Global small-cap equities are trading at a discount to their large-cap counterparts, and most Australian investors are looking the other way. Mega-cap technology, artificial intelligence infrastructure, and domestic recovery plays have dominated portfolio attention through the first half of 2026. Yet a rotation is building beneath the surface. NYSE market strategist Eric Criscuolo noted on 18 May 2026 that profitable small caps, as measured by the S&P 600, were outperforming the broader market, while the Russell 2000’s higher-risk cohort lagged. The signal is specific: quality is the filter that separates small-cap opportunity from small-cap noise. For Australian investors considering an ASX small cap ETF for global exposure, the question is whether this rotation has durability and how to access it without absorbing the lower-quality risk that has historically made broad small-cap allocations volatile. What follows is an examination of the valuation backdrop, the conditions that trigger small-cap leadership, the current evidence for a quality rotation, and how VanEck’s QSML ETF positions ASX investors within this theme.

Global small caps are cheap, but that alone is not the whole story

The discount is real. VanEck’s research publication from approximately 12 May 2026 identified global small-cap companies as trading at a discount relative to large-cap peers, a finding consistent with broader market commentary through early 2026.

“Global small-cap companies are trading at a discount relative to large-cap counterparts, and may be entering a period of relative outperformance.”

A precise, independently verified price-to-earnings or price-to-book spread figure was not available from current research. Investors seeking the latest ratio should consult MSCI or VanEck quarterly fact sheets for updated figures.

The more important point: a valuation discount is a necessary but not sufficient condition for outperformance. Small caps can stay cheap for extended periods when the macro conditions for a re-rating are absent. Australian investors saw this dynamic play out domestically when the S&P/ASX All Technology Index (XTX) fell nearly 30% between January and March 2026. Sharp repricing does not automatically produce a buy signal. It produces a question: what else needs to be true?

When big ASX news breaks, our subscribers know first

What actually triggers a small-cap outperformance cycle

Three conditions have historically preceded sustained periods of small-cap leadership, and they appear consistently across analyst and fund manager commentary from 2025-2026:

- Easing interest rates or falling yields. Smaller companies depend more heavily on external financing than large caps with strong internal cash flows, making the cost of debt an outsized driver of their earnings and valuations.

- Improving risk appetite and market breadth expansion. When more stocks participate in a rally rather than gains concentrating in a handful of mega-cap names, small caps tend to benefit disproportionately.

- Post-shock recoveries. When geopolitical or macroeconomic stress recedes, capital rotates away from defensive large-cap holdings and toward higher-beta, attractively valued names.

The rate sensitivity mechanism deserves particular attention. When refinancing costs are elevated, smaller companies face margin compression that large caps with balance-sheet buffers can absorb. The effect is asymmetric: rate cuts help small caps more than they help large caps, and rate persistence hurts them more.

Why quality matters more than size in this cycle

Not all small caps respond to these triggers equally. The distinction between quality-filtered and broad small-cap exposure has widened in 2026:

- S&P 600 constituents must meet profitability requirements, filtering out loss-making companies. This index was outperforming as at 18 May 2026.

- Russell 2000 constituents include unprofitable and heavily indebted names. This broader index lagged the S&P 600 by approximately 1% on the same date, per NYSE data.

- In uneven macro environments where not all three triggers are fully confirmed, quality screens have consistently separated outperformers from underperformers within the small-cap universe.

The private capital drain on small-cap indexes has compounded this dynamic structurally: nearly half of Russell 2000 constituents are currently unprofitable, up from roughly one in four before the Global Financial Crisis, as venture capital keeps the best growth companies private longer and private equity buyouts remove the highest-quality public names from the index entirely.

The checklist, then, is not simply “are small caps cheap?” It is: are rates easing, is breadth expanding, is geopolitical stress fading, and does the exposure target profitable companies? Australian investors should hold that framework as they assess the current evidence.

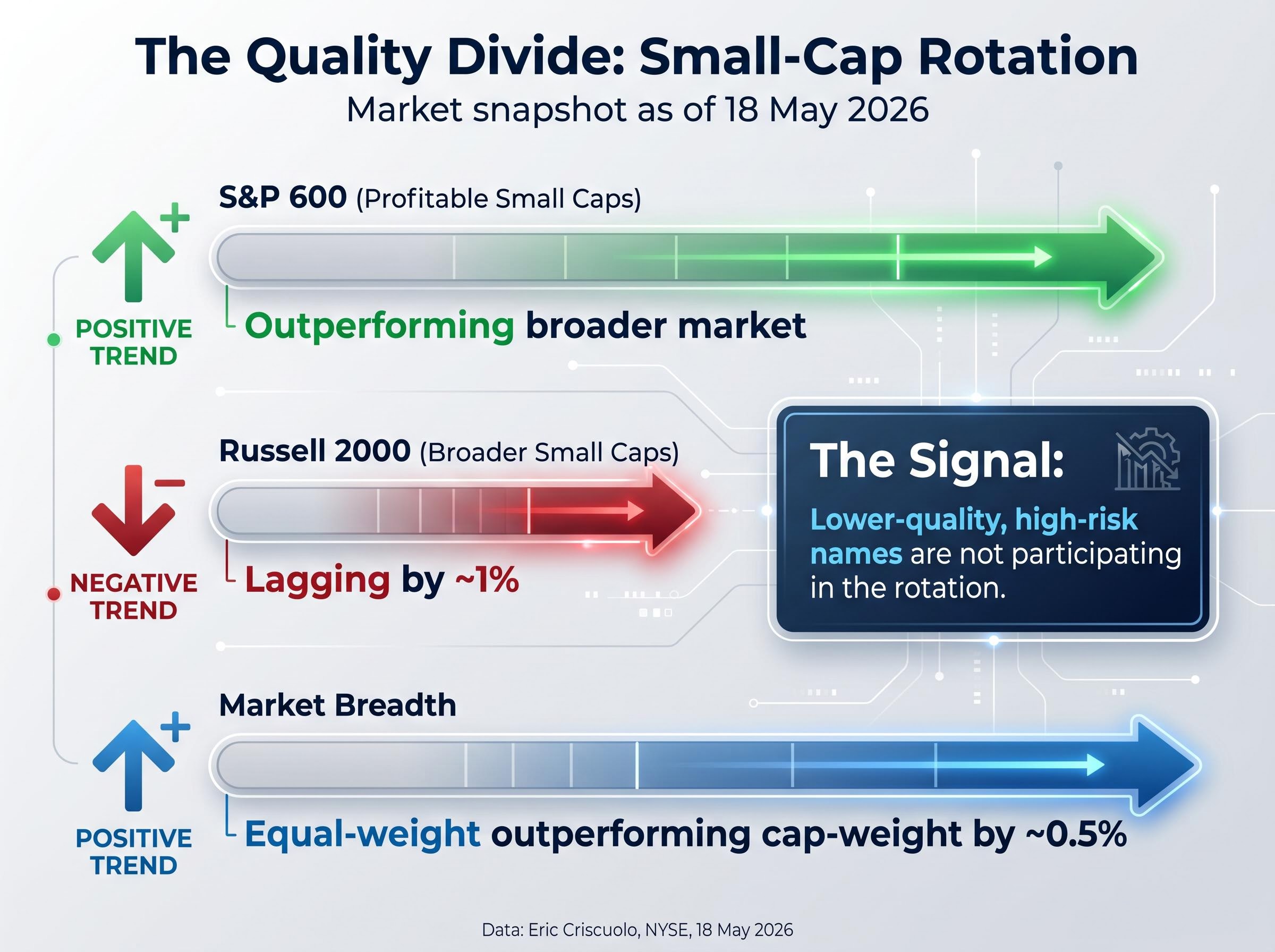

The current market evidence: rotation is underway but not yet confirmed

The most current, directly dated evidence comes from Eric Criscuolo at the NYSE on 18 May 2026. The picture is encouraging but uneven.

| Index / Measure | Performance Signal (18 May 2026) | What It Suggests |

|---|---|---|

| S&P 600 (profitable small caps) | Outperforming the broader market | Quality small caps are leading the rotation |

| Russell 2000 (broader small caps) | Lagging by approximately 1% | Lower-quality names are not participating |

| Equal-weight vs cap-weight | Equal-weight outperforming by approximately 0.5% | Breadth is expanding beneath the surface |

Criscuolo noted that AI-related weakness was masking improved underlying market breadth on the same session. Higher-risk segments, including neoclouds, data centres, crypto, and quantum, were being sold off while the broader market quietly broadened. The rotation is real, but it is selective.

VanEck’s view, published approximately 12 May 2026, adds a geopolitical layer: easing geopolitical tensions are redirecting investor attention from defensive large-cap holdings toward fundamentally sound, attractively priced companies. Morningstar’s markets commentary from 2026 reinforced that macro and geopolitical conditions, including the Iran-related rally in bitcoin, remained significant drivers of rotation behaviour in mid-2026.

Two of the three historical triggers (improving breadth and easing geopolitical sentiment) are showing evidence. The rate environment remains the open question.

Small-cap fund flows have shifted sharply in 2026, with the segment capturing approximately 25% of equity inflows compared with roughly 8% in 2025, accompanied by formal allocation recommendations from Goldman Sachs, Morgan Stanley, JPMorgan, and Bank of America calling for 10-15% portfolio shifts toward the category.

How QSML gives ASX investors access to quality international small caps

The thesis points toward quality small-cap exposure. QSML, listed on the ASX and managed by VanEck, is designed to deliver precisely that.

The fund’s key characteristics:

- Portfolio size: Approximately 150 international developed-market securities

- Selection criteria: Quality screen based on profitability and balance-sheet strength, not simply market capitalisation

- Geographic scope: International developed markets, providing diversification away from domestic ASX concentration

As at 14 May 2026, QSML held total net assets of $1.55 billion, a scale that signals meaningful market acceptance among Australian investors. The fund is accessible through standard brokerage accounts.

ASIC’s regulatory guide for exchange-traded products sets out the issuer obligations, portfolio disclosure requirements, and product design standards that govern ASX-listed ETFs, including the naming conventions and distribution obligations that apply to funds like QSML.

The quality screen is the feature that connects QSML to the rotation dynamic described above. Its profitability and balance-sheet criteria align the portfolio with the S&P 600-type segment of the small-cap universe, the segment that was outperforming as at 18 May 2026, rather than the broader Russell 2000-type exposure that lagged. For Australian investors who accept the directional thesis but want to avoid the lower-quality tail risk embedded in broad small-cap indices, the fund’s construction addresses that concern directly.

For investors unfamiliar with how quality screens work in practice, our full explainer on quality factor investing for ASX portfolios covers what high return on equity, stable earnings growth, and low financial leverage actually mean as selection criteria, including how QUAL and AQLT apply these screens and how quality-screened exposures differ from sector or market-cap approaches.

The risks that could delay or derail the small-cap thesis

The bull case has specific, dated evidence behind it. So do the counterarguments.

- USD strength and currency effects. For Australian investors in an unhedged global small-cap product, a stronger US dollar can erode AUD-denominated returns. This is an additional layer of return variance that does not feature in a domestic small-cap position.

- Liquidity risk. Small caps trade with thinner liquidity than large caps. In periods of market stress, this amplifies drawdowns and can make exits costly, a dynamic visible even on 18 May 2026 as higher-risk segments repriced sharply.

- Earnings vulnerability. Smaller companies face greater margin pressure from elevated refinancing costs and demand slowdowns than large-cap peers with stronger cash-flow buffers. If borrowing conditions remain tight, valuations can stay depressed despite an apparent discount.

- Rate sensitivity. The rate environment is the unconfirmed trigger. If central banks pause or reverse easing trajectories, the most rate-sensitive segment of the equity market, small caps, would bear the greatest cost.

The 18 May 2026 session illustrated this unevenness in real time. Neoclouds, data centres, crypto, and quantum names were sold off even as breadth improved elsewhere. Small caps are not a monolith, and the exit from higher-risk positions can be abrupt.

The quality factor in macro stress environments has a consistent historical pattern: in periods where consumer sentiment collapses while headline indices hold elevated levels, high-ROE, low-leverage companies have historically delivered relative outperformance by absorbing margin pressure that forces weaker-balance-sheet peers into distress.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

A valuation discount plus a quality filter: the case for watching this space closely

The investment case rests on a specific conjunction. Global small caps are trading at a directionally confirmed discount. A quality-filtered rotation is evidenced by dated May 2026 market data. And QSML’s design aligns with the precise segment of the small-cap universe that is leading rather than lagging.

The core thesis: a valuation discount becomes actionable when paired with a quality filter and supported by broadening market participation, and early evidence suggests those conditions are forming.

The investor profile for whom this thesis is most relevant: those with a medium-term horizon, an existing allocation to large-cap global equities, and an appetite for introducing quality small-cap exposure as a diversification layer. The $1.55 billion in net assets held by QSML suggests a meaningful cohort of Australian investors has already reached that conclusion.

Two of the three historical triggers for small-cap leadership, improving breadth and easing geopolitical sentiment, are present. The rate environment remains the outstanding variable. The rotation is early-stage, the conditions are partially but not fully confirmed, and the logical next step for interested investors is to review the most current VanEck QSML fact sheet for updated performance and flows data before acting.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.