What Nvidia’s $100 Billion per Gigawatt Figure Actually Means

45 mins ago

SpaceX is targeting a June 12, 2026 listing under the ticker SPCX, and the public S-1 prospectus is expected to land on SEC EDGAR as early as this week. If the offering prices within its reported target range of $1.75 trillion to $2 trillion, it would represent the largest IPO in recorded history. Yet as of 18 May 2026, not a single verified revenue figure, profitability metric, or governance disclosure exists in the public domain. Everything changes when the prospectus drops. This guide walks U.S. retail investors through what to look for in the S-1, how to evaluate a valuation step-up of this magnitude, what comparable mega-IPOs reveal about the risks ahead, and how to think about participation before the roadshow launches.

The gap between what the market believes about SpaceX and what has been officially disclosed is, at this moment, enormous. Secondary market transactions, media valuations, and analyst speculation have all circulated freely for months. None of them carry the legal weight of a public prospectus.

SpaceX confidentially submitted a draft registration statement to the SEC on 1 April 2026, as confirmed by Bloomberg, CNBC, and Reuters. A confidential filing under the JOBS Act allows a company to begin the regulatory review process without making its financials public. It is not a prospectus. It discloses nothing to retail investors.

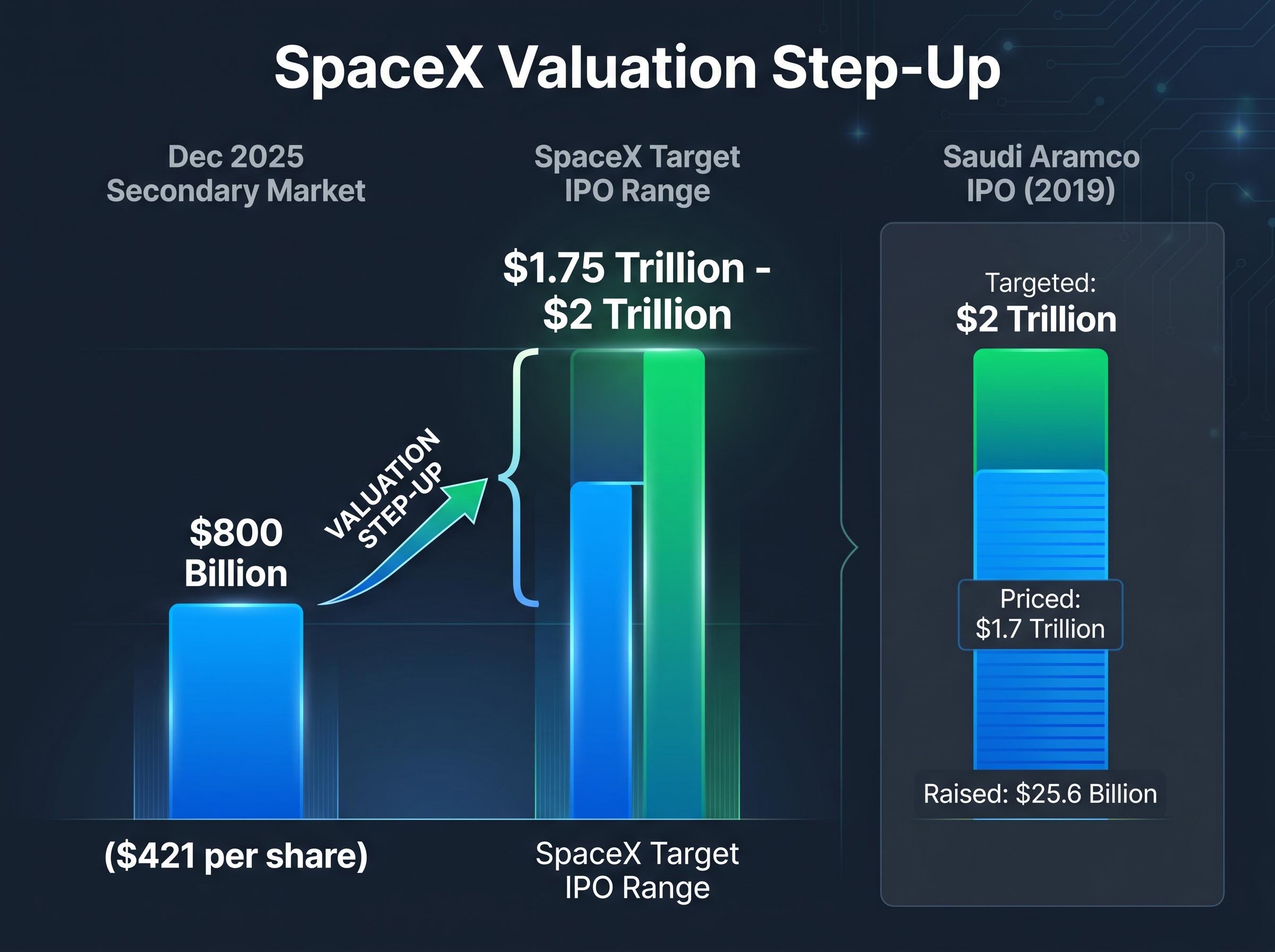

The public S-1, expected on EDGAR during the week of 20-22 May 2026, will be the first document to contain verified financial and structural data. Until it arrives, the last hard price anchor is the December 2025 secondary market transaction, which valued SpaceX at $800 billion ($421 per share).

The following categories of disclosure remain unavailable and will only appear in the public S-1:

SpaceX confidentially filed with the SEC on 1 April 2026. The public S-1 is expected by the week of 20 May 2026, with a proposed listing date of 12 June 2026 under the ticker SPCX.

| Date | Event |

|---|---|

| 1 April 2026 | Confidential draft registration statement submitted to the SEC |

| Week of 20-22 May 2026 | Public S-1 expected on SEC EDGAR |

| Early June 2026 | Roadshow launch and IPO pricing targeted |

| 12 June 2026 | Proposed listing date under ticker SPCX |

Retail investors who act on valuation claims circulating before the S-1 lands are making decisions without the data the company is legally required to disclose. Reading the prospectus critically is the single most protective step available.

The weight placed on the SpaceX S-1 is partly a function of the current SEC disclosure regime, where confidential draft filings under the JOBS Act allow companies to complete much of the regulatory review process before a single verified figure reaches the public; a proposed rule change moving eligible companies from quarterly to semiannual reporting would extend that information gap further for listed companies.

The last verified transaction valued SpaceX at $800 billion. The IPO is targeting $1.75 trillion to $2 trillion or above. That is a step-up of more than 100% from the most recent secondary market price, and it would occur within roughly six months.

Some of that premium reflects structural factors. Public market listings create liquidity that private secondary transactions cannot. Institutional demand for direct exposure to the space economy has few alternative outlets. SpaceX combines a reusable launch business, a defence and government contracting portfolio, and Starlink, a satellite broadband network with an undisclosed but reportedly large subscriber base. Scarcity alone may support a material premium.

The question is how much. Without disclosed revenue, earnings, or subscriber metrics, standard valuation approaches (price-to-earnings, enterprise-value-to-revenue) cannot be applied with any precision. That methodological gap is where institutional investors and retail investors diverge. Institutions will negotiate pricing during the bookbuilding process with access to management presentations. Retail investors, in most cases, will not.

EBITDA multiples at this valuation, reported at approximately 250x on current estimates, price in decades of compounding growth at rates that have no clear precedent in comparable infrastructure or technology businesses, a compression risk that compounds when the discount rate environment is already elevated.

| Valuation Reference Point | Amount | Context |

|---|---|---|

| December 2025 secondary transaction | $800 billion | Last verified private market price ($421/share) |

| IPO targeting range | $1.75-$2 trillion+ | Reported target; not yet confirmed in a public filing |

| Saudi Aramco IPO (2019) | $1.7 trillion | Targeted $2 trillion; institutional resistance forced pricing lower; raised ~$25.6 billion |

The Saudi Aramco precedent is instructive. Aramco targeted a $2 trillion valuation. Institutional investors pushed back, and the offering ultimately priced at $1.7 trillion, raising approximately $25.6 billion. Valuation targets and final pricing are not the same thing.

Saudi Aramco’s final IPO pricing landed at $1.7 trillion after global institutional investors pushed back firmly against the $2 trillion target, a pattern that underscores how reported valuation ambitions and actual bookbuilding outcomes can diverge significantly in even the most anticipated offerings.

Goldman Sachs noted in its 2026 outlook that “hot valuations may increase market volatility” in a broadly supportive but rate-sensitive growth environment.

Morgan Stanley’s 2026 outlook projects government bond yields remaining range-bound with a potential mid-year rally before drifting higher. For a high-multiple IPO entering the market in June, that yield trajectory is directly relevant to how aggressively the offering can be priced.

The S-1 prospectus for a company of this scale will likely exceed 200 pages. Most of it is legal boilerplate. Five sections contain the information that will determine whether the valuation is supportable and what risks are attached to participation.

Many technology companies list with dual-class share structures. In a typical arrangement, Class A shares (sold to the public) carry one vote per share, while Class B shares (held by founders or insiders) carry ten or more votes per share. The result is that a founder can retain majority voting control while holding a minority economic stake.

The specifics of Musk’s ownership percentage and voting rights have not been disclosed and will only be confirmed in the public S-1. What matters for a retail investor buying SPCX shares is the distinction between economic interest, meaning the right to share in the company’s profits and value appreciation, and voting control, meaning the power to approve or block corporate decisions. A dual-class structure can grant full economic participation while limiting shareholder influence over governance.

The Alibaba IPO in 2014 demonstrated that governance complexity does not preclude massive institutional demand. However, the variable interest entity (VIE) structure and governance concentration did define the limits of public shareholder power in practice.

Risk analysis is not a reason to avoid an investment. It is the work that separates informed participation from buying based on momentum. For an offering of this magnitude, the risk categories fall into two groups: company-specific and market-timing.

The U.S. 10-year Treasury yield was trading near a 15-month peak as of 18 May 2026. European and Asian sovereign yields sat at multi-year highs in the same period. S&P Global’s 2026 economic outlook noted that sovereign-debt concerns remain a risk even in a lower short-term-rate environment. For a high-multiple IPO with no publicly disclosed earnings, an elevated yield environment compresses the present value of future cash flows, which is precisely what investors are paying for at $2 trillion.

The U.S.-Iran conflict, approximately 80 days into a ceasefire as of 18 May, continues to create energy price uncertainty. That pressure feeds into the yield environment and broader equity market volatility, both of which affect how aggressively a growth IPO can be priced.

Broader technology sector positioning adds a layer of market-timing risk that sits above the company-specific factors: sell-side consensus forecasts for technology growth have climbed above independent industry estimates, global fund managers are at their most overweight US tech since before the 2021 peak, and at least one major institutional manager has moved underweight the sector, all of which shape the demand pool that will set final IPO pricing.

| Risk Category | Specific Exposure | Why It Matters | What to Watch in the S-1 |

|---|---|---|---|

| Regulatory | FCC licensing, export controls | Operations depend on government approvals that can be delayed or revoked | Disclosed regulatory dependencies and pending approvals |

| Governance | Musk voting control concentration | Public shareholders may have limited influence over corporate decisions | Dual-class structure details and insider voting percentages |

| Contract concentration | NASA, DoD revenue dependency | Government contract cycles and budget priorities create revenue volatility | Revenue breakdown by customer and contract renewal timelines |

| Macro rate sensitivity | Elevated Treasury yields | High-multiple valuations compress when discount rates rise | Growth rate assumptions and capital expenditure requirements |

The U.S. 10-year Treasury yield was trading near a 15-month peak as of 18 May 2026, a directly challenging environment for high-multiple, pre-revenue-disclosed IPOs.

IPO share allocation favours institutional investors by design. In a heavily oversubscribed offering, and an IPO of this profile is expected to be massively oversubscribed, institutional buyers typically receive the vast majority of shares. Retail investors who submit indications of interest through participating brokerages often receive a fraction of what they request, or nothing at all.

As of 18 May 2026, no public information is available on which brokerages will participate as distribution partners, what allocation minimums will apply, or whether any dedicated retail access mechanism will be offered. These details are expected in early June 2026 alongside the roadshow launch and underwriter announcements.

The Saudi Aramco IPO in 2019 offers a useful reference: heavy retail and domestic investor participation was a deliberate structural decision by the issuer and its advisers. Retail access is a design choice, not a default feature of every large offering.

Investors can begin preparing now. The following steps can be completed before the roadshow launches:

Investors who want step-by-step guidance on the brokerage account requirements, indication of interest process, and timing windows will find our comprehensive walkthrough of SpaceX IPO retail access, which covers E*TRADE as the confirmed retail distribution channel, the June 8 roadshow timeline, and the alternative exposure routes available through ETFs and existing public holdings for those who cannot secure an allocation.

Three access pathways are likely to be available to retail investors:

The SpaceX IPO may well prove to be a generational investment opportunity. It may also prove to be a case where the hype cycle prices in more than the financials can support. The difference between those outcomes cannot be determined until the S-1 is public.

The discipline for evaluating this offering is straightforward:

The prospectus is expected on EDGAR beginning the week of 20 May 2026. That is the starting point for every informed decision that follows.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections and IPO valuations are subject to market conditions and various risk factors.

The S-1 is the public registration document SpaceX must file with the SEC before listing, and it will be the first source of verified financial data including revenue, profitability, Starlink subscriber counts, and governance structure. Until the S-1 is published on SEC EDGAR, no legally confirmed financial or structural information is available to retail investors.

SpaceX is targeting a listing date of June 12, 2026 under the ticker SPCX, with the public S-1 prospectus expected on SEC EDGAR during the week of May 20-22, 2026. The roadshow and IPO pricing are targeted for early June 2026.

Retail investors can attempt to access SPCX shares through participating brokerages such as Fidelity or Schwab once underwriters are announced, with allocation details expected in early June 2026 alongside the roadshow launch. Alternative pathways include buying SPCX shares on the secondary market after listing or gaining exposure through ETFs if the stock is added to space or technology-focused funds.

Saudi Aramco targeted a $2 trillion valuation for its 2019 IPO but ultimately priced at $1.7 trillion after institutional investors pushed back, raising approximately $25.6 billion. This precedent shows that reported valuation targets and final IPO pricing can diverge significantly, even in the most anticipated offerings.

The main risks include elevated U.S. Treasury yields near a 15-month peak that compress high-multiple valuations, governance concentration from a potential dual-class share structure limiting public shareholder influence, contract revenue dependency on NASA and the DoD, and regulatory exposure through FCC licensing and export controls. All of these risks will be detailed for the first time in the public S-1 prospectus.