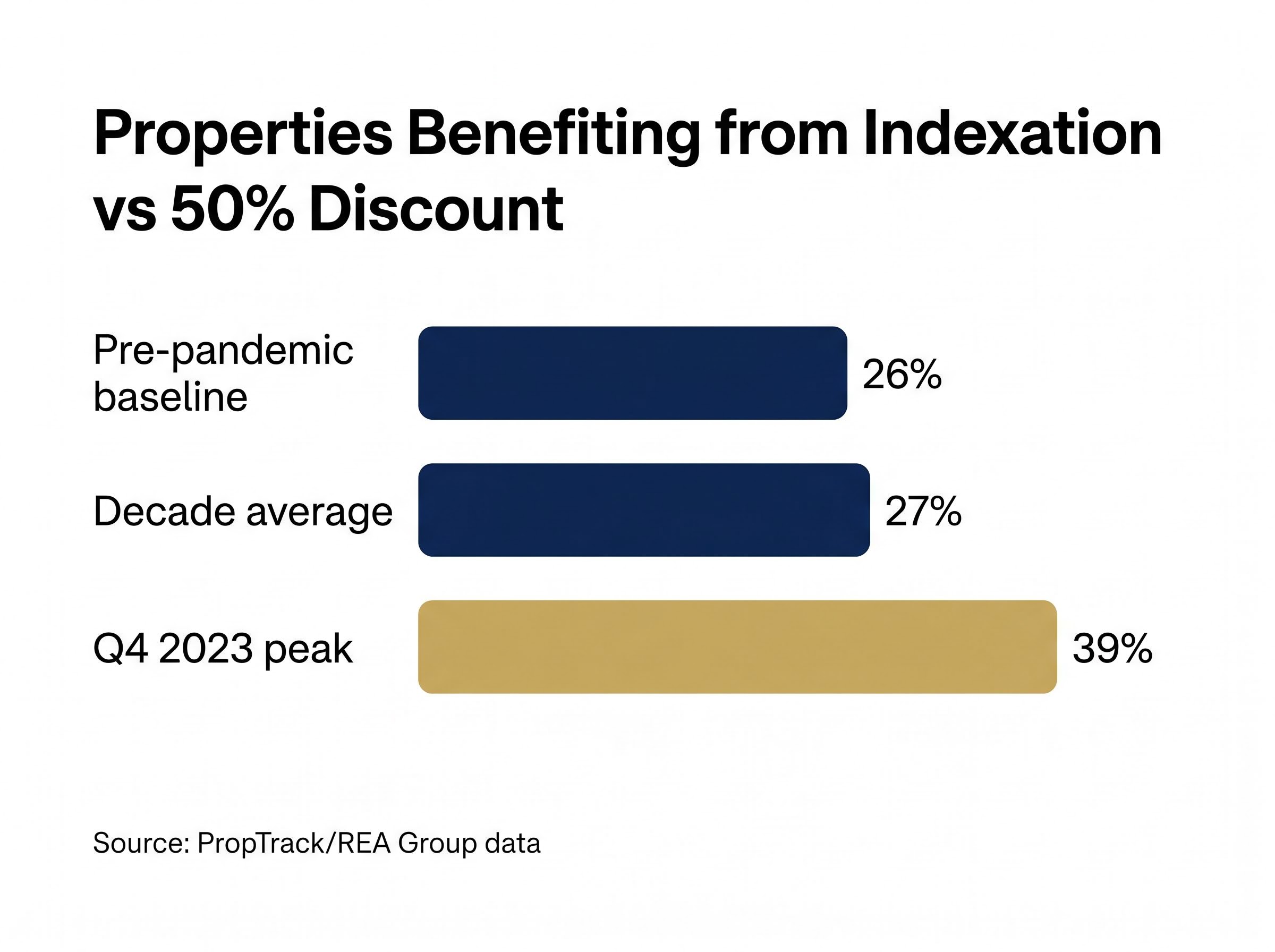

PropTrack data shows that roughly one in four properties sold over the past decade would have produced a smaller tax bill under indexation than under the current 50% capital gains tax (CGT) discount. By Q4 2023, that proportion had climbed to 39%. The federal budget announced on 12 May 2026 just made that calculation permanent.

Australia’s 2026 budget confirmed that the 50% CGT discount for assets held beyond 12 months will be replaced by an indexation model from 1 July 2027. The shift returns the system to the principle abandoned in 1999: taxing only the real, inflation-adjusted gain rather than applying a flat cut to the nominal one. A new-build exemption carves out newly constructed dwellings from the revised treatment. What follows is the investor-level arithmetic of who actually comes out ahead under indexation, the geographic split across Sydney, Melbourne, and Brisbane, and the projected knock-on effects on prices, rents, and construction supply that economists are beginning to forecast.

Australia operated under an indexation-based CGT system until September 1999, when the Howard government replaced it with the 50% discount following the Ralph Review of Business Taxation. The rationale was administrative simplicity and investment stimulus, not a principled position on what portion of a gain should be taxed.

The two systems differ in a single, consequential way:

For 27 years, the flat discount meant that a property doubling in nominal value during a period of high inflation still attracted tax on half the headline gain, even if most of that gain simply reflected the falling purchasing power of the dollar. Treasury’s stated rationale for the reversal centres on restoring equity: removing the incentive to hold underproductive assets purely for the tax benefit and aligning the system with genuine economic gain.

The ATO’s 2026 budget CGT reform detail confirms that the indexation methodology applies only to gains accruing after 1 July 2027, with a 30% minimum tax rate applying to individuals, trusts, and partnerships, alongside the new-build exemption that preserves more favourable treatment for newly constructed dwellings.

The new-build exemption sits inside that logic. It is not designed to reduce investor appetite for residential property; it is designed to redirect it toward new construction.

For readers wanting to situate the CGT indexation change within the complete fiscal package, our full explainer on the three 2026 budget reform pillars covers the negative gearing ring-fence that took effect on 12 May 2026, the CGT discount replacement from 1 July 2027, and the 30% minimum tax on discretionary trust distributions from July 2028, including the grandfathering boundaries that separate each measure and the ASX developer stocks flagged as potential beneficiaries.

Under the incoming rules, the cost base is adjusted upward by CPI for the period the asset was held. Tax is then paid on the residual real gain at the investor’s marginal tax rate, or a 30% floor, whichever is greater.

One category of assets previously shielded from CGT entirely is now captured. Assets acquired before 1985, which were exempt under the prior framework, fall within the new system’s scope.

The relative tax burden under each system is not fixed. It is a function of two variables interacting: how long the asset was held, and the inflation environment during that holding period.

Consider the pattern that emerges from the data. According to PropTrack/REA Group, approximately 27% of properties sold over the last decade would have incurred less tax under indexation than under the 50% discount. That figure is a decade-wide average. It masks a sharp spike: by Q4 2023, roughly 12 months after Australian inflation reached its highest recent point, the proportion had climbed to 39%.

The PropTrack analysis of indexation vs discount outcomes published by REA Group provides the primary data source for the decade-wide 27% figure and the Q4 2023 peak of 39%, identifying the inflation spike of 2022-2024 as the dominant variable lifting that proportion above its long-run baseline.

Even in the low-inflation pre-pandemic years, the baseline was not negligible. Approximately 26% of investor property disposals would have yielded a lower taxable gain under indexation.

Grattan Institute’s Danielle Wood noted that indexation tends to favour shorter-term holders in low-inflation environments and long-term holders when inflation is high. The interaction of these two variables, not the policy label alone, determines who pays more.

The decision framework can be simplified into two scenarios:

| Holding Period | Inflation Environment | Lower Tax Bill Under |

|---|---|---|

| Short (under 5 years) | Low | 50% discount |

| Short (under 5 years) | High | Varies; closer to neutral |

| Long (10+ years) | Low | 50% discount (marginal) |

| Long (10+ years) | High | Indexation |

The implication for investors who bought during the low-inflation pre-pandemic years and plan to sell soon after 1 July 2027 is direct: most will fall outside the 27% who benefit.

Each city’s exposure to the CGT change is the product of its own capital growth trajectory over the past decade, not an arbitrary geographic split.

Sydney investment properties sold between 2016 and 2022 strongly favoured the 50% discount over indexation. The city’s outsized nominal capital growth during that cycle meant the flat discount removed more from the tax bill than an inflation adjustment would have. For most Sydney investors who realised gains in that window, indexation would have produced a higher taxable amount.

PropTrack data on Sydney sales from 2016 to 2022 showed a pronounced preference for the flat 50% discount, reflecting the scale of nominal price appreciation relative to inflation.

Melbourne broadly tracked Sydney through the mid-2010s, but a growing proportion of investor sales in recent years now produce a lower taxable outcome under indexation. Melbourne’s more subdued growth since 2018 means the gap between nominal gain and inflation-adjusted gain has narrowed, tilting the arithmetic.

Brisbane sits at the opposite end. Its strong recent capital growth trajectory means investors there are more likely to face a higher taxable gain under the new system, not less. Capital growth has outpaced inflation by a wide enough margin that the flat discount remains more generous.

| City | Capital Growth Character (Last Decade) | Likely CGT Outcome Under Indexation | Sensitivity to Reform |

|---|---|---|---|

| Sydney | Strong nominal growth, especially 2016-2022 | Higher tax for most investor sales in that period | High (large established investment stock) |

| Melbourne | Subdued post-2018; narrowing gap to inflation | Growing share of sales favour indexation | High (high-value established stock) |

| Brisbane | Strong recent growth, outpacing inflation | Higher tax under indexation for recent sellers | Moderate |

Post-budget analysis from CoreLogic, major bank research teams (CBA, Westpac, NAB, ANZ), and financial press coverage converges on the same point: Sydney and Melbourne are most sensitive to the reform due to their concentration of high-value established investment stock.

The retrospective arithmetic of existing portfolios is one side of the ledger. The other is where rational capital will now flow.

The new-build exemption is designed to redirect, not destroy, investor appetite. By maintaining the more favourable CGT treatment for newly constructed dwellings, the policy creates a structural tilt in the after-tax return of new versus established property.

The CGT indexation change is only one of three structural shifts announced on 12 May 2026; the negative gearing ring-fence that took effect immediately on budget night restricts loss offsets against other income for established investment properties acquired after that date, compounding the after-tax calculus for any investor building or restructuring a portfolio in the current window.

Institutional responses reflect this reading:

No post-12 May 2026 quantitative modelling of the exemption’s impact on dwelling commencements has been published by any institution. Neither the HIA nor the Property Council has released forecasts quantifying additional dwellings attributable to the exemption. Treasury’s budget papers explain the rationale but provide no publicly accessible pipeline modelling.

This absence is itself a meaningful data point. Investors cannot rely on scenario-specific numbers. Directional consensus, that the exemption favours new construction over established property, is the best available guide for acquisition decisions made before detailed modelling enters the public domain.

The direct tax arithmetic determines who pays more or less. The downstream market effects determine what happens to the assets themselves.

CoreLogic post-budget commentary described “modest downward pressure on investor demand” translating to “slight downward pressure on dwelling prices” and “mildly higher rents.”

That framing captures the consensus. PropTrack/REA Group reiterated that the CGT change is expected to have only a “modest” impact on prices, emphasising that supply constraints and interest rates remain the dominant drivers. Major bank economics teams (CBA, Westpac, NAB, ANZ) noted the CGT change as a secondary headwind for investor demand, particularly in Sydney and Melbourne.

The causal chain runs in sequence. Reduced investor participation in established property tightens rental supply. Tighter rental supply contributes to mildly higher rents than would otherwise be the case. On the construction side, a slight reduction in new dwelling starts is projected relative to the counterfactual of the 50% discount remaining, partially offset by the new-build exemption’s redirection of capital.

| Effect | Direction | Magnitude | Primary Driver |

|---|---|---|---|

| Dwelling prices | Slight downward pressure | Modest | Interest rates and supply constraints (CGT secondary) |

| Rents | Mild upward pressure | Modest | Reduced investor supply of established rentals |

| New construction | Slight reduction vs. counterfactual | Incremental | Construction costs and planning approvals (exemption partially offsets) |

No city-specific numerical forecasts attributable solely to the CGT change have been published by any institution since 12 May 2026. All commentary frames CGT as a secondary driver; interest rates, construction costs, and planning constraints remain dominant.

The PropTrack figures provide the clearest available anchor. Over the past decade, 27% of property sales would have incurred less tax under indexation. At the Q4 2023 peak, that figure was 39%. In the low-inflation pre-pandemic baseline, it was approximately 26%.

Three variables determine which side of that split an individual investor falls on: the length of the holding period, the inflation environment during that period, and the city where the asset is located.

Investors who hold assets today and plan to sell after 1 July 2027 face a more complex calculation than the current article’s winner-loser framework captures: the split-calculation grandfathering rules apply the 50% discount to gains accrued up to the transition date and the new indexation model only to gains accruing afterward, meaning the blended effective rate depends on when in the holding period most of the appreciation occurred.

Profiles more likely to benefit from indexation:

Profiles more likely to face a higher tax bill under indexation:

No public tool or post-budget modelling framework currently exists to run this calculation at scale. The most prudent action for any individual investor is to model their specific scenario under both systems before the 1 July 2027 transition date.

The directional consensus that the reform raises the tax burden for most property investors is clarified considerably by dollar-level cost modelling: projections show after-tax wealth reductions exceeding $50,000 for a leveraged property investor and more than $225,000 for a founder selling a $1 million business, figures that make the abstract arithmetic of the 27% question concrete for individual planning decisions.

The 1 July 2027 transition date gives investors a defined window to assess their position under both systems and make deliberate portfolio decisions before the rules change. That window is the only certainty the current evidence base offers.

No post-budget quantitative modelling exists for holding-period cohorts, city-specific price impacts, or construction pipeline uplift from the new-build exemption. The qualitative consensus is directional but unquantified.

The reform’s actual effect on housing affordability, rental supply, and new construction will ultimately depend on whether complementary state-level reforms, including upzoning, planning approval acceleration, and stamp duty restructuring, accompany the federal CGT change. The question the evidence cannot yet answer is whether the new-build exemption proves sufficient to redirect enough investor capital into new construction to meaningfully improve housing supply, or whether the dominant effect is simply reduced investor participation in the established market.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

From 1 July 2027, instead of halving the nominal capital gain, investors will have their cost base adjusted upward by CPI so that tax applies only to the real, inflation-adjusted gain, with a 30% minimum tax rate applying to individuals, trusts, and partnerships.

Your outcome depends on three variables: how long you held the asset, the inflation environment during that holding period, and the city where the property is located. Long-term holders who held through the 2022-2024 high-inflation period are most likely to benefit, while short-term holders in high-growth markets like Brisbane are more likely to face a higher tax bill.

PropTrack data shows approximately 27% of properties sold over the past decade would have incurred less tax under indexation, rising sharply to 39% by Q4 2023 when inflation was at its recent peak.

The new-build exemption maintains more favourable CGT treatment for newly constructed dwellings, creating a structural tilt in after-tax returns toward new construction over established property and aiming to redirect rather than reduce overall investor participation in residential property.

Post-budget commentary from CoreLogic and major bank research teams describes only modest downward pressure on dwelling prices and mildly higher rents, with Sydney and Melbourne considered most sensitive due to their concentration of high-value established investment stock, though interest rates and supply constraints remain the dominant market drivers.