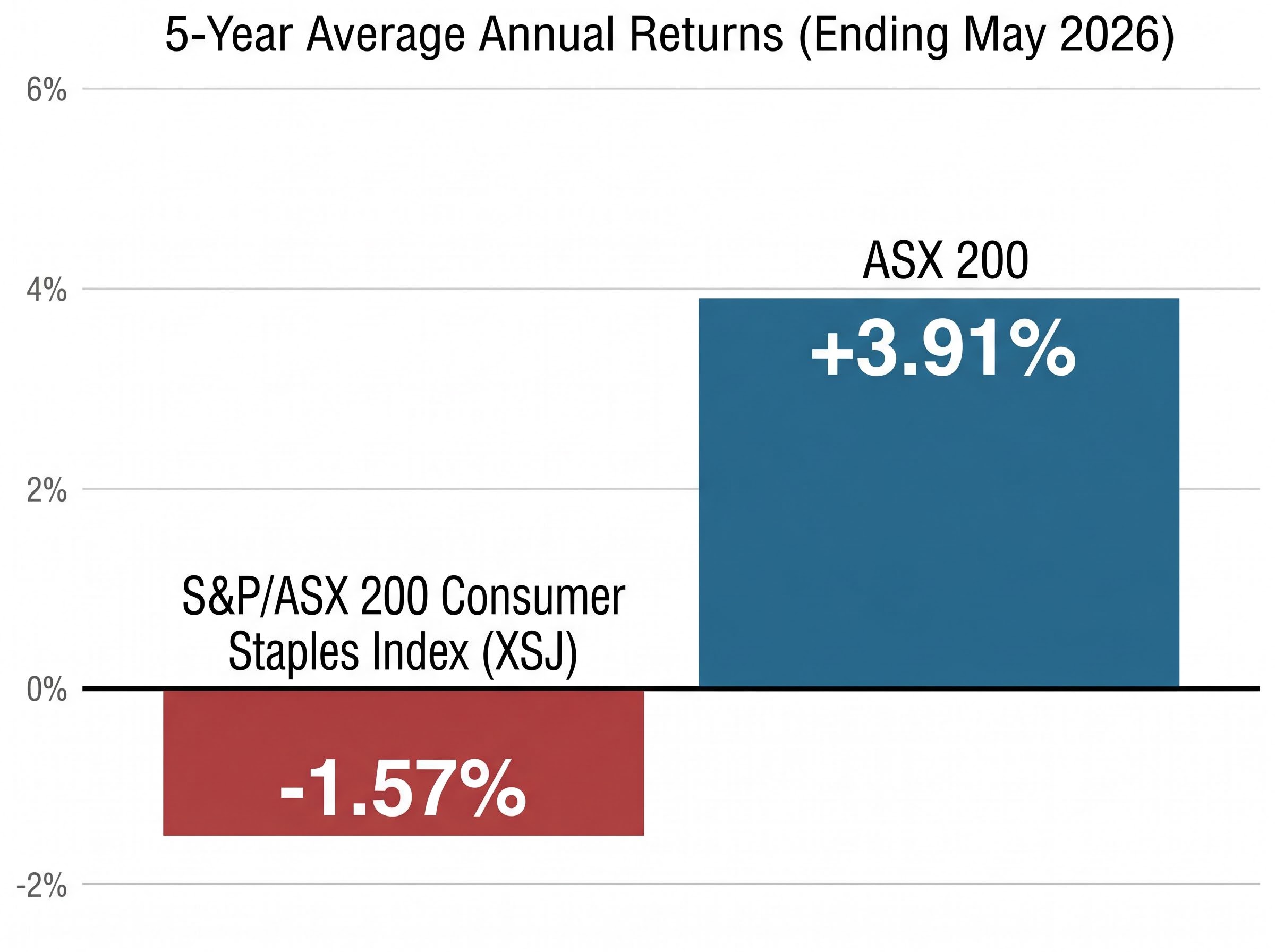

The S&P/ASX 200 Consumer Staples Index returned an average of -1.57% per year over the five years ending May 2026. Over the same period, the broader ASX 200 returned 3.91% annually. Investors who allocated to consumer staples for capital protection did not avoid losses; they locked them in.

That performance gap demands explanation, not dismissal. Rising interest rates, regulatory pressure on Australia’s supermarket duopoly, and elevated starting valuations have converged to challenge the assumption that consumer staples reliably protect capital. Australian investors are now reconsidering sector allocation decisions that were, until recently, treated as settled.

What follows is an evidence-based assessment of what consumer staples on the ASX actually deliver, and what they do not. The objective is a clear framework for deciding whether this sector belongs in a portfolio, and on what terms, so the allocation decision rests on data rather than a label.

What the five-year return gap between consumer staples and the ASX 200 actually tells us

The numbers set up the question the rest of this analysis addresses. Before interpreting them, it is worth anchoring them precisely.

- S&P/ASX 200 Consumer Staples Index (XSJ) five-year average annual return: -1.57%

- ASX 200 five-year average annual return: 3.91%

- XSJ one-year return as of mid-May 2026: approximately -7.82%

- XSJ 2025 full-year return: 1.43%, ranked 8th of 11 ASX sectors

-1.57% per year vs. 3.91% per year over five years. That is the gap investors need to explain before they can decide what to do about it.

Reading the numbers without over-reading them

The index return includes price movements but excludes the effect of franking credits, which matter for Australian resident investors in taxable accounts. Ignoring that benefit overstates the underperformance, though not by enough to close the gap.

More importantly, the underperformance is a statement about capital growth, not about the sector’s ability to deliver stable earnings through a downturn. Consumer staples did not fail at being defensive. They failed at being a capital growth vehicle. Those are two different things, and the distinction shapes every section that follows.

Return dispersion within the XSJ is substantial: Ridley Corporation and Inghams Group have produced materially different risk and income profiles from the index-heavy Woolworths and Coles positions, a point that matters for investors who want consumer staples exposure without concentrating entirely in the supermarket duopoly.

When big ASX news breaks, our subscribers know first

The genuine defensive qualities consumer staples do offer ASX investors

The five-year return gap is real, but so is the sector’s defensive character. The distinction is where that defence operates: at the earnings level rather than the share-price level.

Four qualities underpin the defensive case:

- Earnings stability: Demand for food, beverages, and household essentials does not collapse during recessions the way discretionary spending does. Revenue declines in prior downturns have been modest relative to cyclical sectors.

- Recession resilience: Grocery volumes held up through the cost-of-living pressures of 2023-2025 even as consumer sentiment deteriorated, reflecting the non-discretionary nature of the spend.

- Pricing power: Woolworths (approximately 38% grocery market share) and Coles (approximately 29%) function as price setters in a concentrated market. That position supports margin maintenance during inflationary periods, even when it draws regulatory attention.

- Portfolio diversification: The sector’s low correlation with cyclical sectors can reduce overall portfolio volatility, a benefit that pays off during market dislocations rather than during extended growth cycles.

Woolworths and Coles together control roughly two-thirds of the Australian grocery market. That concentration is the source of both their pricing power and their regulatory risk.

Woolworths currently offers a dividend yield of approximately 4.37% as of May 2026, well above its five-year average of 2.92% annually. That elevated yield reflects genuine income generation, but also a share price that has declined, a point the valuation section below addresses directly.

The sector’s defensive value is real. It is simply more visible during downturns than during the kind of extended growth cycle that characterised the past five years.

Why consumer staples underperform in bull markets, and what drives the current cycle’s headwinds

The underperformance of the past five years is not a sector anomaly. It is the predictable structural outcome of how defensive stocks behave when growth is rewarded and rates are elevated.

| Headwind | How it affects the sector | Current status as of May 2026 |

|---|---|---|

| Rising bond yields | Higher yields on term deposits and government bonds make low-growth defensives less attractive as income alternatives | Rates remain higher for longer; competition from fixed income persists |

| Valuation compression | Elevated multiples at cycle entry leave the sector exposed to de-rating as rates stay high | Post-COVID premium has partially unwound but sector still trades at modest premium to long-run averages |

| Margin pressure | Cost inflation eases slowly while price-sensitive consumers limit the ability to expand margins | Input costs moderating but consumer caution and competitive intensity persist |

| Weak volume growth | Subdued volumes cap earnings upside even where pricing has been partially maintained | Volume growth remains below trend across the sector |

In any bull market, capital rotates toward sectors offering earnings acceleration. Consumer staples, by definition, do not offer that. Their earnings grow slowly and predictably, which is a feature in a downturn and a drag in a growth cycle. That structural dynamic is permanent, not fixable.

The cycle-specific headwinds that amplified structural underperformance

What made 2021-2026 harder than a typical bull cycle for the sector was the convergence of three amplifiers. First, the speed of the Reserve Bank of Australia’s rate-rise cycle compressed the timeline for valuation de-rating. Second, starting valuations were elevated after COVID-era demand for perceived safety pushed defensive multiples to unusual premiums. Third, the ACCC’s supermarket inquiry introduced a regulatory overhang that had no precedent in prior cycles. The one-year XSJ return of -7.82% as of mid-May 2026 confirms these headwinds have not yet fully resolved.

Franking credits, dividends, and the real income case for consumer staples

The income case for consumer staples is stronger than headline yield figures suggest, once franking credits enter the calculation. For Australian resident investors in taxable accounts, a fully franked dividend carries a franking credit that offsets personal income tax payable on the dividend. The effect is a higher after-tax yield relative to an equivalent unfranked payment or an interest payment from a term deposit.

The ATO imputation rules govern exactly how franking credits offset personal income tax payable on dividends, and the mechanics matter: a fully franked dividend from Woolworths or Coles carries a credit equal to the corporate tax already paid, which investors on marginal rates above 30% can use to reduce their overall tax bill rather than simply receiving a gross-up.

| Income source | Indicative yield | Franking credit benefit | Net advantage consideration |

|---|---|---|---|

| Consumer staples large-cap (e.g. WOW) | Approximately 4.37% | Fully franked; tax credit reduces personal tax payable | After-tax yield materially higher than headline for investors on marginal tax rates above corporate rate |

| Term deposit (major bank, 12-month) | Approximately 4.0-4.5% | None; interest taxed at marginal rate | Competitive on headline yield but lower after-tax return for most investors |

| Australian government bond (5-year) | Approximately 3.5-4.0% | None; coupon taxed at marginal rate | Lower headline and after-tax yield, but capital preservation stronger |

Woolworths’ current dividend yield of approximately 4.37% sits well above its five-year average of 2.92%. That gap partly reflects price appreciation of 12.1% from the start of 2025 through May 2026 lagging the yield’s expansion, meaning the elevated yield is partly a function of the share price decline that preceded the recent recovery.

A yield meaningfully above a stock’s historical average warrants deeper valuation analysis, not automatic excitement. It may signal opportunity, or it may signal that the market is pricing in lower future earnings or higher risk.

According to J.P. Morgan’s Guide to the Markets (Australia, March 2026), the appeal of franked dividends relative to fixed income remains mixed in the current rate environment. The franking advantage does not disappear when term deposit rates are elevated, but it narrows. Investors should compare on an after-tax basis, not a headline basis.

Regulatory risk and the ACCC overhang: what investors in Woolworths and Coles need to price in

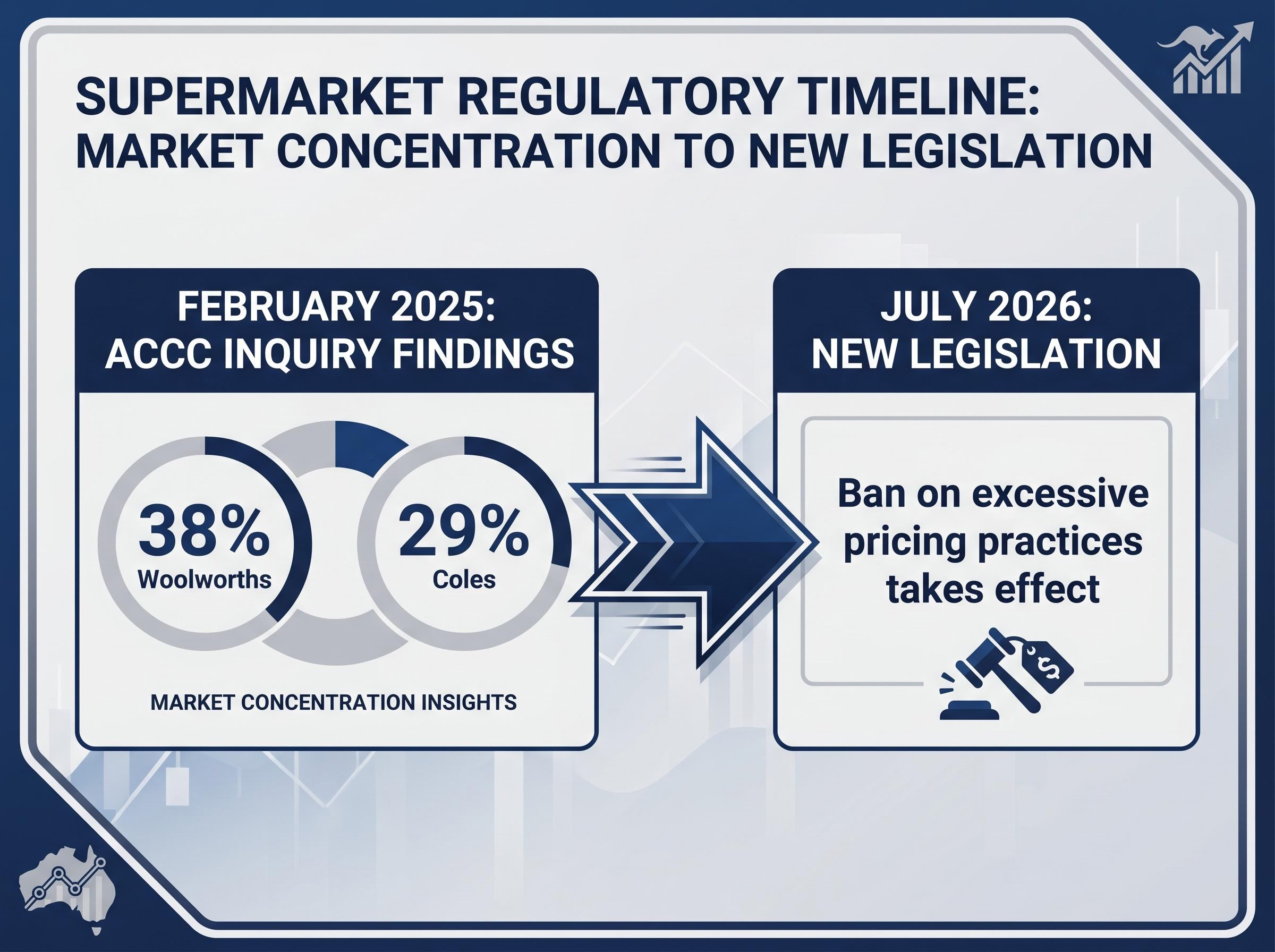

The ACCC’s supermarket inquiry introduced a structural variable into the consumer staples investment calculus that was largely absent from pre-2025 analysis. The regulatory timeline has moved through three stages:

- ACCC inquiry and findings (February 2025): The final report highlighted the duopoly’s combined market concentration (Woolworths at approximately 38%, Coles at approximately 29%) and recommended reforms targeting price transparency, supplier negotiation practices, and competitive conduct.

- Legislative response: Following the report, legislation banning excessive pricing practices was enacted, with the new laws effective from July 2026.

- Ongoing enforcement and compliance risk: Enforcement focus on pricing conduct and supplier relationships continues, with the political sensitivity of food inflation sustaining regulatory attention.

The Coles pricing conduct ruling handed down by the Federal Court in May 2026 illustrates the enforcement dimension the ACCC inquiry set in motion: while all 245 price increases examined were found to be commercially justifiable, a separate finding on promotional timing has left civil penalty exposure unresolved and reinforced the view that regulatory attention on the duopoly is structural rather than episodic.

The investment implication is not that earnings will be immediately reduced. It is that the risk profile of the sector’s two largest constituents has shifted.

What ongoing enforcement means for Woolworths and Coles shareholders

Behavioural compliance costs and changes to supplier relationship practices represent potential margin drag that may not appear in near-term earnings but could accumulate over time. Reputational exposure adds a further dimension: political sensitivity around grocery prices means regulatory attention is structurally embedded in the Australian market, not a response to a single event that will pass. Investors who price consumer staples as a low-risk holding without accounting for this overhang may be underestimating the sector’s actual risk profile.

The next major ASX story will hit our subscribers first

How to use consumer staples in an ASX portfolio: the practical allocation question

The analysis above points to a clear reframing. Consumer staples are a risk-management tool, not a return strategy, and the allocation question is whether an investor’s specific objective justifies the sector at current prices.

“Consumer staples are a risk-management tool, not a return strategy.” The five-year return gap of -1.57% versus 3.91% makes that distinction unavoidable.

The sector suits some investor profiles more than others:

- Income-focused investors in taxable accounts benefit from franking credits and relatively stable dividend streams.

- Tax-aware retirees or those near retirement may value the after-tax yield advantage over fixed income alternatives.

- Volatility-sensitive investors can use the sector’s low cyclical correlation to reduce portfolio-level drawdowns during market dislocations.

- Growth-oriented investors with long time horizons are likely to find the capital return profile unsatisfying relative to other ASX sectors.

- Capital appreciation seekers should recognise that the sector’s structural earnings stability limits the upside during growth cycles.

The diversification benefit is genuine, but it only delivers value when cyclical sectors are under stress. During sustained growth periods, the allocation acts as a drag on total returns.

Sector allocation within ETF portfolios raises a related structural question: a cap-weighted domestic ETF already concentrates nearly half of local equity exposure in banks and miners before any active decision is made, meaning investors who add explicit consumer staples exposure should account for the weight the sector already carries in their broad-market holdings.

Getting the entry price right matters even with defensive stocks

Woolworths’ current yield of 4.37% versus its five-year average of 2.92% illustrates a valuation signal, not a buy signal. A yield meaningfully above historical norms may reflect opportunity, or it may reflect the market pricing in lower future earnings growth or elevated risk. Discounted cash flow (DCF) or Dividend Discount Model approaches provide more rigorous entry-point discipline than headline yield screening alone. A sector with genuine defensive qualities is not a sound investment at any price; starting valuation relative to earnings growth prospects determines whether the risk-adjusted return justifies the allocation.

For investors wanting to apply the DCF and dividend discount discipline the current article recommends before acting on Woolworths’ elevated yield, our deep-dive into Woolworths’ current valuation metrics examines the 1.9% return on equity, the 300% debt-to-equity ratio, forward broker consensus targets, and what the stock’s position within its 52-week range implies for risk-adjusted entry points.

The “defensive” label has an expiry date, and ASX investors should read it carefully

Consumer staples earn their defensive label through earnings resilience, not through capital protection. That distinction has defined the sector’s five-year performance and should define how investors use it going forward.

The conditions under which the sector’s defensive value becomes most visible (recessions, earnings downturns, broad market dislocations) will return. They always do. When they arrive, the earnings stability of Woolworths, Coles, and their peers will matter in a way it has not over the past five years.

Until then, the practical question is straightforward. Before adding consumer staples exposure, investors should clarify whether their objective is income and volatility reduction, a genuine use case supported by the evidence, or capital protection in the short run, which is a misapplication of what the sector delivers.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.