How to Use the Price-to-Sales Ratio Without Getting It Wrong

16 mins ago

In the week of 18 May 2026, global bond yields surged to levels not seen in nearly two decades. Gold retreated from multi-month highs. Base metals across the London Metal Exchange sold off in unison. ASX resources stocks followed. The connection between rising bond yields and falling commodity prices is not immediately obvious to most retail investors, but it is mechanical, repeatable, and worth understanding. This article explains the two distinct channels through which higher yields pressure commodities and commodity-linked equities, uses the mid-May 2026 selloff as a live case study, and provides a framework for evaluating resources exposure when the interest rate environment shifts.

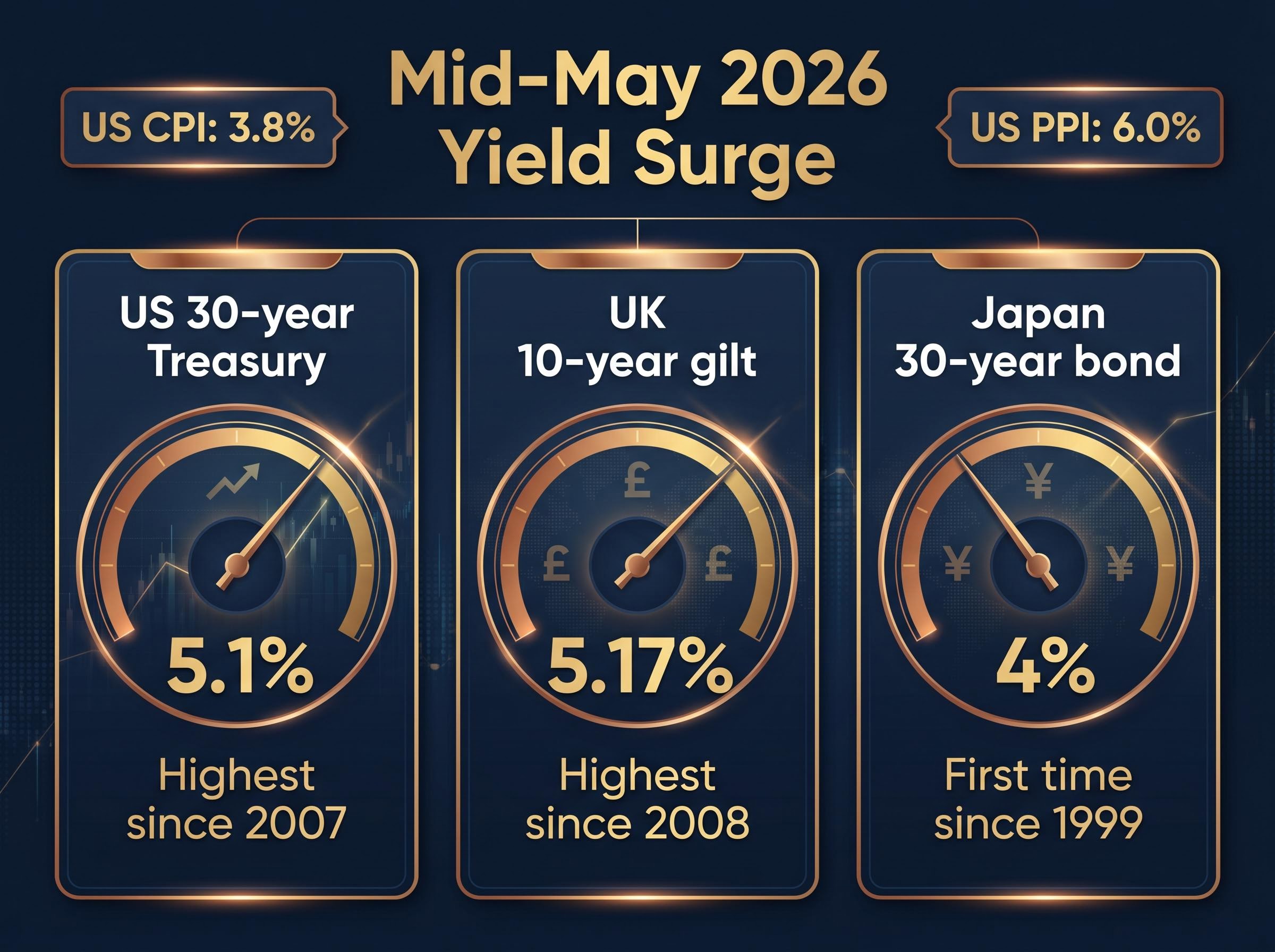

The week began with a jolt. Hotter-than-expected US inflation data for April, with the Consumer Price Index (CPI) running at 3.8% annually and the Producer Price Index (PPI) at 6.0% annually, forced a rapid repricing across global sovereign debt markets. Sustained energy price pressure from the ongoing Middle East conflict had fed directly into those inflation readings, and bond markets responded by demanding higher yields to compensate for the risk that central banks would need to keep rates elevated for longer.

The 3.8% CPI and 6.0% PPI readings that triggered the yield repricing were themselves the product of an oil-to-inflation transmission chain stretching back to the February 2026 US-Israeli strikes on Iran, with Brent crude surging above $111 per barrel and energy costs rising 3.8% in a single month, feeding directly into the headline inflation figures that bond markets then repriced.

The scale of the move was global and synchronised:

The RBA Financial Stability Review on global macro conditions documented how geopolitical pressures feeding into energy prices had contributed to elevated sovereign bond yields and tighter financial conditions across commodity markets, providing the Australian regulatory context for the yield dynamics playing out in mid-May 2026.

The US 30-year Treasury yield above 5.1% marked its highest level since 2007, a threshold that repriced the cost of capital across every asset class globally.

Within the same week, commodity markets moved sharply lower, and not because of any change in physical supply or demand for the metals themselves. Gold spot prices pulled back to an approximate range of US$4,500-4,704/oz, down from prior highs. LME copper traded in the range of approximately US$13,500-14,000/t, with COMEX copper futures extending their decline by approximately 0.9% in subsequent Asian trading sessions. Aluminium and nickel also declined across the complex, though verified figures for those metals remain subject to confirmation.

The pattern was the telling detail. Copper, gold, aluminium, and nickel are commodities with very different end-use profiles and supply dynamics, yet they all sold off in the same week. That simultaneity pointed to a shared macro driver rather than anything specific to individual metals markets.

Gold is structurally different from every other commodity in a rising-yield environment. Copper has industrial demand. Aluminium has construction and packaging end-markets. Gold produces no income: no dividends, no interest payments, no earnings yield. Its entire investment case rests on capital appreciation and its function as a hedge against inflation, currency debasement, or geopolitical risk.

That distinction becomes financially concrete when risk-free bond yields cross certain thresholds. When US 30-year Treasuries yielded near zero (as they did in parts of 2020-2021), the income sacrifice of holding gold instead of bonds was negligible. At 5.1%, that sacrifice amounts to a measurable annual cost.

When the US 30-year Treasury yields above 5%, holders of non-yielding assets face a measurable annual cost for the privilege of earning no income, a cost that did not exist when bonds yielded near zero.

Gold spot prices in mid-May 2026 traded in the approximate range of US$4,500-4,704/oz, reflecting this pressure alongside the broader selloff.

Silver futures dropped more than 4% and platinum also declined in the same period, underscoring that the yield-and-dollar pressure extended across the entire precious metals complex, with silver’s additional industrial demand exposure amplifying losses beyond what the opportunity-cost channel alone would predict.

Gold miners carry the same opportunity-cost headwind as physical gold, plus an additional valuation mechanism. Mining companies generate cash flows projected years and sometimes decades into the future. Those cash flows are valued using discounted cash flow (DCF) models, a standard method that calculates what future earnings are worth in today’s money by applying a discount rate.

When risk-free yields rise, that discount rate rises with them. A simple illustration from financial analysis: a $1 perpetuity (an annual payment that continues indefinitely) is worth approximately $50 when discounted at 2%, but only approximately $20 when discounted at 5%. The cash flow is identical; the rate at which it is discounted determines its present value.

For ASX-listed gold miners such as Newmont and Northern Star, this creates a compounded effect. The gold price itself faces headwinds from opportunity cost, and the miners’ equity valuations face an additional compression from higher discount rates applied to their long-duration cash flows. Investors holding gold ETFs such as GOLD (ETF Securities) or shares in gold producers face both layers simultaneously.

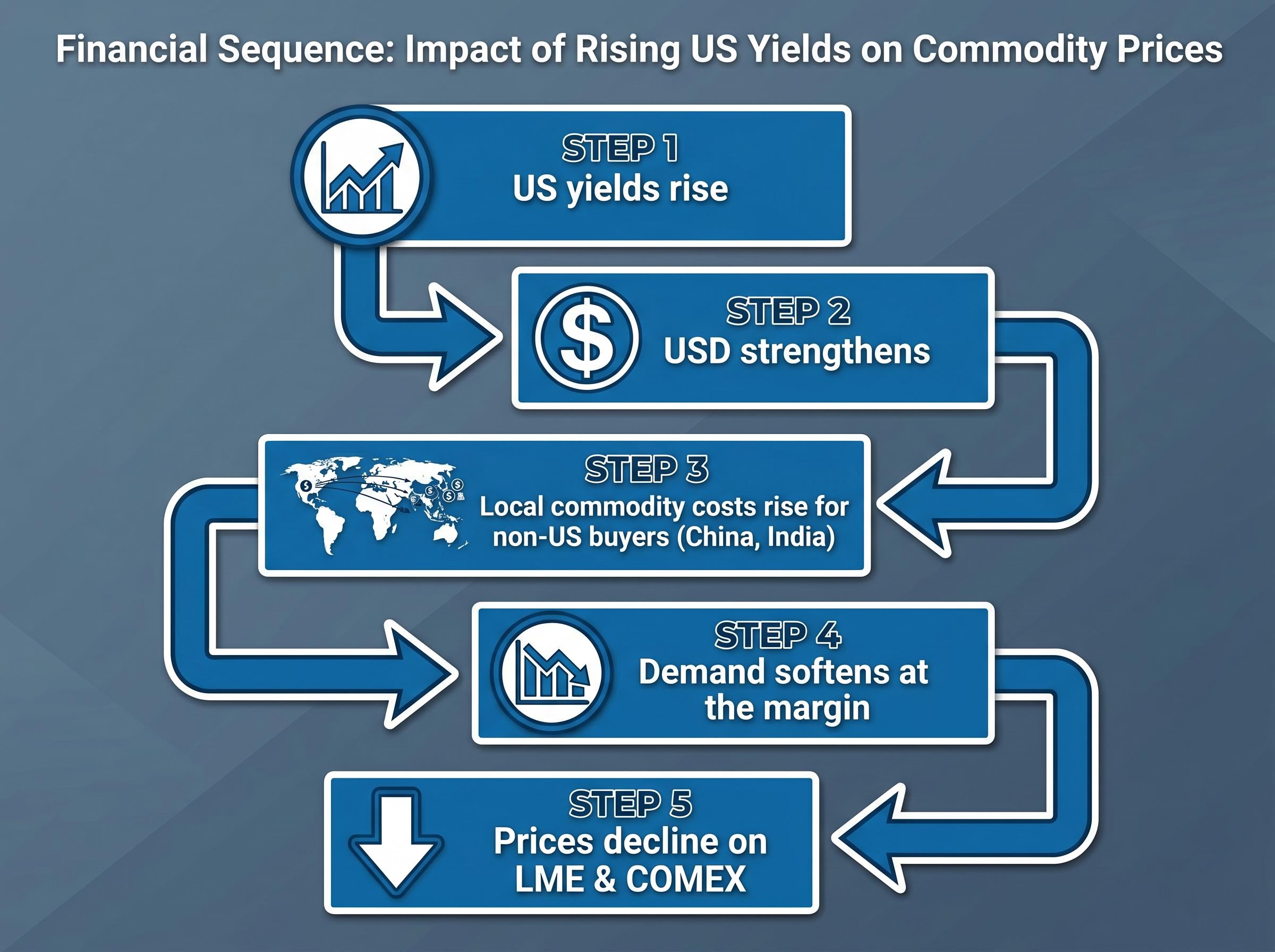

The transmission chain from bond yields to commodity prices runs through the currency market, and it works in a specific sequence.

The mechanism is a currency translation effect. Physical demand for copper or aluminium does not necessarily fall because a bond auction in Washington attracted more bids. But the effective cost to a copper buyer in Shanghai or a nickel importer in Mumbai rises when the dollar strengthens, and that introduces price resistance across USD-denominated commodity markets.

ANZ and Westpac analytical commentary has noted that a stronger US dollar “tightens financial conditions for non-US commodity buyers” and raises landed commodity costs for emerging-market importers. The mechanism applies most acutely to large commodity-importing economies such as China, whose purchase volumes are large enough to move global price benchmarks.

| Stage | What happens | Who is affected |

|---|---|---|

| US yields rise | Dollar-denominated assets attract global capital | Global fixed-income investors |

| USD strengthens | Exchange rates shift against non-US currencies | All non-US currency holders |

| Commodity costs rise in local currency | Import bills increase for the same volume of metals | Emerging-market commodity buyers (China, India) |

| Demand softens at the margin | Buyers defer or reduce purchases | LME and COMEX price benchmarks |

| Commodity prices decline | Global benchmarks adjust to reflect reduced buying | Producers, miners, commodity-linked equities |

For Australian investors, this mechanism carries a specific wrinkle. The majority of ASX-listed miners sell commodities priced in US dollars but report earnings in Australian dollars. When the USD strengthens sharply, the relationship between the headline commodity price and the miner’s AUD revenue becomes more complex, and analyst earnings models often require revision.

For base metals such as copper, aluminium, and nickel, the yield-related pressure operates through a different mix. These are industrial inputs with genuine physical demand from construction, manufacturing, and infrastructure spending. Their investment case does not rest on opportunity cost in the same way gold’s does. The primary pressure channel is the USD strengthening effect described earlier: a stronger dollar raises effective costs for the world’s largest commodity importers, softening demand at the margin and weighing on global benchmarks.

LME copper traded in the approximate range of US$13,500-14,000/t during mid-May 2026. Aluminium and nickel declined directionally across the week, though verified price levels for those metals remain subject to independent confirmation.

| Asset type | Primary yield pressure channel | Secondary pressure channel | ASX examples |

|---|---|---|---|

| Physical gold | Opportunity cost (zero income vs rising risk-free yields) | USD strength raising cost for non-US buyers | GOLD ETF (ETF Securities) |

| Gold miners | Opportunity cost + DCF discount rate compression | Gold price decline feeding through to revenue | Newmont, Northern Star |

| Base metals | USD strength softening demand from non-US buyers | Broader risk-off sentiment during bond volatility | LME copper, aluminium, nickel |

| Diversified miners | Commodity price softening from USD channel | DCF discount rate compression on equity valuations | BHP, Rio Tinto |

For ASX-listed diversified miners such as BHP and Rio Tinto, higher bond yields create pressure from two directions simultaneously. Softer commodity prices reduce the revenue line in analyst models. At the same time, the higher risk-free rate raises the discount rate applied in DCF valuations, compressing the present value of cash flows expected from long-life mining projects.

CommSec commentary has noted that the lift in risk-free rates lowers the present value of long-life mining projects, contributing to weakness in the S&P/ASX 200 Materials index. For diversified miners, the balance between the two pressures depends on where the actual commodity price sits; at verified copper levels of approximately US$13,500-14,000/t, the price-softening component may be less acute than the valuation compression component. Both, however, work in the same direction when yields are rising.

The question is not “sell commodities” or “hold.” It is a structured re-evaluation of why each commodity holding exists in a portfolio and whether that rationale remains intact when the yield environment shifts materially.

The evaluative framework starts with three questions for each holding:

The yield environment shift was not confined to US Treasuries; RBA rate repricing following Australia’s own 4.6% CPI reading had pushed the cash rate to 4.1% by April 2026, meaning Australian investors faced a double compression: rising global risk-free rates applying downward pressure on commodity valuations, and rising domestic rates making income-producing alternatives materially more competitive within their own portfolios.

According to the Australian Financial Review (March 2025), advisers reported clients “shifted from gold ETFs back into income-producing hybrids and bond funds” once yields on cash and short-duration fixed income exceeded 4-5%.

The 2024-2025 period offers direct precedent. BetaShares published model portfolio data showing gold exposure cut from approximately 10% to approximately 5% of total assets in response to higher yields, explicitly framing the decision around opportunity cost. Vanguard Australia noted in November 2024 that with bond yields “back near or above long-run averages,” the case for large tactical gold allocations as a diversifier had lessened in some cases.

These are 2024-2025 precedents, not May 2026-specific observations. But they demonstrate that Australian retail investors and advisers have already worked through this exact trade-off in recent years, and the framework they used remains directly applicable.

Government bond yields set the risk-free rate that underpins every other asset valuation. When that foundation shifts, all assets built on top of it must reprice, not because anything about those assets has changed but because the standard against which they are measured has moved.

The mid-May 2026 episode was notable for its speed and synchronicity. US CPI at 3.8% annually and PPI at 6.0% annually arrived hotter than expected, the US 30-year yield broke above 5.1% for the first time since 2007, the UK 10-year gilt reached its highest since 2008, and Japan’s 30-year bond hit 4% for the first time since those securities were first issued in 1999. Gold, copper, aluminium, and mining equities all moved lower in the same week.

The mechanism this episode illustrates is permanent. It will recur whenever bond markets reassess inflation expectations or monetary policy trajectories.

For investors wanting to place the May 2026 gold pullback within a longer historical valuation context, our dedicated guide to the Dow-to-gold ratio examines how the ratio’s current reading of approximately 10.5, roughly 30% below its 50-year average, compares with the extreme readings at the 1980 and 1999 secular turning points and how analysts use it alongside metrics such as the Buffett Indicator to assess whether equity or gold cycles are stretched.

Three durable principles worth retaining:

The two mechanisms, the USD-demand channel and the opportunity-cost channel, are not unique to May 2026. They operate every time the yield environment shifts materially. A portable framework for evaluating resources exposure at those moments involves four steps:

Resources exposure can still make sense in a higher-yield environment. But it requires a more active rationale than it did when bonds yielded near zero. The 2024-2025 precedent showed that investors who reviewed and adjusted positions deliberately, rather than reactively, were better positioned to articulate exactly why they owned what they owned. That deliberateness is the lasting lesson.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

—

Rising bond yields pressure commodity prices through two main channels: the opportunity cost channel, where non-yielding assets like gold become less attractive relative to income-paying bonds, and the USD strengthening channel, where higher US yields attract global capital into dollars, raising the effective cost of USD-denominated commodities for non-US buyers and softening demand.

Gold produces no income, so when the US 30-year Treasury yield rose above 5.1% in mid-May 2026, investors faced a measurable annual opportunity cost for holding gold instead of bonds, making income-producing alternatives more competitive and reducing demand for non-yielding assets like gold.

When higher US yields attract global capital and strengthen the dollar, commodity buyers in countries like China and India face higher local-currency costs for USD-denominated metals, which softens demand at the margin and pushes global benchmarks such as LME copper prices lower.

ASX gold miners face a compounded effect: the gold price itself faces headwinds from opportunity cost as yields rise, and the miners' equity valuations are further compressed because higher risk-free rates increase the discount rate applied to their long-duration future cash flows in DCF models, reducing their present value.

Investors should identify the role each holding plays (inflation hedge, growth, diversification), assess whether the opportunity cost has changed as income-producing alternatives become more competitive above 4-5% yields, check whether USD strength affects demand channels for that specific commodity, and verify whether any miner's equity thesis relies heavily on long-duration cash flows sensitive to discount-rate changes.